Figure 14.1. Two-sided platforms.

How Digitization Is Changing Everything

We increasingly shop and do our banking online, read our news on websites, use Uber, carpool using BlaBlaCar, and reserve accommodations through Airbnb. The digitization of society is at the heart of economic and social changes in the twenty-first century. It will have an impact on all human activities, just as it has already changed trade, finance, the media, and the travel and hospitality industries.

Everyone will have to adapt, including some surprising organizations. Confronted by the decline of the press and the traditional media, in 2014 National Public Radio (NPR) in the United States transformed itself into the Spotify of radio: its app NPR One asks you to rate its programs, examines the length of time you spend listening to each of them, analyzes your podcast downloads, and eventually provides you with tailor-made programming suited to your interests. This is only the beginning. Digitization will turn insurance, health care, energy, and education upside down. Professional medical, legal, and fiscal services will be transformed by intelligent algorithms based on machine learning,1 just as robots will transform a number of other services.

Economic interactions are only one dimension of this change. Digitization influences personal relationships, civic life, and politics. Businesses are preoccupied by the way the structure of industry is changing, by changes in the nature of work, and by fears about cyber-security and ransomware. Digitization has an impact on intellectual property rights, competition law, labor law, taxation, and regulation in general. The digital economy is bringing extraordinary technological progress that is giving us better health, as well as more time and purchasing power, but it also creates dangers we cannot ignore. The goal of this chapter and the one that follows is to analyze a few of the biggest challenges so that we can understand better and prepare ourselves for this profound transformation of business, the world of work, the system of regulation—in short, society in general.

This chapter focuses on the strategies of digital companies, and the challenges involved in regulating these markets. Two-sided platforms are the hub of the analysis. They enable different sides of the market (we might call them “supply” and “demand,” or “sellers” and “buyers”) to meet and interact. They are large and growing in their importance. Today (August 2017), the five largest global companies (by market capitalization) are two-sided platforms: Apple, Alphabet (Google), Microsoft, Facebook, and Amazon. Seven of the ten largest startups are also two-sided platforms. This chapter will analyze their business model and consider whether these businesses are making us better off.

PLATFORMS: GUARDIANS OF THE DIGITAL ECONOMY

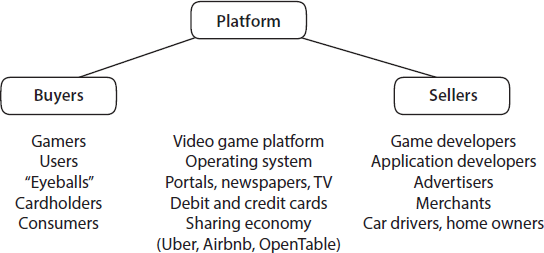

Your Visa card, your PlayStation, the Google search engine, the instant messaging service WhatsApp, and the real estate agent on the corner have more in common than you might imagine. They are all examples of “two-sided markets.”2 That is, a market in which an intermediary (Visa, Sony, Alphabet, Facebook, the real estate agency) enables sellers and buyers to interact. These “platforms” bring together different communities of users seeking to interact with each other—for example, players and developers of games in the case of the videogame industry; the users of operating systems (Windows, Android, Linux, or OSX on your Mac or iOS on your iPhone) and application developers; users and advertisers in the case of search engines and media; or holders of bank cards and merchants in the case of card transactions. These platforms bring both groups together and also provide a technological interface allowing them to interact. Which is worth a little further explanation.

THE ECONOMICS OF ATTENTION

For a long time, economists assumed economic progress meant inventing new products, producing them at lower cost, and trading them more efficiently by reducing transaction costs, often the transportation costs and customs duties that hindered international trade (empirical studies testing “gravity models” of international trade show that levels of trade between and within countries rise as transportation costs fall).

Fifty years ago, someone who wanted to read or listen to music could access only a limited number of references. A reader bought a newspaper for information about current events. To read a book or listen to a record, the reader was restricted to the catalogue of the local library. A wealthier household might put together a proprietary library, but it would be relatively small. When shopping, consumers were limited to their neighborhood stores. Someone who wanted to make friends or find a partner was dependent on relationships in the village or community.

In contrast, the cost of sharing information and transporting a digital good from one side of the planet to the other is almost zero. Catalogues are now limitless. While, for many millennia, our ancestors had trouble finding trading partners, now our problem is identifying, among the millions of partners with whom we could trade, the one that best corresponds to our expectations. We suffer from too much choice, not too little. Our problem now is how best to allocate time and attention to this plethora of potential activities, trades, and relationships. The economics of attention fundamentally changes behaviors and interactions. We need the combined insights of economists, psychologists, and sociologists to understand the consequences.

