18

Wishing Won’t Make It So

“He who would climb the ladder must begin at the bottom.”

—ENGLISH PROVERB1

“He who wishes to be rich in a day will be hanged in a year.”

—LEONARDO DA VINCI2

“The only place where success comes before work is in a dictionary.”

—VIDAL SASSOON3

IN PEOPLE’S MINDS, THE NAMES Warren Buffett and George Soros tend to be linked with their impressive investment track records—24.4 percent and 28.2 percent per year, respectively. It’s as though they appeared from nowhere with this genius for investing.

Nothing could be farther from the truth. When Buffett began his Buffett Partnership in 1956, he drew on twenty years of experience of saving, investing, and learning about business and money. Similarly, Soros had already spent seventeen years learning his craft when he established the Double Eagle Fund in 1969.

For both, it was this long apprenticeship that made it possible for them to post such stellar returns from the very first day they entered the fund management arena.

In this respect, Buffett and Soros are no different from, say, Tiger Woods, who started to learn to play golf as soon as he could stand up. It wasn’t as though he just burst onto the scene to win his first professional title at the age of twenty-one. He already had nineteen years of experience.

Buffett’s Head Start

Compared to Tiger Woods, Buffett was a late starter. He didn’t buy his first stock until he was eleven years old. And he waited until he was five before starting his first business, a stand in front of his house selling Chiclets to passersby. This was followed by a lemonade stand positioned not in front of his house but in front of a friend’s, as he had noticed there was far more traffic there, and so many more customers. At six, he was buying six-packs of Cokes from the general store for 25 cents, and selling them door to door for 5 cents a bottle.

Many kids have a paper route or some other part-time work in order to supplement their pocket money. Not Buffett.

At the age of fourteen, Buffett had several paper routes, set up as a business. He was delivering 500 newspapers a day—but he had organized the route so it only took an hour and a quarter. He used his access to customers to sell them magazine subscriptions to maximize his income. He was making $175 a month from this paper route alone, an incredible sum for a teenager in the mid-1940s, money he planned to keep, not spend.

Other business ventures included collecting lost golf balls and selling them—not just a handful, but hundreds at a time. He and a partner owned pinball machines placed in barbershops. That business brought in $50 a week ($365 in today’s dollars), and was sold when he was seventeen for $1,200. He even had half ownership of a Rolls-Royce which was rented out at $35 a day.

This experience in starting and running businesses, tiny as they were compared to the smallest of Berkshire Hathaway’s acquisitions, gave him an understanding of business that’s simply not available from reading a book or taking a course.

Indeed, at Wharton (which he attended before going to Columbia) the nineteen-year-old “disgustedly reported that he knew more than the professors.”4 According to a classmate, “Warren came to the conclusion that there wasn’t anything Wharton could teach him. And he was right.”5

Buffett was also fascinated by stocks and spent a lot of time in his father’s brokerage, sometimes chalking up prices on the blackboard. He began to chart prices, “bewitched by the idea of deciphering their patterns.”6 His first stock purchase was Cities Service. He bought three shares at $38—and they soon dropped to $27. Buffett hung on, eventually selling out with a $5 profit. After which the stock kept going up all the way to $200.

While other kids read the sports pages or played ball, the young Buffett pored over the stock tables and read the Wall Street Journal after school. His high school teachers even asked him for investment advice.

But although he spent a lot of time studying the stock market, he wasn’t really doing all that well. He tried everything—“I collected charts and I read all the technical stuff. I listened to tips,”7 he later recalled—but nothing worked too well. He had neither a framework nor a system—until he found Benjamin Graham.

When he entered Columbia University in 1950 to attend Benjamin Graham’s class on security analysis, he was just twenty years old. But he was already a seasoned investor. He had already made many of the mistakes, and had many of the learning experiences, that most of us don’t begin to have until our twenties or even thirties …

• he had read every business and investment book he could lay his hands on—over 100 in total;

• he had tried (and discarded) a variety of approaches to investing, including reading charts and listening to hot tips; and

• for a twenty-year-old, he had an unusually wide experience in business, and had already demonstrated his business acumen.

