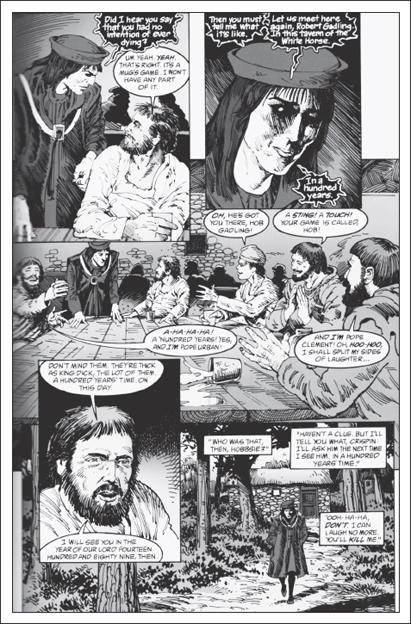

Hob Gadling was drinking in an English tavern in AD 1389 when he made the comment that “Death is a mug’s game.” 1 Dream and Death, of the Endless, happened to hear Gadling’s comment, and at Dream’s request, Death agreed to let Gadling live until he wanted to die. Dream approached Gadling for a drink and the two arranged to meet at the same bar at the same time on the same day—a hundred years in the future. Gadling thought it was a joke, but a hundred years later, there he was.

That, my friend, is how you do it. Neil Gaiman et al., Men of Good Fortune, in SANDMAN (VOL. 2) 13 (DC Comics February 1990).

Gadling is a recurring character in Neil Gaiman’s epic Sandman run, and one of the characters that most directly addresses one of the problems with immortality: How can one retain one’s fortune over the years without people figuring out that one is immortal? There are a number of reasons one might wish to keep such a thing secret—pitchforks, torches, etc.—but completely reinventing one’s self every few decades defeats one of the obvious advantages of immortality, i.e., the ability to accumulate wealth over a much, much longer period of time than we mere mortals.

In this chapter, we take a look at some of the legal issues surrounding death and dying. First, whether there are any inherent problems with abnormally long life spans. Second, the problems associated with creating and maintaining successive cover identities. Finally, we’ll examine the implications of resurrection on inheritance and property law.

“The days of our years are threescore years and ten; and if by reason of strength may be fourscore years, yet is their strength labour and sorrow; for it is soon cut off, and we fly away.” 2 Or, at least, that’s been the received wisdom since longer than anyone can remember. And because death after seventy or eighty years is such a fundamental part of the human experience, the difference between living two hundred years and not dying at all is, from the perspective of the legal system, pretty trivial.

Turning back to Gadling, one of the problems he ran into was people starting to get suspicious about his preternatural agelessness. This required him to disappear off to Scotland or the East Indies on a number of occasions, to return as his own long lost “son.” This gets at one of the main issues that an immortal who doesn’t want his immortality to be widely known will have to face: the creation and maintenance of successive cover identities.

The idea of an alter ego comes with certain legal complications, as has been recognized long before the publication of the first comic book. In Robert Louis Stevenson’s Strange Case of Dr. Jekyll and Mr. Hyde, first published in 1886, one of the main plot drivers is Jekyll’s pains to ensure that he maintains access to his property when he changes into Hyde. 3 This largely took the form of instructing his servants to pay heed to Hyde and executing a will leaving everything to Hyde should Jekyll disappear.

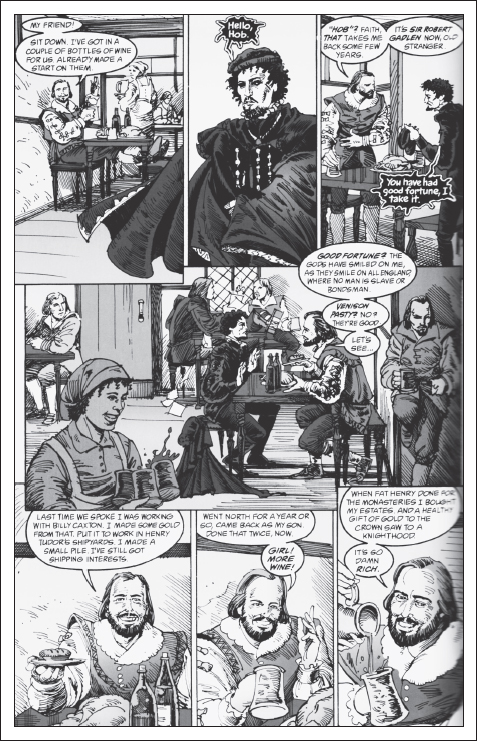

Hob Gadling explains some of the practical details of amassing wealth and creating new identities as an immortal being. Neil Gaiman et al., Men of Good Fortune, in SANDMAN (VOL. 2) 13 (DC Comics February 1990).

