Lisa J. Servon

The consumer financial services system in the US is broken. This system consists of mainstream banks and credit unions, “alternative” check cashers and payday lenders, and informal tools such as rotating savings and credit associations (ROSCAs) and loan sharks. In the last four decades, but particularly since the financial crash, consumer financial services has transformed into a system that no longer serves the needs of the lower and middle classes.

Policy makers and researchers are concerned about the growing numbers of Americans who have no bank account or who use “alternative” financial services (AFS) such as check cashers and payday lenders. In 2014, the FDIC reported that 17 million Americans are “unbanked” (they have no bank account) and another 43 million are “underbanked” (they have bank accounts but continue to rely on alternative financial services) (Burhouse and Osaki 2012). The numbers are more stark in low-income areas, and among racial and ethnic minorities (Cover et al. 2011). As many as 28.2 percent of low-income families (making less than $15,000) are unbanked and 21.6 percent are underbanked (Barr and Blank 2009). Black, Hispanic, and households of foreign-born non-citizens are also disproportionately underbanked. Only 48.7 percent of Hispanic households are fully banked; this figure falls to 45.8 percent in households of foreign-born non-citizens, and to 41.6 percent in Black households (Burhouse and Osaki 2012).

Policy makers and researchers have set up false dichotomies between the banked and the unbanked, and the financially “included” and “excluded.” These frames are misleading. Labeling people as “banked,” “underbanked,” or “unbanked” presumes that relying exclusively on banks is the desired norm and that anything else is inferior. Similarly, the term “financial exclusion” assumes that people who do not have a bank account have no access to financial services. As this chapter demonstrates, these people are very much a part of the financial services system, sometimes by choice, sometimes because mainstream institutions fail to meet their needs, and sometimes because they are actively excluded.

These debates also ignore the interconnections between the different types of financial services providers and how they rely on each other to make their profits. Existing policy efforts tend to try to move the unbanked and underbanked to the banked category without a thorough understanding of the context in which they are making financial decisions and the viable options that are available to them (see, for example, the BankOn programs that began in San Francisco in 2006 and currently exist in 76 cities).

The purpose of this chapter is to tell the story of how the consumer financial services system became so dysfunctional and to show that key myths we hold about how low- and moderate-income people make financial decisions are incorrect. I discuss the three trends that have led to the current situation: (1) changes in bank practices and in policy relating to banks; (2) Americans’ increasing financial instability; and (3) over-reliance on credit. Given this context, I will then show why it makes sense that so many people are turning to alternative financial services in greater numbers. Using data from participant observation and over 100 interviews, I will debunk four prevalent myths about the alternative financial services industry: (1) everyone needs a bank account; (2) people use alternative financial services because they lack financial literacy; (3) more regulation of alternative financial services will solve the problem; and (4) people who use alternative financial services don’t save.

This chapter relies on a deep literature and policy review that informed the sections on the trends underlying the dysfunctional financial services landscape. I also spent hundreds of hours embedded as a teller at RiteCheck, a check casher in the South Bronx, and as a teller and loan collector at Check Center in downtown Oakland, California. After working at each of these businesses, I interviewed 50 customers at each store. For one month, I volunteered as a staffer on a hotline for people having difficulty repaying their payday loans. I conducted a range of interviews with experts on banking and alternative financial services, policy makers at the Consumer Finance Protection Bureau and the FDIC, relevant researchers, the head of a subprime credit bureau, and consumer advocates. I attended local and national trade association meetings of check cashers and payday lenders, and conferences run by the Center for Financial Services Innovation.

My use of ethnographic and other qualitative methods allowed me to get as close to the issues I wanted to understand as I possibly could. By inhabiting a neighborhood-based financial institution that serves a largely banked/unbanked population, I was able to better understand the reasoning behind consumers’ financial decisions. Spending a large amount of time in the neighborhood also enabled me to build trust and to get to know other ways in which people met their financial needs.

Policy makers tend to decry the large numbers of unbanked and underbanked people, moving directly from the FDIC statistics to interventions that move people into bank accounts. This process misses the necessary step of analyzing a larger set of possible reasons that have led to the current situation. I found three trends that have taken place during the same period in which the alternative financial services component of the consumer financial services industry has grown: (1) changes in banking policy and practices; (2) greater reliance on credit; and (3) increasing financial insecurity.