Thus, the most significant transaction costs are no longer transportation costs, but rather assessing what is on offer and choosing who to do business with, along with the signaling costs (seeking to convince potential trading partners of one’s reliability). Our almost infinite sources of information, and the limited time we have to process and understand them, put the intermediaries and platforms that help us find these partners at the heart of the economic process. The more the other costs (transportation, customs duties, listing) fall, the more important costs associated with signaling, reading, and selecting become, and the more we need sophisticated platforms to match the buyers and sellers.

These platforms supply precious information about both the quality of what is on offer and who would be the best match, by communicating the reputations of vendors (the ratings of hotels on Booking.com, resellers on eBay, or Uber drivers) and providing advice about the products best suited to our tastes (through recommendations on Amazon or Spotify). They put us in contact with partners who are either more reliable or just better suited to our needs. They enable us to find a way, at low cost, through the maze of offers.

What is known as the sharing economy falls into this category. Its logic is to take better advantage of underused resources: apartments (Airbnb), private cars (Drivy or UberX), private planes (Wingly), or empty space on car trips (BlaBlaCar) or delivery vehicles (Amazon On My Way, You2You). But intermediaries are necessary to help each side identify what they would gain from taking part—for example, the trade between a tourist looking for a particular type of apartment on a particular date, and a householder who will be away from home at that time and wants to earn extra income. The user lost in a gigantic maze of information will need to trust the intermediary: trust the impartiality and quality of the recommendations, have confidence that personal data will be protected and deleted when promised, and believe that this data will not be transmitted to third parties. I will return to these points in the next chapter.

The ease of finding suppliers leads to trade that would otherwise be unimaginable. It often also causes prices to fall by putting suppliers in competition with each other. This is not always the case, however. Glenn and Sara Ellison at MIT have shown that the prices of rare secondhand books, for which there is little demand, are often more expensive online.3 Those who are actively searching for “niche products” like these are prepared to pay a lot to acquire them, whereas those who come across them by chance in a bookshop or a garage sale tend not to be prepared to pay as much. The higher price online is not necessarily a sign of economic inefficiency, however. Without search engines and platforms, the buyer would probably never have been able to find the rare book.

TECHNOLOGICAL PLATFORMS

Unlike Google, eBay, or Booking.com, payment card platforms such as PayPal or American Express do not put sellers and buyers in direct contact with one another: instead, they work on the basis that we are already engaged in a transaction with a merchant, and are simply looking for a way to pay rapidly, safely, and without having to go to an ATM or make a bank transfer.

Similarly, we do not need PlayStation or Xbox to inform us about the products the videogame developers have designed for their consoles. There are independent information channels (including advertising, reviews in newspapers, displays in stores, and keywords on Google’s search engine) to tell us about new games. Rather, the consoles manufactured by Sony or Microsoft allow us to play the videogames developers design in the same way Windows allows us to use applications, commercial or not, compatible with the software on our computers. More generally, a second function of platforms is not so much to match and recommend buyers and sellers who would not know about each other, but rather to supply a technical interface so as to allow interactions to be as smooth as possible between users; in the same spirit, Skype or Facebook allow us to stay in contact with our family and friends through a convenient and congenial interface.

TWO-SIDED MARKETS

The economics of two-sided markets provide a theory that sheds light on the behavior of companies in all these—apparently disparate—markets. This theory is regularly used as much by management consultants as by competition authorities.

THE BUSINESS MODEL

These platforms have two communities of users, and the challenge is to find a viable economic model that ensures that both participate. Every two-sided platform faces a chicken-and-egg problem. A manufacturer of videogame consoles must attract both players and developers of videogames. Players want a wide choice of games, while developers want to reach the broadest possible market. The console manufacturer wants to stimulate enthusiasm on both sides. Media organizations (newspapers, television channels, websites) have the same problem, because to create a sustainable business model they must capture the attention of audiences and also interest advertisers. For payment systems such as American Express, PayPal, and Visa, the goal is to attract consumers and simultaneously ensure that merchants will accept their method of payment. All these activities make it essential to get two categories of customers onboard by taking advantage of their respective interests.

After a certain amount of trial and error, a new business model has emerged. I will use the language of economics to explain it first before turning to some familiar examples. The economic model depends on the elasticity of demand and on externalities between the different sides of the market. First, for each side of the market, the elasticity of demand is a measure that reflects how many users (in percentage terms) the platform loses when it raises the price by 1 percent. In all industries, two-sided or not, the elasticity of demand is a key concept when it comes to setting prices. A high elasticity of demand enforces price moderation, whereas a low elasticity encourages price increases. This is a theoretical concept, but it corresponds to everyday business experience and explains why competition generally makes prices fall: in increasing its price, a business will lose more customers, because they can defect to its competitors rather than just stop consuming.