Legally, there is no reason Jekyll could not do this. A property owner may dispose of his property in any legal way that he sees fit, and giving it to himself, while usually pointless, is not illegal. The problem is not that Jekyll’s design was illegal, but that it was unusual, to the point that people noticed something was up. Indeed, it was the very attempt to create and maintain this alter ego that led to the discovery of his dual identity. If Jekyll/Hyde had been content to live two entirely different identities with no overlapping property or affairs, i.e., if Hyde had been willing to forego all of Jekyll’s advantages, the story could have ended quite differently.

So the problem is not only in the creation of an alter ego, but doing so within the bounds of the law in ways that will maintain the integrity of the illusion. Both of these will cause problems on a number of levels.

The relationship between one’s real and cover identities is significant. If one starts life as a mundane person and then acquires a masked identity, e.g., Bruce Wayne becoming Batman, things are fairly straightforward. Wayne doesn’t usually run errands as Batman, so his cover identity doesn’t really need legal papers or even identification. But creating a new mundane identity to live and work in, as one would need to do if faking one’s own death or moving from one mundane identity to another, is more difficult. Governments do this for people on a regular basis for things like witness protection programs, espionage, and undercover operations, but there are two main facts about this that present problems for superheroes. First, government-created identities are obviously created with government approval, so no laws are being broken. Second, outside of witness protection these identities are rarely intended to be used either for significant transactional purposes or for very long, i.e., they are not intended to fully or permanently replace the original identity.

The basic problem then is that to create a new identity without government authorization requires the commission of a number of federal felonies, potentially including making false immigration statements, identification document fraud, perjury and numerous related offenses under state law. 4 And trying to live in contemporary society without such documents will be very, very difficult. One cannot buy a car, rent an apartment, get a checking account, or engage in a host of transactions essential to the logistics of mundane life without some form of government identification, identification that a superhero wanting to create a new mundane identity would need to forge. Creating successive false identities all but requires one to engage in illegal activities. See, for example, the discussion of immigration law in chapter 10. Hob Gadling actually comments that maintaining these identities has gotten harder with the bureaucratization of society in the twentieth century.

Even if our hero can stomach breaking the law in this way, these sorts of illegalities do tend to attract enough attention to make maintaining a secret identity pretty difficult, particularly if one wishes to maintain some kind of base-level commitment to law and order. Al Capone was eventually brought down not for racketeering or the St. Valentine’s Day Massacre, but for simple tax evasion.

Speaking of taxes, transferring large sums of money without a paper trail is difficult to do legally. Money laundering is a federal offense, and suggestions of financial shadiness tend to attract the attention of prosecutors. Jumping through offshore banks is no guarantee of secrecy either, as the discipline of forensic accounting exists almost solely to analyze patterns of financial transactions for irregularities. Even sticking to cash transactions is no solution: (1) one cannot move more than ten thousand dollars in cash across the border without declaring it; (2) banking transactions over ten thousand dollars in cash in a single day must be reported to regulators. 5

So even though money must technically be “dirty,” i.e., the proceeds of or used for some unlawful activity, 6 in order for disguising the origin and ownership of such funds to be a felony, simply the attempt to disguise it is likely to raise red flags all over the place, because most of the people engaged in that sort of activity are doing so for nefarious reasons. If our superhero or an artificial “mundane” persona is going to need to spend any money, this poses problems of the sort that could easily trigger an IRS audit. As the Joker observed, “I’m crazy enough to take on Batman, but the IRS? No, thank you!” 7 So again, it seems that some of our heroes are faced with a difficult choice: maintain their secret identity or live within the bounds of the law. But even breaking the law in this way is no guarantee of success.

