TWO MONTHS AFTER Morgan’s defeat in the battle of Dubuque, a congressional commission began examining the same problems he had detected in the railroad industry’s structure and behavior.

On the surface, the United States Pacific Railway Commission had a narrow charge—to determine the financial condition of the railroads built with government loans and their ability to repay that money. More precisely, the commission’s target was the Union Pacific. That road was not only the best known and most expensive of the land-grant railroads, but the one in the most parlous economic straits. In the course of its inquiry, however, the commission would lay bare everything that had gone wrong with the industry in the years since the meeting at Promontory.

The UP’s chief problems were excessive competition and plunder by insiders, which left the road physically decrepit, financially crippled, and under the control of a hostile Congress disinclined to give it a break. Had the railroad’s senior bonds been held by private individuals, the commission reported, they would have been “almost valueless.” The government had powers of foreclosure not available to individuals, the commission observed, but this step would merely give the taxpayers ownership of a wasting asset, “a result which can not be desired by any intelligent legislator.” As was observed in 1885 by the railroad’s government directors (put in place ostensibly to safeguard the federal investment in the road), the Union Pacific had been endowed with a “perfect and absolute monopoly” and “princely” profits, yet its finances were a shambles. The fact that the company had collected enough revenue to float $40 million in securities and pay out more than $26.6 million in dividends on its shares, yet still had not the means to redeem its government debt, pointed inescapably to the conclusion that “the past history of the company appears now like a travesty upon corporation management.”

The government directors and the commission together expressed the hope that conditions henceforth would be different under Charles Francis Adams Jr., who had been appointed president of the Union Pacific three years earlier, in 1884.

Seen through one lens, Adams seemed miscast to take over the railroad’s management. The UP was a huge enterprise in a complicated industry, but Adams had no operational experience as a business manager at any level (though he had served on the UP board since 1882.) The co-author of the muckraking classic Chapters of Erie (parts of which were written by his brother Henry), it was Adams who years earlier had predicted that the UP would end up as “two rusty streaks of iron on an old road-bed” if speculators continued to manipulate the road’s finances under the nose of Congress. (This description was commonly paraphrased as “two streaks of rust.”)

Critical challenges faced the Union Pacific in 1884. The speculative piracy of which Adams warned had come to pass, and worse was in store. Jay Gould was gone, which was a good thing; but he had left the road desperately ill-equipped to meet the looming maturity of the government loans that had financed construction through to the driving of the golden spike. The initial installment of debt, calculated at more than $50 million in principal and interest, was scheduled to come due on November 1, 1895. Whatever sentiment might have existed in Congress to forgive the loans or take repayment at a discount had evaporated with the Crédit Mobilier disclosures, for a failure by the government to demand payment of principal and interest in full would look like an endorsement of flagrant criminality. In 1878 Congress had attempted to anticipate the maturity deadline by passing the Thurman Act, which created a fund to sequester all payments the government made for official use of the railroad, along with a portion of the UP’s annual profits. The expectation was that the fund would grow enough by 1895 to cover the debt repayment, but it was a forlorn hope. By that point, it now seemed clear, the fund would hold only about $17.6 million.

