Steps 5 and 6: Net Profitability Calculations

Introduction to Net Profitability

The next steps are to collate all statistically-estimated effects, (described above),

with any other financial information, such as one-off costs.

If an analysis has both cost and revenue implications, you can combine these into

a profitability analysis. The following sections discuss aspects of such profit calculations.

Basic Profit

As you no doubt know, basic profit is calculated as revenue minus cost. Your first

point of interest would be to ensure that the outcome of your statistical analysis

is a positive profit. In many business situations, just having positive profit is

not necessarily good enough – you would want your profit to be high enough to beat

a cost of capital that is relevant to your business or the project involved.

Breakeven

Breakeven is the idea that you can calculate the conditions that achieve a minimum

level of profit, generally conditions that at least lead to zero profit. In other

words, analysts usually consider breakeven to have occurred at Profit = 0, although

as discussed in the previous section, sometimes a breakeven may be Profit > 0 to cover

a cost of capital.

Now, if your analytical analysis allows you to define an equation for profit, then

you can often calculate the conditions that achieve breakeven. Say, for instance,

that production levels are your variable of interest. If you know the price, the fixed

costs and the variable costs of production perhaps your simple profit equation is:

Profit = (Production levels * Price) – Fixed costs – (Production levels * Variable

cost)

If breakeven occurs at zero profit then perhaps you are interested in calculating

the production levels required to achieve this. So:

(Production levels * Price) – Fixed costs – (Production levels * Variable cost) =

0

Breakeven production level = Fixed costs/(Price – Variable cost)

See the example in Some Simple Examples of Business Extrapolation below for an illustration of a breakeven calculation.

Note that in some cases, organizations would demand a minimum cost of capital that

requires a higher-than-zero breakeven. Your finance courses would no doubt have taught

this principle.

Return on Investment

Introduction to ROI

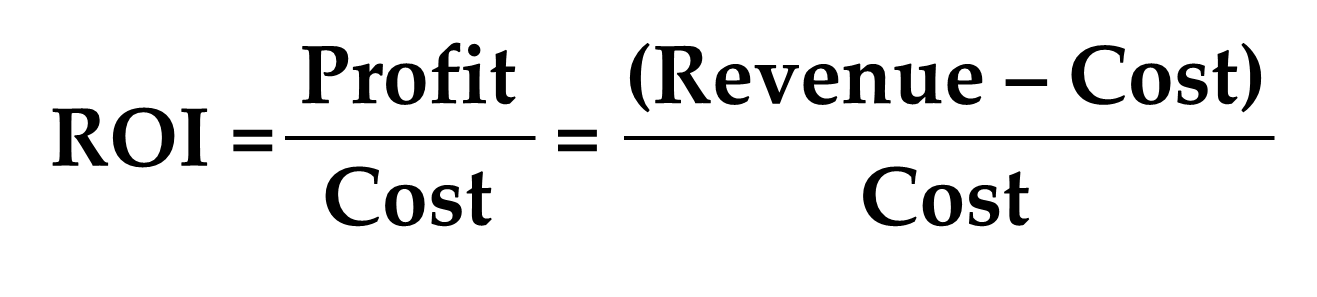

Return-on-investment (ROI) is perhaps one of the most popular and important concepts

in modern business. It is a ubiquitous yet simple financial concept that expresses

how efficiently a certain business activity translates input money into profit. ROI

gives us a generic way of measuring this. The formula is as follows:

As can be seen, ROI is a ratio. As with all ratios, when it is reduced to a single

figure then it expresses how many of the numerator to every one of the denominator.

Note that the numerator is profit and the denominator is costs. The following section

expands on the meaning of the ROI.

ROI Example

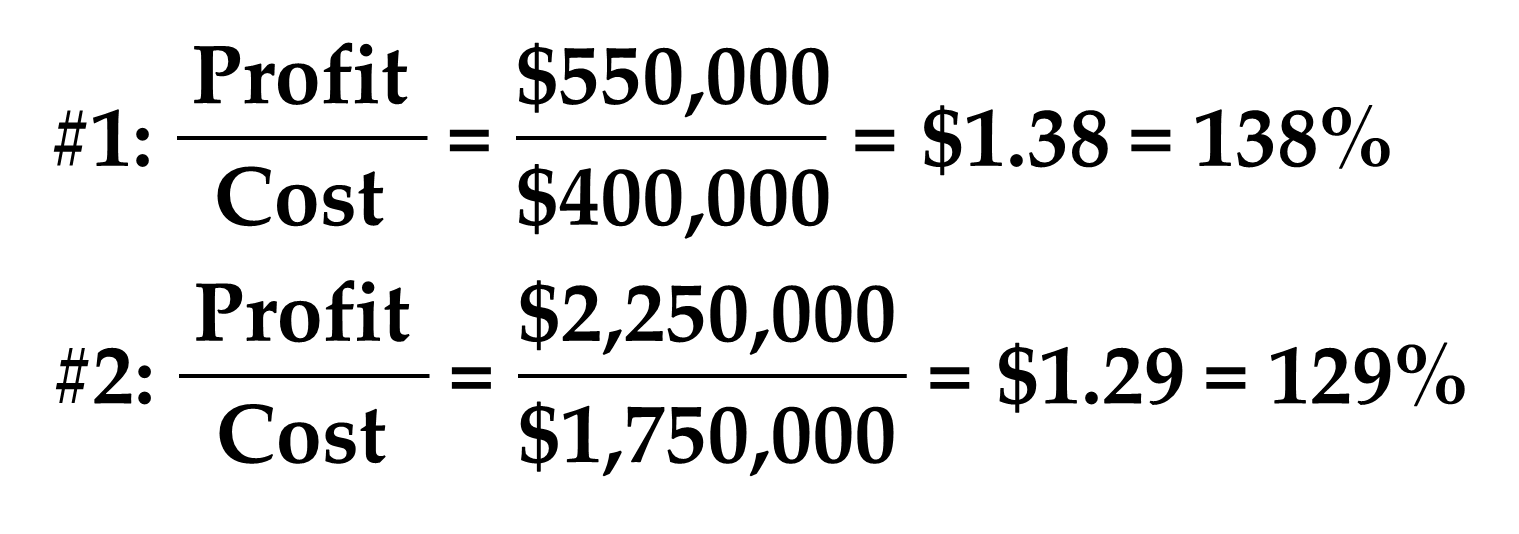

Say that you have two projects. The first project cost $400,000 and made an estimated

$950,000 in revenue (i.e. $550,000 in profit). The second project cost $1,750,000

and made an estimated $4 million in value (i.e. $2.25 million in profit).

The ROI estimations of the two are as follows:

Interestingly, even though the second program made considerably more profit in absolute

terms, it has a smaller ROI. The first one made $1.38 for every $1 invested; the second

made only $1.29 per $1 invested. Therefore, the first program made more efficient

use of every dollar invested, and is the more profitable program.

One can also express ROI as a percentage, by multiplying it by 100. If you do this,

then it expresses the rate of return you are achieving over and above expenses.

Expressing ROI as a Percentage

For example, an ROI of 145% (which would correspond with an ROI of $1.45) is a 145%

rate of return on expenses. This can be compared with the project cost of capital:

the criterion would be that the ROI percentage should exceed the cost of capital.

Most of you have probably studied ROI in a previous finance course, but the point

of discussing it here for business statisticians is that ROI can often form the final

step of an extrapolation from statistics to business outcomes.