Debates about the dangers of overly large banks have been going on since at least 1912, when then Democratic Party presidential candidate Woodrow Wilson wrote:

The great monopoly of this country is the money monopoly. So long as that exists our old variety and freedom and individual energy of development are out of the question. A great industrial nation is controlled by its system of credit. Our system of credit is concentrated. The growth of the nation, therefore, and all our activities are in the hands of a few men, who, even if their action be honest and intended for the public interest, are necessarily concentrated upon the great undertakings in which their own money is involved and who necessarily, by very reason of their own limitations, chill and check and destroy genuine economic freedom. (Wilson 1912)

The term “too big to fail” was actually coined in 1984 and was used to justify the government bailout of Continental Illinois, the nation’s seventh largest bank, shortly after the branching bans began to be lifted and 24 years before the most recent financial crisis that made it a commonplace catchphrase (Haltom 2013). Congressman Stewart McKinney used the term in a Congressional hearing discussing the FDIC’s decision to bail out Continental Illinois, the largest bank failure in US history. Between 1993 and 1997, 2,829 banks were obtained through merger or acquisition. Power became increasingly concentrated in a small number of banks.

Over and over, for more than a century, we’ve heard that banks are too big, and that they don’t have our best interests at the center of their decision-making. The situation has only worsened since then. When Washington Mutual went under during the financial crisis in 2008, the bank was seven times larger than Continental Illinois had been. The four biggest banks collectively hold about half of total US bank assets, a total of $6.8 trillion (Schaefer 2014). The largest banks are enormous. Ellen Seidman, a Senior Fellow at the Urban Institute who has worked for decades in financial regulation told me, “I don’t think you’ll find a [bank] regulator . . . who thinks they are governable or regulable.”

The unchecked growth of banks is hardly the only factor that created the situation we’re in now. To understand what has happened, we need to go back to the beginning of the last century.

Early concern about harmful bank practices led policy makers to pass the Unfair or Deceptive Acts and Practices legislation in 1914 as a component of the Federal Trade Commission Act. These laws were reinforced by the passage of the Truth in Lending and Truth in Savings Acts in 1968 and 1991, respectively. These laws require that creditors disclose the costs and terms of credit and require that advertisements not be misleading or inaccurate, or misrepresent an institution’s deposit contract (FDIC 2004). A second A, for Abusive, was added to the acronym in July 2010 when the Dodd–Frank Act was passed. Although it responded to real problems and was well-intentioned, UDAAP regulations differ from state to state, and are up to judges’ interpretation of the terms “abusive” and “deceptive.” The law has rarely been invoked since the passage of Dodd–Frank.

The Great Crash of 1929 intensified the focus on consumers. Policy makers responded to the crash by trying to ensure that what happened in 1929 couldn’t happen again. The crash devastated so many families that it drove the next 40 years of bank legislation.

Between 1933 and the late 1960s, almost no new federal banking policy was made, and bankers and regulators acted cautiously within the newly growing economic landscape. Between 1941 and 1964, the number of bank failures nationwide was negligible – for context, only one Federal Reserve member bank in the Seventh District (serving Chicago and the Upper Midwest) failed during those years (Federal Reserve Bank of Chicago n.d.). In the mid-1960s the political climate again changed. The policy that’s relevant to our story was made in the 1960s, when the intense activism we associate with that era caused Americans to reexamine a whole range of businesses, practices, and norms. A young Ralph Nader made a big splash with his 1965 book Unsafe at Any Speed, an exposé about the auto industry. The civil rights movement and the women’s movement had gathered steam, and both movements converged on financial issues. In 1961, the US Commission on Civil Rights found that African-American borrowers were often required to make higher downpayments on homes and other major credit-based purchases, and pay off loans faster than whites (Westgate 2011: 382). Still, discrimination persisted. In urban neighborhoods, activists organized “bank-ins,” to protest credit discrimination and bring attention to the problem, both to decision-makers at the bank and community members on the whole.

A spate of new federal banking legislation – the first that had been passed in over 30 years – was passed. The Truth in Lending Act (TILA), passed in 1968, the 1970 Fair Credit Reporting Act, and the Equal Credit Opportunity Act (ECOA) of 1974 all aimed to level the playing field for people seeking all kinds of loans. TILA required that banks disclose key information – annual percentage rate (APR), complete loan terms, cost – before extending credit. The Fair Credit Reporting Act regulated collection of credit information and access to credit reports in order to ensure fairness, accuracy, and privacy of the personal information kept by credit reporting agencies. And ECOA focused on discrimination, making it illegal to deny credit on the basis of “race, color, religion, national origin, sex or marital status, or age . . . or because all or part of the applicant’s income derives from any public assistance program” (15 USC § 1691). Together, these three pieces of legislation demonstrated a new commitment to consumer protection by mandating greater transparency on the part of banks. Some states also took the initiative to mitigate discriminatory lending practices. In 1964, California passed legislation requiring state-chartered savings and loans to submit certain lending data to the Commissioner.