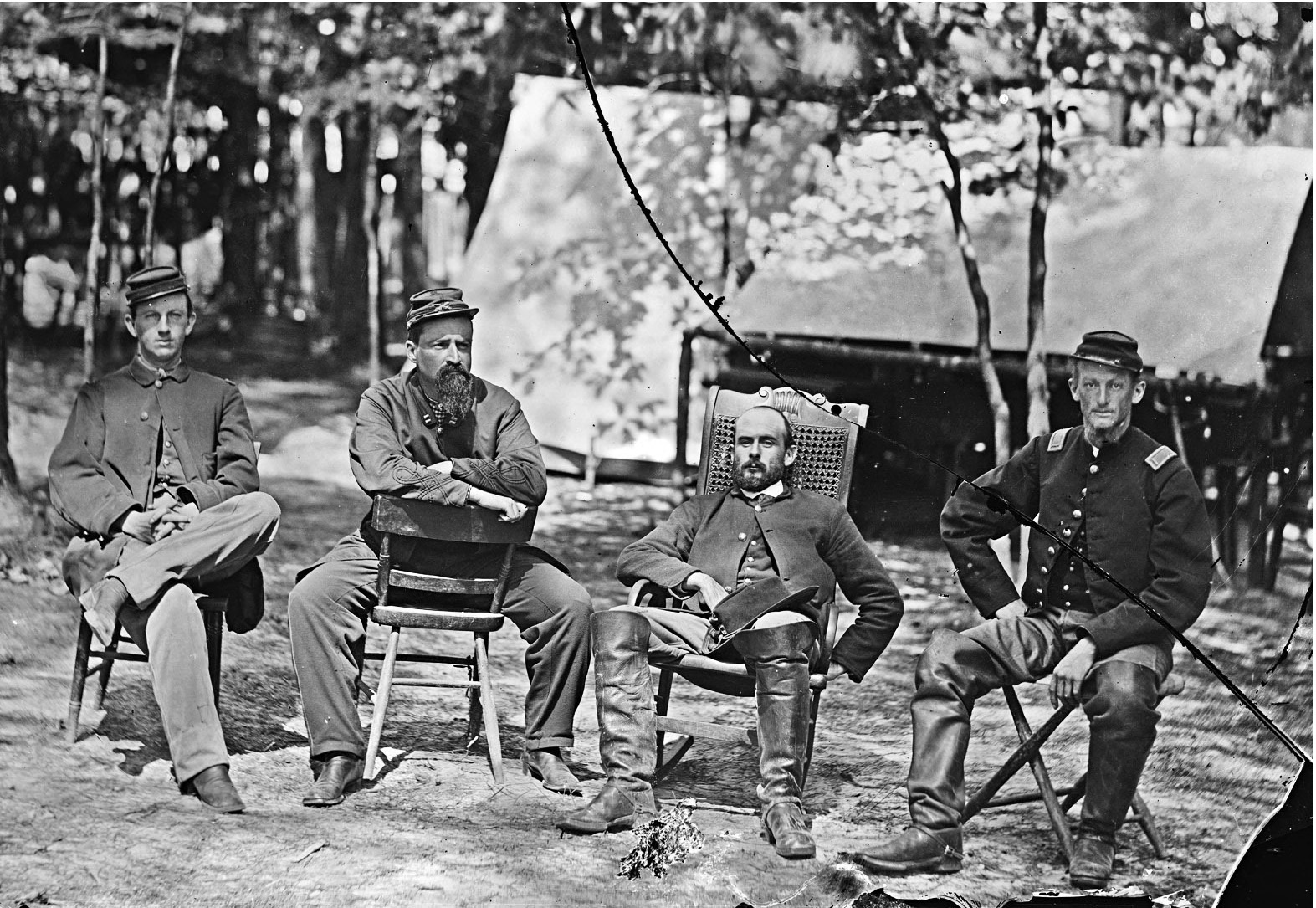

Grandson of one president and great-grandson of another, Charles Francis Adams, second from right in this photo taken with fellow officers during the Civil War, was the railroad industry’s first muckraker. But he failed miserably when he tried to apply what he had learned about railroad management as president of the Union Pacific in the 1880s.

Unless the government debt could be renegotiated and the resulting freed-up capital applied to refurbish its physical condition, the Union Pacific would be unable to meet the competitive challenges of the coming decades.

Seen through that lens, Adams could be considered almost the perfect man for the job. He was Gould’s polar opposite, unsullied by a record of speculation and looting. Not only was his personal character unassailable, but he had devoted much of his career to exposing the very piracy that had brought the railroad industry to bankruptcy and disrepute. He seemed to be the new broom the UP needed at that moment.

No one felt more strongly about his suitability than Adams himself. “With a good deal of natural confidence in myself, I looked upon assuming the management of a great railway system . . . as the legitimate outcome of what had, in my case, gone before,” he would recall years later. “I was simply playing my game to a finish. I was not yet fifty, and I did not want to break off and go into retirement in mid-career.”

He was not unaware of the pitfalls ahead. The Union Pacific “was in bad repute, heavily loaded with obligations, odious in the territory it served; . . . A day of general reckoning was at hand.” Shortly before taking office as president, Adams made a reconnaissance trip along the line with his fellow director Fred Ames, the son of Oliver Ames. They found conditions to be “in a shocking bad way,” he would recall. The line’s “service was demoralized, it had just backed down before its employees in face of a threatened strike, and it was on the verge of bankruptcy.”

Despite these challenges, Adams remained convinced to the end of his days that his scheme for renewal via renegotiating the government debt had been “well-conceived [and] entirely practicable.” The only real flaw, he acknowledged, was his own weakness of character. “Unfortunately for myself, I lacked the clean-cut firmness to adhere to it. Had I only done so, I should have achieved a great success, and been reputed among the ablest men of my time.” Adams had overestimated himself, but also underestimated the challenges he faced. He accepted the presidency of the Union Pacific filled with good intentions and ambition; but the six and a half years he spent in that post would be the most miserable of his life.

CALLING THE UP’S reputation with its prairie customers “odious” was a charitable way of looking at things. Railroads across the nation were anything but popular among their customers, but the Union Pacific was especially detested, for not only was it a monopoly along much of its length, but an especially pitiless monopoly. According to the government directors’ 1885 report, its rates were set “upon the principle that corporate extortion is a performance in which a railroad management may indefinitely indulge with impunity.” Compounding the evil of extortionate rates were the freight rebates and free passenger passes the UP bestowed upon politically well-connected shippers and their cronies, which invested the whole enterprise with the acrid stink of corruption. Rank dishonesty seemed to be baked into its bones.

As for the Gould legacy, the looming economic downturn would expose the folly of his management style just as a receding tide exposes derelict vessels to the open air. One appalling example uncovered by Adams involved the Denver & South Park Railroad, a branch line Gould purchased in 1882 from John Evans, the governor of Colorado Territory. “Everything in Colorado was in that very inflated condition which usually precedes a great collapse,” Adams testified to the Pacific Railway Commission. “The chief source of revenue was in carrying men and material into Colorado to dig holes in the ground called mines, and until it was discovered that there was nothing in those mines the business was immense. . . . Everyone was crazy. When [the craze] broke down and these mines and villages were deserted—and they stand there deserted to-day—of course the business left the road.” But the branch line stayed in the UP portfolio, draining resources at a rate of $60,000 a year.

Adams took office armed with the best wishes of the Union Pacific’s customers and government patrons. At the outset he seemed to fulfill their hopes. Adams and his managers “have done away with a great deal of obnoxious abuses” and done much “to smooth down the differences of difficulties between the people of this state and their road,” an Omaha newspaper editor told Congress in 1886. The Pacific Railway Commission praised the Adams administration for having “devoted itself honestly and intelligently to the herculean task of rescuing the Union Pacific Railway from the insolvency which seriously threatened it at the inception of its work.”

