Just because a shop wants to sell you a $300 pair of shoes, it doesn’t mean you have the money to buy it. Bummer, right? But what would happen if a friend offered to lend you money to cover the cost if you promised to pay it back? Would you say yes?

Okay. Now what if it wasn’t a friend offering you the money but a credit card company? And as you paid the money back, you also had to pay something called “interest”?

Still sound like a good deal? Before you say yes this time, here are a few things you need to know about credit.

Not so fast. Although it seems everybody’s whipping out plastic every time you turn around—at the mall, in restaurants, online, and even in the air—credit has a way of turning into a big balance. At the time of writing this book, American citizens had $2.45 trillion in consumer debt!

One of the main reasons credit-card debt spirals out of control comes down to one word: interest. That’s a kind of fee credit-card companies—issuers is actually the right word—charge you for borrowing money from them. If they make you pay 15 percent interest and you spend $100 on some fancy goldfish, scooter, or new necklace, you’re out an extra $15 if you don’t pay up by the end of the year.

Absolutely, credit-card companies should charge us some kind of fee if we don’t pay back the money when we say we will. After all, by loaning out the cash, they’re taking a risk. It’s only fair.

a) Paper b) Plastic c) Cardboard d) Cloth

Answer: c) Cardboard. In 1950, Diners Club offered its first card to be used at 27 restaurants in New York City. Within one year, nearly 20,000 Americans had them in their wallets. Move ahead to the end of 2009. There were 576.4 million (plastic) credit cards in America, and people had used them over 20 billion times!

But the problem with credit-card fees is that the issuers don’t simply charge interest at the end of each year. They charge it each month, and the interest compounds.

(Deep breath now. This whole compounding thing is easier to understand than it seems.)

For example, let’s take that $100. A month’s worth of interest is $1.25 ($1.25 x 12 months = $15). Because the interest compounds, the next month you’re paying interest on $101.25. After a while the extra cents really add up.

The credit-card issuers must love him. He’s their perfect client. He pays some of his loan (or principal) on time, but pays plenty of interest, too. How much? If he borrows $5,000 and makes the 2 percent minimum payments per month, it will take him 32 years to pay it off! Not only that, he’ll also pay $7,789.56 in interest.

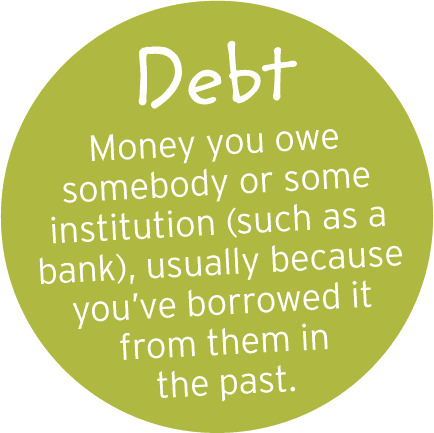

Suddenly, that $5,000 has cost your family $12,789.56. In debt terms, dear old Dad is a “revolver,” someone whose debt cycle just keeps going around and around in circles—and keeps making the credit-card company money! To avoid this nutty schedule, he should pay off bigger chunks each month. But even if he does increase the size of his payments, your dad is now living with something called debt. D-E-B-T: It’s amazing how those four little letters can cause such a ruckus for you, me…even entire countries.

Debt can be a good thing. Nearly everyone at one point in their life goes into some kind of debt when they borrow money to get something quite expensive that they can’t pay for all at once—such as a home or a car. And over time, most people pay these loans back. But debt can also be a big drag if we’re not careful. When that happens, a family can be sucked down into a vortex of debt and have a really hard time getting out of it. Some people even have to declare bankruptcy.

But this definitely doesn’t have to happen to you. Imagine you decide to go to university or college but don’t have all the money you need to pay for tuition, books, housing, and food. You can apply for a student loan. (Just ask your school counselor where to go to get the papers to apply or how to apply online. Or hit your favorite bank. It’s an easy and common process.) This is known as a good debt because it’s going to help you get a better job and earn a better salary someday. In the long run, you’ll be better off with the education than without it.

Just one word of warning: Pay your student loan back on time, or you could end up paying a lot more than you bargained for. If you don’t get a job after school right away, go to the bank. In some cases, they can give you a little more breathing room before you have to pay.

How can an institution that gives you a loan know you’re not going to take the money and run? It’s impossible to tell for sure, but they can examine your credit rating, or score, and determine the likelihood you’ll pay the money back.

A credit rating is made up of complicated statistical information gathered from all the loans you’ve taken out before. If you paid them back on time, your credit score number goes up. If you didn’t pay back a loan or were late with payments, your number goes down.

Scores are measured between 600 and 900. Any number below 650 is considered “poor” and you’ll have a hard time getting another loan. If you hit 750 and up, you’ve got a “great” rating.