So basically, if an immortal wants to disguise his immortality, he’s going to have a pretty tough time doing it. Much of what he’ll need to do is illegal, and even the technically legal things are often so shady as to attract unwanted attention. This is not to say that it’s impossible, but most of the people who have successfully pulled off something like this usually tend to lie low.

Generally speaking, the legal system is set up to deal with people dying on a regular basis, and even someone living past a hundred does odd things to societies in which inheritance is important.

But when people start living much past that, especially if they aren’t aging normally, things can get really weird. This is important for comic book stories, because even ignoring the fact that time passes somewhat strangely in comic book universes (i.e., the origin story of various characters has been “time shifted” forward—Tony Stark was once imprisoned in the Vietnam War, then the first Gulf War, and now it’s Afghanistan) when compared with how time passes in the “real world,” comic book universes are full of characters that live for a long time, potentially forever. 8 Marvel has Wolverine, Apocalypse, Deadpool, and Dr. Strange, and that’s not even the whole list of arguably human characters. DC has Ra’s al Ghul, Wonder Woman, and quite possibly Superman as well. Is there anything illegal, as such, about being immortal?

Not as such, at least not in the real world or in comic books that aren’t Logan’s Run, 9 and there aren’t any laws against reaching any particular birthday either. But there are a few legal doctrines for which immortality could prove quite problematic. The biggest one has to do with property ownership. The way things are now, when a person buys a piece of real estate, he can generally assume that he has what is called a “fee simple,” i.e., complete freehold ownership of the land with no termination condition. 10 This is frequently referred to as having “clear title,” and it’s so important that banks will generally not sell a mortgage for a property where clear title is in question. 11

As it turns out, the legal system is actually pretty invested in making sure this happens, and the device that ensures it is the bane of first-year law students everywhere: the Rule Against Perpetuities, frequently abbreviated as the RAP. To explain the RAP, we’re afraid we’ll have to turn to a non-comic-book example.

Consider a family dairy farm. Say mom ’n’ pop are sentimental about the farm, so they leave it to their son with some conditions, like so: “To our son, we leave the family dairy farm, but if he ever stops using it as a dairy farm, the property will go to our eldest grandson.” This means that the son will not have a fee simple to the land, 12 because there is a condition wherein he might lose it. But the grandson can do whatever he wants with it: the condition stops with the son’s ownership.

But what if they said: “To our son, we leave the family farm, but if he or any of our descendants ever stop using it as a dairy farm, the property will go to the next-eldest descendant.” That’s quite a bit more restrictive, because while the first example would theoretically permit the grandson to turn the farm into a subdivision (or a horse ranch or whatever) because the condition only applied to the son, the latter example does not. This will make it a lot harder to use the property as anything but a dairy farm, even if the property can’t be used that way anymore (e.g., if zoning regulations prevent it or cows go extinct or something).

The RAP dates back to early-modern England, when it was realized that aristocratic families were doing exactly this sort of thing, usually in order to preserve the family fortune. Aristocrats would place restrictions on the use of their lands in an effort to keep them from being parceled up and sold off. There were insanely complicated systems of shifting interests that sometimes endured for centuries. So much real estate was so encumbered with conditions on inheritance that it was becoming impossible to transfer good title to vast swaths of the countryside. In response, the courts imposed a rule that no interest was valid unless it could “vest,” i.e., become a present interest in a living person, within twenty-one years after the death of some person alive when the interest was created. As a practical matter, this meant that you’re allowed to create interests that vest in your kids or their kids, but you can’t perpetually encumber your property such that your distant descendants won’t have clear title to the property.

Many states have modified or abandoned the RAP, as hereditary land dynasties are no longer fashionable, and simply administering the RAP was a pain in the neck. Law students are still taught it, but as often as not it’s a form of hazing, in which professors inflict obsolete doctrines on students because, dammit, they had to learn it, so you do too. The RAP comes up rarely in practice.

However, an immortal could, to put things mildly, completely screw this up. How? Because the RAP says that you can’t create an executory interest that vests more than twenty-one years after the death of someone currently alive. Because our immortal isn’t ever going to die, he can use himself as the “measuring life,” and so set up an impossibly complex set of shifting interests, all of which would be permitted by the RAP.