Yet Adams’s efforts were doomed to founder on hidden shoals. Raised in a family devoted to government service and as experienced in the ways of Washington as any clan in the country, he was deeply shocked at the moral climate of the capital in the 1880s. He wrote that his initial visit to Capitol Hill, where he hoped to fend off legislation consigning the Union Pacific to receivership, became “my first experience in the most hopeless and repulsive work in which I ever was engaged—transacting business with the United States government, and trying to accomplish something through Congressional action.”

On Capitol Hill he had run smack into “the most covertly and dangerously corrupt man I ever had opportunity and occasion carefully to observe in public life.” Adams had the patrician grace not to identify his adversary by name in retailing this history in his autobiography, but he was undoubtedly referring to Senator George F. Edmunds of Vermont. Adams wrote that his experience with Edmunds contradicted the Vermonter’s reputation for “ability and . . . rugged honesty” in every respect: “I can only say that I found him an ill-mannered bully.” Assessing Edmunds’s integrity, Adams judged that the senator’s antipathy toward the UP derived entirely from his pique over the railroad’s refusal to put him on its payroll.

Edmunds blocked Adams’s every effort to reach a financial agreement with the government. In the end, Adams slinked away in defeat: “I was—there is no use denying it, or attempting to explain it away—wholly demoralized,” he wrote of his final eighteen months as UP president. “I hated my position and my duties, and yearned to be free. . . . Railroads, and the railroad connection, occupied over twenty years of my life; and when at last, in December 1890, I got rid of them, it was with a consciousness of failure, but a deep breath of relief.” He would never engage with the railroad industry again.

But Edmunds’s corruption had been only one obstacle Adams faced. There was also the behavior of his fellow railroad bosses. The building of new competitive lines had fallen off after the Panic of 1873, but resumed with the return of prosperity. Every surviving railroad faced new rivals; staggered by the crushing fixed costs bequeathed them by the watered financing of the post–Civil War era, they had no choice but to attract freight contracts by any means at hand—most often by cutting rates to the level of fixed costs or, in the most desperate situations, even lower, just to have some revenue flowing in.

Through the 1880s the railroad bosses tried to fight against rate cutting with every form of collusion they could contrive, chiefly through pools. These were agreements in which competing railroads apportioned traffic among themselves or shared the income from secretly fixed rates. Instead of undercutting one another, in other words, the railroads strived to keep rates high, jointly pocketing the excess profits.

The pools all failed, for two main reasons. First, customers’ perception that the roads were colluding against them gave rise to official investigations and legislative action to outlaw the arrangements. Second, the railroad bosses simply were unable to work in concert, even for mutual gain. As the Commercial and Financial Chronicle observed, every railroad leader “has been wholly selfish, bristling all over with hostile purpose towards every other. No right of territory, no settlement of rates, no adjustment of business, stood for a moment as a hindrance to the insatiable craving of getting business.”

As president of the Union Pacific, Adams had joined in a pool to end a rate war among eastern railroads; the pool’s collapse in 1884 taught him the inevitability of failure. The final meeting of the presidents “struck me as a somewhat funereal gathering,” he recounted. “Those composing it were manifestly at their wits’ ends. They evidently felt, one and all, that something had got to be done; yet no one knew what to do. Everything had been tried and everything had failed. . . . They reminded me of men in a boat in the swift water above the rapids of Niagara. They were looking one at another in blank dismay, and asking ‘What next?’ and no one could tell what next.”

Initiatives by several states to outlaw pools were overruled in 1886 by the US Supreme Court on grounds that they had no authority under the Constitution to regulate interstate commerce. That dumped the matter into the lap of Congress, which responded in 1887 with the Interstate Commerce Act, the first major effort at industrial regulation in American history. At first the railroads fought the act as ferociously as they had been fighting each other. Eventually, they settled for keeping the Interstate Commerce Commission, which was to administer the act, securely under their thumbs.

By the time of the act’s passage, the railroad industry was in a state of anarchy, desperate for someone to impose order—a Bismarck. The hour produced the man, in the person of Pierpont Morgan. The challenge confronting Morgan was daunting indeed, but he was fully aware of its magnitude. “For forty years,” observed John Moody, “American railroad promoters, reckless optimists, gigantic thieves, huge confidence men—magnified a hundred times by the size of their transactions—had juggled and manipulated and exploited this great business for their own profit and the general loss of every one else concerned. Morgan had been watching.”