Second, and more specific to two-sided markets, users benefit from the presence of those on the other side of the market—there are externalities between the two groups. If one side of the market benefits a lot from interactions with the other side, then the platform can charge more to the former and, in a “seesaw” pattern, will want to charge less to the latter side to make it attractive to join. The platform provider thus needs to know which side of the market is most interested in the service (has the lowest elasticity of demand, and is therefore likely to pay more without ceasing to consume), and which side brings more value to the other side.

Platforms often grow thanks to very low prices on one side of the market, which attract users on that side, and indirectly enables the platform to earn revenues on the other side. The structure of prices between the two sides of the market takes full advantage of the externalities between them. The basic idea is simple: the real cost imposed by a user is not the straightforward actual cost incurred in serving them. The user’s presence creates a benefit for the other side of the market, which can be monetized—thus, de facto, reducing the cost of serving this user. In some cases, one side of the market might not pay anything, or might even be subsidized, the other side paying for both. Many newspapers—particularly free papers like Metro and 20 Minutes—, radio stations, and websites do not ask their audiences to pay anything in exchange for the information and entertainment they supply. All their revenue comes from advertising. The PDF software for reading a file can be downloaded free of charge, but anyone who wants to create more than a very basic PDF file must pay for the professional version of the software. Why? Because the person who writes and distributes the document generally has a greater desire to be read than a potential audience has to do the reading. In contrast, readers of books willingly pay for a best seller.

Similarly, users of Google benefit from its numerous free services (search engine, email, maps, YouTube, and so on). The presence of the users (along with the information obtained during searches, from sent emails, and through other activities on the Google platform, as well as the information collected by other websites and purchased from data brokers) attracts advertisers, who can present their wares on the platform in a targeted way. Advertisers pay very large sums for this privilege.4 This model is often replicated by platforms in other sectors. For instance, OpenTable, an online restaurant reservation firm that manages twelve million reservations per month, does not make consumers pay—but charges restaurants one dollar per guest.

The payment cards sector is particularly interesting. When a consumer makes a payment by American Express card, American Express makes a profit from the commission it charges the seller—say, between 2 and 3 percent. This commission, also called the “merchant fee,” is deducted from the purchase price (a bank that is a member of Visa or MasterCard also receives a percentage of the transaction, but indirectly through the “interchange fee” paid by the merchant’s bank to the cardholder’s bank). This explains why cards are often provided for free (or even at a negative price if they also give air miles or rebates in cash to the card user). The business model consists in providing consumers with cheap debit or credit cards and making merchants pay a percentage on each transaction. Even though the merchant fees are high (0.5 to 2 percent for Visa and MasterCard, around 3 percent for PayPal) the merchants have an interest in accepting the cards, because otherwise they risk losing customers. This is especially true for American Express, which benefits from an up-market image and many business clients, allowing it to charge higher commissions.

As we have seen, platform price structures are often favorable to one side of the market and very unfavorable to the other. Are these predatory prices (that is, abnormally low) or abusive prices (abnormally high)? It is far from clear—even companies that are not at all dominant in their markets (unlike Google) use this kind of price structure. We will return to this when discussing competition policy in two-sided markets.

WHEN THE EGG COMES BEFORE THE CHICKEN …

Two-sided platforms have another problem if one of the sides using them needs to invest before the other side arrives in the market. In this case, expectations matter. For example, when a new videogame console is launched and there is no established customer base, independent game developers start work well before they are assured of the console’s success. They assume the risk of developing (at great cost) videogames created for a platform that might not attract enough customers to make their investment profitable. To reassure developers, the console manufacturer generally announces that it will levy a royalty of five dollars to seven dollars on each game sold. These royalties increase the platform’s stake in a wide diffusion of the console, and so will encourage the platform to put consoles on the market at a low price to attract new users: the platform gets not only the console’s sale price, but also some commission on the subsequent sales of games. By contrast, if the platform’s only source of revenue came from selling consoles, it would sell them at a high price, way above the manufacturing cost. Few consumers would buy the console and the game developers would sell few games. The royalty levied on the sales of games gives the platform some skin in the game, so to speak, and somewhat aligns the platform’s incentives with the interests of game developers, who are then reassured that the console will not be too expensive.

Table 14.1. Asymmetric but Efficient Pricing

Low price side |

High price side |

Consumers (search engine, portal, newspaper) |

Advertisers |

Cardholders |

Merchants |

Indeed, console manufacturers such as Sony or Microsoft often sell their consoles at a loss of up to a hundred dollars per unit.5 Given this assurance, game developers may be willing to create titles long before the console is on the market. The platform can also develop its own games before the console goes on the market, as Microsoft did with Halo when it launched the Xbox in 2001.

