13 Market incompleteness and one-period trinomial tree models

Market incompleteness is everywhere in actuarial science, as typical insurable risks embedded in life insurance or homeowner’s insurance cannot be (exactly) replicated using tradable assets. Public policy and tight regulations in the insurance industry prevent insurers from trading their insurance policies to exactly offset a liability. It may also be impossible to (exactly) replicate certain financial risks. For example, prior to the creation of credit default swaps (see Chapter 4), it was nearly impossible to hedge against losses resulting from credit risk.

The risk management implications of an incomplete market are rather important. It basically means that some risks cannot be synthetically replicated. We illustrate this in the next example.

Example 13.0.1Impact of default risk on replicating portfolios1

Suppose that on the financial market, a share of ABC inc. currently trades for $40 and it is assumed that, in a year, its value will be either $50 or $30. You also know that $100 invested at the risk-free rate will accumulate to $104 in a year. Your company sells a 1-year at-the-money investment guarantee on ABC inc.; this is marketed as an investment that provides the upside on the stock return with a protection against the downside. We know from Chapter 6 that the investment guarantee can be replicated by combining the stock and a put option on this stock. As the risk manager, you decide to replicate this put option and then add one share of the stock to the resulting replicating portfolio.

As we have done before, we could model the price of this stock using a binomial tree. However, there is a probability of 1/100 that ABC inc. will go bankrupt during the next year, which means its stock price will plunge to zero. As this probability is very small, you decide to ignore it and go through with replication assuming the stock price follows a binomial tree model.

In a binomial model, we can easily replicate the put option with the following system of equations:

We obtain x = −0.5 and y = 25/1.04 = 24.038461538. Therefore, the no-arbitrage price of the put option is 40x + 1y = 4.038461538.

In conclusion, to replicate the investment guarantee, the company needs to buy 1 + x = 1 + ( − 0.5) = 0.5 share of the stock and y = 24.0385 units of the risk-free asset, which can be done by selling the investment guarantee for 44.038461538 = 40 + 4.038461538 to the customer. In 99 out of 100 cases, this will be a riskless venture for the company.

However, in the unlikely event that the stock price goes to 0, i.e. if ABC inc. bankrupts, then your company will have to pay the guaranteed amount of $40 to the customer, while its assets in the portfolio will be worth only

In 1 out of 100 cases, your company will suffer an important loss of 40 − 25 = 15. Consequently, there is real danger to assume the stock price follows a binomial model in this situation.

◼

This example illustrates that a risk such as bankruptcy or the possibility of a financial crisis, if not properly hedged, can have a very important impact on a risk management strategy. This risk might have been ignored by the risk manager because default risk was considered insignificant (as in the above example) or because no additional assets were available in the market to eliminate this risk. We will come back to this example later in Section 13.4.

In this chapter, we will introduce the concept of market incompleteness and we will present a few one-period trinomial tree models with the main objective of understanding the mathematical, financial and risk management implications of the impossibility to replicate specific risks in the financial and insurance markets. The model is very simple and tractable as it only adds a third possible outcome to a one-period tree model. This seemingly simple extension has numerous implications that we will analyze in various contexts.

One-period trinomial tree models also allow us to easily explain and illustrate some of the most complex concepts in financial mathematics, namely complete and incomplete markets, super and sub-replicating portfolios, the existence of multiple risk-neutral probabilities and the Fundamental Theorem of Asset Pricing (FTAP).

The specific objectives are to:

differentiate complete and incomplete markets;

build sub-replicating and super-replicating portfolios;

understand that in incomplete markets, there is a range of prices that prevents arbitrage opportunities;

derive bounds on the admissible risk-neutral probabilities and relate the resulting prices to sub- and super-replicating portfolios;

replicate a derivative in a one-period trinomial tree model with three traded assets;

examine the risk management implications of ignoring possible outcomes when replicating a derivative;

analyze how actuaries cope with the incompleteness of insurance markets.

The beginning of this chapter has the same structure as Chapters 9–11, i.e. we first introduce the trinomial model for a risky asset, then we attempt to replicate payoffs and retrieve the risk-neutral probabilities. The last sections of this chapter will analyze more specific consequences of market incompleteness in actuarial contexts.

13.1 Model

Just like the one-period binomial model, the (one-asset) one-periodtrinomialmodel presented in this chapter is based upon two time points: the beginning of the period is time 0 and the end of the period is time 1. Again, time 0 represents inception or issuance of a derivative while time 1 stands for its maturity. It is a frictionless financial market composed of the following two assets:

a risk-free asset (a bank account or a bond) which evolves according to the risk-free interest rate r;

a risky asset (a stock or an index) with a known initial value and a random future value.

Note that in Section 13.4, the two-asset trinomial model will be presented to include an additional risky asset like a second stock.

13.1.1 Risk-free asset

The risk-free asset B = {B0, B1} is an asset for which capital and interest are repaid with certainty at maturity. In a one-step trinomial tree model, we assume there exists a constant interest rate r ⩾ 0 for which we can either write

with B0 = 1.

13.1.2 Risky asset

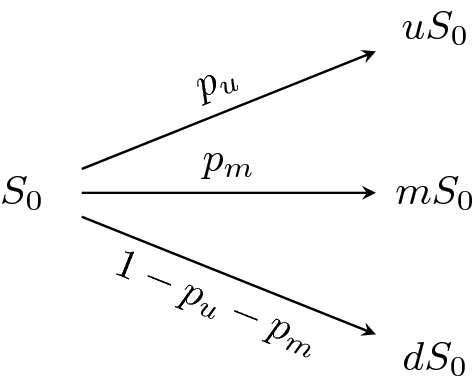

The evolution of the price of the risky asset is denoted by S = {S0, S1} where S0 is the price today which is a known (observed) quantity. Moreover, S1 represents the risky asset price at the end of the period which is random. This random variable S1 is taking values in {su, sm, sd} with probability pu, pm and pd respectively, where 0 < pu, pm, pd < 1 are fixed values such that pu + pm + pd = 1 and where sd < sm < su. In other words, S1 has the following probability distribution (with respect to the real-world (or actuarial) probability ):

Note that if we specify the values of pu and pm, then we must have pd = 1 − pu − pm, and vice versa. Therefore, the one-period trinomial tree model is a seven-parameter model, namely , two more than the corresponding one-period binomial model.

The one-period trinomial tree is often represented graphically as follows:

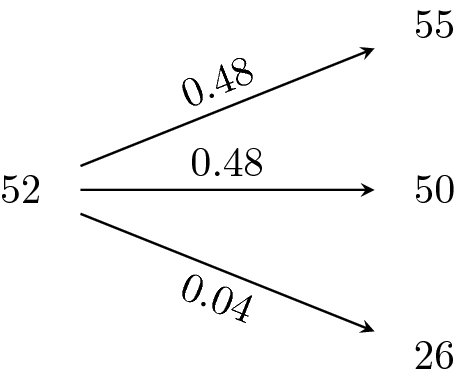

Example 13.1.1Construction of a trinomial tree

According to financial analysts, the price of a stock currently selling for $52 will be equal to either $55 or $50 in 3 months if the markets behave normally. However, it will dramatically drop to $26 if a financial crisis occurs. These analysts have determined there is only a 4% chance for a crisis to occur, while the other two scenarios are equally probable. A 3-month Treasury zero-coupon bond, with a face value of $100, currently trades for $99.

Let us build the corresponding one-step trinomial tree for the stock price in 3 months.

First, we have B0 = 1 and . From the above information, pd = 0.04 while pu = pm = 0.48, which means that the trinomial tree for the stock is

◼

To make sure a trinomial model is arbitrage-free, none of the two assets should be doing better than the other one in all three scenarios. In other words, investing in either the risk-free asset B or the risky asset S should be such that S1 > S0B1 and S1 < S0B1 are both inadmissible. Mathematically, the arbitrage-free condition reads as follows:

(13.1.1)

which looks exactly like the condition in equation (9.1.1) for the binomial model. One must realize here that this no-arbitrage condition also says that it does not matter whether S0B1 is smaller or larger than sm, as long as it is not bigger than su or smaller than sd.

Example 13.1.2Arbitrage between the stock and the bond

The model depicted in example 13.1.1 is arbitrage-free because investing S0 to buy a stock may yield more or less than lending at the risk-free rate. The same can be said when lending S0 at the risk-free rate: it may earn more or less than buying a stock. Mathematically,

Suppose now that the risk-free asset is such that B1 = 1.07. Then S0B1 = 52 × 1.07 = 55.64 > 55 = su, which means the no-arbitrage condition in (13.1.1) is violated.

To exploit this arbitrage opportunity, the key is always to buy the cheapest asset/portfolio and sell the most expensive i.e., we invest (borrow) in the asset that yields the most (least). Therefore, we sell the stock for $52 and invest the proceeds at the risk-free rate. At time 0, the net cash flow is 0. At maturity, the risk-free investment earns 55.64 and we need to close our short position on the stock. We buy the stock at either $55, $50 or $26. The arbitrage profit is

in all three scenarios. The arbitrage opportunity is thus exploited in exactly the same manner as in the binomial model.