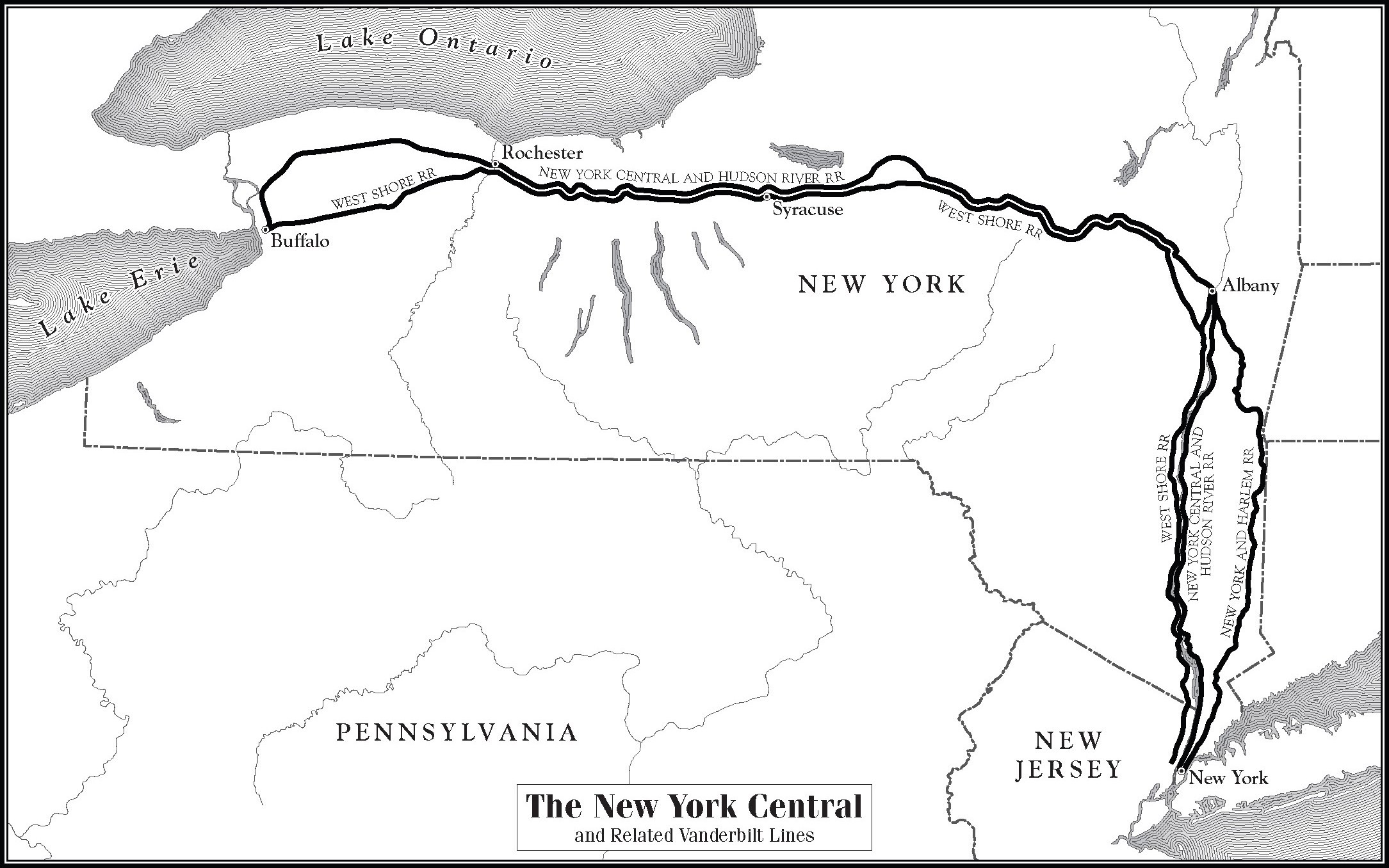

PIERPONT MORGAN HAD exploited the knowledge he gained during his 1869 grand tour to dabble in railroad securities throughout the 1870s. Then, near the end of the decade, came the deal that brought him into railroading in a major way. It involved the vast holdings in the New York Central of William H. “Billy” Vanderbilt, who had inherited the stake in 1877 upon the death of his father, the Commodore. Billy decided in 1879 to shed a large portion of the unwieldy investment, in part because he had wearied of the constant warfare it provoked with his family’s old adversary, Jay Gould. Moreover, the investment was threatened by a movement in the New York legislature to ban single-family ownership of major railroads. Vanderbilt hired Morgan to unload the shares through an international syndicate, converting the New York Central from a private family holding into a public company. The sheer scale of the transaction was breathtaking: The sale of Vanderbilt’s 250,000 shares was “the largest ever made by a single owner of railroad stock,” reported the New York Tribune, which added that the result would affect “the entire railroad interests of this country.” That was because the deal effectively united the interests of Vanderbilt and Gould, whose “Wabash syndicate” became the largest holder of the New York Central by acquiring 60,000 shares.

What was perhaps most significant was that in consummating the deal, Pierpont took a seat on the New York Central board as well as the authority to fill two other seats, which he gave to Gould associates Cyrus Field and Solon Humphreys. Although Vanderbilt remained the president of the New York Central—and would continue in that role until his death in 1885—Pierpont Morgan had gained a perch at the heart of the industry from which to start exercising power over “the entire railroad interests” of the United States.

Over the next decade Morgan would continue to build his influence. Starting in 1880 he managed financings for the Northern Pacific, whose mercurial new controlling shareholder, the German-born Henry Villard, was trying to complete the construction plans halted by the collapse of Jay Cooke & Co. Morgan took a seat on the Northern Pacific board in 1883, the same year Harriman had joined the IC board, and subsequently helped to oust Villard in order to clear the way for a more complete reorganization. In 1885 he took on the rescue of the Philadelphia & Reading, a declining road serving the coal mines of western Pennsylvania, again taking a seat on the board along with the chairmanship of the voting trust that controlled the road. By the end of the 1880s, the news that Pierpont Morgan had interested himself in the financing or management of an otherwise hobbled railroad was often enough to restore that line’s access to investors in the United States and across the Atlantic.

