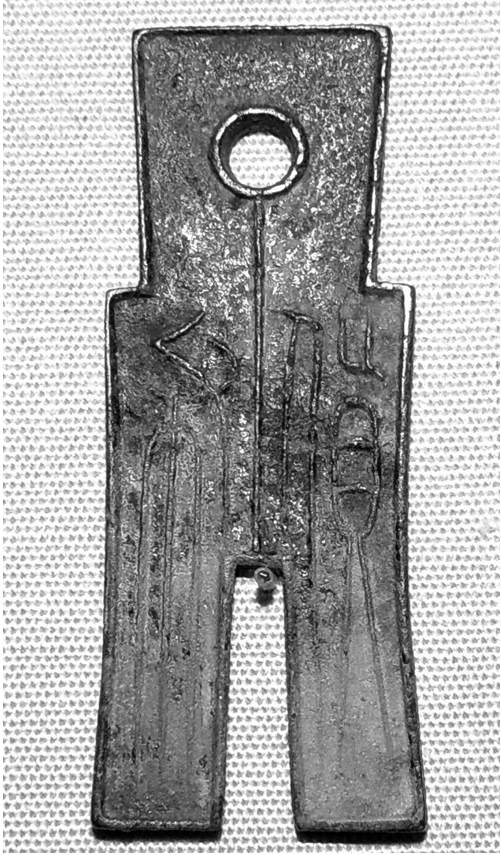

Chinese bronze hoe coin (early 1st century CE )

The simplest way to trade goods is to barter. In barter, goods are exchanged and no money is involved. The goods may be raw materials such as grain, manufactured items such as pots, or services such as labour or story-telling.

But barter is a highly inflexible system, as it relies on each of two traders having exactly the goods that the other wants. There is little evidence that barter was ever used systematically in societies without money or credit. It seems more likely that once humans started to regularly trade goods they would soon have moved on to agreeing to keep a tally of goods exchanged so that the seller of a good could retain a ‘credit’ for later use.

Both money and credit arose for this reason. Credit, at its simplest, is a record of how much one party ‘owes’ to another. Money is anything that has a generally agreed value, and lets credits be transferred between parties. What matters is that sellers can go to market and ask for a certain sum for their goods, in the knowledge that they can use that sum to buy different goods. Money also makes it easier to store wealth, or to borrow it.

Where there was trust within a trading community, and no need to carry money over distance, a simple tally system or valueless tokens could be used. But where there was less trust, or trading over longer distances, other solutions were needed. One early record of credit was the tally stick, a notched stick broken in half, with the creditor and debtor taking one half each (since no two sticks break the same way, it was easy to check that there was no foul play). Some societies also chose to use objects with some intrinsic value or rarity for money, since items with intrinsic value could be used even if not accepted as money, and rare objects were harder to fake. These might be tokens made from precious metals such as silver and gold, but there was a variety of earlier forms, including rare seashells (valued for their use in jewellery), useful tools, wheat and cattle.

Chinese bronze hoe coin (early 1st century CE )

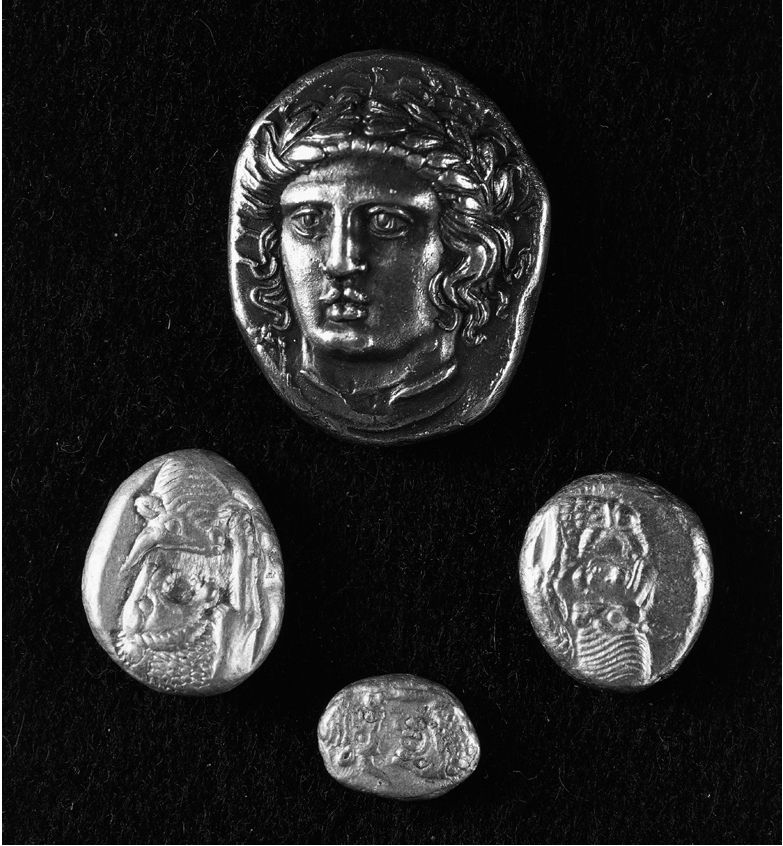

Shell money has been used at various times on virtually every continent. Cowrie shells served as tokens of exchange around the Indian Ocean as early as 1200 BCE , and shell money was still legal tender in parts of West Africa through to the mid-19th century. In China, cowries were such important tokens of exchange that the classical Chinese character for ‘money’ or ‘currency’ derives from a pictograph of a cowrie shell. As time went on, people living some way from the coast could not obtain enough cowries for their trading needs, so began to make token versions out of available materials such as horn, bone, stone, clay, bronze, silver and gold.

Around 1100 BCE the Chinese had adopted another system of tokens. These were miniature replicas of tools and weapons – previously valuable barter items – cast in bronze. But the sharp points of miniature hoes, spades, daggers and arrows made for awkward handling, and as time went by these items came to be represented by metal discs.

The first ‘proper’ coins, however, were minted on the other side of Asia, around 560 BCE in the kingdom of Lydia, in what is now Turkey. They were made from a mixture of gold and silver called electrum, and were stamped with the seal of the king, as a guarantee of value. As the metalworkers advanced in skill, they added more details, to demonstrate that each coin had the same metal content and the same weight. What counted about money, they realized, was that people must trust it.

The intrinsic value of a monetary token is rarely as high as its exchange value. Cowrie shells and gold and silver have a certain value, based on their decorative possibilities, but their use as currency enhances their value. Currencies that use everyday commodities are more rare. A notable exception was the wheat currency of the ancient Egyptians. For millennia they based a complex banking and financial system on wheat, which, as a staple food for the whole population, had an instant and significant intrinsic value. In many parts of the world, such a monetary system would not be possible, because of the unpredictability of harvests, but the annual flood and the dependable soil of the Nile valley meant that the Egyptians could rely on wheat as a stable – if bulky – currency.