500 must be in writing. If you were to go into a department store and buy something for 400 the transaction would not have to be in writing.

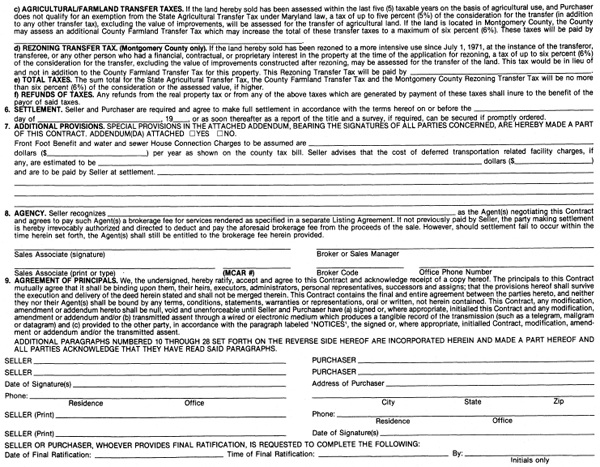

500 must be in writing. If you were to go into a department store and buy something for 400 the transaction would not have to be in writing.2 |

Contracts |

In the process of purchasing property and building a home you will be signing many contracts and purchase orders (a form of contract). Accordingly, it is important for you to understand some of the legal aspects of a contract and the contracting process.

For our purposes, we will use the definition of a contract taken from Real Estate: Principles and Practices (South-Western, 1987) by Maurice A. Unger, a professor of Real Estate and Business Law at the University of Colorado.

Generally, a contract is an exchange of promises or assents by two or more persons resulting from an obligation to do or refrain from doing a particular act, which obligation is recognized or enforced by law.

A contract may be formed when a promise is made by one person in exchange for an act or the refraining from doing of an act by another. The substance of the definition of a contract is that by mutual agreement or assent the parties have created legally enforceable duties or obligations that did not exist before.

If all the terms of the contract have been fulfilled, it is said to be executed. If something in the contract remains to be done, it is said to be executory.

We also need to define what real estate is as it relates to contract law. It is very important to understand the technical meaning of the term. Real estate is land, dirt, rocks, and trees. If you have a piece of property that is unimproved, it is real estate. If it had a house on it when you bought it, both the property and the house are real estate. If you buy the property without a house on it and you add a house, the house is real estate. Real estate is the natural land and any improvements that are on it.

What real estate is not is personal property that is not part of the improvements or not yet part of the improvements.

Your fire insurance policy or your homeowner’s or builder’s risk policy will cover the improvement in your real estate. As you build the foundation, the policy will cover the foundation; as you build the first floor, the policy will cover the first floor; and when you build the house, the policy will cover the completed house. But, before it becomes attached to the house, the material to be used is personal property.

So, if you’re building your house and someone delivers twelve windows to your job site and six of them are installed and six are on the ground, and there is a fire that night, your builder’s risk policy will cover the windows in the house because they are part of the real estate. But it will not cover the windows on the ground, because they are personal property. It is possible to add a provision to your insurance policy (known as a rider) that covers building material stored on the site. Accordingly, it is important that you understand the concept of real property, the distinctions between real property and personal property, and the legal and insurance ramifications associated with the distinctions between the two.

Many people think that contracts must be in writing, but they don’t have to be. Let’s say that you drive up to a gas station on a hot summer day, and say, “Fill ’er up,” and the attendant pumps gas into your car and then says, “That will be fifteen dollars.” And you reply, “No deal. We didn’t have a contract.” Who wins?

He wins. “Fill ’er up!” is an oral contract.

You go into a restaurant. You order a meal. “I’ll take the filet, I’ll take the asparagus, I’ll have a coke.” The waitress serves all of this and gives you a bill. Are you obligated to pay? Absolutely.

So an oral contract clearly can be a contract, and it can be as binding and enforceable as a written contract.

A contract need not even be oral. You drive into the same gas station, but now it is pouring down rain. The kid comes running out. Your windows are rolled up and you signal with your hands: “Fill ’er up!” And he signals: “okay.” He puts the gas in. Do you have a contract? Yes. It was implied. And an implied contract is an enforceable contract.

Similarly, if you go into a restaurant and you start eating the buffet, that binds you. It is an implied contract.

Sometimes a contract that is not a contract at the time can become a contract at a later date. For example, if you say, “Let’s sign the documents now,” and you don’t, and then you subsequently perform as if the contract had been signed, that is called affirmation by action. Your subsequent actions may ratify a contract.

An executory contract is one in which there is something still to be done—and it is very important in real estate. Most contracts are executory. Something still remains to be done. When the terms and conditions of the contract are completed, it is said to be executed.

If you sign a contract to buy a piece of property, it is an executory contract because you have agreed to buy that piece of property in the future and the seller has agreed to sell you that piece of property in the future. Generally there are some conditions and terms that have to happen in the interim. You are both bound by the terms and conditions, but they are things to be done in the future. When you settle on your property and you give the owner the consideration and he gives you a deed, that transaction then becomes an executed contract.

The statute of frauds is an integral part of contract law. It states that some contracts must be in writing. It does not say that an oral contract is not a contract; it says only that some contracts must be in writing. A written contract is more lasting, more comprehensible, and less controvertible than something oral. So as the contract becomes important and potentially more controvertible, the law says it must be in writing.

The statute of frauds, which comes from English law, has been adopted by most countries that follow the English legal system. It covers many aspects of contract law. In this book we will discuss only three considerations in the statute of frauds which are relevant to real estate and contract law as they relate to building a home.

(1) The statute of frauds says that all contracts must be in writing if the transaction involves real estate.

(2) In most states, the Uniform Commercial Code says that any transaction involving the sale of goods and services in excess of 500 must be in writing. If you were to go into a department store and buy something for 400 the transaction would not have to be in writing.

(3) Any contract that will take longer than a year to perform must be in writing. This is only logical.

Lawrence P. Simpson’s Handbook of the Law of Contracts (West Publishing, 1965), which is frequently referred to as the Bible on contracts, says:

When a contract is expressed in writing which is intended to be the complete and final expression of the rights and duties of the parties, parole evidence of prior oral or written negotiations or agreement of the parties or their contemporaneous oral agreements which varies or contradicts the written contract is not admissible.

The term “parole evidence” has nothing to do with getting out of prison on parole. In contract law, parole evidence is essentially any oral discussion that occurred prior to or contemporaneously with a contract. Here is how it might work in a real estate transaction: Judy has said she will sell John a house. They are close to arriving at a price but John is still undecided, so Judy says, “I’ll tell you what I’ll do. I’ll plant pansies on your property.”

John says, “I don’t like pansies. They have to be taken care of.”

Judy says, “I’ll take care of them. I’ll plant the pansies and I’ll mulch them if you buy this house for 100,000.”

They then write the price of the house in the contract. The contract says nothing about mulching pansies, although it does say they will be planted. They go to settlement, and John says, “Nice house, but how about mulching the pansies that you planted?”