Pierpont’s hands-on work, however, also made him intimately familiar with the behavior that was destroying the industry from the inside, including the building of superfluous lines for no reason but to harry competitors into buying them out. The prime example in his experience involved the New York, West Shore & Buffalo. This was a road partially financed by Gould, George Pullman, and Villard, built along the west bank of the Hudson as a nuisance to the Vanderbilts’ New York Central line across the river (an example of the conflicts with Gould that so wearied Billy Vanderbilt). When the West Shore went bankrupt it was promptly acquired by the Pennsylvania Railroad, which under the leadership of the imperious Thomas A. Scott and his successor George B. Roberts continued to harry the New York Central with rate cutting. By 1885 the Central was forced to set rates so low it was operating its passenger service at a loss and its shares were being crushed. “I look on the West Shore road just as I would on a man whose hand I had found in my money drawer—a common, miserable thief,” Vanderbilt fumed to the New York Tribune. In truth, the Pennsylvania was merely returning to Vanderbilt the same treatment it had received at his hands, for he earlier had built the South Pennsylvania Railroad, an unnecessary line from Harrisburg to Pittsburgh, to compete directly with the Pennsylvania’s own route to the coal fields. The two camps could have settled their conflicts in a draw, but Vanderbilt’s refusal to take the West Shore off the Pennsylvania’s hands at anything above pennies on the dollar prolonged the conflict.

Morgan assumed the task of bringing the hostilities to an end. Planning his voyage home to New York from his annual excursion to London in May 1885, he contrived to book the same steamer as Vanderbilt, then used their week in close quarters to hector Vanderbilt into reaching a deal. After they landed in New York, the final settlement was cemented on Morgan’s yacht, Corsair, as it steamed up and down the Hudson. It was not a relaxing cruise. The July weather was sweltering even into the night. George Roberts, the Pennsylvania’s president, was determined to punish the New York Central for its earlier incursion into his territory. (“Mr. Roberts was not an easy man to deal with,” recalled Satterlee, who found him to be, like Vanderbilt, “a product of the times [who] lived in a world of railroad strife and was accustomed to giving and receiving hard blows.”) Morgan, who by then filled out his six-foot frame with two hundred pounds of flesh, watched over the negotiations as a lowering presence, fingering a big black cigar, inserting an occasional sharp interjection when the unruly discussion needed to be put back on course.

Eventually Roberts capitulated not merely to Morgan’s authority as one of the Pennsylvania’s bankers but to the inescapable logic of striking a compromise. Vanderbilt agreed to acquire the West Shore at a reasonable price, and the Pennsylvania to buy the South Pennsylvania from Vanderbilt. Because the Pennsylvania state constitution forbade the Pennsylvania Railroad to acquire a competing line, the nominal purchaser of the South Pennsylvania was J. Pierpont Morgan. The complex transaction gave rise to one of the legendary verbal exchanges of Pierpont’s career, starting with his instruction to Vanderbilt’s legal adviser, one Ashbel Green, to reduce the provisions into legal form. Green presently reported back that he thought the plan could not be executed legally.

“That is not what I asked you,” Morgan barked. “I asked you to tell me how it could be done legally. Come back tomorrow and tell me.”

Green presently proposed an intricate sequence of securities trades in which a Morgan syndicate bought the West Shore and leased it in perpetuity to the New York Central, while Morgan himself bought a 60 percent stake in the South Pennsylvania and traded it to the Pennsylvania for the bonds of another railroad. The multifaceted deal was widely regarded as a signal achievement for Morgan, who used it as a model for ending several other competitive wars vitiating the railroad industry. His formula was reduced to the term “community of interests”—a recognition that competing magnates would secure mutual benefits by rationalizing rates, ending wasteful construction, and exploiting what were, after all, natural monopolies by crafting mutual alliances. Morgan communicated to the road presidents that until they learned to work together, none of them would be able to turn a reliable profit. Consequently, none could hope to raise capital in the European markets, which would invest only in a rationalized industry. Failure to come to terms meant stagnation and eventually extinction.

Morgan was playing with fire, for the public’s growing disenchantment with the concentration of economic power represented by the development of railroad combines would soon produce the Sherman Antitrust Act of 1890, the first US law to declare monopolies illegal (even if it was only patchily enforced in its first decade).

Pierpont himself embodied the very concept of a community of interests. In time he became not only a director of the New York Central, but of the New York, Providence & Boston, which carried passengers from Grand Central Station to South Station in Boston; he was in constant demand for service on railroad boards along the Eastern Seaboard, not seldom because he also was those lines’ banker; and his partnership Drexel, Morgan & Co. was financier to the Pennsylvania.

Pierpont’s goal was to supplant the old pooling arrangements, which were so brittle in their terms and toothless in their enforcement, with “gentlemen’s agreements.” On the surface these seemed even looser than the old pools, for they exchanged the superficial formality of the pools for what Herbert Satterlee described as undertakings resting “solely on the spoken word between executives. . . . The only punishment for disregarding the object of these associations was to place the offending management in a very unfavorable light before other railroad men.” But it would be a mistake to assume that the informality alone worked where formality had failed. The element that was expected to make the gentlemen’s agreements function was a central authority, and that authority was Morgan.