◼

13.1.2.1 Simplified tree

Again, we can represent the stock price at maturity using an up factoru, a middle factorm, and a down factord as follows:

which implies that we can write

Clearly, we have that d < m < u, and the tree:

With this new notation, the no-arbitrage condition (13.1.1) is equivalent to

as in equation (11.1.1). Recall that B1 is either equal to er or 1 + r.

The underlying probability model

For the one-period trinomial tree, one can choose its sample space Ω1 to be

It is then clear that each state of nature ω ∈ Ω1, that is each scenario, corresponds to a branch in the tree. Clearly, the possible prices at maturity are

13.1.3 Derivatives

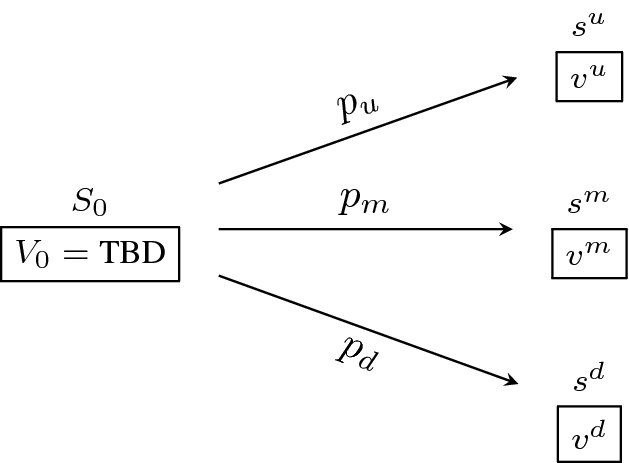

We now introduce a third asset, more precisely a derivative written on the risky asset S, which is completely characterized by its payoff. The evolution of the price of this third asset is denoted by V = {V0, V1}, where V0 is today’s price while V1 is its (random) value at the end of the period. As in the binomial model, V1 is a random variable representing the payoff.

As there are three possible outcomes in the trinomial model, the payoff V1 can take three values, denoted by vu, vm and vd. More precisely, the random variable V1 takes the value vu when S1 takes the value su, it takes the value vm when S1 takes the value sm, and finally it takes the value vd when S1 takes the value sd. Consequently, V1 has the following probability distribution (with respect to the real-world probability ):

As in the binomial model, we can now superimpose the evolution of the derivative price V (in squares) over the evolution of the stock price S:

Finally, we will use the notation C = {C0, C1} and P = {P0, P1} for a call option price and a put option price respectively, where the payoffs are

if they both mature at time 1 and both have strike price K.

13.2 Pricing by replication

The key principle underlying replication in the one-period trinomial model is the same as in the binomial model: we seek to find a strategy that replicates the payoff in all scenarios. But as we will see below, allowing a third possible outcome for the risky asset will complicate matters.

13.2.1 (In)complete markets

For a given payoff V1, we want to find the time-0 price V0 of this derivative in a one-period trinomial model. In the one-period binomial model, we were able to find a replicating portfolio mimicking the payoff in each and every scenario of that model, using only the basic assets B and S.

Again, let us define a trading strategy (or portfolio) as a pair (x, y), where x (resp. y) is the number of units of S (resp. B) held in the portfolio from time 0 to time 1. Then, the value of this strategy over time is given by Π = {Π0, Π1}, where

is the time-0 value, while

is the (random) time-1 value. If our goal is to replicate the payoff V1, then we should choose the pair (x, y) to make sure that

in each of the three possible scenarios, i.e. we must have

(13.2.1)

So, we need to solve (13.2.1), a linear system of three equations with two unknowns, where B1, sd, sm, su are given model parameters and vd, vm, vu are given by the derivative payoff at maturity. The values of x and y are the two unknowns.

Example 13.2.1

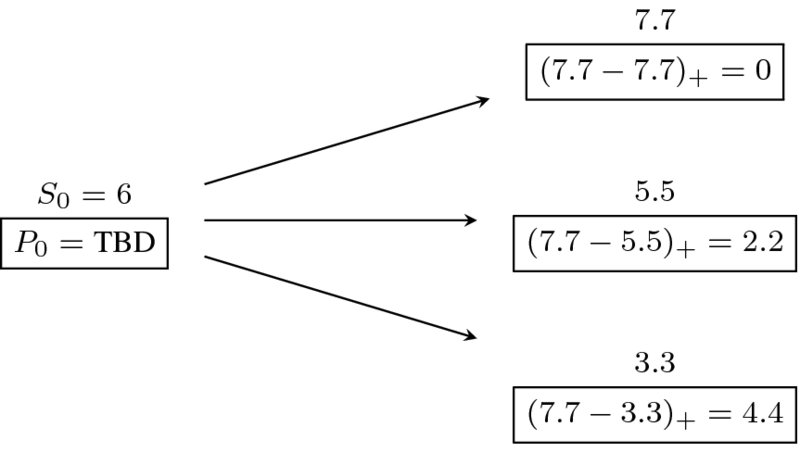

Let us consider the following trinomial model.2 Assume the risk-free asset is such that B1 = 1.1 while the risky asset can take three possible values in one period: su = 7.7, sm = 5.5 and sd = 3.3. Note that the stock currently trades for S0 = 6. We want to find the price of a 1-period 7.70-strike put option written on S. Graphically, we have

We can easily verify that this trinomial tree is free of arbitrage. Note that we do not know what the values of the actuarial probabilities pu, pm and pd are.

Let us find the replicating portfolio, i.e. let us find (x, y) such that

From the first two equations, we get

The couple (x, y) is also a solution to the third equation:

In other words, the trading strategy (x, y) = ( − 1, 7) is a replicating strategy for this put option. By the no-arbitrage principle, we then have P0 = Π0, which yields

◼

In general, it is not possible to solve a linear system of three equations with two unknowns. This means that the last example was a (deliberate) coincidence.

Example 13.2.2

In the previous example, if we had instead considered a put option with strike price K = 6, the system of equations resulting from replication (in each scenario) would have been:

Unfortunately, this linear system does not admit a solution. Indeed, we can find the only x and y solving the first two equations:

However, these values do not satisfy the third equation:

In other words, there is no replicating portfolio for this put option.

◼

The last two examples illustrate that in the one-period trinomial model, it is not always possible to replicate the payoff of a derivative. Indeed, the 7.70-strike put option could be replicated whereas the 6-strike put option could not.

A derivative is said to be attainable if we can find a self-financing strategy to replicate its payoff. In the one-period trinomial model, it is easy to determine whether a security is attainable. If one can find a unique solution to the system of equations in (13.2.1), then the derivative is attainable. But in most cases, we know that we cannot get a unique solution to a system of three equations with two unknowns. Therefore, most derivatives in the one-period trinomial tree model are not attainable. In the previous example, the 7.70-put option was attainable whereas the 6-strike put option was not.

A financial market is said to be complete if there are no arbitrage opportunities in this market and all derivatives are attainable. From this definition, we can deduce that the binomial model is a complete model because we can easily replicate all derivatives in this market by solving systems of two equations with two unknowns. The trinomial model, composed of a risk-free asset and a risky asset, is an incomplete model because we cannot replicate all derivatives. In fact, it suffices not to be able to replicate only one derivative for a model to be incomplete.

13.2.2 Intervals of no-arbitrage prices

The question now is: how do we find the no-arbitrage price of a derivative in a trinomial tree model if we cannot exactly replicate its payoff (in all scenarios)? But first, does a unique no-arbitrage price even exist? The answer to the latter question is no, not in the trinomial model. Instead of finding a unique no-arbitrage price for a given derivative, we will find an interval of no-arbitrage prices by excluding prices for which arbitrage opportunities would exist.

Here is an example on how to exclude non-valid prices in a trinomial model.

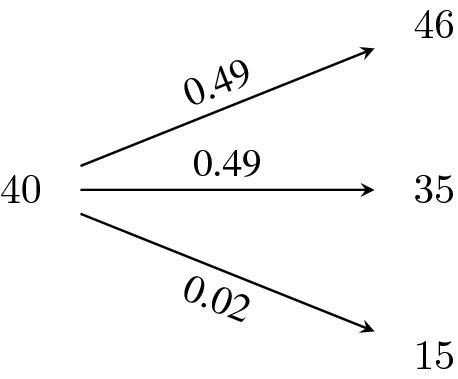

Example 13.2.3Sub-replication

Consider a one-period trinomial tree where a stock evolves as follows:

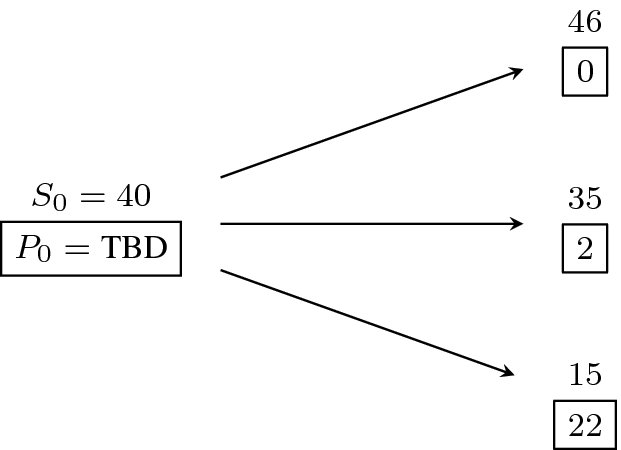

The one-period risk-free rate is at 4%. You have sold a put option with strike price $37 that expires in one period. You want to manage the risk of your financial position. The payoff of the put option is superimposed to the evolution of the stock price in the tree below.

