PV Function

The PV function calculates the present value of an investment (or a loan), assuming a constant interest rate. This is the amount that a series of future payments is currently worth. You can use PV with regular payments (such as a mortgage or other loan), periodic payments, or the future value of a lump sum paid now.

Syntax

PV(rate, nper, pmt, [fv], [type])

Arguments

Please see the Definitions section above for more a detailed description of these arguments.

|

Arguments

|

Description

|

|

Rate

|

Required. This is the interest rate per period.

|

|

Nper

|

Required. The total number of payment periods in an annuity i.e. the term.

|

|

Pmt

|

Required. This is the payment made for each period in the annuity.

If you omit pmt

, you must include the fv

argument.

|

|

Fv

|

Optional. This is the future value of an investment based on an assumed rate of growth.

If you omit fv, it is assumed to be 0 (zero), for example, the future value of a loan is 0. If you omit fv then you must include the pmt argument.

|

|

Type

|

Optional. This argument is 0 or 1 and indicates when payments are due.

0 or omitted = at the end of the period.

1 = at the beginning of the period.

|

Some points to take into consideration when using annuity functions:

- You always need to express the rate argument in the same units as the nper argument. For example, say you have monthly payments on a three-year loan at 5% annual interest. If you use 5%/12 for rate

, you must use 3*12 for nper

. If the payments on the same loan are being made annually, then you would use 5% for rate and 3 for nper.

- In annuity functions, the cash paid out (like a payment to savings) is represented by a negative number. The cash you receive (like a dividend payment) is represented by a positive number. For example, a $500 deposit to the bank would be represented by the argument -500 if you are the depositor, and by the argument 500 if you are the bank.

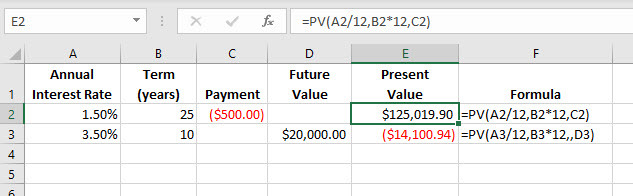

Example

In the example below, we use the PV formula to calculate:

- The present value of a $500 monthly payment over 25 years at a rate of 1.5% interest.

- The present value of the lump sum now needed to create $20,000 in 10 years at a rate of 3.5% interest.

Explanation of Formulas:

=PV(A2/12,B2*12,C2)

As you’ve probably noticed, the units for rate

and nper

have been kept consistent by specifying them in monthly terms, A2/12 and B2*12. The payment (pmt) has been entered in the worksheet as a negative value as this is money being paid out.

=PV(A3/12,B3*12,,D3)

The present value is a negative number as it shows the amount of cash that needs to be invested today (paid out) to generate the future value of $20,000 in 10 years at a rate of 3.5% interest.