The way this would work would be for an immortal to buy a piece of property, and then sell it to someone else with a condition, which, if violated, would automatically shift ownership to some other person, possibly the immortal himself or herself. Because it is impossible to grant better title to land than that you yourself possess, the condition would not go away if the property were sold to a third party. Ergo, any conditions placed by an immortal would remain on the property forever.

This is clearly less than ideal, and though most superheroes would presumably not be unpleasant about this, even a noble superhero who wasn’t paying attention 13 could find that he’d inadvertently frozen a community in time by accidentally preventing any change in the land use. Even worse, one can easily imagine a far-sighted villain like Ra’s al Ghul using this power for evil, if the writers were big enough law geeks. World domination by conquest is admittedly impressive, as is world domination by buying it all over time. But it’s far, far more insidious to wind up controlling the whole world because you used to own it at some point and nobody ever thought that weird clause in the real estate contract would ever come back to haunt them.

So, in short, while there is no inherent problem with being immortal, property law pretty much assumes that everyone is going to die at some point, so the presence of an immortal being could pretty seriously screw things up. It’s almost strange that no writer seems to have done much with this yet.…

But wait a minute. Why does a character need to rely on property ownership to accumulate wealth? Why can’t he just use the magic of compound interest, frequently described as one of the most powerful inventions in human history? It turns out that this isn’t nearly as workable a solution in practice as it is on paper. There are two main reasons for this. The first is historical, and the second economic, but together they conspire to make living off your interest a little harder than it sounds.

Deposit a thousand dollars in a bank today, make 3 percent a year, and in a hundred years you’ll have $19,218.63. Not bad, eh? That’s the theory, anyway. But there are a couple of historical problems with trying to do this for really long periods of time. The first is that the oldest currently operating bank is Monte dei Paschi di Siena, founded in Siena, Italy, in 1472. Which is a long time ago, to be sure, but for someone like Apocalypse or Mr. Immortal, that’s not actually a very long time. There is one other bank that’s been around for that long—also Italian—but the modern banking system really only seems to have gotten started in the seventeenth century. So for characters that live a really long time, compound interest on deposit accounts hasn’t been available for most of their lifetime.

The other main historical problem is long-term stability. The financial industry is remarkably stable over a period of a few years, and the past few decades—2008 notwithstanding—have shown that they can be pretty stable over the intermediate term, but over the really long term? Much, much rarer. There were only a few periods further back in history that had something like our modern financial system. For example, ancient Roman banks seem to have been pretty sophisticated in historical terms, but they have all, for one reason or another, collapsed. Similarly, during the height of the Umayyad Caliphate, it was possible to write a check in Morocco and cash it in Islamabad, but the Caliphate was overthrown and its successors were not always in charge of the same territory. Since deposit insurance is a creature of the twentieth century, this means that if you are an immortal who lived through the end of a major civilization or even a decent financial panic, there was a good chance that you’d lose everything you’d kept in banks. So if you were depending on your deposits to keep you going, well, that’s maybe okay for a few decades, but not on the century timescale, let alone millennia.

To make matters even worse, for a huge chunk of history, the charging of interest was considered ethically problematic. The prohibition against usury still applies in the Muslim world, which is why Islamic banking looks so deeply strange to Western audiences. Western banks used a rather complicated legal arrangement to get around usury prohibitions in the Middle Ages, but the plain fact is that interest-bearing savings accounts the way we think of them really didn’t exist until the twentieth century. You could certainly invest your money, but now we’re talking about something different from simple compound interest.

But even if there was an unbroken continuity of depository institutions that has existed or is likely to exist for more than a few centuries, there’s another problem: inflation.

To make a reference outside our normal genre, consider Mr. Darcy of Jane Austen’s Pride and Prejudice, who is said to have had an income, i.e., money he didn’t have to work for, of £10,000 annually. Which even in current terms is not a terrible income, but most Brits with a job make more than that. But when the book was published in 1813, this represented a sum closer to £6.5 million in today’s currency, which is substantially cooler. But it also goes to illustrate just how badly individual units of currency have inflated over the years. One observer suggests that the effective inflation rate from 1913 to today is about 3.5 percent a year, something in the neighborhood of 1,929 percent over the whole time period. So someone trying to live purely off interest is going to have one hell of a time keeping up with that. They’d need to make 3.5 percent just to break even, so they’d need to make about 7 percent total just to have something to live on unless they had a massive principal investment to start with.