Judy says, “What mulching?”

John says, “You told me you were not only going to plant pansies, but mulch them.”

John’s lawyer comes out and looks at the contract and says, “I don’t see any pansy-mulching in here.” Will John be able to get Judy to mulch his pansies? No. Because parole evidence says that if this contract represents the final and entire agreement between the parties, all prior and contemporaneous written and oral agreements and discussions are merged into the final document. Since the written contract did not refer to mulching pansies there is no agreement concerning them.

Look at the practical aspects. You go to Orlando to buy a condominium. The salesman says, “This condominium comes with everything you see,” and he starts listing all the things that come with it. If he is listing them verbally (and you are not writing them down and getting them in the contract), when you go to settlement and he does not produce—you lose! Whenever a salesman talks about what he is going to do, start writing—and put it in the contract. If when Judy said, “I’ll mulch the pansies,” John had written that into the contract, it would have become part of the signed contract. She would then have had to mulch the pansies.

Any discussions after the contract is signed are admissible, because in so doing we are now creating a new agreement, and any oral representations which are fraudulently presented can be raised as evidence. If there was a pattern on the part of a salesman who promised everybody a mulching of their pansies in order to induce them to buy when he knew from the start that there would be no mulching done, that is fraudulent.

What we so often hear is, “The salesman told me . . .” If the salesman tells it to you, write it down.

Some contracts merge into others. Some statements merge into others. When parties to a simple contract consent to a subsequent or higher contract, the new contract absorbs the elements of the old contract, and the elements of the old contract are said to merge with the new.

This is important. Using what we know about merger and non-merger, an executory contract merges into the executed contract. If you sign a contract for the purchase of a piece of property and subsequently go to settlement, pay the money, and receive the deed, the deed represents an executed contract. And that is the final contract between the two parties. The previous contract—the sales contract which is the executory contract—dies at that point. There has been a merger of the two contracts.

You have to be aware of merger, but you can also prepare for non-merger. In the case of Judy’s and John’s mulching transaction, when she said “I’m going to mulch your pansies,” John should have written, “The mulching of the pansies will survive this contract.” That would be the lay expression; the legal expression is: “The mulching of the pansy provision will not merge with the deed.” It is ongoing. If John specifically prevents it from merging, then it does not merge.

To summarize, mulching your pansies is not going to happen unless it is written into the contract. If it is written in the contract but you then sign a final contract, it is still not going to happen unless you provide for a non-merger. If it is not written in the new contract, you cannot come back later and say, “You told me you were going to mulch the pansies.” Even if you write it in the executory contract, then go to settlement and the pansies are not mulched you are still out of luck. Therefore get it in writing and make sure that it is a non-merged element.

There are five essential elements that must be present in any contract. The three most important are:

(1) There must be two or more parties

(2) There must be mutual assent

(3) There must be consideration

The others, that you should at least be aware of, are:

(4) The two or more parties must have the legal capacity to contract

(5) The object of the contract must be a legal or lawful act

Now that we have an understanding of what contracts are and their essential elements, let’s look at the three contractual situations that are most likely to confront you in building and possibly selling your home: the land purchase contract, the construction contract, and the listing agreement.

There are several types of real estate contracts. There is a contract for the purchase and sale of improved property, commercial property, rental property, cooperatives, condominiums, and investment properties. When you go to a realtor’s office you will usually find a variety of different forms drawn up for different transactions. A contract is binding on both parties but contracts can be written with terms that are more favorable to one party than the other. You can usually obtain blank contracts from the board of realtors in your state. In some states similar (but not identical) contracts are printed in two different colors, one color being more favorable to the seller and the other being more favorable to the purchaser. But the principles that govern the sensible terms of a contract can apply to both sides. The contract we will be mostly concerned with is the Land Purchase Contract.

Make sure you identify the parties to the contract. If you’re the buyer, make sure you identify the seller. If the seller is married make sure that both husband and wife sign. The seller may be a partnership or a corporation. Make sure a general partner signs for a partnership and a corporate officer signs for a corporation. If it is a corporation, make sure there is a corporate resolution that permits the corporation to execute the contract and authorizes the particular officer to sign it.

Make certain that the property is precisely identified. The property should be staked out and surveyed and the sections and parcels correctly identified. Go out to the property yourself, check the stakes, and verify the descriptions. After identifying your property make sure it is correctly identified in your contract. Frequently large subdivisions will contain Sections A, B, C, and perhaps Lots 1 through 25 or more. Occasionally someone will buy Lot 15 in Section A, but by mistake it will read “Lot 15, Section B” in the contract. Not only is there a technical question of ownership, but sometimes in large subdivisions the covenants are different in each section. You should make certain the covenants you are observing are for the section where your property is located.

These are periods of time within which you will be expected to perform the contract. In an executory contract there could be two or even three performance dates. One would be the time in which you are to settle on the property. Another would be the time by which you need to complete all of the contingencies to be discussed in the next section of this chapter. There may also be a particular time frame for a financing contingency, another for feasibility contingency, and a time frame within which you have to close. For example, if you bought a piece of property on September 1, you might say, “I want thirty days for an investigation period, I want sixty days to secure my financing, and I want to close thirty days after all these contingencies are met—no later than ninety days from the day of the contract.” If you’re the buyer, you want to avoid having the expression “time is of the essence” appear in the contract, because it could create a serious problem if you did not meet that deadline.

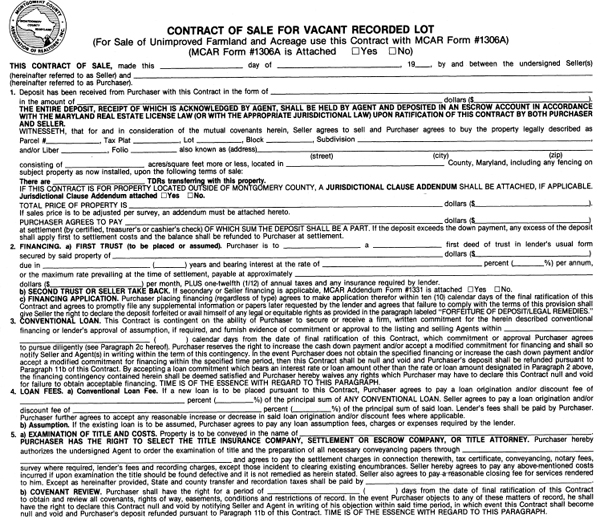

10. SPECIAL NOTICE. THE AGENT(S) ASSUME NO RESPONSIBILITY FOR THE CONDITION OF THE PROPERTY NOR FOR THE PERFORMANCE OF THIS CONTRACT BY THE PARTIES HERETO. PURCHASER HEREBY WARRANTS AND REPRESENTS UNTO SELLER AND THE REAL ESTATE BROKERS THAT NO AGENT, SERVANT OR EMPLOYEE OF SAID REAL ESTATE BROKERS HAS MADE ANY STATEMENT, REPRESENTATION OR WARRANTY TO THEM REGARDING THE CONDITION OF THE PROPERTY OR ANY PART THEREOF UPON WHICH PURCHASER HAS RELIED AND WHICH IS NOT CONTAINED IN THIS CONTRACT.