Since before the Great Depression, federal and state banking regulation aimed to limit branch banking. The passage of the McFadden Act of 1927 prohibited interstate branch banking in the United States. Some states passed laws further regulating intrastate savings and loan (S&L) branch banking. For a century, all branch banking was prohibited in Illinois, beginning with the passage of the State Constitution of 1870, which specifically prohibited branch banking, until a 1983 state law repealed branching restrictions.

Similarly, until 1982, Pennsylvania banks were allowed to branch only in the county where their head offices were located and in contiguous counties (Jayaratne and Strahan 1999). A number of other states also severely restricted intrastate branching before 1985, but relaxed or eliminated these regulations by 1991, including Kansas, Montana, Nebraska, Oklahoma, Texas, and Wyoming. Only Colorado, Minnesota, and North Dakota made no changes to the restrictiveness of their state branching regulations during those years. Other states restricted branching based on town population: New York and Oregon prohibited branching when the town population was less than 50,000 people. New Hampshire prohibited branching in towns with populations of less than 2,500 people, but only if there was another bank within the town. Hawaii restricted branching within Honolulu (Calem 1994).

States enacted restrictive bank legislation in order to limit the power of banks, due to concern that if banks became too big they would gain too much political and economic power. Many customers feared that deposits made in small towns would be siphoned to make loans in the state’s larger financial centers, leaving small businesses and local communities without adequate available capital. Branching restrictions were also intended to protect banks from excessive competition from bigger banks (Rice and Davis 2007).

In 1977, the passage of the Community Reinvestment Act (CRA) facilitated the growth of bank branching. The CRA sought redress to the severe shortage of available credit in lower-income neighborhoods and, in states without severe restrictions on branching, S&Ls were incentivized to locate in underserved areas. The effects of this legislation happened in tandem with the easing of regulations restricting branching on the state level. Fifteen states passed legislation allowing branching between 1970 and 1985, as did another dozen by 1989. Although the idea behind the CRA was to make financial services more accessible in low-income communities and communities of color, the branches that resulted did not have the same knowledge of the local communities as independent banks did. Community connected banks and relationship banking was no longer the norm in most states by 1990.

The Riegle–Neal Interstate Banking and Branching Efficiency Act of 1994 permitted interstate bank branching, and represented a turning point in banking regulation. By allowing interstate branching, it allowed larger banks to easily grow bigger, often by buying single branch and small banks in large metropolitan areas, particularly those that spanned state lines, such as the Washington DC metropolitan area.

Following deregulation in the 1980s, the number of S&Ls fell sharply as larger banks bought out smaller banks, and a number of smaller thrifts closed, unable to keep pace with growing competition. Between 1986 and 1995, the Federal Savings and Loan Insurance Corporation (FSLIC) and the Resolution Trust Corporation (RTC) closed 1,043 thrift institutions, approximately half of the total number in the US.

In December 2010, The New York Times Dealbook reported that there were 734 thrift institutions operational in the US (Protess 2010). This dramatic drop in the number of thrifts over the last few decades means that individual consumers have many fewer choices in where they can bank, which creates less incentive for banks to compete to best service customers. By 1999, virtually all of the protections that had been created following the Great Crash had been eliminated. Congress passed the Financial Services Modernization Act, known as Gramm–Leach–Bliley, that year, allowing banks to engage in both commercial and investment activities. Once again, depositors were left unprotected from the consequences of banks’ high-risk investment strategies.

We all know what happened next. In September 2008, Lehman Brothers collapsed, sending panic through the stock market and threatening to bring down the world’s financial system, and creating a “credit crunch” as taxpayer-financed bailouts held up the limping finance industry (The Economist 2013). The crisis was brought on by irresponsible mortgage lending to subprime borrowers – primarily people with poor credit history who struggled to repay their loans. The risky mortgages were bundled in supposedly low-risk securities by financial engineers at big banks, while in fact these weak mortgages retained their risk. Banks used finance instruments in unsafe ways, betting against themselves and creating a vulnerable financial environment. But regulators like the Fed also were to blame; by failing to exercise sufficient oversight, they allowed the Lehman Brothers collapse to happen, leading to the downward spiral that caused the largest economic downturn since the Great Depression.

Commercial banks still see service to consumers as a poor stepchild, secondary to their core business. With the expansion allowed by deregulation, they have branched out (literally) to the depository and loan services previously provided by community-based thrifts, but because the profit returns from these services are much smaller, retail banking is not treated as a priority by the nation’s largest banks.