If you can find a relatively safe investment (i.e., a place you can put money that will give a return without you needing to work at it, that makes 7 percent a year), consistently, for more than a few years in a row, you are, without question, the most brilliant financier in the history of the world. The only way to make more than that is to either (1) own stuff yourself, be it land, a factory, a business, intellectual property, whatever, or (2) get a day job. Rich people choose the former; most people choose the latter, usually out of necessity. But the idea that you can just have a bunch of money, let it essentially sit, and expect to make a decent living for any serious period of time is problematic. Throughout history, the people in the world who have gotten rich have not done so on the basis of interest. Inflation, combined with long-term instability, makes that kind of thing truly implausible.

Don’t believe it? Think about the royal houses of Europe. If compound interest works the way it’s supposed to under the myth, they should be the richest people in the world. And make no mistake: the royal houses that have managed to survive are pretty well off. But they’re far from being the richest people in the world, and a lot of their current wealth comes from marrying people who got wealthy in other ways, e.g., oil barons, shipping magnates, etc. One might realistically ask if they’d be wealthy at all if they’d had to rely solely upon their own fortunes. Others are officially supported by national governments, which is an awesome gig if you can get it, but does tend to preclude the kind of hiding-in-the-shadows, living-a-life-without-obligations thing that Hob Gadling and most other immortal characters tend towards. 14

One might be tempted to say “ah, but what about the stock market?” Unfortunately, it presents many of the same problems: stock markets haven’t been around much longer than banks (the NYSE only goes back to 1817), they suffer the same long-term instability problems, and positive returns on one’s investment are impossible to guarantee. Inflation applies to securities exchanges too. Adjusted for inflation, the historic peak of the DJIA was just over 1,000, and in the early 1980s would have actually been at a level deep into the plunge of the 1930s! What’s more, stock markets and their participants tend to be even more heavily scrutinized than banks these days—complying with SEC regulations is a significant burden on publicly traded corporations and their directors—so in some ways they’re an even worse choice for an immortal trying to lay low. You can open a bank account without attracting any regulatory scrutiny, but securities trading is a lot harder to disguise for very long. No, buying stock on public exchanges is no substitute for private ownership, nor is it a plausible way of putting compound interest or something like it to work in the very long term.

Almost every American old enough to read has at least heard of Social Security, and with good reason: it’s been a key part of the United States’ social safety net for three quarters of a century. The program is so ubiquitous that Social Security Numbers (SSNs) have become one of the primary ways that United States citizens identify themselves in transactions with the government.

That alone poses a problem for an immortal character trying to lay low, as SSNs are associated with birthdates, and each time an SSN is used in an official transaction, there’s the chance that someone will notice a birthdate that’s way older than it should be. More than that, though, one’s SSN is intimately connected to one’s legal identity. It is a unique identifier and without one (or a Taxpayer Identification Number), the federal government isn’t necessarily going to be totally sure that you exist, bureaucratically speaking. It’s how taxes are tracked, and it’s very difficult to engage in even the most routine government transactions without one. If you’re curious, the statute that creates them is 42 U.S.C. § 405.

All of which conspires to make the SSN an essential part of constructing an alter ego, as discussed earlier in this chapter. Of course, forging them is a crime, and just running the numbers there’s a three percent chance that whatever number you make up is going to be currently in use by someone else (though it’s actually even greater than that given the rules for valid SSNs).

The other completely ubiquitous part of Social Security is taxes. 15 Social Security taxes are imposed by the Federal Insurance Contributions Act, better known as FICA, and codified at 26 U.S.C. §§ 3101–3128. At the moment, the Social Security tax rate is 6.2 percent of gross income, plus another 6.2 percent contributed by employers, so really 12.4 percent. 16 The self-employed must pay both halves out of their own pocket, hence self-employment taxes, but the difference is more one of perception than reality.

Either way, if you make money by working, i.e., you earn a wage or salary, the government wants its cut, and the IRS doesn’t much care who you are: even Superman can expect a visit from the taxman. 17 If you’re earning money, and it’s more than a couple of grand a year, the IRS will eventually find out. So unless a character is independently wealthy—which means he’ll be paying taxes in other ways, just not FICA—it’s going to be very, very hard to evade Social Security taxes for very long.