Not everyone was willing to concede him that power. Railroad presidents as a species were accustomed to getting their own way and distinctly unaccustomed to taking orders from others. Jay Gould, for his part, remained under the impression that he was still the most powerful figure in the industry and therefore the man to dictate the terms of peace. In early December he presented Morgan with a roster of proposals to squelch competition, including a five-year ban on construction of parallel lines, all to be binding upon railroad presidents on pain of their being blacklisted for refusal. Gould’s record, however, had won him Morgan’s enduring disdain. According to Satterlee, Morgan was convinced that Gould and his cronies had “made it easy for the self-appointed champions of the people’s rights to build up a public opinion unfriendly to the railroads. . . . [They] had wrecked railroads and disrupted lines that might have grown into systems. . . . Their methods had often made legislatures and courts of law bywords of contempt.” (By contrast, Satterlee judged indulgently, his father-in-law “had the best interests of the public and the railroad employees at heart.”)

Numerous railroad presidents had stated publicly that they would not attend any meeting at which Gould would be present or “join in any arrangement Mr. Gould may propose,” the New York Tribune reported. But Morgan knew he could not avoid including Gould in the railroad confederation he envisioned, since it would be better to have Gould’s roads inside the arrangement than taking shots at it from the outside, so he tendered the buccaneer an invitation to participate. The proposal Morgan eventually put forth would share some features with Gould’s, but it would be made clear that the ideas were Morgan’s, not Gould’s, and that Morgan was driving the train, with Gould merely one passenger among many.

MORGAN SUMMONED A dozen railroad presidents and their bankers to his sumptuous art-filled mansion at 219 Madison Avenue on December 20, 1888, for the opening stage of his campaign to end the railroad civil wars. The underlying purpose of the meeting was for “the representatives of capital . . . to show the railroad men the whip,” one of Morgan’s confidants later explained. “They intended to convey a very definite impression that further misbehavior would be punished by cutting off the supplies” of capital.

Charles Francis Adams arrived at 9 A.M. to find the railroad men seated grumpily around Morgan’s dining room table, joined by representatives of the banking firms Drexel, Morgan & Co.; Kidder, Peabody; and Brown Brothers. Adams marked Gould as looking “dreadfully sick and worn,” as he recorded in his daily journal. (Gould was, in fact, suffering from the tuberculosis that would kill him three years later.)

From the head of the table, Morgan brusquely informed the railroad men that he had called the meeting “to cause the members of this association to no longer take the law into their own hands when they suspect they have been wronged. . . . This is not elsewhere customary in civilized communities, and no good reason exists why such a practice should continue among railroads.”

The railroad presidents bristled at Morgan’s tone. “I object to this very strong language, which indicates that we, the railroad people, are a set of anarchists,” groused Roberts of the Pennsylvania. He was right to be irked, for none of the overbuilding that provoked the rate cutting could have taken place had not the bankers in the room connived to finance the excess construction.

The railroad leaders were not yet ready to yield a dictatorial role to Morgan, though they had nothing novel to offer. Ransom Reed Cable, the truculent head of the expansion-minded Rock Island line, offered a scheme to fix rates that Adams mentally judged to be “the old story once more—proposing to bind the railroads together with a rope of sand.” Cable’s plan, which carried no provision for enforcement, was greeted with “expressions of contempt,” Adams noted. After the meeting adjourned for the day, Adams trudged up Madison Avenue with his old rival Jay Gould. “I told him that it seemed to me to be the merest child’s play for us to be going round and round in this old circle,” he recalled. “We might as well go home and leave events to take their course,” unless the joint arrangement they mapped out would be subject to some “compulsory force which would establish obedience.” Casually, Adams suggested using the very entity that the railroads had worked so hard to render toothless—the Interstate Commerce Commission. To his surprise Gould jumped at the suggestion and even offered to present it personally to the gathering the next day.

The more Adams turned the idea around in his mind, the sounder it seemed. “The railroad situation today is one of simple anarchy,” he reflected. “We need law and order. We resemble nothing so much as a body of Highland clans—each a law unto itself—each jealous of its petty independence, each suspicious of any outside power which could compel obedience. Such a state of affairs . . . cannot—and will not—last. The thing is to back it up. In other words, a railroad Bismarck is needed,” he concluded, using the increasingly common term for a dictatorial authority. Would Morgan be able to exercise the authority needed to bring the rest of the presidents to the same conclusion? “It remains to be seen,” Adams mused.

The next day’s meeting did not start auspiciously. Gould presented the idea of bringing in the ICC, “but in so weak and vague a way that it made no impression,” Adams recalled. Adams took over, and according to his own recollection, finally made the idea take—though not before he delivered some home truths to his colleagues. The industry’s troubles, he told them, “lie in the covetousness, want of good faith, and low moral tone of railroad managers, in the complete absence of any high standard of commercial honor.” The question was whether the railroad bosses were prepared to publicly state that they would violate the precepts of the Interstate Commerce Act “rather than submit to arbitration” by the government regulators. The meeting ended with an agreement to meet again on January 8, and for Morgan in the meantime to interest the ICC commissioners in the plan.

The January 8 session convened in an atmosphere of mutual resentment, for another round of rate cutting had occurred in the interim. Yet improbably—and surely to the amazement of all concerned—the meeting resulted in what appeared to be an enforceable agreement, signed by twenty-two railroads. The ICC agreed to assume the role of arbiter of interline disagreements by convening a board to take testimony when necessary. One ICC member, Aldace Walker, the commission’s only experienced railroad man, resigned to become chairman of what was dubbed the Interstate Commerce Railway Association, an example of the revolving door between government and private service that is generally frowned upon today but was interpreted then as a sign of confidence in the arrangement.