We do not expect to be able to replicate this put option. However, from our own analyses and experience, we think that the probability of a financial crisis and hence that the stock price crashes to 15$ is only 2%. Therefore, let us ignore this scenario and replicate the put only in the other two normal scenarios, as if it were a binomial model. In other words, let us find the pair solving

We know that the solution to this system is given by

The initial value of this strategy is then given by

By construction, the value of the strategy at time 1 in the normal scenarios is such that

Based upon our judgment, there should be a 98% chance that the portfolio will exactly replicate the payoff of the option at maturity.

But what will happen to this portfolio if a financial crisis occurs? In that case, the time-1 value of the strategy will be equal to

while the put option payoff will be (37 − 15)+ = 22. In other words, the portfolio will be short by 22 − 5.636363 = 16.36364, with probability 0.02.

The portfolio given by is what we call a sub-replicating portfolio because

in all three scenarios (see also next table).

Stock

Put

Sub-rep ptf

Value if bull market

46

0

0

Value if bear market

35

2

2

Value if financial crisis

15

22

5.6363

Initial price

40

TBD

0.76923

Consequently, to avoid arbitrage opportunities, this put option must not be sold for a value less than .

◼

Let us illustrate how to exploit an arbitrage opportunity in this setting.

Example 13.2.4Exploiting an arbitrage opportunity

In the previous example, we built a sub-replicating portfolio, i.e. a portfolio such that , in all three scenarios. Suppose now that the put option can be bought for only $0.50. Let us explain how to exploit this arbitrage opportunity.

As the option is underpriced, we will buy it and we will short the sub-replicating portfolio. We buy the put option (− 0.50 at inception) and sell the sub-replicating portfolio (+ 0.76923 at inception), for a net initial cash flow of 0.26923. At maturity, if the stock price is either 46 or 35, the net proceeds are zero. However, if the stock market crashes, the strategy yields a profit of 22 − 5.6363 = 16.3637. Therefore, you receive 0.269 at inception, and you will receive a non-negative amount at maturity, thus exploiting this arbitrage opportunity.

◼

It is also possible to create super-replicating portfolios whose terminal values dominate that of the corresponding option payoff in all scenarios. We illustrate this in the next example.

Example 13.2.5Super-replication

Your colleague thinks that you should instead replicate the put in the bull market scenario and in the financial crisis scenario only, and therefore ignore the bear market scenario. In other words, she suggests to find the pair solving

We know that the solution to this system of equations is given by

The initial value of this strategy is then given by

By construction, its value at time 1 is such that

But what happens if we set up this portfolio and then the bear market scenario is realized? In that case, the time-1 value of the strategy would be equal to

while the put option payoff would be (37 − 35)+ = 2. In other words, selling the put and holding this portfolio will generate an extra amount of 7.806454 − 2 = 5.806454, with probability 0.49, and break even the rest of the time.

The portfolio given by is a super-replicating portfolio because

in all three scenarios.

◼

Let us now illustrate another arbitrage opportunity.

Example 13.2.6Exploiting an arbitrage opportunity (continued)

In the previous example, we built a super-replicating portfolio, that is a portfolio such that in all three scenarios. Suppose now that the put option can be sold for $4. Explain how to exploit an arbitrage opportunity, if any.

The following table shows the value of the put option and of the super-replicating portfolio in all scenarios.

Stock

Put

Super-rep ptf

Value if bull market

46

000

0000000

Value if bear market

35

002

7.806454

Value if financial crisis

15

022

0000022

Initial price

40

TBD

3.002484

Selling the put option and buying the super-replicating portfolio will yield an important profit in the bear market scenario. Now if the put option sells for $4 on the market, we can simply sell it and buy the super-replicating portfolio, yielding a profit of nearly $1 at inception (4 − 3.002 = 0.998) and an additional gain when the second scenario realizes. This is an arbitrage opportunity since there is no possibility of loss.

If the put option was sold below $3 (say even $2.99), then the preceding strategy would be a bet that the bear market will occur at maturity. This is no longer an arbitrage opportunity. Therefore, any price below 3.002484 will prevent arbitrage opportunities.

◼

In the previous examples, there were three pairs of scenarios we could choose from to set up portfolios inspired by our work in the binomial model. There is one such pair we have not looked at. More precisely, what happens if we now decide to ignore the bull market scenario?

We are essentially replicating the scenarios where the put matures in the money. We will be short-selling the stock and investing 35.57692308 at the risk-free rate for a negative initial cost (−4.423076923).3 This is shown in the next table.

Stock

Put

This ptf

Value if bull market

46

00

00000000−9

Value if bear market

35

02

0000000002

Value if financial crisis

15

022

00000000022

Initial price

40

TBD

−4.423076923

This strategy is sub-replicating the payoff of the put option because , in all three scenarios. What this says is that the no-arbitrage price of the put option should be at least −4.423076923, which is not informative since we already found that it should be larger than 0.76923 to avoid arbitrage.

To conclude the above examples, the initial price of the put option should be:

larger than 0.76923;

lower than 3.002484;

larger than −4.4231.

Taking the intersection of the latter three conditions, we find that any price in the interval (0.76923, 3.002484) will not introduce an arbitrage opportunity in this market model.

13.2.3 Super- and sub-replicating strategies

We are now ready to formalize the ideas seen in the previous section. In a one-period trinomial model, we can build three strategies associated to the three pairs of scenarios: (u, m), (u, d) and (m, d). The idea is to ignore one scenario, (temporarily) treat the model as a binomial model and build the corresponding replicating portfolio. These strategies are not replicating strategies for the trinomial model as we are not mimicking the payoffs in all three scenarios.

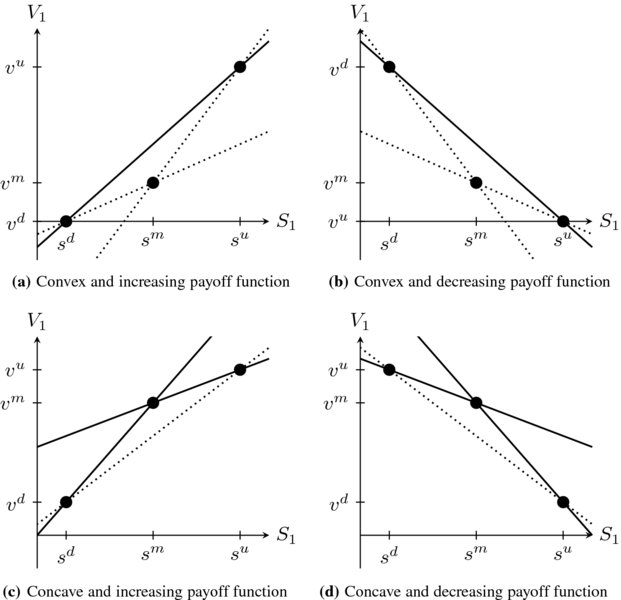

Out of these three strategies, there always exists at least one super-replicating strategy and at least one sub-replicating strategy. Figure 13.1 illustrates various payoffs that are convex or concave functions of S1. A line that is located at or above (below) the three points represents a super- (sub-) replicating strategy. The case of call (upper left panel) and put (upper right panel) options is depicted in the upper panels of Figure 13.1. We see that depending on the shape of the payoff function, we might have two sub-replicating strategies and one super-replicating strategies or vice versa.

Figure 13.1 Different payoff functions and their corresponding super-replicating (continuous lines) and sub-replicating (dotted lines) strategies

A super-replicating strategy (or portfolio) for a derivative with payoff V1 = g(S1) is a pair such that

in all three scenarios, i.e.

The best super-replicating strategy is the cheapest in the set of all super-replicating strategies. In other words, there might exist many super-replicating strategies for V1 and the best is simply the one with the lowest cost. We denote the initial value of by .

In the case of call and put options, a quick plot of the payoff function, as in Figure 13.1, suffices to see that there is only one super-replicating portfolio: the one based upon u and d (see the upper panels of Figure 13.1). Therefore, the best super-replicating strategy for a call option is obtained by solving

(13.2.2)

whose unique solution is given by

We can proceed similarly for a put option to find its super-replicating portfolio.