11. FORFEITURE OF DEPOSIT/LEGAL REMEDIES. a) If Purchaser shall fail to make full settlement, the deposit herein provided for may be forfeited as liquidated damages at the option of Seller, in which event Purchaser shall be relieved from further liability hereunder. If Seller elects not to require forfeiture of the deposit, Seller shall notify Purchaser and Agent(s) in writing within thirty (30) days from the date provided for settlement herein of his election to avail himself of any legal or equitable rights which he may have under this Contract, other than the said forfeiture. In the event that Seller elects not to require forfeiture of the deposit, said deposit shall be retained by Agent holding the same pending resolution of Seller’s legal action. In the event of the forfeiture of the deposit, or if Seller shall fail to take any action or fail to pursue any legal or equitable remedies, then and in that event, Seller shall pay the Agent(s) as compensation for services one-half (½) of the amount of the deposit, said amount not to exceed the amount of the full brokerage fee. If after a breach by Purchaser, Seller shall release Purchaser from liability hereunder or authorize refund of the deposit, Seller shall pay the Agent(s) as compensation for services one-half (½) thereof, said amount not to exceed the amount of the full brokerage fee, but said amount shall not be less than one-half (1/2) of the deposit in the event of a compromise agreement. If the Agent(s) is required to participate in any legal proceeding, either as Plantiff, Defendant or Third Party, Seller agrees to pay reasonable attorney’s fees for Agent’s own attorney.

b) Except with respect to disbursement of the deposit at settlement hereunder, the deposit and accrued interest, if any, shall be given or returned by escrow agent to any of the parties to this transaction only when an “Agreement of Release” has been ratified by all principals or as directed by a court order. If either Purchaser or Seller refuses to execute a release of the deposit when requested to do so in writing and a court finds that that party should have executed same, that party shall be required to pay the reasonable expenses, including reasonable attorney’s fees, incurred by the adverse party in that litigation.

12. TITLE. The property, including personal property which conveys hereunder, is sold free of encumbrances, unless otherwise stated herein. Any financing statements will be paid and released by Seller at time of settlement. Title is to be good of record, merchantable and insurable, subject however to the convenants, rights of way, easements, conditions and restrictions of record, if any; otherwise, the deposit is to be returned and sale declared null and void at the option of Purchaser, unless the defects are of such a character that they may be remedied by legal action within a reasonable time. However, Seller and Agent(s) are hereby expressly released from all liability to Purchaser for damages by reason of any defect in the title. In case legal steps are necessary to perfect the title, such action must be taken promptly by Seller at his own expense, whereupon the time herein specified for full settlement by the parties will thereby be extended for the period necessary for such prompt action.

13. PERFORMANCE. Settlement is to be made at the office of the Attorney or the Title Company examining the title. Delivery to the Attorney or to the Title Company of the cash payment and settlement costs as herein stated, the executed deed of conveyance and such other papers as required of either party by the terms of this Contract shall be considered good and sufficient tender of performance in accordance with the terms hereof. It is agreed that funds arising out of this transaction at settlement may be used to pay off any existing encumbrances, including interest, as required by the lender(s).

14. ADJUSTMENTS. Rents, taxes, water, sewer charges, escrow, insurance and interest on existing encumbrances, if any, and other operating charges are to be adjusted to date of settlement. Taxes, general and special, are to be adjusted according to the certificate of taxes issued by the collector of taxes, except that assessments for improvements completed prior to the date of acceptance hereof, whether assessment therefor has been levied or not, shall be paid by Seller or allowance made therefor at time of settlement. If the property is serviced by the Washington Suburban Sanitary Commission or local government, annual Front Foot Benefit charges and sewer and water House Connection charges of said Commission or local government (which typically appear in the annual county real estate tax bill) are to be adjusted to date of settlement and assumed thereafter by Purchaser. PURCHASER HEREBY ACKNOWLEDGES THAT HE IS ASSUMING ANY OUTSTANDING AND UNPAID FRONT FOOT BENEFIT AND SEWER AND WATER HOUSE CONNECTION CHARGES WHICH WILL BE PAID ANNUALLY.

15. CONVEYANCE. a) Seller agrees to execute and deliver a good and sufficient special warranty deed. Purchaser agrees to have the deed of conveyance recorded promptly.

b) Seller or Purchaser, if a corporation, is qualified to do business in the State of Maryland and is a corporation in good standing and is empowered to execute this Contract and is acting pursuant to a duly passed Resolution of its Board of Directors, a copy of which is attached hereto.

c) If either Seller or Purchaser is a general or limited partnership, then such party represents and warrants that it is duly organized and in good standing, is qualified to do business in the State of Maryland, and that any partner executing this Contract on behalf of the partnership is acting pursuant to authority granted to such partner in the Partnership Agreement or pursuant to a duly passed Partnership Resolution, a copy of which is attached hereto.

16. INSURANCE. The risk of loss or damage to said property by fire or other casualty until the deed of conveyance is recorded is assumed by Seller.

17. POSSESSION. Seller agrees to give possession and occupancy at time of settlement, and in the event he shall fail to do so, he shall become and be thereafter a tenant by sufferance of Purchaser and hereby waives all notice to quit as provided by the laws effective in the state in which the property is located. All notices of violations of orders or requirements noted or issued by any governmental authority or actions in any court on account thereof, against or affecting the property at the date of settlement of this Contract, shall be complied with by Seller, and the property conveyed free thereof.

18. PROPERTY CONDITION. At the time of settlement Seller will leave property free and clear of trash and debris. Seller will deliver the property in substantially the same physical condition as of the date of final ratification. In addition to any other specific inspections provided for in this Contract, Purchaser has the privilege of one (1) final inspection of the entire property prior to settlement. Except as expressly contained herein, no other warranties have been made by Seller nor relied upon by Purchaser.

19. LENDER REQUIREMENTS. Seller agrees to comply with reasonable lender requirements.

20. SUBDIVISION PLAT. Purchaser acknowledges receipt of an entire copy of the single recorded subdivision plat prior to execution of this Contract.

21. GENERAL/MASTER PLAN. Purchaser acknowledges that he has been apprised of his rights to review the applicable Master Plan, any adopted amendment to the Plan, and the Wedges and Corridors General Plan for the Bicounty region, including Master Plan maps showing planned land uses, roads, highways, parks and other public facilities affecting the property herein described prior to execution of this Contract. Purchaser further acknowledges that Seller has informed him that amendments affecting the Plan may be pending before the Planning Board or the County Council. Purchaser acknowledges that he has reviewed said applicable plans and adopted amendments thereof prior to executing this Contract or does hereby waive his right to do so. Purchaser also acknowledges that the Agent has advised him of the relative location of any airport or heliport existing within a five (5) mile radius of the property. Purchaser acknowledges that he is aware that the applicable Master Plan or General Plan for Montgomery County is available at the Maryland-National Capital Park and Planning Commission and that at no time did the Agent explain to him the intent or meaning of such a Plan, nor did he rely on any representation made by Agent pertaining to the applicable Master Plan or General Plan.