Morgan won universal praise for his role and the agreement itself was hailed as the harbinger of a new age of harmonious cooperation in a major industry. “When the party that furnishes all new money needed, and the party that owns the old money invested, and the party managing the corporation meet, the result means revolution,” gushed the Commercial and Financial Chronicle. The Chronicle was certain that the ICC’s arbitration board would act effectively: “Kickers”—that is, railroad presidents who violated the terms—“will be brought into line or suppressed. . . . With, then, the stockholders of American roads and with the world’s capital as its reserve backing this new institution, there need be no fear of a lack of strength to enforce its decisions.”

Yet Morgan’s compact was doomed to failure as inevitably as the pooling arrangements it supplanted. Within two months of its signing—“barely enough time for the railroad presidents to get back from Morgan’s,” historian Gabriel Kolko reflected—a new rate war erupted in the West. Adams’s own Union Pacific was at its center, in a contest for coastal traffic with Henry Villard’s Northern Pacific. By June, Kolko noted, “the chaotic status quo was restored.”

For more than a year, Morgan struggled to reimpose order. In December 1890 he summoned another clutch of railroad presidents to his town house, emerging with another compact among fifteen railroads and another proclamation that peace was at hand. “Think of it,” Morgan told the press—“all the competitive traffic of the roads west of Chicago and St. Louis placed in the control of about thirty men.” To later generations, power concentrated to this degree would seem scandalous; to Morgan, it made the agreement “as strong as could be desired.” But his optimistic words could scarcely conceal the enmity that had afflicted the presidents’ dealings with one another. It soon transpired that at one point during the negotiations A. B. Stickney, formerly the president and now chairman of the Chicago, St. Louis & Kansas City road, had blurted, “I have the utmost respect for you gentlemen individually, but as railroad presidents I wouldn’t trust you with my watch out of my sight.” Thomas Oakes, the head of the Northern Pacific, snapped in response: “Have you reached that opinion recently, Mr. Stickney, or did you entertain it when you were a president?”

That attempt to conjure up a “community of interest” would fail like all those that came before it and followed afterwards. The chaos among the railroads only grew wilder in the first years of the 1890s, and left the industry utterly unprepared to face what would be the worst crisis in its existence: the Panic of 1893.

UNLIKE ITS PRECURSOR in 1873, the Panic of 1893 was not primarily triggered by the railroads, though they would be among the most deeply injured enterprises. The immediate cause, instead, was the failure of the most admired of the industrial trusts that had sprung up over the previous decade, the National Cordage Association. The “cordage trust,” which controlled some 90 percent of the rope market in the United States, had been riding high in investors’ esteem as recently as January 1893, when it issued a 100 percent stock dividend, shaving its share price to $70 from $140 to enhance its appeal to Wall Street speculators. (The stock dividend did not change the capitalization of the trust, for it merely doubled the number of shares, which traded at half the previous price—a shareholder who previously owned one share valued at $140 now owned two valued at $70 each.) The collapse of the trust was another example of the ills of monopolization that had prompted Congress to enact the Sherman Antitrust Act in 1890.

The real problem, as was true of many other overgrown trusts of the era, was that the financial condition of the cordage trust was opaque to its investors and even its bankers. Of its directors, only the president and treasurer knew all the facts—specifically, that the trust was hobbled by overproduction, a lack of credit, and the evaporation of its working capital. On May 2, the trust had assured the public that it had $4 million in ready funds. In fact, the cash box held but $100,000.

Businesses dependent on public confidence are the most vulnerable to sudden collapse when the first crack appears in the wall of trust. The end came for Cordage on May 5, when it abruptly announced that it had placed itself in the hands of bankruptcy receivers. “Cordage has collapsed like a bursted meteor,” reported the Commercial and Financial Chronicle the next day, “and the other industrials have all of them shared to a considerable extent in the decline.” Belatedly, the Chronicle rued the lack of transparency of the nation’s biggest industrial concerns. “We know little about ‘Cordage,’” the journal observed. “We know but little also about most of the other industrials; indeed it is because so little is generally known of these properties and prices are consequently so largely speculative that confidence in them has been so grievously disturbed.”

To be sure, the Cordage collapse did not occur in a vacuum. Disquieting currents had been swirling within the American economy for years. One was a persistent conflict over the monetary system. Laborers, farmers, miners, and other producers of commodities, all of whom would benefit from inflation, favored an expansion of the money supply through the free coinage of silver to supplement gold as the specie backing the US currency. Manufacturers and bankers were on the other side. They demanded adherence to the gold standard, which governed international trade and promoted stable currency values. These were important to bondholders and other investors expecting periodic returns over long periods of time; devaluation of the dollar through an expansion of the money supply could only sap their investments of their worth.

This conflict played out in the presidential election of 1892, particularly in the contrast between Grover Cleveland, seeking his nonconsecutive second term as a gold-standard Democrat, and James Weaver, the candidate of the new Populist Party, which advocated silver coinage. At the time, the silver lobby appeared to be in the ascendance, due to passage of the Sherman Silver Purchase Act of 1890, which mandated limited government purchases of silver. Cleveland balanced his ticket with Adlai Stevenson, a silver-coinage advocate, as his vice presidential running mate, and won a plurality of the popular vote and a decisive electoral-vote majority when the Populists and Republicans split the pro-silver vote. (In a political turnabout, the Populists later would merge with the Democratic Party, which would nominate silver advocate William Jennings Bryan as its presidential candidate in 1896, 1900, and 1908.)