Sometimes when people get a big loan, they don’t borrow all the money they need to buy an item. Instead, they present a large chunk of money toward the price called a down payment. For example, if you’re buying a $17,000 car, you might offer a $5,000 down payment and borrow the remaining $12,000 with a loan. Obviously, the bigger the down payment, the better.

Clearly, mishandling credit cards and loans can be a little scary. So let’s say you decide you’re smarter than that. There’ll be nothing but full, on-time payments for you! You’ll be the perfect customer, right? Actually…in the topsy-turvy credit world, good customers like you can actually be considered bad.

Huh?

Think of it this way. Unlike the beloved “revolvers”—people who owe lots of money, pay lots of interest, but don’t default (stop paying entirely)—people who pay off their entire balance every month are considered a disaster! They’re borrowing money but not paying any interest. No interest equals no money for the credit-card people. And because other credit-card companies can check in and see this awesome track record—also known as a credit rating—the next time these responsible people try to get another card they might be told, “No way!”

Researchers discovered that people were willing to pay twice as much for basketball tickets when they used a credit card instead of paying cash. Credit-card spending just doesn’t feel like real money. There are a lot of other emotional reasons that make us overspend, too.

Whether we’re trying to fit in, feel good, or just give ourselves a little extravagant treat, credit cards allow us to take chances we would never normally consider if we could only pay for things with cash.

Even though credit cards can turn a little debt into a big problem, very few of us actually have a poor credit rating. Most fall into the “great” range. The truth is that even though it’s easy to rack up tons of debt, most people know their limits and don’t spend more than they earn.

But sometimes, even the most level-headed folks end up getting into debt, especially if everybody seems to be splurging. Throughout history, it’s been during the very, VERY good times (called bubbles) that people have gone the most money crazy—and usually been left with empty wallets. In other words, they take a bath. Here’s what I mean:

Gives new meaning to “flower power.”

From 1620 to 1637 people in Holland went wacky for tulips. Professional tulip traders were soon selling them for thousands of gold florins (coins). People swept up by the craze traded their homes, horses, and carriages for the bulbs. Farmers, maids, and chimney sweeps even quit their jobs to buy bulbs in hopes that they could sell them at a higher price later. But in 1637 the bubble burst, and in the end those prized tulips made people dirt poor.

Here, let me help pay—but it’s going to cost you…

Britain was in debt after jumping into the War of the Spanish Succession. Luckily the South Sea Company agreed to finance the debt on two conditions: The Brits had to pay interest, and South Sea would be the only company allowed to trade with the Spanish Americas. For ordinary folks, investing money in the powerful company sounded like a sure bet. Only one problem: By 1720, South Sea had lost its ships...as well as all of the cash that people invested in the company!

“From a land where the streets seem lined with gold…”

On August 16, 1896, three eagle-eyed men found lumps of gold in a Yukon creek in northern Canada. Word got out the next spring, and within one short year, tens of thousands of men, women, and kids had arrived to strike gold, too. Sourdoughs, as the prospectors were called, swatted at swarms of bugs in the summer and braved horrific cold and avalanches in the winter. And for what? While a few of the first people got rich, by 1898 nearly all the gold seekers had left—without gold.

What a shock to the system.

After the horror of the First World War, the twenties were downright exciting. With new technology everywhere—such as radios and improved cars—and a general feeling of happiness, what better time to invest money in the stock market? But the optimism couldn’t last forever. When share prices started falling, some people panicked and cashed in their investments. Then more people. And more. On October 29, 1929, shares dropped like a stone, making people’s investments worthless. Hello, Great Depression.

If I tack an “e” on the name, everyone will buy it!

In the mid- to late-1990s, the world was going gaga over tech companies. The web as we know it today was brand-spanking new and loads of people wanted to invest their money in companies that they hoped would be the next Google or eBay. The problem was that people, not knowing which one would be the Next Big Thing, were throwing their money at any e-company with a half-baked idea. By 2000 reality sunk in, and most of the tech companies scaled way back or tanked—the e-boom went bust. Again, people who invested in these failed companies lost it all.

I’m richer than I think!

Housing bubbles pop up again and again, but the bubble of 2008 was downright wild. For a few years, financial folks played fast and loose with loans—lending anyone with a pulse lots of money to buy a house—as long as they were willing to pay it off with interest over 30, 40, or even 50 years (far longer than the usual 15- to 20-year periods of times past). With so many new people waving cash around, housing prices went sky high…and still people kept buying homes. Eventually, too many people couldn’t pay their mortgages (loans), and the whole housing industry went kaput.

One word: over-optimism.

Let’s say we have a glass that’s filled up halfway with juice. If you’re an optimistic person, you’ll probably say it’s half full. The more pessimistic bunch will say the glass is half empty. But what happens if someone is overly optimistic? He’ll tell you the glass isn’t just half full—he’s convinced that at any moment someone’s going to come along and fill it up to the top!