The example of videogames is an extreme one because one side of the market lags far behind in adopting the platform. But the same problem is found elsewhere. Microsoft’s Halo strategy, in which the company produced its own applications when it did not yet have a large user base, is frequently used. When the iPhone was launched in 2007, Apple did not yet have its App Store, so it produced its own applications. Netflix now produces its own programs and offers them in addition to the films it has bought from external content providers. A recent book by David Evans and Richard Schmalensee describes the importance of getting timing right in two-sided market strategies.6

COMPATIBILITY BETWEEN PLATFORMS

In many cases, consumers in these two-sided markets can choose between several platforms. Should the platforms cooperate so that they are all interoperable? In telecommunications, this cooperation is mandated by regulation. It is unthinkable that a subscriber to one mobile phone network would not be able to call a friend who has subscribed to a different one. But interoperability may be voluntary: real estate agencies often share listings to provide more choice for all their customers.

Other platforms choose not to be compatible. It is not possible to pay a merchant who accepts only Visa and MasterCard with an American Express card. An application written solely for Windows cannot be used with the Linux operating system. Incompatibility may lead users on one side of the market to increase their opportunities to engage with more users on the other side by joining several incompatible platforms, a practice called “multihoming.” This happens, for example, when consumers have several payment cards, or when merchants accept different cards. Videogame developers can port the same game to different console formats. People wishing to buy or sell an apartment can approach several agencies simultaneously if the agencies do not share their listings.

Applications for mobile phones are another example. This is a market characterized by a fairly stable Apple-Android duopoly.7 As one might imagine, multihoming is most widespread for the most popular applications. In this case, the application needs to be developed for each operating system, and the cost of marketing must be duplicated too—it is important for an application to be among the “most popular” of the ecosystem to be noticed by consumers. The same four applications are the most popular on both systems (Facebook, Pandora, Twitter, and Instagram). More generally, 65 percent of multihomed applications are found among the most popular.8

This kind of behavior has an influence on the choice of business model. User multihoming influences the way platforms set their prices. In the United States, for example, American Express had to cut the commissions merchants pay it following the appearance in the early 1990s of no-annual-fee cards on the Visa and MasterCard platforms. American Express’s customers decided it was better to have a second payment card that cost nothing, which they would be able to use if their American Express card stopped working or was rejected by the seller. Then merchants reasoned, “Since my customers with an American Express card now also have a Visa or MasterCard, and these cards charge me less, I can refuse American Express cards without losing or antagonizing the customer.” At that point, American Express was forced to reduce its merchant fees to keep retailers on its platform.

OPENING UP

Sometimes a platform can decide that it will itself act as one of the two sides of the market. Then it conforms to the standard model of the firm, which has only to attract final consumers. Apple is a well-known case.9 In the personal computer market, Apple limited the applications and hardware that would work on its operating system in the 1980s. Apple made the computers itself and set a high price on access to the software development kit, which made it a quasi-closed system. By contrast, Microsoft, with its DOS system (and later Windows), which became dominant in the 1990s, decided very early on to be open10 by distributing development kits almost free of charge and not manufacturing computers itself. Apple has subsequently learned its lesson from this episode of competition between ecosystems, and has opened up (today, there are 1.5 million downloadable applications on the App Store); but it still keeps control not only over its operating systems (macOS and iOS), but also over the manufacture of computers (Mac) and mobile phone hardware (iPhone). Google’s Android mobile phone operating system is more open than Apple’s, even though Google has been accused, as Microsoft was earlier, of limiting access to other competing products.

In addition to the question of possible barriers to entry, to which I will return, the choice of whether to have an open system or not can be analyzed as follows. Apple’s decision to be closed gave it better control over the hardware, but limited consumer hardware choice and raised hardware prices, thus potentially making the Apple brand less attractive. In France, the Minitel, a precursor of the microcomputer, developed a closed model for its applications—and very quickly lost the battle. As we have seen, another consideration is how established the platform is.11 A new platform does not always have a choice; even with an open architecture, it can be led to produce hardware and applications itself, or to sign agreements like the one Bill Gates signed with IBM in the early 1980s (so that IBM computers ran on DOS). It is only with time that platforms get the full benefit of openness.