Example 13.2.7

Let us consider again the example where B1 = 1.1, S0 = 6 and where the possible values for S1 are su = 7.7, sm = 5.5 and sd = 3.3.

In this model, the super-replicating portfolio of a put option with strike K = 6 is given by

And then its initial value is

◼

A sub-replicating strategy (or portfolio) for a derivative with payoff V1 = g(S1) is a pair such that

in all three scenarios, i.e.

The best sub-replicating strategy is the most expensive in the set of all sub-replicating strategies. In other words, there might exist many sub-replicating strategies for V1 and the best is simply the most expensive. We denote the initial value of by .

Due to the convexity of the payoff of call and put options, there are always two sub-replicating strategies: one based upon scenarios u and m, and another based upon scenarios m and d. However, determining the pair of scenarios yielding the best sub-replicating strategy depends on whether S0B1 > sm or S0B1 < sm. If S0B1 < sm, we should consider m and d.

The methodology is still very similar: select the pair of scenarios u and m, replicate the payoff in those two scenarios and compute the cost of the corresponding sub-replicating portfolio. Then, repeat for the pair of scenarios m and d. This is illustrated in the next example.

Example 13.2.8

Let us consider again Example 13.2.2 where B1 = 1.1, S0 = 6 and where the possible values for S1 are su = 7.7, sm = 5.5 and sd = 3.3. We know there are two sub-replicating portfolios: one obtained by replicating the payoff with scenarios d and m, and another with scenarios m and u.

The first sub-replicating portfolio is given by

The initial cost of this portfolio is

The second sub-replicating portfolio is given by

with initial cost

As we used suggestive notation, we conclude that the best sub-replicating portfolio is indeed the second one since 0.2272728 > −0.54545.

◼

What we should remember from this section is that replicating a payoff V1 in the one-period trinomial tree model almost never leads to a solution (a unique replicating portfolio). Consequently, there is no such thing as a unique price V0. Most of the time, we will find a range of prices that prevents arbitrage opportunities: any choice of V0 in the (open) interval

will not give rise to an arbitrage opportunity in the trinomial tree. This is also true of incomplete market models in general.

In the rare cases where we can find a unique replicating portfolio, the interval will collapse to a single value

and then we have a unique no-arbitrage price V0 = Π0 corresponding to this strategy’s initial value.

Moreover, from a risk management perspective, it is important to understand that the seller of a derivative can no longer be indifferent between:

buying the equivalent derivative elsewhere on the market (offsetting positions); or

replicating the liability with basic traded assets.

This is because, in an incomplete market, these two alternatives are not exactly equivalent. Risk management with the second alternative entails some risk.

Which price to use (in an incomplete market)?

In a complete market, there exists a unique replicating strategy for all derivatives. Therefore, risk management is easy: issuing a derivative and holding the corresponding replicating portfolio bears no risk. Moreover, the no-arbitrage price of a derivative is unique.

In an incomplete market, for a given derivative, we find a range of no-arbitrage prices : each price in that interval prevents arbitrage opportunities. This is not very useful: we cannot buy or sell a security using an interval of prices. We need to find a price.

However, the largest price at which a buyer is willing to buy the derivative is whereas the smallest price at which the seller is willing to sell is . This is because the best sub- (super-) replicating portfolio assures the buyer (seller) cannot lose. It is therefore impossible to obtain a unique price at which both the seller and buyer will agree. At any price in between and , the buyer and/or seller will assume some level of risk. Thus, in order to find a price, we will need additional assumptions on the market and the behavior of the buyer(s) and seller(s).

13.3 Pricing with risk-neutral probabilities

Remember that in the one-period binomial model, we rewrote expressions for the cost of replicating portfolios and interpreted them as discounted expectations using risk-neutral probabilities. It is possible to carry out a similar exercise in the one-period trinomial tree model by working with sub- and super-replicating portfolios. In doing so, we will also introduce a very important theorem in the theory of derivatives pricing, which is known as the Fundamental Theorem of Asset Pricing.

13.3.1 Maximal and minimal probabilities

Let us recall that in the one-period binomial model of Chapter 9, the price of the replicating portfolio for an arbitrary derivative with payoff V1 is given by

with

By the no-arbitrage principle, we must have that V0 = Π0.

As we saw, it turns out that there exists unique risk-neutral probabilities q and 1 − q, given by

such that

for any derivative with payoff V1. The risk-neutral probabilities belong to the one-period binomial model, not to a particular derivative.

In the trinomial model, we found that the cost of the best sub-replicating portfolio provides the smallest no-arbitrage price for the corresponding derivative. Even if this portfolio is built to mimick the payoff in only two scenarios, it is still possible to rewrite its cost in terms of a discounted risk-neutral expectation. This will attribute fictitious weights to scenarios u, m and d, similar to what happened in the binomial model. The same can be done for the best super-replicating portfolio.

Let us illustrate the process with call and put options. The cheapest super-replicating portfolio is obtained by considering scenarios u and d, for both options. Hence, we can write

where

Recalling the no-arbitrage condition of (13.1.1), it is clear that . As a consequence, we can also write

where the notation means we are attributing probabilities to scenarios {u, m, d}, respectively.

The best sub-replicating portfolio is obtained by considering scenarios m and d, or scenarios m and u. To illustrate the methodology, suppose that S0B1 < sm, in which case we should consider scenarios m and d. Therefore, we obtain

where

Since we assumed that S0B1 < sm, it is clear that . As a consequence, we can also write

where the notation means we are attributing probabilities to scenarios {u, m, d}, respectively. The methodology is similar when S0B1 > sm, in which case we should consider scenarios m and u.

For convenience, let us define and , as well as and . Then, the range of call option prices such that there are no arbitrage opportunities is given by

while, for the put, it is given by

Risk-neutral probabilities

You might have noticed that we did not use the terminology risk-neutral probabilities for or .

This is because formally, for a probability measure to be a risk-neutral probability measure, it has to be equivalent to . Two probability measures and are equivalent when outcomes that are certain or impossible are the same under both measures.

We know that 0 < pd, pm, pu < 1 and hence all three scenarios are possible. However, both and assign a zero probability to one of the three possible outcomes and therefore both and are not equivalent to . For example, we have while .

13.3.2 Fundamental Theorem of Asset Pricing

The approach we just presented can be framed into a more general setting based upon the Fundamental Theorem of Asset Pricing, which is valid for many financial market models such as the binomial model and the trinomial model, as well as the Black-Scholes-Merton model of Chapter 16.

It is beyond the scope of this book to present a formal statement of the FTAP. First, we will present an accessible formulation for binomial and trinomial trees. In Chapter 17, we will present another version for the Black-Scholes-Merton model.

Loosely speaking, the Fundamental Theorem of Asset Pricing states that:

a market model is free of arbitrage opportunities if and only if there exists at least one set of risk-neutral probabilities;

an arbitrage-free market model is complete if and only if there exists a unique set of risk-neutral probabilities.

In a one-period market model, such as the binomial and trinomial models, we obtain risk-neutral probabilities through the following equation:

(13.3.1)

Equation (13.3.1) is known as the risk-neutral condition.4 In other words, risk-neutral probabilities are artificial probabilities such that the risky asset S earns the risk-free rate r on average. Of course, this is not true using real-world probabilities: there is a real rate of return μ for S that is given implicitly by the model parameters. Let us see how the FTAP works in models we already know.

13.3.2.1 One-period binomial model

Let us first illustrate how the FTAP can be applied in the now well-known one-period binomial tree model. First of all, let us assume that the market is free of arbitrage opportunities, i.e. that sd < S0B1 < su. In a binomial environment, the risk-neutral condition of equation (13.3.1) is equivalent to

Since there is no arbitrage in this market, we have 0 < q < 1 and also 0 < 1 − q < 1. As expected from the FTAP, under the no-arbitrage assumption, we were able to find a risk-neutral probability. Finally, the risk-neutral probability q is unique and therefore the one-period binomial tree model is a complete market model.

13.3.2.2 One-period trinomial model

In the one-period trinomial model, the risk-neutral condition of equation (13.3.1) is equivalent to

Finding risk-neutral probabilities amounts to finding 0 < qd, qm, qu < 1 such that

(13.3.2)

We have three unknowns, namely qd, qm and qu, but only two conditions, namely the risk-neutral condition of (13.3.1) and the probability condition of (13.3.2). This means there are infinitely many solutions or, said differently, infinitely many different sets of probabilities {qd, qm, qu}.

As expected from the FTAP, since we are assuming the trinomial model is free of arbitrage, we are able to find at least one set of risk-neutral probabilities {qd, qm, qu}.

The converse of the FTAP can be illustrated as follows. Assume there exists a set of risk-neutral probabilities {qd, qm, qu}. This means that 0 < qu < 1, 0 < qm < 1 and 0 < qd = 1 − qu − qm < 1, and that

Since {qd, qm, qu} are probabilities, we have that S0B1 is a weighted average of the values {sd, sm, su}, so we have

This is the no-arbitrage condition for the one-period trinomial model.

