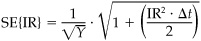

1This assumes that all the error arises from the estimated mean residual return. If we also account for the error arising from the estimated residual risk, we find

where Δt is, e.g., 1/12 if we observe monthly returns. See Problem 3 for more details.

2See Problem 4 for a discussion of why changing the information ratio from an annualized number to a monthly number does not improve our ability to statistically verify investment performance.