22. THE PLAN, GENERAL/MASTER PLANS (CITY OF ROCKVILLE, MARYLAND ONLY). Purchaser acknowledges that he has been afforded the opportunity to examine the Approved and Adopted Land Use Plan Map portion of The Plan for the City of Rockville and all amendments to said Map (hereinafter referred to as the “Plan”). Purchaser further acknowledges that Seller’s real estate Agent has provided said opportunity to examine the Plan by either producing and making available for examination a copy of the Plan or escorting Purchaser to a place where the Plan is available for examination by Purchaser. Purchaser also acknowledges that Seller’s real estate Agent has advised him of the relative location of any airport or heliport existing within a five (5) mile radius of the property. Purchaser acknowledges that at no time did the Agent explain to him the intent or meaning of such Plan nor did he rely on any representations made by the Agent(s) pertaining to the applicable Plan. (This paragraph supersedes paragraph 21 hereof only when the property being sold is in the City of Rockville.)

23. NOTICE AND DISCLOSURE OF AVAILABILITY OF SEWAGE DISPOSAL SYSTEM AND DESIGNATED AREAS. a) Notice is hereby given, pursuant to the Montgomery County Code, to the prospective Purchaser of the obligation of Seller, or his duly authorized Agent(s), to disclose to Purchaser any information known to Seller as to whether the property is connected to, or has been authorized for connection to, a community sewage system and, if not, whether an individual sewage disposal system has been constructed on the property, whether an individual sewage disposal system has been approved by the County for such property, or whether the property has been disapproved by the County for the installation of an individual sewage disposal system.

b) Purchaser hereby acknowledges that, prior to entering into this Contract of sale, Seller or his duly authorized Agent(s) provided the above information, as known to Seller or his Agent(s).

c) If an individual sewage disposal system has been or is to be installed upon this property, and if said property is located in a subdivision, Purchaser acknowledges that he has reviewed the said record plat, including any provisions thereon with regard to areas restricted for the initial and reserve well locations and the individual sewage disposal system, and the restricted area in which construction of the building to be served by the individual sewage disposal system is permitted.

d) Seller, at his expense, shall furnish to Purchaser, prior to settlement, a written certification by the County Health Authority or recognized private engineer or laboratory stating that, as applicable, well water is potable and that the individual sewage disposal system is in working order.

24. NOTICE TO PURCHASER AND ALL OTHER PARTIES-GUARANTY FUND (MARYLAND ONLY). Any person aggrieved in accordance with Article 56A, Section 4-404 of the Maryland Code may be entitled to recover compensation from the Maryland Real Estate Guaranty Fund for his monetary actual loss not to exceed Twenty-Five Thousand Dollars ($25,000). A purchaser is protected by the Guaranty Fund in an amount not exceeding Twenty-Five Thousand Dollars ($25,000).

25. FINANCING PROVISIONS. a) In the event that mortgages are used rather than deeds of trust, the word “mortgage” shall be substituted automatically.

b) If the Contract provides for the assumption of existing trusts, it is understood that the balance of such trusts and the cash down payment are approximate.

c) Trustees in all deeds of trust are to be named by the parties secured thereby.

d) Seller shall allow inspections of all of the property and furnish any pertinent information required by Purchaser or his lender in reference to obtaining a loan commitment.

e) Proceeds of loans acquired pursuant to Paragraph 2 shall be applied to the purchase price.

26. CREDIT INFORMATION RELEASE. Purchaser hereby authorizes the Agent to disclose and deliver to Seller or any lender the credit information provided to Agent by Purchaser.

27. NOTICES. Notices required to be given to Seller by this Contract shall be in writing and effective as of the date on which such notice is delivered to one of the Agents of Seller named in Paragraph 8 hereof at the principal place of business of said Agent(s). Notice required to be given to Purchaser by this Contract shall also be in writing and effective when either delivered to Purchaser or when mailed to Purchaser’s address as shown on page one hereof.

28. ATTORNEY’S FEES. Should any litigation be commenced between the parties hereto concerning the property, this Contract, or the rights and duties of either in relation thereto, the party (Purchaser or Seller) prevailing in such litigation shall be entitled, in addition to such other relief granted, to a reasonable sum as and for his attorney’s fees in such litigation, to be determined by the Court in such litigation or in a separate action brought for that purpose. If Agent is required to participate in any legal proceedings, either as Plaintiff, Defendant or Third Party, Seller agrees to pay reasonable attorney’s fees for Agent’s own attorney.

An important note for the seller. If your purchaser includes this contingency provision in the contract, you really don’t have much of a contract.

If you need financing, make the contract and your purchase subject to financing. Then if you are unable to obtain financing you can usually get out of the contract. You will, of course, have an obligation to try to find financing. The seller will probably help you and perhaps even say, “My brother will finance you.” This would be all right if you have written in the contract, “subject to reasonable financing.” You should be sure to ask the seller, “What rate will your brother charge?”

Making the contract subject to market rate financing is a good rule to follow, because it is more definitive. You can look at a Wall Street Journal and arrive at a market rate.

Making the contract subject to financing or even reasonable financing is not sufficient. It is not sufficiently precise and leaves room for dispute. Making the contract subject to market rate financing is more precise and probably offers you adequate protection. But we recommend even more precision, which offers even more protection.

We recommend the following in the contract: “This contract is subject to Purchaser’s securing a loan in the amount of ____________.” In this blank you insert the largest number possible in order to protect yourself. If you need 100,000, put in 105,000. The Seller may want to put in 95,000. You are trying to get the highest amount while he is trying to get the lowest. Also include “at an interest rate not to exceed ___________.” If you want 9%, put 8½%. The Seller will probably say 9½%. Also include “for a term not less than ____________.” [you will probably say forty years and the Seller will say twenty years] and for points not to exceed ____________.” (Points are explained later in this book.) You are trying to achieve the most favorable scenario. If you are unable to obtain a loan after making reasonable efforts, you would then be relieved of your obligation under the contract and would be entitled to a return of your deposit. With the precision set forth above, a dispute over the financing will be less likely.

The ultimate financing contingency protection for you as the purchaser is to make the purchase subject to the purchaser securing financing acceptable to him in his sole discretion. With this contingency you have total control over whether you want to accept the financing available to you. While this may not seem fair, it is perfectly legal. Remember that although you have the exclusive right to determine if the financing is acceptable to you, you must take affirmative steps to secure financing. If you don’t try to secure financing, even if you can reject all that is offered, you are not relieved of your obligation to purchase under the contract.