There is a connection between the lack of quality, affordable financial products and the “too big to fail” mentality. There are currently 6,900 banking institutions in the US and ten of them hold 80 percent of total deposits (Hryndza 2014). As banks have grown larger and their numbers have dwindled, they have become less and less responsive to the needs of consumers. Big banks have focused on profit at the expense of their customers. Perhaps not surprisingly, the alternative financial services industry has grown significantly during the same period that banks have consolidated and become more expensive to use.

Over the past several decades, Americans have relied increasingly on credit. Low interest rates and easy access to credit made credit cards a simple option for people experiencing financial stress. In 1983, only 43 percent of US households had a MasterCard, Visa, or some other general purpose credit card. By 1995, that number had risen to 66 percent. As of 2010, 68 percent of families had one or more credit cards. That means roughly 152 million consumers (two-thirds of adults above age 18) were holding 520 million credit cards in 2010 (Canner and Elliehausen 2013).

Credit card companies also sought new markets with aggressive marketing, eventually targeting riskier customer segments. In 2005, credit card companies sent nearly six million pre-screened solicitations to consumers, or 20 solicitations for every man, woman, and child in the US. As companies’ tactics changed, so did the mix of cardholders. In 1995, cardholders were more likely to be single, to rent instead of own their homes, and to have less seniority at work than they were in 1989. These new borrowers were riskier than previous cardholders. They had a substantially higher debt-to-income ratio, which meant that even small drops in income could lead to financial distress. New borrowers were also more likely to work in unskilled jobs with wages dependent on the business cycle.

One means of evaluating the composition of credit card borrowers is to look at those who were targeted with credit card solicitations. According to an analysis by the Federal Reserve, about 63 percent of individuals received credit card solicitations in 2007. This rate dropped to 27 percent by 2009. Individuals with credit scores in the lowest quartile (who pose a higher risk of default) received about 11 percent of credit card mailings in 2007. By 2009, that number had dropped to only 2 percent (Canner and Elliehausen 2013).

Credit card companies raised credit limits in the period leading to the Great Recession also. The median available credit per card increased about $900, or about one-third, and the median outstanding balance rose from $1,100 in 1989 to about $1,700 in 1995. In 2010, most families that held credit card debt owed relatively stable amounts. The median owed by families carrying debt was $2,600. However, the average amount owed by US households in general is significantly higher at $7,100 (Canner and Elliehausen 2013). When considering only those families who are in debt, average household debt is $15,224 (Federal Reserve Board 2014).

The cost of using credit cards has also risen, and policy has abetted rising costs. Consumer debt has grown along with the deregulation of the credit card industry beginning with the 1978 Supreme Court ruling of Marquette v. First Omaha Savings Corp., which virtually eliminated interest rates on credit cards. In 1996, the Smiley v. Citibank decision did the same for credit card fees, allowing them to be determined by the lender’s home state. Prior to this decision, credit card late fees averaged $16; in 2007 the average late fee was $34 (Garcia 2007).

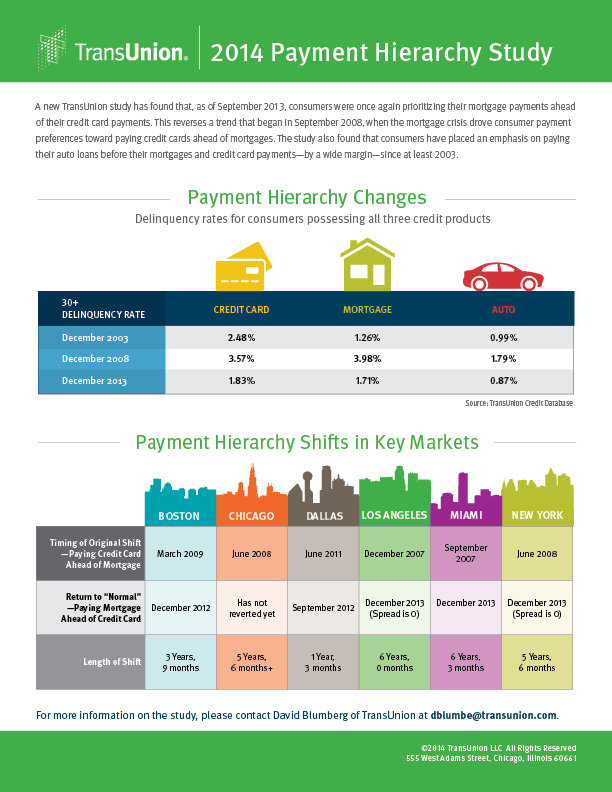

One of the most significant impacts of the Great Recession was a change in the way consumers managed payments. As more consumers faced financial constraints and made difficult choices, many chose to prioritize their credit card payments over their mortgages; they needed the liquidity to make ends meet (Vornovytskyy et al. 2011; TransUnion 2014). The credit card industry abetted this trend; low interest rates and easy access to credit fueled an increase in credit card debt that peaked in January 2009, six months into the financial crisis (Garcia 2007; Canner and Elliehausen 2013).