Thanks to the power of compound interest, his unusual head start has added untold billions of dollars to his current net worth.

Buffett’s Mentor

For the next six years Buffett absorbed everything he could from Graham, first, as a student where he received the only A+ Graham ever awarded;8 then, working at Graham-Newman Corp., Graham’s fund management company, from 1954 to 1956.

But Buffett was already showing signs that he would excel his teacher.

Buffett was quicker at everything. Graham would amaze the staff with his ability to scan a page with columns of figures and pick out an error. But Buffett was faster at it. Howard Newman, [Graham-Newman partner] Jerry Newman’s son, who also worked there, said, “Warren was brilliant and self-effacing. He was Graham exponential.”9

And Buffett immediately applied what he had learned.

When he arrived at Columbia in 1950 he had $9,800 accumulated from his teenage business ventures.* When he left New York for Omaha in 1956 to start managing funds on his own, he had turned that sum into $140,000†—nearly a million of today’s dollars!—an annual compounded return of over 50 percent.

He had acquired his investment philosophy, developed his investment system, and tested it—successfully. He was ready.

The Failed Philosopher

When George Soros graduated from the London School of Economics in the spring of 1953, he was hoping for an academic career. But his grades weren’t good enough.

So after graduation he took the first of a series of odd jobs until, as a means of paying the rent, he hit upon the idea that there was money to be made in financial markets.

Soros wrote a personal letter to the managing director of each of the merchant banks in the City of London. One of his few interviews was with the managing director of Lazard Frères, who gave him an appointment for the sole purpose of telling him he was barking up the wrong tree trying to get a job in the City of London. He told Soros:

“Here in the City we practice what we call intelligent nepotism. That means that each managing director has a number of nephews, one of whom is intelligent, and he is going to be the next managing director. If you came from the same college as he did, you would have a chance to get a job in the firm. If you came from the same university, you may still be all right. But you’re not even from the same country!”10

Eventually, Soros did secure a job in the City with Singer & Friedlander, whose managing director was, like Soros, Hungarian. His time there was hardly illustrious, though what he was learning by doing—for example, to arbitrage gold stocks—began to make him more comfortable with a financial career.

But his time there was hardly an abject failure, either. A relative had given him £1,000 (then $4,800) to invest on his behalf. When he left in 1956 to join F. M. Mayer in New York, he took with him $5,000, which was his share of the profits made on that original £1,000. He clearly had a natural talent for operating in the investment marketplace.

In New York, Soros began arbitraging oil stocks—buying and selling the same securities on different international markets to profit from small price discrepancies.

But he first made his mark on Wall Street as a research analyst covering European stocks, where he had enormous success until John F. Kennedy entered the White House. One of Kennedy’s first acts as president in 1961 was to introduce the “interest equalization tax” to “protect” the balance of payments. This 15% tax on foreign investments brought Soros’s highflying business in European stocks to a crashing halt.

With little to do, he turned back to philosophy. In 1961 and 1962 he worked weekends and evenings on The Burden of Consciousness, a book he had begun writing while studying at the London School of Economics. He did indeed complete it, but it failed to satisfy him.

There came a day when I was rereading what I had written the day before and couldn’t make sense of it.… I now realize that I was mainly regurgitating Karl Popper’s ideas. But I haven’t given up the illusion that I have something important and original to say.11

It was only then, at the age of thirty-two, that Soros decided to focus his full attention on investing. In 1963 he made his last-but-one move, to Arnhold & S. Bleichroeder, where he began testing his philosophical ideas in the markets. It was here that the Quantum Fund was first conceived and, eventually, born.

In 1967 the First Eagle Fund was launched by Arnhold & S. Bleichroeder with Soros as its manager. A second fund, the Double Eagle Fund, was established in 1969—seventeen years after his first job in the City of London. Soros’s current net worth in the billions began then with his own investment in the fund of just $250,000. The following year, Jimmy Rogers (author of The Investment Biker) became Soros’s partner. They set up as independent fund managers—Soros Fund Management—in 1973, taking the Double Eagle Fund with them. It was renamed the Quantum Fund a few years later, and the rest is history.