You should have a provision for a period in the contract that will permit you to investigate certain elements of the transaction about which you want to be satisfied before you settle on the property. You could specify an investigation period of thirty or sixty days, or whatever period you negotiate. Once you secure this investigation period and determine a time frame, then the contract is contingent upon the investigation proving to be informative as it relates to certain contingencies. You want to know that the property is properly zoned, which you will investigate. You should check out the covenants of the property and make sure you are satisfied with them and that they are compatible with your concept of a lifestyle. You should find out all you need to know about the neighborhood and the neighbors. And you should make sure that you can get all the requisite permits needed to build your home. Many people will put a provision in the contract that the purchase is subject to securing a health permit. They then find they can get a health permit but cannot get a building permit. So then they might say, “I’ll add a health permit and a building permit to the terms.” Then they get both of those, only to find they cannot get approval from the architectural review board. Rather than enumerating each permit to the contract you want to say, “This contract is subject to Purchaser being able to secure all requisite permits in order to build his home.”

This investigation period is the purchaser’s opportunity to check out the property before actually becoming the owner. Use this time wisely. Be thorough in your investigation. Make sure the property suits your needs and that you can build the home you want to live in.

Embodied in both the investigation period and financing is an affirmative obligation on the part of both parties to try to accomplish all prerequisites. If you sign a contract that says you have time to investigate the property, you must investigate it. If you sign a contract and agree to try to get financing at a certain amount at a certain rate you must try to get financing. If you try to get it and fail you are relieved of the commitment. If you don’t try to get it, you are not relieved of the contract. You have a contractual obligation to make an effort.

You can include almost any contingency in a contract, although the other party is not obligated to sign it. We knew of one case in which the buyer said he would not close until his grandmother died, and it was written in the contract. If his grandmother did not die, he would not be obligated to buy the house.

Because of the contingency period in a contract during which the buyer is seeing if he can make the deal work and find financing, some sellers include a “kick-out” clause in the contract. A KO clause enables the seller to sell his property sooner without contingencies. A typical kick-out clause would read as follows: “If the Seller notifies Buyer that the Seller has another bona fide buyer that will purchase the property without contingencies, the Buyer will have _______days [some agreed upon time period] to notify Seller that Buyer will settle at the agreed upon settlement date without contingencies.”

If the first buyer is unwilling or unable to agree to settle without contingencies, then the seller may void the contract and enter into a non-contingency contract with the second buyer. In this case, the first buyer gives up all rights in the contract and is entitled to a refund of his deposit. A KO clause is frequently used when the buyer has placed a lot of contingencies in the contract or has requested a distant settlement date.

The following is a typical KO clause situation. The buyer agrees to purchase the seller’s home contingent upon the sale of the buyer’s home. The seller accepts the contract but with a KO provision that if the seller finds another buyer that will settle sooner without contingencies, the first buyer must perform or lose his interest in the contract.

A KO clause is a benefit to the seller. It is negotiable. If you, as the buyer, are not able to perform without contingency, it may be the only way the seller would agree to sell to you.

Both parties have an affirmative obligation to attempt to resolve all the contingencies. If the contract is subject to the purchaser securing financing and the purchaser cannot obtain financing, he is relieved of his obligations provided that he tries to get it and cannot. But if he sits on his hands, or if he goes into the bank and says, “I’m broke,” he has not made reasonable attempts to obtain financing.

Quitting a job and then citing unemployment as a reason for not being able to secure a loan is also not permissible. It is not performing positively under the contract. However, losing a job would be a valid reason to withdraw from a contract. As sad as it may seem, when people enter into a contract to purchase a piece of property and subsequently decide to get a divorce before the contract runs out, that does not relieve them from performing under the contract. They are required to take positive, affirmative actions to close on the transaction. Getting a divorce is not a positive, affirmative action.

You want the contract to specify that the property is not under condemnation proceedings.

You want the contract to refer to you, John Doe, “or assigns,” which means that you can assign the contract to someone else. The person to whom you assign it must accept it subject to the same conditions. The only way that the assign situation would not work would be if the seller were providing financing to you based on your credit application. In this case, he would not have to assign it to somebody else whose credit might be worse than yours. But if it is a cash deal you can assign the contract to a third party, and he does not have to sign it. This is very important, especially in a real estate contract.

If both parties sign a contract for the purchase of a piece of property and the buyer does not leave a deposit, is it a binding contract? Absolutely. It is a binding contract because a promise to buy and a promise to pay are elements of consideration which are the elements of a contract. The deposit does not bind the parties. It is the mutual promises of the parties that make the contract.

The deposit is the money that a purchaser leaves in escrow with either the seller or the realtor to insure his performance. In the event that he does not perform, the deposit can be kept by the seller and/or realtor as liquidated damages. Keep in mind that if you are the seller and the buyer did not put up a deposit it does not mean you do not have a binding contract. What binds the contract is mutual consideration, which is the promise to buy and the promise to sell.

It is important that you include provisions for notice in a contract. Notice is how you inform the other party of particular events. Don’t get into a situation in which you are the buyer and you don’t know where the seller is. You may have to tell him that the contingencies have fallen through. You need to know how to “notice” the seller, and you want the seller to know how to “notice” you. You don’t want to go to settlement and have the seller say, “I couldn’t get in touch with you.” Make certain that both your address and the seller’s address are in the document. Sometimes a contract will have only the seller’s name. You should include your address so you will be notified if any problems arise concerning the property or permits.

You want it specified in the contract under what jurisdiction the contract can be interpreted. If you’re buying a piece of property in Maryland, for example, you want it to be interpreted under Maryland laws. You might think this is standard procedure, but it isn’t. You need to keep the laws of the contract in a jurisdiction close to home.

When someone does not perform under a contract, this is known as a breach. There is also an anticipatory breach, which means that if one party thinks the other party is not carrying out his part of the contract he doesn’t have to wait for the duration of the contract to charge breach. If you have six months to obtain financing but are doing nothing about it, and it is obvious you’re doing nothing about it, the other party does not have to wait six months to sue you. If, after a reasonable length of time, he can prove you’re doing nothing to obtain financing, he can sue.

When a purchase contract is breached there is a breaching party and there is an aggrieved party, and it is important to know what these terms mean. The breaching party is the one who does not perform. The aggrieved party is the one who stands to suffer thereby.

If a real estate contract is breached the remedies available to each party are different. If a buyer agrees to pay 100,000 for a piece of property and the seller agrees to sell it and the buyer subsequently breaches, the seller is entitled to receive damages for the breach. The seller would be entitled to the lost profits he would have made on this particular transaction because the seller has a right to be made whole. At this particular point, the seller is obligated to mitigate the damages. The seller can try, using reasonable efforts, to sell that piece of property. If he sells it for more than the price the buyer agreed to pay, then he has suffered no damages. But if he sells it for less than that—say 90,000—the buyer is liable for the amount between the contract price and the price at which it could be sold within a reasonable time frame and in a reasonable market—in this case 10,000.

