9

Strategic Planning and the Business Plan

Local governments need to ensure that their strategic plans and business plans are consistent and interconnected. Planners now recognize that resource allocations that result from the strategic plan’s objectives and tactics must be coordinated with ongoing budgeting tasks, responsibilities, and work assignments.

The three-year (2003–2005) plan of Grand Rapids, Michigan, includes the following statement on its cover.

Several documents represent the strategic direction of the city, including the city’s mission statement, fiscal plan, performance measurement plan, three-year strategic plan, and various departmental, technical, and community strategic plans. Together, these documents form the strategic blueprint for the city to provide equitable access to urban life for all citizens.

Worcester, Massachusetts, is typical. Goals, objectives, and strategies of its strategic plan for 2000 were all tied to its performance budgeting system, which identifies service delivery inputs, outputs, and departmental outcomes. These were linked to departmental performance, budget priorities, and financial allocations. The system identifies costs, benefits, efficiencies, and constraints of municipal dollars and services.

In Maricopa County, Arizona, the 2000 strategic planning effort made a clear connection between strategy and business planning.

Maricopa County is ready to manage for results, developing strategic plans that integrate planning with budgeting and performance measurement. This effort will create powerful tools for making good business decisions and achieving department/agency and corporate goals and priorities….Of importance, the guide will provide information and time lines on how the county will move toward performance-based budgeting and the integration of results-oriented performance information in every employee’s appraisal….The resource guide also provides the methodology for creating alignment of the people, resources, and systems of each department/agency. This makes it possible for each employee to know how his or her job contributes at every level of the organization.

This thorough integration of various planning and budgeting programs has been acknowledged consistently by the communities cited in this book. In some cases, the budget and business plans were used to drive the strategic planning process, although in most instances that order was reversed. In many cases, the municipal leadership incorporated the components of the budget into the strategic plan itself. Objectives and implementation plans from the strategic plan are also frequently embedded into the budget process and documents. See Appendix H for an example of Winston-Salem, North Carolina’s integration of strategic planning and business planning.

In this way, planners and staff are forced to connect the documents, the thinking, and the planning. Neither the strategic plan nor the business plan is entirely functional without the other. Making the connection ensures that the ongoing decision-making processes concerning resource allocations are governed not just by funding availability but also within the context of established needs assessments and priorities, and with an eye on the long-term vision for the community. The budget transmittal document of Sedona, Arizona, shows how cross-referencing also enables staff to assign proper priorities to long-term and day-to-day operations.

The FY 2001 budget represents the first strategically developed expenditure plan. The city council’s adoption of the strategic management and planning system…laid the foundation for the development of this budget document. The strategic management and planning system links the strategic and community plan’s goals and objectives to the planning process. This linkage is accomplished through a series of issue papers or decision packages that the city council approves for major expenditures and work objectives for the upcoming fiscal year. This alignment of the strategic and community plans with the budget and work priorities for the city is intended to make sure that “first things are put first.”

Sedona then itemized planned expenditures in the context of the relevant strategic focus.

|

Proposed budget expenditure |

Cost |

Strategic plan reference |

|

Traffic officer to improve traffic enforcement and education |

$36,110 |

Customer service goals and objectives, goal #1: Provide high quality, effective, and efficient public service |

|

Assistant engineer/project manager to manage major sewer and non-sewer collection and conveyance system |

$43,192 |

Infrastructure goals and objectives, goal #1: Continue expansion of the city’s sewer projects |

|

Assistant planner to provide quality controls on the city’s current planning efforts |

$36,865 |

Smart growth management goals and objectives, goal #2: Strengthen the city’s design standards to prevent franchised architecture, thereby retaining our unique community |

|

Maintenance crew to maintain drainage ditches, cut brush, and perform other right-of-way maintenance |

$150,496 |

Customer service goals and objectives, goal #1: Provide high quality, effective, and efficient customer service |

Both Olathe, Kansas, and Columbus and Franklin County, Ohio, make a very clear connection between the needs of the community as laid out in the strategic plan and the budget that will support the programs planned to meet these needs.

To make clear the link between the strategic plan and the budget, the Olathe, Kansas, 2001 strategic plan summarizes its strategic targets (goals); numbered items are action items from the plan. For each of the action items, a parenthetical statement about the cost of each action is inserted.

1.City should actively consider traffic mitigation needs when planning, developing, and constructing all infrastructure projects (costs borne by developer)

2.City should consider the impact that all infrastructure projects have on east/west connections before plans are finalized

- Develop the 127th Street overpass (approximately $15 million)

- Develop the 159th Street connection (approximately $36 million)

- Develop the 111th Street arterial in partnership with the school district and county (approximately $18 million)

3.City should consider the impact that all infrastructure projects have on circulation patterns in and around downtown. The city should also consider opportunities that:

- Move traffic north/south in the area west of Olathe Lake and around downtown (approximately $100 million)

- Capitalize on opportunities to create a gateway to the city from the south, such as extending Kansas Avenue south of the mall (cost to be determined)

4.City infrastructure funding priorities should be assessed in terms of their impact on how they promote traffic flow…. The city should also provide needed funding to keep infrastructure working properly (approximately $70,000 annually)

5.City annexation and development criteria should consider impact on traffic flow (approximately $50,000 annually)

6.City should use intelligent transportation systems technology to improve traffic flow (approximately $6 million).

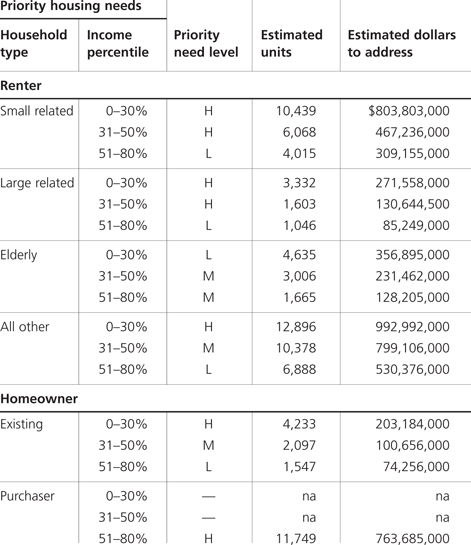

The consolidated plan of Columbus and Franklin County, Ohio, covers their collective housing and community development needs, and it uses a slightly different format, as seen in the following sample section.