The consequence of silver coinage for the United States proved Gresham’s law, the economic principle that “bad money drives good money out of circulation”—that is, people will hoard good money (in this instance, gold) and use debased currency to settle accounts wherever possible. Because only gold, not silver, was accepted by foreign creditors in settlement of international trade, gold began to flow out of the United States at ever-increasing volumes. Silver became the preferred settlement currency only for domestic transactions. A loss of confidence abroad in the stability of the US economy and a slowdown in economic activity were the harvest.

Benjamin Harrison, the Republican who occupied the White House between Cleveland’s two terms, tried to put the best face on a faltering economy. “There never has been a time in our history when work was so abundant or when wages were as high, whether measured by the currency in which they are paid or by their power to supply the necessaries and comforts of life,” Harrison said in his final annual message to Congress on December 6, 1892. “If any are discontented with their state here, if any believe that wages or prices, the returns for honest toil, are inadequate, they should not fail to remember that there is no other country in the world where the conditions that seem to them hard would not be accepted as highly prosperous.”

Harrison put in a plug for the tariffs he had imposed: “I believe that the protective system . . . has been a mighty instrument for the development of our national wealth and a most powerful agency in protecting the homes of our workingmen from the invasion of want.”

But matters worsened after Cleveland began his second term. In the panic year of 1893, more than 640 banks failed—5 percent of all the banks in the United States—and fifteen thousand businesses went bankrupt. Of the nation’s nearly 178,000 miles of railroad track, roughly one-fifth were owned by railroads in receivership.

JUST AS THE panic struck that summer, Morgan allowed himself to be dragged into another railroad rescue. This time the object was that perennial damsel in distress, the Erie, still wearing the scarlet letter pinned on its finances by Drew, Vanderbilt, Gould, and Fisk. The inevitable bankruptcy occurred in mid-1893. Morgan was tasked with the reorganization. The work would be notable not merely as a step in the evolution of Morganization—but as the occasion for a second clash of wills between Morgan and Edward Harriman.

Morgan’s plan laid most of the burden of the restructuring on holders of the Erie’s second-mortgage bonds, while protecting its shareholders from any sacrifice. This struck many observers as unjust on its face, since shareholders normally were last in line among a bankrupt enterprise’s investors. Among the holders of second-mortgage bonds was Harriman, who commuted on the Erie to New York City from his estate at Arden, New York. He obligingly stepped up as a spokesman for the objecting bondholders. In a series of open letters, the publication of which Harriman orchestrated, the creditors attacked Morgan’s plan as “unjust” and, more to the point, financially imprudent, since it would do nothing to reduce the Erie’s fixed charges—the real cause of the bankruptcy.

Morgan bulled through his reorganization plan at the Erie shareholders’ meeting that March. But he did not reckon with Harriman, who formed his own committee and filed a lawsuit to block the plan. (This episode gave rise to one of the more persistent, if fanciful, anecdotes about Harriman. It was said that he had visited Morgan’s offices to present his objections to the reorganization plan in person. When asked by Morgan whom he represented, he snapped, “Myself!” The journalist who appears to be the first to retail this story, Edwin Lefèvre, acknowledged in his article that “it may not be true,” but that as “characteristic of Harriman” it was plausible enough to be published.) When the dispute came to court, Harriman was dealt a defeat by the financial establishment: A New York judge ruled that, since holders of $31 million of the $38 million in second-mortgage bonds had assented to the plan and Harriman owned a bare $40,000, “the court should not interfere.”

Harriman’s last-ditch effort accomplished little beyond intensifying Morgan’s animosity. “Harriman always wanted to get terms which were a little better than other people’s,” remarked Satterlee (though Morgan himself was hardly above extracting the best terms possible in his own transactions). What truly irked Morgan was that Harriman “followed his usual tactics of retaining counsel and fighting in court,” Satterlee continued. “But he was unsuccessful in the end.”

That might have been true tactically, but subsequent events showed that Harriman had been absolutely correct in his assessment of the plan’s risks. Within a year, the Erie defaulted on the interest payments due on the reorganization securities, just as Harriman had forecast. Morgan was forced to put through a second reorganization plan that finally reduced the Erie’s fixed-charge burden so it could profit from the economic recovery of the final few years of the nineteenth century.

Morgan may have communicated his distaste for Harriman to the managers of the Erie. Soon after this second skirmish, Harriman sought a routine courtesy from the Erie typically offered by railroads to executives of other lines, such as the Illinois Central. One day Harriman missed the Erie local he had planned to take from New York to the trotting races at Goshen, about twenty miles away. He phoned the Erie to ask if its Chicago Express would make an unscheduled stop in Goshen to let him off. This time he was flatly refused. Still, since he knew that the westbound Chicago Express could be flagged to pick up any passenger for boarding along the way, he wired a friend in Goshen to buy a ticket to Chicago. When the train stopped in Goshen to pick up the phantom passenger, Harriman hopped off.

But the Erie contretemps, like the earlier confrontation over the Dubuque & Sioux City, was only a prelude to the struggles to come.

Harriman was as yet little known to the public as a railroad leader and little respected in Morgan’s elite circle. That was about to change. What would finally bring Harriman to prominence was the railroad that Morgan and his fellows still dismissed as “two streaks of rust”—the Union Pacific. Jay Gould, in one final act of destructiveness, had provided Harriman with the opening.