It is different if you’re the seller and you breach. If you’re the seller and you agree to sell that property for 50,000, and then decide “I’m not going to sell it for 50,000” (probably because it is worth more than 50,000), the remedy available to the buyer is called specific performance. He can sue and require you to perform specifically under that contract and to deed the property to him for the sum of 50,000. The reason for the two different approaches to remedying a default is that the law says it would be very difficult to determine damages if the seller breaches. The property is unique, you have a contract for it, and you’re entitled to it.

When you sign a contract be prepared for the consequences of a breach, depending on whether you are the buyer or the seller. If you’re the seller and there is a realtor involved, you have an obligation to the realtor if that realtor produces a buyer who is ready, willing, and able to buy. As the seller you need to be ready to make arrangements to satisfy the interests of the realtor in the event there is a breach by either you or the buyer.

If you’re the buyer there should be a provision in the contract that in the event of a breach by the seller (or in the event of litigation), the seller must pay the buyer’s attorney’s fees. If you’re the seller, you may want to include a provision that in the event of a breach by the buyer, the buyer will pay the seller’s attorney’s fees. These are permissible additions to a contract, and you should keep in mind which status you occupy and protect yourself accordingly.

If you’re a buyer and you execute a contract for the purchase of a piece of property and you subsequently breach, you are liable to the seller for his damages. One way to limit your liability is to state in the contract that, as buyer, in the event that you do not perform you agree to forfeit your deposit and that the forfeiture of the deposit will relieve you from any further liability under that contract. If you don’t have a provision in the contract that permits you to forfeit the deposit and relieve you of any further liability and you breach, then you may be responsible for the seller’s entire damages—not just the loss of your deposit.

When you sign a contract you frequently put up a deposit. That deposit will often equal an amount that has been provided for liquidated damages. This means that in the event of breach rather than having to litigate to determine the damages, you have predetermined them. If there is a breach by the buyer he will forfeit the amount of money specified as liquidated damages.

This eliminates the cost of litigation. So frequently the deposit on a contract is made to equal liquidated damages. Be careful, though. Some contracts will say that if you, the buyer, breach, you are liable not only for the deposit but for any other legal or equitable remedy that the seller may have under the law. As a buyer, you want your contract to read that the buyer leaves “a deposit in the amount of ____________.” You then state the amount to be used as liquidated damages in the event the buyer does not perform under the contract. Then if the buyer does not perform under the contract he forfeits his deposit and is relieved of any further liability under this contract.

Of course, if you didn’t perform under the contract because the contingencies were not met then the issue of liquidated damages is not relevant, and accordingly your full deposit would be refunded.

Study the contract that follows. In the thirteenth century, there was a philosopher named William of Occam who said, “What happens if we have two competing theories and they both have the same intellectual strength? They both make sense. Which theory is the better?” The answer was the simpler of the two, and thus the postulate, “Occam’s razor,” which is often cited in game and risk theory and economics. This contract is a classic example of Occam’s razor. You could use this contract to do ninety percent of the contracting for your home.

In drawing up construction contracts it is important to know who the players are and to keep their distinctions clearly in mind. Under the law a general contractor is anyone who contracts directly with the owner. For example; you hire a builder, John Jones, to build your home. He’s usually known as a general contractor. But let us assume you also hire Tom Smith, an electrician, to do the electrical work. He’s also a general contractor because he contracted directly with the owner. If you’re the owner and are also managing the building of your own home then you are both the owner and general contractor. In this case the electrician is also a general contractor because he contracted directly with the owner of the house. But if John Jones had hired him instead of you then Smith, the electrician, would be a subcontractor.

In the practical sense a general contractor is somebody who manages the building of your home and hires the other trades. But from a legal standpoint a general contractor is anyone who contracts directly with the owner. From a legal standpoint it is important to make a distinction between the general contractor and the subcontractor. In building your own home most of the people with whom you will be contracting will be general contractors, regardless of their job description.

In addition to the Owner and General Contractor, the other players are:

The Subcontractors or Mechanics: The subcontractor is a worker or mechanic who contracts with the general contractor. A mechanic is an old English term, somebody who performs a trade—a plumber, an electrician, an insulation mechanic, a trim carpenter, or framing carpenter. All trade people are mechanics. A mechanic’s lien is the right of somebody who has performed the work on your house to claim an interest in that house for nonpayment for services that he has performed.

Materialmen: The materialmen supply the material. It could be lumber or it could be drywall. A mechanic can be not only a mechanic but also a materialman. So there can be a mechanic’s lien or a materialman’s lien; the effect is the same.

In the contract you need to list the parties to the contract and to specify exactly what is to be done. And you need to specify the cost and payment schedule. The more specific you are in every category, the better. If a contractor is going to install the heating, ventilation, and air conditioning, he should identify the quantity of material and the brand name or that what he will furnish will be comparable to a brand name. If he says, “Carrier or comparable” for the air conditioner, for example, that’s a legal term. But it has to be something that is comparable to a Carrier. If you want only a Carrier, scratch out the words “or comparable” and make sure you both initial the change.

When the contractor signs the contract it is then an offer to furnish and install. He will specify a time frame (generally ten days or thirty days) within which it can be accepted. If you don’t accept it within that time frame, the offer expires. If you do sign it within that time frame, it is an executory contract.

All material is to be guaranteed as specified; all work is to be completed in a “workmanlike” manner. That is a legal term, meaning it has to conform to the industry standards in your particular area. Any alteration or deviation from these specifications involving extra cost will be executed only upon written order. You can alter it orally if it is less than 500, but we recommend that all changes, no matter how small, be in writing.

The contract also makes reference to workmen’s compensation insurance. Workmen’s compensation insurance is probably not sufficient coverage. You contractor should have general liability insurance as well. Ask him for a certificate from his insurance carrier for both types of coverage. The greater the amount of work he is to perform the more important the insurance is.

This contract does not specify that the work must “conform to code” (the local regulations). You can insist on that but you will usually have to write it into the contract. And be sure to include provision for attorney’s fees in the event that you have to sue.

Some people like to specify that in the event of a dispute it will be turned over to arbitration. We do not recommend this. Studies have shown that in arbitration there is an effort to compromise on the problem rather than to solve it on the merits. And no matter how the arbitration agreement is drafted, in all probability the party who loses arbitration is going to sue anyway. So arbitration just delays the inevitable.

Look for the elements included in our contract in whatever form your contractor uses. If he doesn’t have a form, we recommend this one; it can be bought at any stationery store. Don’t make your agreement on an envelope while standing on your property, because you could omit something important.

The payment schedule needs to be well thought out. We can illustrate this point with a story. A home improvement contractor comes to your neighborhood and agrees to build five family rooms for five different homeowners. He gets out of his car, looks at your house, and starts walking around, still looking, he already knows that it’s going to cost him 10,000 to do the job, and he’ll probably mark it up a hundred percent, charging you 20,000. But he’s taking plenty of time in order to make his estimate look studied and solid. He quotes the same price to all five homeowners, but they all decide on different payment schedules.