13.3.3 Finding risk-neutral probabilities

We always assume that the trinomial tree is free of arbitrage, meaning that equation (13.1.1) is verified. Then, the FTAP guarantees the existence of at least one set of risk-neutral probabilities {qd, qm, qu}.

As discussed above, we will find infinitely many risk-neutral triplets {qu, qm, qd} satisfying conditions (13.3.1) and (13.3.2). We have that 0 < qd, qm, qu < 1 are such that

Clearly, we can reduce this to a system of one equation with two unknowns:

or, written differently,

(13.3.3)

In other words, we can parameterize qu in terms of qm, or vice versa.5 However, we have to make sure that

These last conditions will restrict the range of values for qu and qm, i.e. they will not be allowed to vary in the whole interval (0, 1).

The algebra needed to determine all possible risk-neutral triplets {qu, qm, qd} can be tedious but it is elementary, as we will see in the next example.

Example 13.3.1

Let us consider again the example where B1 = 1.1, S0 = 6 and where the possible values for S1 are su = 7.7, sm = 5.5 and sd = 3.3. As verified earlier, this trinomial model is free of arbitrage, so according to the FTAP, there are risk-neutral probabilities in this model.

The risk-neutral condition in (13.3.1) can be written here as

Collecting the terms for qu and qm, we get

If we decide to express qu in terms of qm, then we have

and

Our free variable qm might not be allowed to take any value in (0, 1). We must keep in mind that qu and qd, as functions of qm, must take values in (0, 1):

These two inequalities are equivalent to qm satisfying both

This means that qm must be chosen such that

or qu and qd might not belong to the interval (0, 1).

In conclusion, we have fully characterized the set of risk-neutral triplets (in terms of qm). Indeed, for any fixed and arbitrary value of qm taken in (0, 0.5), the corresponding values for qu and qd are given by

For example, if we take qm = 0.4, then

and we obtain the following risk-neutral triplet .

◼

13.3.4 Risk-neutral pricing

Now that we know how to obtain risk-neutral probabilities {qu, qm, qd} in a one-period trinomial tree, the next step is to find the interval of no-arbitrages prices as discounted risk-neutral expectations.

Let us denote by a set of risk-neutral probability weights {qu, qm, qd} (meeting the risk-neutral condition). Then, for a random payoff V1, the discounted risk-neutral expectation

lies within the interval of no-arbitrage prices meaning that

We will not provide a proof of this statement, but the discussion leading to both and should provide the necessary intuition.

This means that for a given risk-neutral probability triplet , the value is a valid no-arbitrage price for the payoff V1. The notation thus emphasizes that this price depends on the specific choice of risk-neutral triplet .

If the values of qu and qd are expressed as functions of qm, then we will write V0(qm) instead of to emphasize that the price is a function of qm. In other words, we will obtain a parameterized (in terms of qm) interval of arbitrage-free prices, just as in the super-replication and sub-replication procedure. The next example illustrates the process.

Example 13.3.2

Let us go back to the previous example where B1 = 1.1, S0 = 6, su = 7.7, sm = 5.5 and sd = 3.3. We have fully characterized the set of risk-neutral triplets in terms of qm: for each 0 < qm < 0.5, if we set

then the resulting triplet is a set of risk-neutral probabilities.

We would like to find the interval of no-arbitrage prices for a put option with strike price K = 6 and repeat the procedure for a strike price of K = 7.7.

First, if K = 6, then vu = (6 − su)+ = 0, vm = (6 − sm)+ = 0.5 and vd = (6 − sd)+ = 2.7, and, for a given , we have

As we have chosen to express qu and qd as functions of qm, we further obtain

Clearly, when qm covers the interval (0, 0.5), the corresponding values of P0(qm), which decreases in terms of qm, will be such that

As we now know, any put option price located within this interval will prevent arbitrage opportunities. We notice that those also correspond to the cost of the best super- and sub-replicating portfolios (see examples 13.2.7 and 13.2.8).

Second, if K = 7.7, then vu = (7.7 − su)+ = 0, vm = (7.7 − sm)+ = 2.2 and vd = (7.7 − sd)+ = 4.4, and, for a given , we have

In other words, no matter what is the triplet , the interval of no-arbitrage prices for this put collapses to a single value, more precisely P0 = 1. This should not be a surprise since we were able to exactly replicate this put option.

◼

Maximal and minimal no-arbitrage prices

It is possible to prove that

where and mean taking the infimum and the supremum over all possible risk-neutral triplets , respectively.

In particular, if qu and qd are expressed as functions of qm, then clearly we have

where means taking the infimum within the possible values for qm. It is now a minimization problem for a one-variable function. Similarly, we have

13.4 Completion of a trinomial tree

The reader might have noticed that the incompleteness of the trinomial tree model comes from an insufficient number of basic assets to perfectly hedge (to replicate) all risks in the model. Mathematically, this means trying to solve a system of three equations, associated to the three possible outcomes, with only two unknowns, associated to the two basic assets B and S.

If three basic assets were traded in this trinomial market, then replication would mean solving a system of three equations with three unknowns, making replication achievable. Adding a third basic asset, i.e. another risky asset such as another stock or index, will complete the trinomial market model, as we will see below.

13.4.1 Trinomial tree with three basic assets

If we add a third basic asset to the previous trinomial tree model, this asset must be such that:

it cannot be replicated with the first two basic assets, i.e. it is not a redundant asset;

it does not introduce any arbitrage opportunities into the market.

From a financial point of view, the first condition amounts to adding a new asset and not just a combination of the previous two basic assets. From a mathematical point of view, we want this asset to help us solve the system of equations associated to the replication problem. Let us illustrate this with an example.

Example 13.4.1Trinomial model with two stocks

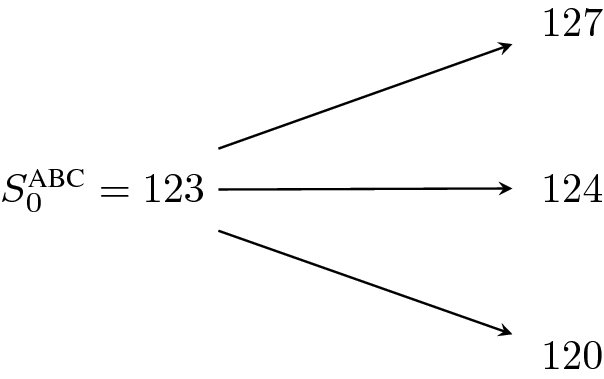

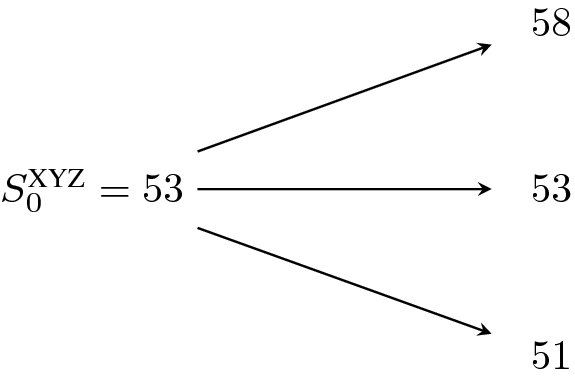

Consider a trinomial market model where two stocks are traded, that of ABC inc. and of XYZ inc., each evolving according to a 3-month trinomial tree. This is illustrated in the trees below.

We should note that the up scenario occurs at the same time for both stocks. We then say the events and are the same. This also holds true for the other two scenarios, meaning that the events and are also the same.

Assume also that the annual interest rate, compounded each 3 months, is at 4%. Thus, we have B1 = 1.01. We want to find the no-arbitrage price of a 3-month exotic derivative with payoff

In each scenario, the value of this payoff is given by

V1

u

6.50

m

2.50

d

0

In this modified trinomial model, a trading strategy is a triplet , where (resp. and y) is the number of units of (resp. and B) held in the portfolio from time 0 to time 1. If we want this strategy to replicate the payoff, we must solve:

Subtracting the first two equations and the last two in order to eliminate (1.01)y, we get

Consequently,

Putting these values back into one of the three original equations, we obtain

which yields y = −68.847242. Therefore, the initial value of this replicating portfolio (for this exotic derivative) is given by

By the no-arbitrage principle, this is also the derivative’s initial price.

◼

In the previous example, we saw a modified version of the trinomial tree model, now with three basic assets, namely B, and . This time, the fact that we were able to replicate the payoff V1 in a trinomial environment is not coincidental. Since none of the basic assets is redundant, it allowed us to replicate all the risks in the model. Mathematically, this meant solving a system of three equations, associated to the three possible outcomes, with now three unknowns, associated to the three basic assets B, and .

Here is another example where the third asset will be a credit default swap, as seen in Section 4.4 of Chapter 4.

Example 13.4.2Completing a trinomial market by adding a CDS6

Let us have another look at Example 13.0.1. We will introduce a third basic asset, namely a credit default swap (CDS) paying 1$ upon ABC inc.’s default, and 0 otherwise. As we are in a one-period model, assume the CDS requires a single premium at time 0. The following table illustrates the possible realizations of the three basic assets in the three scenarios, along with the payoff of the investment guarantee (IG).