In the aftermath of the financial crisis, the use of credit cards has declined as banks tightened lending standards; less credit was available to consumers as they lost their jobs (and income). Between 2000 and 2011, households became less likely to hold credit card debt. In 2000, 51 percent of households held credit card debt. In 2011, the percentage had decreased to 38 percent (Vornovytskyy et al. 2011). Twenty-nine percent of Americans don’t own any credit cards, the highest proportion since 2001, and those holding credit cards have 3.7 cards, down from 4 in April 2001.

These changes have occurred because of a combination of changes in policy and practice by lenders, not solely because of changes in consumers’ behavior. In some cases, frugal borrowers paid off their outstanding balances. In other cases, as consumers struggled to make payments, credit card companies experienced a rise in delinquencies and charge-offs. Card issuers responded to these conditions by changing the terms offered on credit cards, the amount of credit offered to borrowers and the strategies used to market their products (Garcia 2007; Canner and Elliehausen 2013; Athreya et al. 2014).

These changing dynamics of the credit card industry are one reason that an increasing number of consumers turn to payday loans. These loans are perhaps the most hotly debated topic in the area of consumer financial services. It used to be that you could walk into a bank and get a $500 loan with just a signature. If you were white, at least. Greg Fairchild, professor of management at UVA, told me his father called those loans “white man’s loans.” Now, no matter what your race or gender, those days are gone. Payday lending is a $90 billion industry; there are more payday lending stores than there are McDonald’s and Starbucks combined (Graves and Peterson 2008).

The contraction of credit has also caused people to juggle their available credit and to use payday loans in ways that seem counterintuitive without complete knowledge of individuals’ situations. Some of the people getting payday loans also had credit cards on which there was still available credit. It would seem that they should use the credit cards before getting a payday loan, right? Not necessarily. Tim Ranney relays a conversation he had with the head of risk for a major credit card company who asked him, “Why are people taking out loans instead of using their cards?” Ranney told me, “This guy was implying that these people weren’t smart enough to make the ‘right’ decision. I laughed in his face. ‘They’re protecting the card!’ I told him. People don’t want to use their last available credit line.” In these cases, the credit card is the safety net. Whereas failure to repay a payday loan won’t affect a consumer’s credit score, failure to repay a credit card will.

In order to truly understand the problem of reliance on credit, it is necessary to analyze what consumers are using credit for. When we do this, we see an increase in the number of people using credit cards to pay for basic needs. In 2006, one out of three families reported using credit cards to pay for basic necessities such as rent or mortgage, groceries, utilities, or insurance (Garcia and Draut 2009). Across the board, people are substituting credit for income, a strategy that is unsustainable. And, as credit has become more difficult to obtain, consumers have turned increasingly to expensive forms of small dollar credit, such as payday loans.

The changes in banks and credit cards discussed above have led to changes in the context in which we make financial decisions. During the same period that banks became more expensive to use and the use of credit expanded, conditions for American workers declined. Despite decades of increased productivity, the typical American family has experienced a steady decline in inflation-adjusted income since 1972 (Garcia and Draut 2009). Between 2000 and 2004, people at all income levels experienced a decline. The hardest hit were those in the lowest 20th percentile, whose wages effectively decreased 1.5 percent (Garcia 2007). Minimum wage workers are older and more educated than they used to be (Cooper and Hall 2013).

Declining wages have combined with a rising cost of living to make Americans’ financial situations even more precarious. Between 1984 and 2004, the cost of living has increased 90 percent due to the rising costs of healthcare, housing, and transportation (Dēmos 2007; Garcia 2007). Income volatility doubled between 1973 and 2004 (Hacker and Jacobs 2008). The average cost of higher education – a key indicator of future financial mobility – increased by 165 percent (in 2005 dollars) between 1970 and 2005. In the ten-year period between the 2003–4 and 2013–14 school years, prices for undergraduate tuition, room and board increased 34 percent at public universities and 25 percent at private schools (US Department of Education 2016). In addition, childcare is now a significant expense for families, whereas it was virtually non-existent as an expense as recently as a generation ago (Garcia 2007).

As a result of this squeeze between decreasing income and increasing cost of living, many people have begun to substitute credit for income, an unsustainable strategy (TransUnion 2014). Starting around 2000, many households began to use credit cards to cover basic expenses after first liquidating their savings and draining equity from their homes (Garcia 2007). Andrew Ross coined the term “creditocracy” to describe the current situation, one that emerges when the cost of goods, regardless of how staple, has to be debt financed and when indebtedness becomes the precondition for meeting basic needs.