Easy Money

Everyone would laugh at the idea that you could just pick up a golf club and take on Tiger Woods without any special training. Only a lunatic would bet on a complete novice beating André Agassi at Wimbledon. And who in his right mind would get in the ring with Mike Tyson and expect to last longer than fifteen seconds?

So why do people think they can just open a brokerage account, plonk down $5,000, and hope to make the same kind of returns as Warren Buffett or George Soros?

The myth that investing is an easy way to riches, that no special training or apprenticeship is needed, is implicit in every single one of the Seven Deadly Investment Sins. And it is reinforced by the fortunes that some rank amateurs occasionally make when they’re lucky enough to jump on a bandwagon like the Internet boom.

Even Master Investors such as Warren Buffett and Peter Lynch contribute (unwittingly) to this myth when they say that all you need to do is find a few good companies you can buy at the right price and sit on them.

It’s true that there are no barriers to entry. You don’t need any special physical skills. You don’t need to start while you’re in kindergarten, as top athletes and concert pianists must. And every investment book, every talking head on CNBC makes it all sound so easy.

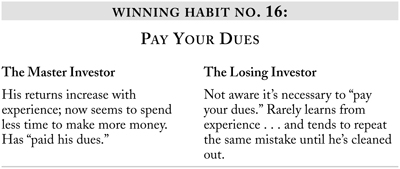

And investing is easy—when you have reached the state of unconscious competence. But to get there, you must first “pay your dues.”

Neither Buffett nor Soros actually set out with the intention of paying their dues. But by going through the process of making mistakes with real money, analyzing them, and learning from them, that is exactly what they were doing. By following this process, the losses they incurred were an investment in their long-term success.

Going through the pain of losing real money is an essential component of accumulating experience. How you react to such losses is the crucial element that determines whether you will ultimately succeed or fail as an investor.

Both Buffett and Soros were dedicated to succeeding. They are always willing to “go the extra mile” to reach their goal. A mistake, a loss, does not impact on their confidence in themselves. They don’t take it personally. As Buffett puts it: “A stock doesn’t know who owns it. You may have all these feelings and emotions as the stock goes up and down, but the stock doesn’t give a damn.”12

By taking responsibility for their actions they feel in control of their own destiny. They never blame the markets or their broker. They lost money because of something they did wrong—and so the remedy was within their control.

The investor who doesn’t react to his mistakes as Buffett and Soros react to theirs won’t stick it out long enough to pay their dues.

Paying the Price

Even investors who are spectacularly successful for a while sometimes fail to pay their dues and inevitably pay the price—just like Long-Term Capital Management.

Long-Term was founded in 1994 by John Meriwether, the former chief of Salomon Brothers’ Arbitrage Group, and most of the other traders from the same department. Long-Term started with $1.25 billion, raised mainly with the help of two of its partners, the Nobel Prize–winning economists Robert C. Merton and Myron S. Scholes.

At Salomon, the $500 million a year in profits these traders had averaged trading bond spreads accounted for the bulk of the firm’s profits.

For its first few years, Long-Term successfully replicated those profits by following exactly the same strategy. They knew what they were doing, and they did it well.

Too well. By 1997, the partners had a problem: They had too much money, even after they returned a big chunk of it to the investors. And at the same time, the margins on their bread-and-butter business of bond spreads had shrunk as everyone else on Wall Street piled in.

Except for Meriwether, most of the other partners were “quants”: people with PhD’s in economics or finance who had studied with Merton or Scholes or one of their followers. Underlying their approach was the fundamental belief that “markets are efficient.”

At Salomon, they had built computerized models of the bond markets to identify and exploit bond market inefficiencies. Bonds were their circle of competence—and, there, they had paid their dues.