Scenario

Bond B1

Stock S1

CDS CDS1

IG

u

1.04

50

0000

050

m

1.04

30

0000

040

d (default)

1.04

00

1000

040

Initial price

100

40

0.07

TBD

From the table, we have that S0 = 40 and that CDS0 = 0.07. Let us see how to use the CDS to manage credit risk and replicate the IG.

Let be the number of shares of the stock, the number of units of CDS and the number of bonds we need to buy to exactly replicate the payoff of the investment guarantee. We need to solve a system of three equations along with three unknowns:

From the first two equations, we directly find and y = 25/1.04 = 24.038461538. This is the same as in example 13.0.1. Now, from the third equation, we find

Therefore, we need to add 15 units of this CDS to the portfolio.

The initial cost of this replicating portfolio (for the IG) is thus

Compared with the strategy deployed in example 13.0.1, for an extra dollar (1.05 to be more precise) the company can completely hedge against credit risk and assure to meet its obligations in all three scenarios.

This is interesting because replicating the first two scenarios might yield a loss of $15 in case of bankruptcy of ABC inc. Therefore, we need to buy the number of CDS required to protect against a possible loss of $15.

◼

The previous example is pretty realistic in the sense that credit default swaps became commonly traded in the financial markets in the early 2000s. They were one of the many securities that appeared in the markets following the deregulation of financial markets between 1970 and 2000. Securitization is a process commonly used to create tradable securities and it became increasingly important during the same period to help complete the market.

In the insurance business, catastrophe and longevity derivatives, as seen in Chapter 7, can also be viewed as securities helping toward the completion of the insurance market. Natural catastrophe risk and longevity risk were traditionally managed by setting aside an appropriate reserve or with reinsurance. The emergence of these insurance derivatives helped risk managers transfer a significant part of these risks to other investors willing to bear them.

13.5 Incompleteness of insurance markets

Market incompleteness arises because there are risks that cannot be perfectly hedged using traded assets. Insurance markets are incomplete by nature: an insurer cannot replicate the payoff of a life insurance policy issued on the life of an individual by trading on the markets, e.g. by buying an equivalent policy from another company. Recall that this issue was discussed in Chapter 1.

The same holds true for most risks covered by life insurance, homeowner’s and car insurance, health insurance, etc. Therefore, the risk arising from issuing a call option on a stock needs to be managed differently than the risk coming from selling car insurance.

Example 13.5.1Selling car insurance

Imagine a very simple insurance market: there is one car owner seeking loss protection in case of an accident and there is an insurance company willing to sell such an insurance policy. Over the next year, there is a 2% probability of a car accident with damage $5000 and a 98% probability of no loss at all. The expected loss is thus $100.

The customer faces a risk and she seeks to transfer this risk in exchange for a premium. Unfortunately, with only one customer in the market, the insurance company cannot do much to manage this risk. The company cannot resell the policy to another entity, nor can it hedge this risk on the financial market. This over-simplified insurance market is incomplete.

◼

Example 13.5.2Incompleteness and mortality risk

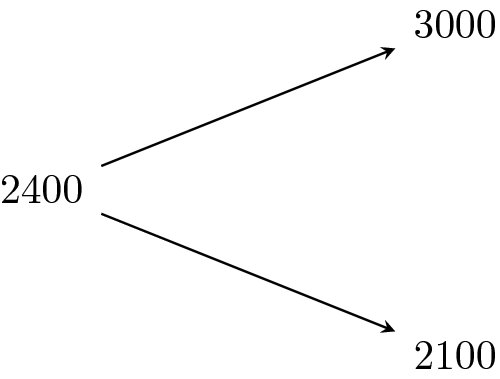

Consider an insured investing $100 in the following insurance product: the initial investment grows with a financial index while the capital is guaranteed upon death or maturity, whichever comes first. Assume the guaranteed amount at time 1 (maturity) is:

$112 if the investor dies prior to maturity;

$108 if the investor is still alive at maturity.

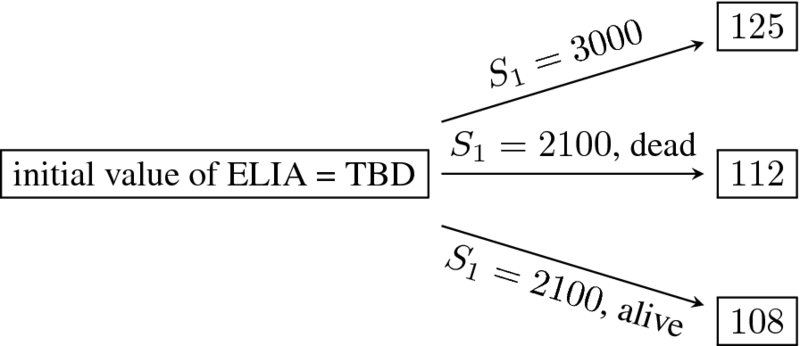

The current value of the financial index is S0 = 2400 and, at time 1, the index has possible terminal values of su = 3000 and sd = 2100, which means we assume the price of the financial index follows this tree:

Even if the financial index has two possible values at maturity, there is a total of four outcomes: the policyholder is either dead or alive at maturity, while the index has two possible values. For example, at maturity, the policyholder could be alive and the index could be worth $2100, or the policyholder could have died during the period and the index could be worth $2100, and so on. There are four possibilities, as shown in the next table.

Scenario

Index

Insured

Benefit

1

3000

Alive

125

2

3000

Dead

125

3

2100

Alive

108

4

2100

Dead

112

However, as we can see in this table, benefits only take three different values in these four states because the death and maturity benefits are the same when the index is at 3000.

Consequently, if we are only interested in pricing and risk managing this insurance product, we can model this situation with a one-period trinomial tree model:

There are two basic assets traded in this market and three possible outcomes driven by the survival of the individual. Market incompleteness arises from the (legal) impossibility to trade individual mortality risk.

◼

We have illustrated how market incompleteness appears in the insurance market. We now illustrate how insurers deal with market incompleteness when they issue typical insurance policies to individuals.

Example 13.5.3Selling car insurance (continued)

Car insurance works well when there are many similar individuals whose risk is independent from one to another. Now assume the company has issued such a policy to 10,000 of these individuals and that if one ends up in a car accident then the likelihood of another insured ending up in another accident is not impacted (statistical independence). Each of these insureds faces an important potential loss, but here insurance will work: the company can write a car insurance policy to each of these individuals and charge a premium of about $100 due to diversification.

It is important to note that even if the insurance market is composed of thousands of i.i.d. individuals, it is still incomplete because it is impossible for an insurance company to trade assets to replicate the risks arising from its car insurance policies. The insurer can manage this risk by issuing a sufficient number of policies, thanks to diversification. As seen in Chapter 1, for such a large portfolio of independent and identically distributed risks, it can predict with almost certainty the total number of claims.

◼

Example 13.5.4Incompleteness and mortality risk (continued)

In the context of the previous example, assume that $1 invested at the risk-free rate accumulates to 1.10 over that period. Assume also that mortality risk (from the insured) is independent of the evolution of the financial index.

Let us describe the risk management implications of selling this equity-linked insurance product with an initial investment of $100 to:

a single 60-year-old policyholder having a 1-year death probability of 1%;

10,000 (independent) 60-year-old policyholders each having a 1-year death probability of 1%.

There are two risks embedded in this contract: the financial risk from the random variations of the financial index used to determine the benefit, while the actuarial risk stems from the uncertainty of the survival of the policyholder(s).

1) With a single policyholder in the insurance market, the insurer assumes entirely the uncertainty on the life of the policyholder as it cannot trade the mortality of this investor.

One possible hedging strategy could be built as if the policyholder were to survive until maturity, i.e. by ignoring the third scenario (the one where the index goes down to $2100 and the policyholder is dead at maturity, in which case the benefit would be equal to $112). As we now know, this would lead to a sub-replicating portfolio for this investment guarantee.

One more conservative hedging strategy could be built as if the policyholder were to die prior to maturity, i.e. by ignoring the second scenario (the one where the index goes down to $2100 and the policyholder is still alive at maturity, in which case the benefit would be equal to $108). As we now know, this would lead to a super-replicating portfolio for this investment guarantee.

2) Across the 10,000 insureds, the financial risk is systematic, i.e. the financial index will go up or will go down for all 10,000 contracts, while the mortality risk is diversifiable. Now, let us see how the insurance company can manage the risks underlying these contracts, as we did in Section 8.5 of Chapter 8. In particular, we refer to example 8.5.2.

Due to the law of large numbers, we can expect that 100 policyholders will die by the end of the year, whereas 9900 of these will survive. In other words, we expect that 100 contracts will require the payment at maturity of a benefit worth either $125 or $112 depending on the index value at that time, while 9900 contracts will require the payment of a benefit worth either $125 or $108 depending on the index value at that time.