A DIFFERENT BUSINESS MODEL: PLATFORMS AS REGULATORS

CLASSIC AND TWO-SIDED ORGANIZATION

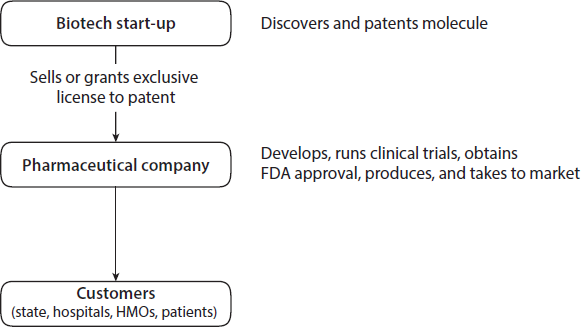

To understand why platforms differ from classic markets, let’s take the example of the “classic” or “vertical” business model of the pharmaceutical industry. Increasingly, innovative drugs are produced by entrepreneurial biotech companies. However, these companies have no comparative advantage in development, clinical trials, securing approval from the regulatory authorities (such as the Food and Drug Administration in the United States), manufacturing, or marketing. So they sell their patents, grant exclusive licenses, or are acquired by a large pharmaceutical company such as Aventis, Novartis, Pfizer or GlaxoSmithKline.

In every case, a single pharmaceutical company will market the drug, because if there were multiple licenses, competition between pharmaceutical companies would lower the price that could be charged, decrease the value of the patent, and so reduce the revenue from licensing it. A biotech firm will therefore take care to create a downstream monopoly that maximizes profits from selling the drug.

Compare the platform model (figure 14.1) with the vertical model (figure 14.2). In the vertical model, the biotech startup has no contact with the end customer, and transacts only with the seller—the pharmaceutical company. The startup has no direct interest in whether the pharmaceutical company sets low prices that would increase consumption of the drug. That does not mean that the pharmaceutical company, which (in contrast) deals with both the startup and the customers, plays the role of a platform: the startup and the customers have no interaction with each other. This distinction between the vertical model and the platform model has important consequences.

Another illustration of the difference between vertical and platform organization is the comparison between a fruit and vegetable market (which is a platform, because the sellers interact directly with customers, but need the marketplace to do so) and a supermarket (where food suppliers have no interaction with customers, but instead sell their products directly to the supermarket, which then retails them to customers). In a fruit and vegetable market, sellers are not only concerned by such things as the conditions for acquiring a stall, or what share of their revenues they have to pay to the market’s owners, but also in whether the market will be able to attract buyers. A supermarket supplier, on the other hand, has a contract to provide a certain number of units at a given price. It does not care how many customers visit the supermarket.

These examples show that platforms are not a phenomenon peculiar to the digital era, even if digital technology has made them pervasive. And the organizational choice (classic vs. two-sided) is not cast in stone: when it began in 1994, Amazon was not a true two-sided platform, but a vertical (although digital) retailer: it bought books from publishers and resold them on the web.

PLATFORMS AS REGULATORS

A two-sided platform interacts both with the seller and the customer. This means that it cares about the customer’s interests. This is not philanthropy. A satisfied customer will pay more to the platform, or will be more inclined to return. This underlies the uniqueness of the two-sided platform business model.

Competition among sellers. The first implication is that, unlike a holder of a pharmaceutical patent, a platform is usually not hostile to competition among sellers. For instance, many operating systems, such as Windows, have built their success on opening their platforms to external applications. These applications are often in competition with each other, and also with applications produced by the operating system owner itself.12 This competition drives down prices and improves quality, making the platform more attractive to consumers. It is as if the platform has granted licenses to several sellers. It is more concerned with protecting the buyer’s interests than the biotech startup of the vertical model.

Price regulation. Similarly, platforms sometimes regulate the prices that sellers can ask. The music sales offered online in 2007 by Apple’s iTunes Store limited the charge for downloads to $0.99 per track and $9.99 per album; likewise, payment card platforms frequently forbid merchants from charging extra for payments by card.

Monitoring quality. To protect their customers, platforms also try to keep undesirable counterparties from accessing the platform. Nightclubs and dating agencies screen their customers at the entrance. Stock markets set solvency requirements (more precisely, they demand collateral) to prevent a member’s bankruptcy from having negative effects on other members. They also prohibit unethical behavior, such as “front running,” a practice close to insider trading in which a broker buys or sells for himself before executing a major buy or sell order for a client. Apple monitors the quality of the applications on the App Store, and Facebook employs numerous people (although perhaps not enough given the concern about “fake news” and other issues) to keep an eye out for offensive content and behavior. Many platforms do not release the buyer’s payment to the seller until the buyer has received the purchased item and is happy with it.

Providing information. Finally, platforms protect users by providing them with information about the reliability of sellers through a rating system. Sometimes they also have a quasi-judicial function by offering conflict arbitration—for example, sites that auction used cars do this.