Fifteen percent of Americans had poor credit scores (300–599) prior to the recession. By 2010, more than 25 percent were in this category (Whitehouse 2010). This change, combined with the contraction of credit discussed above, means that Americans are increasingly turning to expensive sources of credit such as payday loans and auto title loans. Although the research about whether these sources of small dollar credit are helpful or harmful to consumers, it is clear from the surge in usage of these loans and the reasons consumers cite for using them that financial insecurity has reached a crisis point.

The combination of these three trends correlates highly with the increase in the use of alternative financial services (AFS). Policy makers continue to push consumers to use banks instead of alternative financial services, but they rely on false assumptions about the differences between mainstream and alternative financial services businesses and the people who use them. Policy also fails to incorporate an understanding of the changing environment as laid out above.

The research for this section of the paper focuses on the time I spent embedded as a teller, loan collector, and hotline staffer, and on the interviews my research assistant and I conducted with over 100 customers of the businesses where I worked. This research enabled me to challenge four myths about what policy makers and researchers call “financial inclusion.” The first myth is that everyone needs a bank account. The second is that financial literacy would lead most people to make different (read better) decisions. The third myth is that the problem lies with the providers of alternative financial services, as opposed to the mainstream banks or broader systemic factors. And the fourth is that people who use alternative financial services lack mechanisms for saving. These myths and the stories we tell about the people who use AFS are detached from actual people’s lives, and lead us to believe that the problem is confined to a small, marginal group, when in reality it is an enormous problem that affects us all.

The agenda of the FDIC is to move the unbanked and the underbanked to bank accounts. The underlying assumption is that these Americans are underserved and that banks are the appropriate route to the “financial mainstream.” However, the FDIC’s arguments lack recognition of the complexity of the situation. The agency’s economicinclusion.gov website, for example, highlights only the downside of check cashers and payday lenders, and only the benefits of banking. A growing number of people do not have enough money to enjoy these benefits.

When I interviewed RiteCheck and Check Center customers about why they chose to frequent these businesses, they cited three reasons: cost, transparency, and service.

Policy makers, consumer advocates, and the media criticize check cashers for their high fees (Fox and Woodhall 2006; Choi 2011). However, when I asked customers why they used a check casher instead of a bank, they often told me that they found banks to be too expensive. Zeke, a RiteCheck customer I interviewed, told me that he had had a bank account in the past but that he had closed it after losing his job. “I’d like to go back, but I can’t afford the monthly charges,” he said. Zeke has been a RiteCheck customer for two years. Maria left her bank for the same reason. “The fees were just ridiculous!” she said.

Indeed, banks have become more expensive, and the increases in charges relate directly to the changes in policy discussed above. Policy, starting with Glass–Steagall, has attempted to keep banks from engaging in the kind of risky behavior that led to the Great Crash of 1929 and the 2008 financial crisis. Legislators have also required banks to serve the entire public without discriminating. Invariably, restrictions on banks in one area have led them to increase fees and rates in another.

The Community Reinvestment Act (CRA), discussed above, provides just one example of this dynamic. CRA was intended to combat redlining by requiring banks to provide banking and credit services to all communities. The law essentially grafted consumer services onto a system that had pulled away from consumers. CRA prohibited banks from engaging in other, more profitable services, such as mergers and acquisitions, unless regulators determined that the bank was in compliance with the law. Unfortunately, the law has never had very sharp teeth. It did incentivize banks to open branches in low- and moderate-income areas, but these branches were not always profitable; the customers in these neighborhoods have less money to save and invest than their wealthier counterparts, and checking accounts – a staple product for most consumers – do not make enough money for banks.

Banks therefore began to charge more for their services. They instituted a range of new fees and raised existing charges on everything from ATM withdrawals, which more than doubled between 1998 and 2011, to wire payments, debit card replacements and paper statements. The availability of free, non-interest bearing checking accounts decreased from 76 percent in 2009 to only 39 percent in 2011, and the average monthly service fee on checking accounts increased 25 percent in one year alone, from 2010 to 2011 (Bankrate, Inc. 2012).

Trust and relationships are another key reason people choose to use check cashers. Banking has grown increasingly depersonalized. Technology has abetted changes in the way we bank, and these changes have lowered costs for banks. While banking has become less relationship oriented, check cashers have maintained this focus on the customer. I experienced this when I worked behind the teller window, and the customers I interviewed also told me stories about the service they had received.

