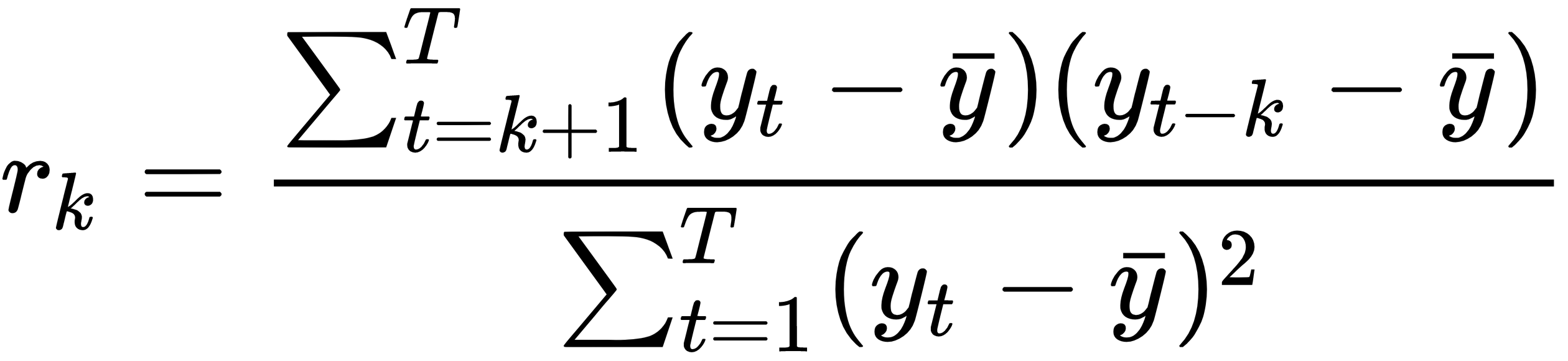

Autocorrelation is a measure of the correlation between the lagged values of a time series. For example, r1 is the autocorrelation between yt and yt-1; similarly, r2 is the autocorrelation between yt and yt-2. This can be summarized in the following formula:

In the preceding formula, T is the length of the time series.

For example, say that we have the correlation coefficients, as shown in the following diagram:

To plot it, we get the following:

The following are some observations from this autocorrelation function plot:

- r4 is higher than other lags, which is mostly because of a seasonal pattern

- The blue lines are the indicators of whether correlations are significantly different from zero

- Autocorrelation at lag 0 is always 1