The sharing economy that we hear so much about these days has adopted all these strategies. A platform like Uber verifies a driver’s background, requires the driver to provide quality service, has users give ratings, and stops drivers with a bad reputation from accessing the platform. Sharing economy platforms also sometimes offer mediation, and guarantee to reimburse dissatisfied customers.

THE CHALLENGES TWO-SIDED MARKETS POSE FOR COMPETITION POLICY

REVIEWING THE SOFTWARE OF COMPETITION POLICY

What should we think about two-sided platforms’ technology and marketing practices? Today, competition authorities in every country face this question. The traditional reasoning set out in competition law is no longer valid. Remember that it is common for a platform to set very low prices on one side of the market and very high prices on the other side. Offering goods at a low price (or even for free) on one side of the market naturally creates suspicion among competition authorities. In classic markets, it could be a predatory act against weak competitors. In other words, it may be a strategy to put rivals out of business by weakening them financially, or simply by signaling the intention to be aggressive. Conversely, a very high price on the other side of the market may suggest monopoly power. But in practice even small firms entering the market, such as a new website or a free newspaper funded by advertising, practice this asymmetric type of pricing. A regulator who does not bear in mind the unusual nature of a two-sided market may incorrectly condemn low pricing as predatory, or high pricing as excessive, even though these pricing structures are adopted even by the smallest platforms entering the market. Regulators should therefore refrain from mechanically applying the classic principles of competition policy where they are simply not applicable. New guidelines for competition policy as adapted to two-sided markets would require instead that the two sides of the market be considered together rather than analyzed independently, as competition authorities still sometimes do.

FAREWELL TO COMPETITION LAW IN THESE SECTORS?

Although applying competition policy to two-sided markets requires care, it would be wrong to conclude that the sectors they serve should be abandoned to a sort of legal no-go zone into which competition law does not venture.

Making Competitors’ Customers Pay …

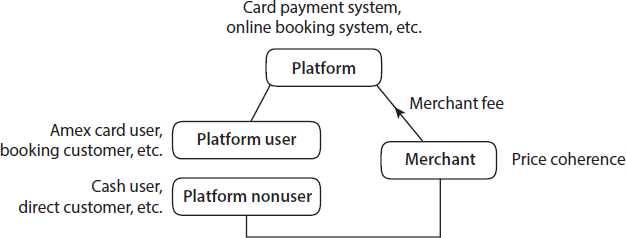

Many platforms have a practice that affects us all indirectly: they require the sellers not to charge the platform’s customers more than they would pay using any other channel. Often, the buyer has alternatives to a platform in buying from the seller. But the merchant is not authorized to charge more for a transaction via the platform than for one that bypasses it. Put differently, platforms require that the merchant fee they levy on the seller is not passed on to the end customer. (In economic jargon, we say the price is “single” or “uniform,” that there is “price coherence,” or that the platform user enjoys a “most favored nation” clause.)

For example (see figure 14.3), American Express charges merchants a transaction fee, but the consumer can pay merchants using cash, check, or another payment card instead. In the absence of specific regulation, American Express requires that the merchant not charge a higher price to consumers using their AmEx card. Similarly, a night in a hotel or a plane ticket can be reserved either through an online reservation platform, such as Booking.com or Expedia, or directly with the hotel or the airline company. The online reservation platform requires that direct purchases not be cheaper: the price of a room at an Ibis, Novotel, or Mercure hotel must be the same whether the room is reserved directly thorough their parent company (Accor) or through Booking.com or Expedia.13 Amazon too implements this policy for its suppliers (such as book publishers) in many countries, although regulators in some others, including the United Kingdom and Germany, have ruled that platforms cannot insist on price coherence.

In the case of payment cards, competition authorities in some countries have insisted that merchants be free to levy surcharges on payments by card. Yet price uniformity also has two virtues. First, it avoids captive customers facing unexpected additional fees at the last moment.14 We have all been on websites where we have found the plane ticket we wanted, entered all our information, only to discover at the final screen a ten dollar surcharge because we want to pay by card. Sometimes this online experience has equivalents in physical stores, in those countries that have freed merchants from the obligation to charge a single price (the United Kingdom, the Netherlands, the United States, Australia, and others); the surcharges are then much greater than the merchant fee levied by the card platform. In practice, though, surcharges are relatively rare, especially in stores with repeat customers. Second, for reservations made through a platform such as Booking.com or other online travel agencies, uniform pricing also has the advantage of preventing a consumer from finding the hotel they want on the platform’s website, and then going directly to the website of the hotel or another website for a lower price, leaving no revenue for the entity that helped them find the hotel in the first place.