Then there’s the question of benefits. Right now, every American over the age of 67 (lower in some cases) can collect old-age benefits. Fair enough. But the actuarial tables for calculating benefits, taxes, budgets, etc., are predicated on most people dying within a decade of their seventy-fifth (or so) birthday. Wolverine could theoretically have been collecting Social Security—assuming he got his citizenship status worked out—almost since the program was inaugurated!

This is problematic for two reasons. One, when the government is cutting you a check every month, that’s one more month where someone might notice that you’re still around. A situation in Japan where hundreds of elderly people collecting old-age pensions were discovered to be missing, sometimes for decades, illustrates that while the machinery of bureaucracy does have a lot of inertia, people living beyond their nineties is still quite unusual and does raise red flags. 18 So a character who is either immortal or has a longer than normal lifespan will almost certainly get noticed sooner or later. Whether or not the character minds is dependent upon the facts of their particular story, but this could be problematic for many characters.

But second, Social Security was intended as a sort of last-resort measure to prevent the elderly from becoming destitute. It doesn’t really work that way anymore, as those people who have to rely solely upon Social Security pretty much are destitute, and plenty of people who don’t need the money at all still collect benefits for decades, but that’s still the theory. The discovery of a group of people who aren’t going to die at all, or who are going to collect benefits for fifty plus years is likely to encourage Congress to take a long, hard look at establishing some kind of limitation on the ability of people to collect benefits forever. Depending on just how bad the budgetary situation is at that time, this could be as little as a fix to exclude the truly immortal or as draconian as limiting benefits to three decades for everyone. But some kind of congressional action does seem pretty likely, and the existence of immortals among us might just be sufficiently distressing to the American population to give Congress the motivation it needs to actually do something about the government’s bleeding balance sheet.

The fact that even in the comics that contain the largest number of immortal beings there are perhaps a few hundred in the entire world is not likely to mitigate this fear either. The American media and populace are terrible at issues of scale. This, of course, is just one more reason immortals might want to keep their existence hidden, which means taking pains to conceal their longevity and identity. Simply declining to accept the benefits is probably insufficient to head off congressional action too, since not every immortal is likely to be so charitable.

Death is notoriously less than permanent in comic book stories. The basic rule of thumb is that unless we actually see a character die, and their body afterward, they aren’t dead, and even then writers can get creative. 19 But most of the time, the story is that the character wasn’t actually dead, but was just hiding, or in hibernation, or in a different dimension, or stuck in the pattern buffer, or whatever.

This doesn’t present any significant problems for the legal system, which already knows how to deal with people that are presumed to be dead but turn up later. A person who is legally absent, i.e., a person whose whereabouts are unknown for quite some time, will generally be presumed dead after a few years. Five to seven is pretty common, though interestingly for the citizens of Metropolis, New York, gives you only three. 20 It usually takes a court proceeding to get someone officially declared dead in the absence of a body, and in general, the courts will presume that a person is alive until there is clear evidence to the contrary or state statute operates to force presumption.

That last bit is actually of interest. Pretty much every state has a statute saying that if one is legally absent for a specified period of time, a court can declare one to be dead. But a few states also have a provision that exposure to a “specific peril of death” can permit a court to rule one dead before the specified period expires. 21 As superheroes are exposed to specific perils of death basically all the time, and would not generally be suspected to be dead in the absence of such a peril, it seems likely that a court, or at least a genre-blind one, would be willing to rule on a superhero’s death pretty quickly. Which makes things a bit complicated if they aren’t actually dead.

Southern Farm Bureau Life Ins. Co. v. Burney, 590 F. Supp. 1016 (E.D. Ark. 1984) is the big case here. In 1976, John Burney of Helena, Arkansas, ran into financial difficulties. On June 11, he was involved in a traffic accident on a bridge crossing the Mississippi River and managed to clamber over the railing and down the bridge into the river, where he swam to Mississippi instead of back home to Arkansas. He caught a bus and spent the next six years living in Florida as “John Bruce,” complete with a new wife and child, neither of whom had any inkling of his former life. He was discovered when he returned to Arkansas in 1982 to visit his father. Unfortunately for him, Burney’s wife and business partners had filed claims on various life insurance policies taken out on him and received benefits totaling $470,000. The wife, who may have been annoyed at finding out that her husband had completely abandoned his family and set up another one, contacted the insurer immediately. The insurer was annoyed and promptly sued Burney into next Tuesday.