Nina, who has lived most of her life in the Mott Haven section of the South Bronx, where the store I worked in is located, told me that her mother had been very ill and that the RiteCheck staff had called to ask about her. “So we can be family,” Nina said. “We know all of them.”

Being a regular at a check casher also brings more tangible benefits. Marta, another regular, came to my window one afternoon with a government-issued disability check to cash. When I input her information into my computer, a message popped up indicating that Marta, a middle-aged Puerto Rican woman, owed RiteCheck $20 on every check she cashed. It turned out that Marta had recently cashed a bad check. Rather than charging her an overdraft fee or closing her account, as a bank might, RiteCheck had worked out a plan for her to pay back what she owed in $20 installments. On that particular day, Marta told me, she could not afford to pay the $20; she needed her entire check to cover an unexpected expense. We allowed her to cash her check and keep the entire amount (minus the regular fee).

Many customers also told me that a lack of transparency at banks contributed to the costs they incurred; they found it difficult to predict when and what they would be charged. Banks are required to provide customers with disclosure agreements when they open a checking account. These agreements, on average, are 111 pages long, and the language is difficult to penetrate. The date on which monthly fees can be withdrawn is subject to change. Customers who are living close to the financial edge, a category that is increasing, need transparency. Check cashers also have very clear and easy to read signage, as opposed to banks, which have virtually no signage. Consumers who are not familiar with banks have difficulty understanding what they can do in banks and what it will cost. Walking into a check casher feels more like walking into a fast food restaurant. Every service available is posted in large font on signs that span the top of the teller windows, along with its price.

Policy makers believe that people would make different choices about how they manage their finances if they had better information. What became more apparent to me as I worked in these businesses was that people lack good options more than they lack financial literacy. Many of the people I interviewed paid a high price to get their money or to borrow money because they had no alternative.

Many of the payday borrowers I interviewed knew that they would be unable to pay their loans back on time, but they saw no other way out of the situations they found themselves in. Azlinah, one of my fellow tellers in Oakland, took out five loans ranging from $55 to $255 each when her car broke down and she needed it both to get to work and to take her young daughter to daycare. The loans cost $15 for every $100 borrowed; all were due on the date of her next paycheck. Azlinah, a 22-year-old single mother, took the bus for a few weeks, but found it impossible to get to work and daycare on time. When the due date came, Azlinah could not repay the loans; she needed every dollar of her paycheck to pay the rent and utilities, and to buy food. So she paid the loans back and immediately took out others, paying a whole new set of fees and effectively extending the length of the loans. When the lenders tried to withdraw what she owed from her checking account, her account didn’t have enough money to pay out, and she was hit with overdraft fees that quickly mounted to $300. Suddenly, her debt had skyrocketed.

As a teller, Azlinah understood that these loans can be problematic. Day after day she deals with customers who pay off their loans and immediately take out another. “I know it’s bad,” she told me. “I knew what a payday loan was.”

Working as a teller and a counselor, I learned that the customers I served often paid high prices for their money because they needed every penny they could get as soon as it became available to them. Banks routinely hold checks for several days until they clear, while check cashers enable customers to get their money (minus a fee) immediately. Joe Coleman, president of RiteCheck, told me that his customers would rather pay a flat fee that they understand than get hit with unexpected charges and overdraft fees at a bank. He explained that people trust his tellers and continue to return because they find RiteCheck to be less expensive than the local bank, and because they value the transparency, the convenience, and the service they receive: “Let’s say a customer gets paid on Friday. If he brings his check to us, he gets his money immediately. He can pay his bills right away, go food shopping over the weekend. If he goes to the bank, his check won’t clear until sometime the next week. He’ll be late on his bills. And if he writes a check and it hits his account before the check he deposited clears, he’ll be hit with an overdraft fee for more than $30 – much more than the fee he would have paid us.”

Michelle, a young RiteCheck regular, came to my window one morning to withdraw money from her Electronic Benefits Transfer (EBT) card. The New York State Office of Temporary and Disability Assistance (OTDA) delivers cash and Supplemental Nutrition Assistance Program (SNAP) benefits on these cards. The state deposits benefits into an electronic account that recipients can access by swiping a card at an ATM or a terminal like the one I used at RiteCheck. RiteCheck charges a $2 flat fee for any withdrawal regardless of the amount. Michelle asked me to withdraw $10 from her account; she would get $8 back and pay what amounted to a 20 percent fee. Even though EBT recipients are allowed two free withdrawals each month from certain ATM machines, these machines only dispense money in certain amounts. Most machines have a minimum withdrawal of $20.