For some crazy reason people have a really hard time learning from old mistakes. We think: “The Great Depression? Hey, that was back in 1929! Our situation in Future Land is completely different.” But guess what? We might be wearing different clothes, listening to different music, and eating different snacks at school, but when it comes to racking up debt, we’re sadly just as good at it as we were back then. Maybe even better.

No matter what year we live in, these economic bubbles start because overly optimistic people assume great things are on the horizon. They think what they buy today will be worth more tomorrow.

A better burger. Make your own hamburgers at home using meat from your local butcher and they’ll cost about the same amount as the ones you eat at big hamburger chains starting with the letters “M” and “C.” Farmers near you will thank you.

Righteous rugs. Looking for a new carpet for your room? Choose one with a GoodWeave label. To earn the label, carpet exporters and importers pledge not to employ kids under age 14 and to pay fair wages to adults. Since the program launched in 1995, experts estimate that the number of kids working on South Asia’s carpet looms has dropped from 1 million to 250,000.

Bogus bottled water. Thirsty? Bypass bottled water and fill up a reusable bottle instead. Not only will you keep bottles out of the landfill, but you’ll save money, too. Drinking the recommended daily amount of water using bottled water will run you about $1,400 a year. Good old tap water? Try 50 cents.

Cheap clothes not cheap. That $9 pair of shoes looks like a great deal...but probably not for the people who made them. In order to make a product that inexpensive, someone probably had to cut corners.

Gas guzzling’s got to go. The British spend more for their petrol—that’s gasoline to you, cowboy—than people in North America. Why? Taxes. Although grown-ups grumble about paying the taxman, where would we be without him? Taxes pay for your roads, your community pool, your library, and the trees planted outside your home. Taxed gas costs more money, but there’s an upside, too. Because Europeans spend more for gas, car companies build cars that use less of it.

It’s only fair. Invited to your best friend’s birthday and have no idea what to give her? Visit one of the hundreds of fair trade stores around the world (or hop online with a parent to peruse the virtual shelves). These shops buy from small businesses and collectives that treat their employees right. Buy a gift for your friend and you’ll give the gift of fairly paid work to someone on the other side of the planet or even close to home.

Smaller house rules. Want your family’s dollar to make a big difference? Live in a smaller home. Think less energy and fewer building materials like wood, bricks, and fiberglass. Less space also means fewer pieces of furniture to buy—and toys to pick up!

Wondering how healthy, green, or socially responsible that hand lotion or toaster pastry really is? Trying to decide where to spend your cash? Compare over 65,000 products, the best and worst brands, at www.goodguide.com.

Now we know that spending too much can do a number on our families, our friends, and even our country’s economy. So how do we stop plunking down our hard-earned cash or abusing credit to buy stuff we don’t actually need?

TIP #1 Think small. Studies show that when people are asked to focus on the cash in their wallet instead of in their bank account, they spend less. That full piggy bank back home? Repeat after me: “It doesn’t exist.”

TIP #2 Use your imagination. Here’s something I do whenever I’m tempted to buy some new gadget or gizmo: I imagine it in my home, unused and collecting dust. Hey, that’s probably what’s going to happen to it eventually anyway…

TIP #3 “But everybody’s got one!” Even if it seems like everyone at school is snatching up whatever the latest fad happens to be this week, don’t believe the hype. Chances are there are a lot more kids who haven’t jumped on the bandwagon. Do the math. You might be surprised.

Not long ago I got a call from my credit-card company that went something like this:

“Hi Kira. We just wanted to check something out. Have you been making any purchases in Saudi Arabia lately?”

“Uh, no.”

“That’s what we thought. So we’ve frozen your card and will be sending you a new one with a new number.”

It turned out that someone had found a way to steal my credit-card number and then tried to use it to buy plane tickets in the Middle East and pay a utility bill in Europe. My card really got around! Luckily, credit-card companies hire smart people who spend their whole day trying to thwart the bad guys—fraudsters—who try to get access to our personal information.

So what are the best ways to foil the credit thieves? (Don’t have a credit card yet? You should still pay attention—one day these tips could save you a lot of money and grief!) Never, and I mean NEVER, give your credit-card number out to telemarketers who call your house. Shield the card when you go out so no one can take a photo of the number with their phone. Finally, only shop online with a credit card if you trust the site. (In other words, check with your parents beforehand. Sounds uncool? That’s nothing compared to how uncool it is to get massively ripped off…)

So now that you know credit can get you out of trouble and into trouble, maybe it’s time to put all that aside for a while and try—wait for it—saving your money instead! I know. Crazy concept. We’re all so used to seeing something we want, buying it, and paying for it later. But as you’ve just read, with credit, some of us pay for our purchases in more ways than one.