Here’s where things get interesting for whack-a-mole-type supers: Burney’s wife and business partners, who had no knowledge of Burney’s whereabouts and had assumed that he had died in the accident, wound up a total of $470,000 richer. The judge let them keep that money, theorizing that “the policy of the law is to encourage settlement of litigation and to uphold and enforce contracts of settlement 22 if they are fairly arrived at, not in contravention of law or public policy.” 23 Burney wound up being found liable for $470,000 plus interest—whether or not he paid is another matter—but the people who received property as a result of his death were permitted to keep it.

The implication here—and there really isn’t much case law beyond this, because most people who are presumed to be dead are actually dead—is that if a person dies or is presumed to be dead, courts are not going to be very eager to disturb the settlement of property distributed via inheritance or devise unless there is a clear statutory reason to do so. Many states have statutes addressing this subject, but they’re all over the place.

•Cal. Prob. Code § 12408 specifies that a person who reappears after being presumed dead may recover any of his estate which has not been distributed, but property that has been distributed is only recoverable if it is “equitable under the circumstances,” and not at all if five years have passed.

•Va. Code Ann. § 64.1-113 provides that property which has not been distributed and property which is in the hands of someone who received it as a result of the presumption of death shall be returned to the person presumed dead, but bona fide purchasers of estate property are allowed to keep it.

•20 Pa.C.S. § 5703 requires that if a person is declared dead in whole or in part on the basis of his continued absence, no property can be distributed out of his estate without the distributee posting a bond for the value of the property. Clearly, a superhero who fears that he may erroneously be declared dead at some point should consider moving to Philadelphia.

•New York doesn’t seem to have a statute on this subject at all, meaning that any property distributed because a person is presumed to have died could be pretty difficult to get back.

So this really becomes a question of the state’s law where our supposedly deceased character’s will or estate would be probated. A returning or resurrected character could find that they get back most of the property they lost, or they could wind up with nothing. The longer they take to come back, the more likely the second outcome is.

But what if the person really was dead? Like really, honestly, no-foolin’, dead dead. Like Ben Grimm in Fantastic Four #508. 24 While in Latveria in the aftermath of Dr. Doom’s exile to hell, Doom started to possess Grimm, and the only way to prevent that was to kill Grimm. Which is what happened. Obviously, Grimm came back from that, but he didn’t “get better.” Richards didn’t clone him back to life. Grimm’s soul hadn’t been hiding out in a convenient contraption Dr. Doom had left lying around. No, Grimm was dead for reals, to the point that the rest of the Fantastic Four had to travel to heaven to try to persuade God himself to return Grimm to life.

The rest of the team was, of course, successful in pleading Grimm’s case. The question is whether it makes a difference to the legal system whether Grimm was simply presumed dead in error or actually dead and then returned to life. The answer is, probably not. This is almost certainly a place where a judge would go with pragmatic analysis. The alternative is to insist that Grimm had actually died and that his resurrection, while restoring him to life, did not restore him to any of the legal positions he had previously occupied. Essentially, the day of his resurrection would be his new “birthday,” and he’d have to reestablish his entire legal persona. This would be an enormous pain in the neck for everyone involved, and since there really doesn’t seem to be any good reason for going that direction, a judge faced with the question would almost certainly treat Grimm as if he hadn’t died in the first place. 25

Still, resurrection would likely have two important differences from simply being gone for a while. First, if one had never died in the first place, one’s legal duties during that time would continue. So if, for example, a character had child support obligations, or owed taxes on interest income, or had a contract duty to fulfill, the character’s absence might not exempt them from these obligations. Any exemption would have to come from a case-by-case analysis. But a character that was truly dead and subsequently resurrected would probably be entitled to a get-out-of-jail-free card for any obligations during the period in which he was dead.