A compromise is needed. Uniform pricing is not necessarily good for the consumer. The reason is simple: high commission charges levied by the platform are passed on to third parties—the customers who do not use the platform. Thus, the 15 to 25 percent commission charged to hotels by Booking.com is paid in part by customers who do not use Booking.com. Given that 20 percent of all hotel reservations pass through Booking.com, the site’s customers pay only a small portion (20 percent) of what the hotel is charged by the online reservation platform, while 80 percent is paid by customers who do not use the platform. This is in effect a private tax levied on non-platform customers.15 It is not all that surprising that excessive sales commissions can be charged.16 In this case, the market failure is not an asymmetric price structure (which, as we’ve seen, is typical of two-sided markets), but the negative externality imposed on those who do not use the platform.

There are other examples of this problem. The question for the future will be whether we should regulate sales commissions, and if so, how. Uber clearly creates added value; but is it worth the 20 or 25 percent levied on the driver? Is there enough competition between platforms to keep their profits in check?

Platforms must create value, and not be parasites. But services that put the two sides of the market together might seek to extract an economic rent, either in the form of excessive sales commissions or, on the consumer side, by abusing advertising and lower-quality service. We’ve all had the experience of looking for a little restaurant on the web, but we can’t find its website—in any case, not on the first page of the search engine’s results—because several platforms interpose themselves between us and the restaurant.

The economic analysis of these issues, whether in regard to sales commissions or other platform practices, is in its infancy, but it will provide the principles of regulation in this type of market. In the case of payment cards, for instance, economics suggests that merchant fees should be based on the principle of the internalization of externalities, as described in several chapters of this book;17 the merchant fee should be equal to the extra profit the merchant derives from accepting a payment by card, as compared to an alternative method of payment.18 The consumer, in choosing the method of payment, then imposes no externality on the merchant. This principle is now the one adopted by the European Commission to regulate the open Visa and MasterCard systems.

In this domain, as in others, neither laissez-faire nor a hasty set of regulations is warranted. A thorough economic analysis is required.

When Sellers Fight Back …

Platforms are not always in control. Sometimes they face something stronger than they are. One example is the price comparison sites for air travel in the United States.19 The business model of these price comparison sites depends on access to airline data on prices and seat availability (so they only offer a price if there is a seat available). The airline sector is very concentrated in the United States, and the larger airline companies have tried to keep price comparison sites (especially smaller ones) from gaining access to the data they need. Why do they refuse to be listed on these comparison sites?

The airlines want to retain control over their customer data so they can target individuals with advertising and offers suited to them. Sometimes, they do not wish to pay the sales commission charged by the site (which indeed can be high and end up hurting consumers, but refusals to list happen even when there isn’t a commission to pay). They are reluctant to admit, though, that they also do not want travelers to compare prices easily. In other sectors, when consumers can easily compare prices there is downward pressure on them. If an airline is known to have many flights to a destination, it is probable that the traveler will go to its website if it is not listed on the price comparison platform. A refusal to be on the platform may be anti-competitive.

Contestability

It does not take long to notice that information technology markets are highly concentrated. Often, one company (Google, Microsoft, Facebook) dominates the market. There is nothing abnormal about this; there will inevitably be a concentration of users on one or two platforms, but there are still grounds for concern about whether competition is functioning properly. There are two reasons for this concentration.

The first reason for the concentration is a network externality: we need to be on the same network as the person with whom we want to interact. That is Facebook’s model. If our friends are on Facebook, we need to be there too, even if we would really prefer another social network. We want to be on Instagram to share our photos with others who are on Instagram. When the telephone was invented, the initial competition among (noninterconnected) networks ended with a monopoly, because ultimately users wanted to be able to call one another. When competition was reintroduced into the telephone industry in the 1980s and 1990s, it was necessary to ensure that the networks were interconnected, and thus gave one another access—without regulation, incumbent operators would not have given this access to new, smaller entrants.

Network externalities can be direct, as in the case of Facebook, or indirect, as in the case of a platform for which many apps or games have been created—the more people use a platform, the greater the number of apps, and vice versa. Or a greater number of users may increase the quality of service by allowing better predictions, as with search engines (Google) and GPS-based geographical navigation apps (Waze); for instance, while competing search engines can rival Google’s for the most common requests, they do not have access to enough data to satisfy unusual search requests. Thus, a platform user benefits from the presence of other users on the same platform, even if there is no direct interaction with them, in the same way that a city dweller can benefit from the presence of other city dwellers who, although forever strangers, are the reason for amenities, such as bars or cinemas.