The first, Mr. Stingy, says, “Tell you what I’m going to do. I’m going to give you 2,000 now and 18,000 upon completion.” Down the street is Mr. Quickdeal. He says, “I’ll give you 10,000 now and 10,000 when you complete the job.” The next guy is Mr. Reasonable. He says, “I’m going to pay you 5,000 now, 5,000 when it is 25% done, 5,000 when it’s 50% done, and 5,000 upon completion.” The next guy is Mr. Smart. He says, “I’m going to give you 1,000 now and then I’m going to give you 5,000, 5,000, 5,000 and 4,000. That adds up to 20,000.” The last guy is Mr. Justright. He agrees to put down 2,000, make three payments of 5,334 as the work progresses, and pay 2,000 when the work is completed.

The contractor signs up all five homebuilders. Which house does he start on first? You can be sure he does not start on Mr. Quickdeal’s house. Quickdeal would be the last one he starts because he already has 10,000 without doing any work. And he’s not going to start with Mr. Stingy’s home first because he’ll receive only 2,000 up front and must then complete the job before he receives another cent.

The point to remember is that you have to position yourself somewhere between too stingy and too generous with your contractor. Both the Mr. Reasonable and Mr. Smart deals are all right but we prefer the arrangement made by the last one, Mr. Justright. It does three things: (1) it brings and keeps people on the job, because as they work they receive instantaneous reward, (2) it never gives the contractor more than ten percent of the contract price at a time—any more would be providing capital for the contractor (which should be unnecessary), and any less would make him think you are stingy, and (3) at the end, it does not hold back a large sum and give him the feeling he will never be paid. Holding back at least ten percent assures that he will finish the job. This is the 10/80/10 rule, which is the best payment schedule—never more or less than ten percent to begin with; never much more or less than ten percent at the end; and the middle eighty percent should entail as many payments as practicable. This will keep the contractor’s morale high. It is very important to establish a good rapport with your contractors. Frequent payments for work performed will do more to get your home built quickly than any other incentive or contract provision we know. Overpaying or underpaying will increase the likelihood that your contractor will avoid your job site. He’s going to go somewhere where he gets paid when he does some work. A fair payment program is the most effective way we know to keep the contractor(s) on the job.

You will find that almost all contractors are licensed, bonded and insured. But you should check to make certain that they are properly certified. The contractor should have two licenses—a trade license and a business license which authorize him to perform his trade in your county. A trade license is granted him by the authority that regulates his trade, and it is very important. A business license is a permit to operate a business in that county. From your standpoint a business license is not as important as the license for his trade. You should make certain that the plumbers’ association in your area certifies that he knows how to plumb.

You also need to know for how much and for what he is bonded. A bond for 1,000 isn’t going to help you much if he can’t perform. The word “bonded” on the side of a truck does not really mean much. However, if you pay him for his work and materials on a reasonable draw schedule, the you don’t have to worry about whether a contractor is bonded. If he isn’t overpaid and doesn’t finish the work your loss will be the administrative effort to find another contractor rather than a financial loss for paying for work not done.

The legal term quantum meruit means that a person is entitled to be paid a reasonable amount for the work that he has done even if he doesn’t complete the entire contract. It makes no difference whether you fire him or he quits. If a plumber contracts to plumb your house for 5,000 then quits (or gets fired for cause) after he’s done half of the work, do you owe him money? The answer is yes. You owe him for that portion of the contract he has completed. But, if he has done half the work does he get 2,500? Probably not. You only owe him the difference between what it will cost you to have the job completed and 5,000. When someone quits halfway through a job the new person will probably charge more than half the total amount of money to complete the job.

When a person breaches a contract the aggrieved party has an obligation to mitigate (minimize) the damages that result from that breach. In the above example of the plumber who quit after completing half of the work you must make reasonable efforts to find someone to complete the job for the best price possible. (Remember, the first plumber gets the difference in the contract price and the completion price.) You cannot take advantage of the first plumber by agreeing to pay 4,000 to complete the job if the second plumber would have done it for less. Also, if the first plumber has left his material or tools out in the weather you must make a reasonable effort to keep them from being damaged. Even if you’re upset with him you are legally responsible for mitigating (minimizing) his damages.

As we have said, most people sell their homes within eight to ten years. Hence, sooner or later, you’ll probably need to know something about listing contracts. A listing contract is an agreement between you and somebody who is going to sell your property.

There are essentially four types of listing agreements. The first one is called an open listing.

An open listing is one in which you contract with a realtor or broker and permit him to sell your property. If he sells your property he gets a commission. But the open listing also permits two other arrangements: (1) You can sell your property yourself, and (2) another broker or realtor can also sell your property. You could enter into an open listing with three or four brokers or realtors.

An open listing specifies that anybody who has an agreement with you can sell your property. Of course the selling agent must be a realtor or a broker under the law. You cannot just have anybody sell your property who wants to do so, except for yourself. You can sell your own property whether or not you are a realtor or broker.

An exclusive listing gives only one realtor or broker the authority to sell your house. But it also permits you to sell your house. There is a big difference in this agreement and the third example below.

The exclusive authorization to sell is an agreement wherein the broker or realtor gets the commission from the sale of your house regardless of whether he sells it, you sell it, or John Doe sells it. What usually happens with exclusive authorization to sell is that the broker or realtor who is given the exclusive authorization then places your house in what realtors call “multiple listing.” This means that any recognized real estate agency in the area can sell the house. The commission is then split between the selling agency and the agency that was given the exclusive authorization. If that agency sells the house it takes the full commission. The difference between exclusive agency and exclusive authorization is that in the former you can sell your home without paying a commission.

A net listing is when a broker or real estate agent agrees to sell your property and give you a net amount from the proceeds. If you want to sell your house for 100,000 net and you net list your property with a realtor for 100,000, that gives the realtor the opportunity to sell it for 120,000, or 101,000, or any other amount. The realtor or broker then keeps the amount in excess of the 100,000. A net listing is frequently frowned upon by realtor associations and is actually prohibited in some states. Obviously, it is not recommended unless you want to encourage a massive effort on the part of your realtor or broker to dispose of your property.

Listing agreements are usually made for a specific time period or until the house is sold. The seller specifies how long the listing will last—thirty, sixty, ninety, one hundred-twenty days, or even a year. A listing agreement is a binding contract as long as the realtor is putting forth an effort to sell your house. However, if you’re not satisfied most realtors will let you out of a listing agreement after a reasonable length of time although they are not obligated to do so.

Most listing agreements state that not only will the broker be paid a commission if the house is sold during the time frame of the listing agreement, but that if the broker has introduced somebody to your house, and that person subsequently buys your house within a secondary predetermined time frame the broker still gets a commission. The reason for this is obvious. If someone comes to your house on the eighty-ninth day a ninety-day listing and says, “I’m thinking about buying,” you could say, “Don’t buy today! Tomorrow my listing agreement is up and you can come back and buy it from me for the listed price minus the realtor’s commission.” The listing agreement protects the realtor in that situation.