Said differently, selling this investment guarantee to those 10,000 insureds is, on average, equivalent to selling instead:

100 investment guarantees with a guaranteed amount of 112;

9900 investment guarantees with a guaranteed amount of 108.

As mentioned before, as the number of deaths will not be exactly 100, the insurance company will not be perfectly hedged. In practice, companies set aside a provision for adverse deviations of mortality.

◼

These examples have shown that to manage typical insurable risks that cannot be replicated in the markets, insurance companies need to diversify these risks across a large number of policyholders. We have also illustrated that systematic and diversifiable risks need to be treated differently. Ideally, systematic risks should be hedged as much as possible, or even replicated when possible, whereas diversifiable risks should be mitigated by underwriting additional independent policyholders.

13.6 Summary

One-period trinomial model

Risk-free interest rate: r.

Risk-free asset price: B = {B0, B1}, where B0 = 1 and

Risky asset price: S = {S0, S1}, where S1 is a random variable such that

No-arbitrage condition: sd < S0B1 < su.

Derivative (written on S): V = {V0, V1} where V1 is a random variable such that

Simplified tree: up and down factors u > m > d such that

Alternative no-arbitrage condition: d < B1 < u.

Trading strategy/portfolio

Portfolio: a pair (x, y).

Number of units of S, the risky asset: x.

Number of units of B, the risk-free asset: y.

Portfolio’s value: Π = {Π0, Π1} where

Pricing by replication

A strategy (x, y) replicates V1 if its time-1 value is such that Π1 = V1, i.e. if

For most payoffs V1, a (unique) solution/portfolio cannot be found.

Attainable payoff: V1 is attainable if it admits a replicating portfolio.

Complete market model: all payoffs are attainable.

One-period trinomial model (with one risky asset) is an incomplete market.

A strategy (x, y) super-replicates V1 if its time-1 value is such that Π1 ⩾ V1, i.e. if

The best super-replicating strategy is the cheapest. Its initial value is given by .

A strategy (x, y) sub-replicates V1 if its time-1 value is such that Π1 ⩽ V1, i.e. if

The best sub-replicating strategy is the most expensive. Its initial value is given by .

No-arbitrage price V0 of a derivative is not unique: there exists an interval of no-arbitrage prices .

When a security is attainable, the interval collapses to a single value .

Pricing with risk-neutral probabilities

Risk-neutral probabilities: triplet such that

For each triplet , there is a corresponding no-arbitrage price given by the discounted risk-neutral expectation:

In trinomial model:

– exists infinitely many risk-neutral triplets;

– no-arbitrage price of a derivative is not unique: there exists an interval of no-arbitrage prices .

Fundamental Asset Pricing Theorem:

– a market model is free of arbitrage opportunities if and only if there exists at least one triplet of risk-neutral probabilities;

– an arbitrage-free market model is complete if and only if there exists a unique triplet of risk-neutral probabilities.

Completion of a trinomial model

Add another basic risky asset such that:

– not redundant, i.e. cannot be replicated with the first two basic assets;

– does not introduce any arbitrage opportunities.

Consequence of completion: replication is possible (exists unique replicating portfolio) for any payoff. Market model is complete.

Incompleteness of insurance markets

Incompleteness in general stems from a lack of tradable assets.

Insurance markets are incomplete by nature: it is not possible to replicate most typical insurable risks using tradable assets. Laws and regulations prevent this.

Diversification is a mean to attenuate the adverse effects of the incompleteness of insurance markets.

13.7 Exercises

Suppose there are three states of the economy, namely Ω = {ω1, ω2, ω3}, and there exist three securities S(i)T, for i = 1, 2, 3, paying $1 at time T if scenario/state i is observed. Such a market is known as an Arrow-Debreu market (or economy). The payoff at time T and the current prices for these securities are shown in the table.

ωi

S(i)0

S(i)T

ω1

0.45

1

ω2

0.40

1

ω3

0.10

1

Assume that T = 1 for simplicity.

To avoid arbitrage opportunities, what is the current price of a security paying $1 with certainty?

What is the risk-free rate?

What is the risk-neutral probability of observing state ω2?

To avoid arbitrage opportunities, what is the current price of a stock that is worth 100 in state ω1, 75 in state ω2 and 0 otherwise?

In a financial market, it is possible to buy a share of stock whose value in one period will be in {5, 10, 15}. Assume all derivatives mature in one period and the risk-free rate is 0%. Determine whether the following derivatives are attainable:

a 10-strike call option;

a 5-strike call option;

a 10-strike put option;

a 15-strike put option.

In (a)–(d), would you change your answer if B0 = 1 and B1 > 1? What is (are) the condition(s) on the payoff to ensure a derivative is attainable? Is this market model complete? Justify your answer.

Suppose that for $27, you can buy an asset whose value in one period will be in {23, 28, 32}. Moreover, the risk-free asset is such that B0 = 1 and B1 = 1.1.

Verify that this model is arbitrage-free.

Is this market model complete? Justify your answer.

Using sub-replication and super-replication, find the interval of no-arbitrage prices for a call option with strike price K = 30.

Find all risk-neutral probabilities.

Using risk-neutral pricing, find the interval of no-arbitrage prices for a call option with strike price K = 30.

As in example 13.2.1, a risky asset will take one of the three following values one period later: 7.70, 5.50 or 3.30. Moreover, the risk-free rate is 10% and the initial stock price is 6.60.

Compute the risk-neutral weights of observing u and d if we ignore the existence of scenario m. Is this a probability? Compute the price of a 6-strike put option and relate to the cost of the sub- or super-replicating portfolio.

Compute the risk-neutral weights of observing u and m if we ignore the existence of scenario d. Is this a probability? Compute the price of a 6-strike put option and relate to the cost of the sub- or super-replicating portfolio.

Compute the risk-neutral weights of observing m and d if we ignore the existence of scenario u. Is this a probability? Compute the price of a 6-strike put option and relate to the cost of the sub- or super-replicating portfolio.

In light of (a), (b) and (c), what do you observe?

Consider the following one-period market model with three scenarios and three assets:

Scenario

S(1)1

S(2)1

S(3)1

1

85

0

0

2

100

7

0

3

125

31

18

with S(1)0 = 100, S(2)0 = 9 and S(3)0 = 6. Build a replicating portfolio using the above three assets only in order to find the value of a risk-free asset paying $1 in all three scenarios. Then, deduce the interest rate in this market model.

In the context of example 13.0.1, replicate the investment guarantee assuming the underlying stock follows a binomial model, by ignoring the bankruptcy scenario, and set aside an amount corresponding to the average loss in the bankruptcy scenario. Compare this hedging strategy to the one using a CDS as presented in example 13.4.2. Does it change your answer if you set aside twice or five times the average loss?

Verify that the model considered in example 13.4.1 is free of arbitrage opportunities.

In the context of example 13.5.4 where mortality is managed with a large portfolio, describe the cash flows of the hedging strategy in the scenario that:

93 insureds die during the year (instead of 100);

109 insureds die during the year (instead of 100).

In example 13.3.1, we expressed qu and qd in terms of qm. Redo the example and express qm and qd in terms of qu. Verify that the intervals you obtain are consistent with those already obtained and that setting qu = 0.55 also yields the triplet .

Consider the following two-period market model:

scenario

S0

S1

S2

C2

1

2

2

2

0

2

2

2

3

0

3

2

4

3

0

4

2

4

4

1

5

2

4

6

3

with B0 = (1.1)− 2, B1 = (1.1)− 1 and B2 = 1.

An investor believes that the risky asset will be worth less than $3 at time 2, so she is selling right now the call option with payoff C2, i.e. written on S and with a strike price of K = 3.

Use a tree to describe the dynamics of S.

Verify that this model is free of arbitrage opportunities.

Find a two-period replicating portfolio for this call option and deduce the initial value of the option.

Find the risk-neutral probabilities in this model by looking at each one-period sub-tree separately.

For each risk-neutral probability, compute the corresponding (risk-neutral) value of the option. Is there a pattern?

With the above computations in hand, would you say that this model is complete? Justify your answer.

Consider the following two-period market model where B is the risk-free asset and S the risky asset:

scenario

S0

S1

S2

B0

B1

B2

1

1

1

1

1

1.1

1.2

2

1

1

2

1

1.1

1.2

3

1

2

1

1

1.1

1.3

4

1

2

2

1

1.1

1.3

5

1

2

3

1

1.1

1.3

At time 0, Mr. Brown has the following financial position: he holds three units of the risk-free asset and four units of the risky asset. Another investor, Mrs. McFly, is short two units of the risk-free asset and long nine units of the risky asset. They will both hold on to these positions until time two.

Mrs. McFly has an offer for Mr. Brown: at time 2, he can choose to exchange their financial positions, or not.

How much should Mr. Brown give to/receive from Mrs. McFly, at time 0, for this offer to be fair? To provide an answer to this question, follow these steps:

Use a tree to describe the dynamics of S and compute the payoff of the above exchange derivative.