The second reason is linked to what are called “economies of scale.” Some services require large technological investments. Designing a search engine costs roughly the same, whether there are two thousand search requests a year or two trillion (in the case of Google’s). But obviously, the value of the user data from these two search engines, and what they could charge advertisers, would not be the same at all: they scale up.20 The forces at play lead to a “natural monopoly.” Because of network effects and economies of scale, the online economy is often a case of winner takes all. The browser market was dominated by Netscape, then by Internet Explorer (Microsoft), and now by Chrome (Google).

There are, of course, exceptions: economies of scale and network externalities are not always paramount, and the market is not always covered by one or two companies. There are many online platforms for music and film, such as Apple, Deezer, Spotify, Pandora, Canalplay or Netflix (although they are differentiated, for example, by their degree of interaction with the listener).

The concentration of digital markets again raises the question of competition. If one company has a dominant position, it creates a serious risk of high prices and a lack of innovation. New enterprises must be able to enter the market if they are more efficient or more innovative than the established monopoly; in economic jargon, we say that the market has to be “contestable.” If it is not possible to have vigorous competition between companies at a point in time, we must be satisfied with dynamic competition—or “creative destruction” as Schumpeter called it—in which today’s dominant firm is replaced by another that has made a technological or commercial leap.

This problem of contestability resurfaces regularly. In 1969, an antitrust suit in the United States forced IBM to separate its software activity from its hardware activity, an area in which IBM was dominant. It arose again with Microsoft and the dominance of its Windows operating system (a 1996 lawsuit in the United States and another in 2004 in Europe sought to unbundle the Microsoft operating system from its other services, such as Internet Explorer and the Media Player), and most recently with Google. These antitrust suits often relate to the tie-ins enforced by a dominant company—in other words, either adding another service at the same price (software, in the IBM example) or, more generally, selling this additional service at a very low price, so that the purchasers of the basic service buy both of them anyway.

The question of why these free or low-price add-ons are a problem is more complex than it seems. Suppose IBM’s software is inferior in quality to that of its competitors. A priori, IBM would have an interest in letting its customers use competitors’ software, thus reinforcing the attractiveness of its hardware, which it could sell at a higher price. Following this line of argument, the practice of tying IBM software to hardware suggests the software must be superior to that of its competitors—otherwise IBM wouldn’t have had an interest in tying the sales—in which case there would be no reason to be concerned. On the contrary, preventing IBM from pushing its software onto the market would only damage the user experience.

In antitrust suits, the dominant company will give various reasons—sometimes legitimate—for tying sales. One is the attribution of responsibility: If the product doesn’t work, how does the user know who to hold responsible? Do web searches fail to deliver because of the browser or because of the search engine? Another reason sometimes given is the protection of intellectual property, if compatibility with the products of competing companies requires giving them trade secrets. Another justification often given is the segmentation of markets: IBM used this argument, asserting that the tied sale of punch cards—a potentially competitive additional service—allowed it to distinguish between casual users and intensive users so that it could charge the latter more. A similar argument was used in the 1990s in several “aftermarket monopolization” lawsuits. Primary market manufacturers (car manufacturers, Xerox, Eastman Kodak) refused to supply ISOs (independent service organizations) with parts for repairs or cartridges, arguing that this allowed them to price discriminate between high- and low-usage customers; this allowed them to charge higher prices for repairs and cartridges, thereby lowering the total user cost for low-intensity users and raising it for high-intensity ones. Finally, there is the argument that distribution costs are not duplicated when there is a single vendor, although this is a less convincing argument in the digital era, where many products are distributed over the Internet.

The contestability imperative makes it possible to understand why the practice of tie-in sales can be a problem. It is, in fact, essential that markets be contestable. Entrants into online markets often begin with a specific product, as part of a niche strategy, rather than with a complete range of products. It is only later, after successfully entering the market with one product, that they fill out their range. Thus, Google began with only its search engine before it became the company we know today; Amazon started by selling books. But to be able to get into the market at all, entrants must be able to sell their original product if it is better than the competing one offered by the incumbent. The dominant company may then wish to block even partial new entry to the market—not to improve its short-term profits, but because it might prevent the newcomer from later competing in areas in which the established company occupies a monopoly position.21 In this case, the practice of tie-in sales is anticompetitive.

This analysis clearly shows that it is impossible to formulate a one-size-fits-all policy. There is no predetermined answer to the question of whether competition authorities ought to forbid a dominant company from imposing tie-in sales or anything resembling them (rebates for multiple purchases, for example) on its customers. Such commercial practices may be justified, but they may also serve only to consolidate the dominant position. The only valid way to ensure that competition enables the digital sector to realize its potential is to approach these questions on a case-by-case basis, deploying a rigorous economic analysis.