But their success had gone to their heads. When faced with the problem of where to put all this new money, they took their bond models and applied them to markets like takeover arbitrage where they had no competitive advantage. Not only were these models unproven and untested outside bonds, the “professors” (as the partners were known) didn’t feel that any testing was necessary. They just plunged in with billions of dollars.

Unfortunately for them (as it turned out later), their first forays outside the bond markets were successful. So they expanded to trading currencies, as well as Russian, Brazilian, and other emerging market bonds and spreads on stock options. They even shorted some stocks outright, including Berkshire Hathaway, a trade that eventually cost them $150 million.

Scholes was one of the few partners who was upset about such trades. “He argued that Long-Term should stick to its models; it did not have any ‘informational advantage’”13 in any of these areas. But he was totally ignored.

The other partners acted as if they could walk on water. To them, their previous success proved they were infallible. They had no Plan B to tell them what to do if things fell apart. On the contrary, with mathematical precision they had calculated that a market implosion that would affect all their positions simultaneously was a ten-sigma event, one that might happen once in the life of the universe.

Their first mistake, of course, was going outside their circle of competence. You will not want to make this mistake. You can expand your circle of competence by learning and testing a different way of investing. If you’re willing to pay your dues again. To just dive in with a billion dollars on the line from day one is akin to getting into the ring with Mike Tyson with your eyes closed. A recipe for disaster.

And sure enough, Long-Term imploded in August 1998 when Russia defaulted on its bonds and the markets went haywire. After having quadrupled their investors’ money from $1.25 billion to $5 billion, by October 1998, there was only $400 million left—40 cents on the original dollar.

Of course, their failure to “pay their dues” wasn’t the only mistake the “professors” made. Indeed, they violated almost every single one of the 23 Winning Investment Habits. But the way they believed they could jump straight to the end of the learning curve was an integral part of their demise.

If you haven’t paid your dues, you’ll eventually blow up. It’s inevitable.

“It’s Frightening Easy”

Like any master of a craft, the Master Investor who has paid his dues develops what some people think of as “a sixth sense where they just know that a stock is going to move.… It’s visceral. You just sense it.”14

It could be a backache, as it is for Soros. A mental picture like the one Buffett sees of a company ten or twenty years in the future. Or an internal voice saying, “That’s the bottom!” In whatever form it comes, it’s the years of accumulated experience stored in the Master Investor’s subconscious mind communicating in a kind of mental shorthand.

This is why, for the Master, everything he does seems so effortless.

Before he had achieved the state of unconscious competence, it would have been impossible for Buffett to decide to buy a billion-dollar company in just a few minutes. Nor would Soros have been able to take such a giant position in a currency, as he did when he shorted the pound sterling in 1992. Indeed, until the Plaza Accord in 1985 Soros had lost money on his forays into currencies.

But to some degree, Soros’s and Buffett’s increasing expertise is disguised by the mountain of money each has to invest. With billions rather than millions of dollars to invest, only an investment “elephant” will make a significant difference to either Master Investor’s net worth.

While there are very few “elephant-sized” investments with the prospect of large percentage gains, there are endless investments of this kind for the smaller investor. As Buffett demonstrated in the late 1970s when he and his wife separated and he, personally, was strapped for cash.

Although he was then worth $140 million, it was all tied up in Berkshire stock. He refused to sell a single share of his “work of art.” And he would certainly not declare a dividend just to pay his rent.

So he began buying stocks on his personal account.

“It was almost frightening, how easy it was,” a Berkshire employee said. “He analyzed what he was looking for. All of a sudden he had money.…” According to the broker Art Rowsell, “Warren made $3 million like bingo.”15

The investor who believes that all he needs to do is find the holy grail, the right formula, the secret to reading charts, or some guru to tell him what to do and when to do it, can never develop the expertise of a Warren Buffett or a George Soros.

Paying your dues can be a long and arduous process, one that took Buffett and Soros almost twenty years apiece. But they went about the process unsystematically.

Unlike them, you now know that you must begin at the bottom of the learning curve. This gives you an inestimable advantage over the Master Investor who reached Mastery by a process of trial and error.