Verify that this model is free of arbitrage opportunities.

Find the risk-neutral probabilities in this model by looking at each one-period sub-tree separately.

Is the exchange derivative an attainable derivative? Is this model complete? Justify your answer.

For each risk-neutral probability, compute the corresponding (risk-neutral) value of the exchange derivative.

So, should Mr. Brown give something to Mrs. McFly to enter this agreement? Or is it the other way around?

Exercises 13.10 and 13.11 have been inspired by two exercises from Geneviève Gauthier, with her permission.

):

):

, two more than the corresponding one-period binomial model.

, two more than the corresponding one-period binomial model.

. From the above information, pd = 0.04 while pu = pm = 0.48, which means that the trinomial tree for the stock is

in either the risk-free asset B or the risky asset S should be such that S1 > S0B1 and S1 < S0B1 are both inadmissible. Mathematically, the arbitrage-free condition reads as follows:

in either the risk-free asset B or the risky asset S should be such that S1 > S0B1 and S1 < S0B1 are both inadmissible. Mathematically, the arbitrage-free condition reads as follows:

):

):

solving

is what we call a sub-replicating portfolio because

.

, in all three scenarios. Suppose now that the put option can be bought for only $0.50. Let us explain how to exploit this arbitrage opportunity.

solving

is a super-replicating portfolio because

in all three scenarios. Suppose now that the put option can be sold for $4. Explain how to exploit an arbitrage opportunity, if any.

, in all three scenarios. What this says is that the no-arbitrage price of the put option should be at least −4.423076923, which is not informative since we already found that it should be larger than 0.76923 to avoid arbitrage.

, in all three scenarios. What this says is that the no-arbitrage price of the put option should be at least −4.423076923, which is not informative since we already found that it should be larger than 0.76923 to avoid arbitrage.

such that

such that

is the cheapest in the set of all super-replicating strategies. In other words, there might exist many super-replicating strategies

is the cheapest in the set of all super-replicating strategies. In other words, there might exist many super-replicating strategies  for V1 and the best is simply the one with the lowest cost. We denote the initial value of

for V1 and the best is simply the one with the lowest cost. We denote the initial value of  by

by  .

.

such that

such that

is the most expensive in the set of all sub-replicating strategies. In other words, there might exist many sub-replicating strategies

is the most expensive in the set of all sub-replicating strategies. In other words, there might exist many sub-replicating strategies  for V1 and the best is simply the most expensive. We denote the initial value of

for V1 and the best is simply the most expensive. We denote the initial value of  by

by  .

.

will not give rise to an arbitrage opportunity in the trinomial tree. This is also true of incomplete market models in general.

will not give rise to an arbitrage opportunity in the trinomial tree. This is also true of incomplete market models in general.

: each price in that interval prevents arbitrage opportunities. This is not very useful: we cannot buy or sell a security using an interval of prices. We need to find a price.

: each price in that interval prevents arbitrage opportunities. This is not very useful: we cannot buy or sell a security using an interval of prices. We need to find a price. whereas the smallest price at which the seller is willing to sell is

whereas the smallest price at which the seller is willing to sell is  . This is because the best sub- (super-) replicating portfolio assures the buyer (seller) cannot lose. It is therefore impossible to obtain a unique price at which both the seller and buyer will agree. At any price in between

. This is because the best sub- (super-) replicating portfolio assures the buyer (seller) cannot lose. It is therefore impossible to obtain a unique price at which both the seller and buyer will agree. At any price in between  and

and  , the buyer and/or seller will assume some level of risk. Thus, in order to find a price, we will need additional assumptions on the market and the behavior of the buyer(s) and seller(s).

, the buyer and/or seller will assume some level of risk. Thus, in order to find a price, we will need additional assumptions on the market and the behavior of the buyer(s) and seller(s).

provides the smallest no-arbitrage price for the corresponding derivative. Even if this portfolio is built to mimick the payoff in only two scenarios, it is still possible to rewrite its cost in terms of a discounted risk-neutral expectation. This will attribute fictitious weights to scenarios u, m and d, similar to what happened in the binomial model. The same can be done for the best super-replicating portfolio.

provides the smallest no-arbitrage price for the corresponding derivative. Even if this portfolio is built to mimick the payoff in only two scenarios, it is still possible to rewrite its cost in terms of a discounted risk-neutral expectation. This will attribute fictitious weights to scenarios u, m and d, similar to what happened in the binomial model. The same can be done for the best super-replicating portfolio.

. As a consequence, we can also write

. As a consequence, we can also write

means we are attributing probabilities

means we are attributing probabilities  to scenarios {u, m, d}, respectively.

to scenarios {u, m, d}, respectively.

. As a consequence, we can also write

. As a consequence, we can also write

means we are attributing probabilities

means we are attributing probabilities  to scenarios {u, m, d}, respectively. The methodology is similar when S0B1 > sm, in which case we should consider scenarios m and u.

to scenarios {u, m, d}, respectively. The methodology is similar when S0B1 > sm, in which case we should consider scenarios m and u. and

and  , as well as

, as well as  and

and  . Then, the range of call option prices such that there are no arbitrage opportunities is given by

. Then, the range of call option prices such that there are no arbitrage opportunities is given by

or

or  .

. to be a risk-neutral probability measure, it has to be equivalent to

to be a risk-neutral probability measure, it has to be equivalent to  . Two probability measures

. Two probability measures  and

and  are equivalent when outcomes that are certain or impossible are the same under both measures.

are equivalent when outcomes that are certain or impossible are the same under both measures. and

and  assign a zero probability to one of the three possible outcomes and therefore both

assign a zero probability to one of the three possible outcomes and therefore both  and

and  are not equivalent to

are not equivalent to  . For example, we have

. For example, we have  while

while  .

.

.

as discounted risk-neutral expectations.

as discounted risk-neutral expectations. a set of risk-neutral probability weights {qu, qm, qd} (meeting the risk-neutral condition). Then, for a random payoff V1, the discounted risk-neutral expectation

a set of risk-neutral probability weights {qu, qm, qd} (meeting the risk-neutral condition). Then, for a random payoff V1, the discounted risk-neutral expectation

and

and  should provide the necessary intuition.

should provide the necessary intuition. , the value

, the value  is a valid no-arbitrage price for the payoff V1. The notation

is a valid no-arbitrage price for the payoff V1. The notation  thus emphasizes that this price depends on the specific choice of risk-neutral triplet

thus emphasizes that this price depends on the specific choice of risk-neutral triplet  .

. to emphasize that the price is a function of qm. In other words, we will obtain a parameterized (in terms of qm) interval of arbitrage-free prices, just as in the super-replication and sub-replication procedure. The next example illustrates the process.

to emphasize that the price is a function of qm. In other words, we will obtain a parameterized (in terms of qm) interval of arbitrage-free prices, just as in the super-replication and sub-replication procedure. The next example illustrates the process.is a set of risk-neutral probabilities.

, we have

, we have

, the interval of no-arbitrage prices for this put collapses to a single value, more precisely P0 = 1. This should not be a surprise since we were able to exactly replicate this put option.

and

and  mean taking the infimum and the supremum over all possible risk-neutral triplets

mean taking the infimum and the supremum over all possible risk-neutral triplets  , respectively.

, respectively.

means taking the infimum within the possible values for qm. It is now a minimization problem for a one-variable function. Similarly, we have

means taking the infimum within the possible values for qm. It is now a minimization problem for a one-variable function. Similarly, we have

and

are the same. This also holds true for the other two scenarios, meaning that the events

and

are also the same.

, where

(resp.

and y) is the number of units of

(resp.

and B) held in the portfolio from time 0 to time 1. If we want this strategy to replicate the payoff, we must solve:

and

and  . This time, the fact that we were able to replicate the payoff V1 in a trinomial environment is not coincidental. Since none of the basic assets is redundant, it allowed us to replicate all the risks in the model. Mathematically, this meant solving a system of three equations, associated to the three possible outcomes, with now three unknowns, associated to the three basic assets B,

. This time, the fact that we were able to replicate the payoff V1 in a trinomial environment is not coincidental. Since none of the basic assets is redundant, it allowed us to replicate all the risks in the model. Mathematically, this meant solving a system of three equations, associated to the three possible outcomes, with now three unknowns, associated to the three basic assets B,  and

and  .

.be the number of shares of the stock, the number of units of CDS and the number of bonds we need to buy to exactly replicate the payoff of the investment guarantee. We need to solve a system of three equations along with three unknowns:

and y = 25/1.04 = 24.038461538. This is the same as in example 13.0.1. Now, from the third equation, we find

is the cheapest. Its initial value is given by

is the cheapest. Its initial value is given by  .

.

is the most expensive. Its initial value is given by

is the most expensive. Its initial value is given by  .

. .

. .

. such that

such that

, there is a corresponding no-arbitrage price given by the discounted risk-neutral expectation:

, there is a corresponding no-arbitrage price given by the discounted risk-neutral expectation:

.

. .

.