In most contracts you’ll find legal expressions and terminology. Some are very important, and you should be aware of what they mean.

An agreement between two or more parties where a party agrees to pay a sum in excess of the actual damages in the event of nonperformance. Often confused with a liquidated damages provision, a penalty clause is unenforceable. For example, if a general contractor agrees to pay an owner 1,000 a day for every day of late delivery and the actual damages to the owner are less than 1,000, the clause is unenforceable.

A damage amount predetermined by the parties in the event of a breach. An example of liquidated damages would be one in which the purchaser forfeits his deposit when he fails to settle on the contract. Another example would be a provision whereby the contractor agrees to pay the owner the sum of 100 per day if the home is not completed by a predetermined date. If the 100 is a good estimate of the potential damages then it is a permissible provision. If the figure was 1,000 and was out of line with the potential damages, then it would be a penalty clause and therefore unenforceable.

Whether you call the provision a liquidated damages clause or a penalty clause is immaterial. The effect is the controlling factor. The breaching party can only be held liable for the actual damages. Damages in excess of actual damages are penalties and will not be enforced. Don’t attempt to spur performance by including damage sums in excess of your potential damages, as it will only backfire on you.

This is a legal term and it means, among other things, that if you’re supposed to settle on a property at 12:00 noon on April 21st and you show up at 1:00 P.M., you’re out of luck! What if your husband or wife died on the way? Is that a defense? No. It doesn’t make any difference what happens, if it says 12:00 noon on April 21st, and you don’t close by then you lose your deposit, you lose the property, and you lose the deal. If you’re the buyer, you may want to delete this phrase because it puts you under an ironclad deadline to perform. If you’re a seller, of course, then you may want to include it.

As we shall discuss later, there are certain kinds of warranties, expressed, implied, and statutory involved in a contract. However, when you purchase something with the wording “as is,” then all warranties, expressed or implied, are waived. It is a legal term and whether it relates to a new house, a used house, a vehicle, or a toaster, it eliminates any warranties.

A Latin phrase that translates as “let the buyer beware.” There may be situations in both real estate and contract law when you should be aware that you’re not covered by all the protections you might expect. In this case you are usually forewarned by the term “caveat emptor.”

You will see the word “substantial” in contracts, and it’s not a bad word. The building of a house is an imperfect process. Don’t expect that every 2 × 4 is going to be perfectly straight or every shingle perfectly flat. When the contract says that the builder or plumber or electrician will perform in substantial compliance to the plans and specifications, don’t be too concerned. It merely means that building the house is not a perfect process and the house will be built in substantial compliance. For example, if the plans call for a house to be 44 feet by 28 feet in exterior dimensions and the house is 44 feet by 28 feet ¼ inch, that is substantial compliance. If the contract said it was to be built in substantial compliance with the plans and specifications you wouldn’t be able to avoid paying the contractor because of that quarter-inch difference.

This means the work will conform to the standards of the industry in your area. If a builder or subcontractor says, “Don’t worry about my work because the county’s going to inspect it,” don’t accept that. The county does not inspect for quality control, and it won’t involve itself in a dispute between you and a contractor over the quality of the work. The county will look at the work from the point of view of compliance with building code regulations (for example, how deep the footings are) but not the workmanship.

“Reasonable” means that people of average intelligence within the community would perceive the facts to be fair and equitable to all parties.

This is an important term which is best explained by citing an actual case, Hadley v. Baxendale. A large wheel broke causing a mill to shut down. The mill owner called a transportation company to take the wheel back to the manufacturer for repair. The transportation company picked up the wheel, hauled it off to the manufacturer, had it repaired, hauled it back to the depot, and then lost the wheel! The mill owner then sued the transportation company for losing the wheel.

The cost of the wheel was around 1,000. The mill owner also sued the transportation company for the lost profit associated with all the flour it could have made while that wheel was gone.

Losing the wheel is called direct damages. You lost your wheel. It’s worth 1,000. You’re entitled to 1,000. What about the lost profits?

The lost profits are called consequential damages. The mill owner could not win consequential damages because the transportation company couldn’t foresee that the absence of the wheel meant the mill owner could not grind the flour. It could have logically assumed that the mill owner had another wheel available.

The mill owner could have told the transportation company, “Take this wheel to be fixed, because I’m losing money every day that it’s not fixed,” and the transportation company might have said, “I may lose that wheel. If I lose the wheel, I’m not only going to have to pay for the loss of the wheel but for the loss of the profits, so I’m going to charge you more for transporting it.” If the mill owner had told the transportation company about the potential consequential damages and the transportation company agreed to take on the task, including in its price the risk that the transportation company was concerned about in lost profits, the mill owner would have been entitled to the consequential damages.

In most contracts concerning the building of a home, in the event of a breach (specifically late delivery or late performance) the owner would be entitled to direct damages; but it’s highly unlikely that he would be able to obtain any consequential damages such as rent or lost profit.

“Mitigate” means to soften the negative impact of a breach. In contract law the non-breaching or aggrieved party (the party that suffers under a breached contract) has an affirmative obligation to mitigate his damages. If a person has sold a piece of property and the buyer backs out the seller of the property has an affirmative obligation to take reasonable measures in order to try to sell the property to someone else. A landlord who has a tenant who walks out on a lease must take affirmative action to try to rent the property and at least mitigate or lessen the impact of the breach.

A fixture is an item affixed to a house or a piece of property. If it is permanently affixed it becomes real estate. Examples of fixtures in a house would be a radiator, wall-to-wall carpeting, plumbing fixtures, or a hot water heater. These things could be detached but only with a great deal of difficulty. Since they are permanently affixed and an integral part of the house, they are termed fixtures. As fixtures they are real estate, and as real estate they are governed by a different type of law than personalty.

“Personalty” are items such as furniture and clothing. It should be clearly understood that when you buy a house from someone you don’t get the furniture and you don’t get the clothes. But some things are not so clearly understood. For example, draperies that can be easily removed are likely to be considered personalty and not fixtures. Venetian blinds, on the other hand, have been interpreted to be fixtures because they are permanently affixed.

When you enter into a contract to buy real property you take title to all the real estate but you don’t take title to the personalty. You take title to real estate by virtue of the deed. You take title to personalty by a bill of sale.

The instrument under which you sell and purchase and subsequently take title to personalty, as distinct from real estate.

If you own a house you have an insurable interest in that house because if the house burns down you have a loss. If you have a spouse you have an insurable interest in that person because the loss of that person would be detrimental to your physical, emotional, and financial well-being. You have an insurable interest in a business partner provided the loss of that business partner would have an adverse impact on your income. You must have an insurable interest in real estate, personalty, or an individual in order to obtain insurance on that realty, personalty, or individual.