Second, any time a person dies or is presumed dead, their estate is potentially subject to estate taxes. Estate tax is pretty complicated, and it’s the reason there’s an estate planning industry. The tax is somewhat controversial, but be that as it may, as of 2011, any estate worth more than five million dollars will pay something like 35 percent of the amount over five million dollars to the federal government. This is lower than it has been in years past (in 2001 it was 55 percent of everything over $675,000), but still significant for the very rich, which many superheroes and supervillains are.

So when an estate is probated, estate tax will have to be figured out and, if necessary, paid. The question then becomes whether a person who shows up after taxes have been paid on their estate can get those taxes back. If the person had simply been missing and not actually died, the answer may well be yes, though there is not currently case law to support that proposition. The government can be pretty stingy about that stuff. But there is certainly a good argument to be made that if the estate shouldn’t have been probated in the first place, taxes shouldn’t have been paid, so the person is entitled to a refund. But if the person had really, truly died…Like murder, where resurrection does not change the fact that the elements of the crime have been established, the fact that a person is resurrected does not change the fact that they died, which triggers estate tax obligations. Now the IRS could choose to be generous here, but the way the law is written, there is no strictly legal reason why a resurrected person whose estate had paid estate taxes would be entitled to a refund. So Ben Grimm would have a whole mess to deal with once he conquered death and returned to the land of the living.

1. Neil Gaiman et al., Men of Good Fortune, in SANDMAN (VOL. 2) 13 (DC Comics February 1990).

2. Psalms 90:10 (King James).

3. In the actual short story, the fact that Jekyll and Hyde are the same person is the twist ending, not known from the start, which really gives the problems of alter egos a pretty thorough going-over.

4. 18 U.S.C. §§ 1015, 1028, 1621.

5. These regulations are part of the Bank Secrecy Act in the US. Many other countries have similar laws.

6. 18 U.S.C. § 1956.

7. From The New Batman Adventures episode “Joker’s Millions,” based on David Vern et al., The Joker’s Millions, in DETECTIVE COMICS 180 (DC Comics February 1952).

8. Some stories make a distinction between “true” immortality and simply living a really long time. While this distinction may be important for various plots, the legal significance is minimal: anyone who lives more than about a hundred years without aging normally is going to run into these issues.

9. Marvel actually did a seven-issue series starting in January 1977.

10. The term “fee” derives from “fief,” a feudal landholding. It effectively means “interest in land,” but because that’s cumbersome, the “fee” terminology has survived.

11. Which is actually one of the big problems with mortgage securitization and the recent financial crisis. Property ownership can get so tangled that it’s becoming almost impossible to get good title to some houses. We’ll be sorting out that mess for years.

12. The technical estate would be a “fee simple subject to an executory limitation,” a type of “defeasible fee.”

13. And really, if one is acquiring property over a period of centuries, losing track of a few parcels doesn’t seem impossible.

14. Someone like Apocalypse doesn’t really “hide in the shadows,” but neither does he try to amass legitimate wealth.

15. Taxes are discussed in more detail in chapter 8.

16. At the time of this writing the employee contribution was reduced by 2 percent, but this reduction is expected to expire eventually.

17. See chapter 8 for the full story.

18. It also may help explain why the Japanese life expectancy is so high; maybe they simply aren’t recording the deaths. But that’s neither here nor there.

19. For example, Colossus sacrificed himself in UNCANNY X-MEN #390, his body was cremated, and his ashes were scattered. Nonetheless, he was returned to life three years later in ASTONISHING X-MEN #4.

20. NY CLS EPTL § 2-1.7.

21. See, e.g., 20 Pa. Cons. Stat. § 5701(c).

22. The insurer never actually believed that Burney was dead, but chose to settle the claim rather than fight. The judge reasoned that the insurer had figured the likelihood of Burney’s actually being alive into the settlement offer.

23. Id. at 1022.

24. Mark Waid et al., Authoritative Action Part 6, in FANTASTIC FOUR 508 (Marvel Comics February 2004).

25. This creates the interesting result that for criminal law purposes, a person could be held to have died and come back, while this would be ignored for estate law purposes. This may seem weird, but there is consistency here: in both cases, the law is being interpreted in the light most favorable to the “deceased.” While admittedly a bizarre result, it does seem to be the one most consistent with concepts of equity, which is something courts care about.