The majority of EBT customers I worked with and talked to needed every dollar they could access as soon as it became available to them. This behavior is logical; it is also expensive. Michelle needed that $8 right then; she could not wait to accumulate enough money in her EBT account to be able to pay a lower price per dollar. This is the same dynamic that results in people paying high prices in local delis rather than shopping at discount stores that require buying in bulk. A well-paid job, a steady car, and space to store bulk goods means that spending $200 at once can save money over the long term. The benefits of bulk shopping, like the benefits of banking, are not equally available to everyone.

Working people increasingly need this kind of liquidity also. Carlos came into RiteCheck often to cash checks of several hundred to a few thousand dollars for his small contracting business. One Thursday afternoon he came through the door dressed in work clothes and passed a $5,000 check through my window. I scanned the check, counted out his money, and slid the $4,902.50 through the window. The $97.50 fee – 1.95 percent of the face value of the check – is regulated by state law. New York, which is one of the most highly regulated states, has one of the lowest fees in the country.

There are at least two different reasons why Carlos would pay nearly $100 to get his cash quickly. If he is like many contractors operating in New York City, he relies at least in part on undocumented workers, who are unlikely to have bank accounts. If Carlos had deposited his check into a bank, it would have taken too long to clear for him to have paid his workers on time. Another possibility is that Carlos was hired to do a job that needed to be started quickly. In that case, he would need the cash in order to purchase materials. Michelle’s and Carlos’s stories illustrate that they did not make irrational decisions and that more financial literacy likely would not have changed what they did. This does not mean that alternative financial services work perfectly for the people who use them; for many people, though, they make more sense than banks.

Consumer advocates and policy makers believe that the alternative financial services industry is driving the problem of financial exclusion. Researchers, financial regulators, and the media use words like sleazy, predatory, and abusive to describe check cashers and payday lenders (Noah 2010; Montezemolo 2013; Johnson 2014). As a result, solutions to the problem of “financial exclusion” have focused on further regulating these businesses or making them completely illegal. Although additional regulation is likely warranted, regulation will not eliminate demand. Policy recommendations need to focus on the nature of demand – on the conditions that lead people to seek these products and services. The increasing demand stems from the trends outlined earlier in this paper.

During the time I worked as a credit counselor, I talked to Jeannine, a woman in her thirties who moved to Virginia from Pennsylvania after losing her job. Jeannine quickly found a new job but she had to wait a month before receiving her first paycheck, and she needed money to secure an apartment and cover her moving expenses. She turned to payday loans to get her through the transition. Another hotline caller, Mae, took out a loan to move her mother from a “horrific” nursing home to a better one. “I knew I couldn’t handle the debt,” she told me, “but I couldn’t leave my mother in that place. I would do anything to help my mother. Wouldn’t you?” Both Jeannine and Mae soon found themselves with debt they could not handle, but it is hard to argue that they made poor decisions given their circumstances.

The fourth myth about check cashers and payday lenders is that they inhibit savings. Savings is clearly a problem in the US. The US has one of the lowest savings rates among all developed countries. In the first quarter of 2013, the personal savings rate was 2.6 percent, down from 5.5 percent in 2009 and 3.9 percent in 2012. In comparison, in 2012, the savings rate in France was 12.3 percent, Germany was at 10.5 percent, and Sweden was at 10 percent (Kramer 2013).

It is true that check cashers and payday lenders do not take deposits; given the way they are regulated, they cannot. A few, like RiteCheck, have figured out a way around this problem. RiteCheck partners with a local credit union, Bethex FCU, to offer customers a seamless way to save. RiteCheck customers can open a Bethex account and deposit money into that account at any RiteCheck store. Many of my interviewees also told me they did not trust banks with their money. Some participate in rotating savings and credit associations – ROSCAs – informal groups that are often rooted in immigrant communities. Others save at home. Mike, a regular RiteCheck customer, told me he had a bank account but closed it because he does not like banks. He does save, however, and described his savings process like this: “You gotta put pressure. You say this is what I’m going to spend for the month, and this is what I’m going to put away, even if it’s a hundred dollars. You make sure you don’t touch those hundred dollars. That’s the key.” When I asked Mike where he saved, he said “I put it in a drawer. Put it in the closet and I don’t touch it, and it doesn’t bother me because I budget everything else. Once I budget everything else, then it all adds up.”

Many of the people we met who use ROSCAs earmark this money for building assets. Carmen is using the money she saves in a tanda to build a home for her mother in Honduras; it will be completed this year. Maribel uses the tanda to pay her tuition at a local community college. Even though she has had to provide for her two younger siblings since their mother was deported to Mexico several years ago, Maribel has been able to avoid student loans. She studies early childhood education and plans to get her BA next and then her master’s degree at Columbia. She works part-time at a daycare center on Manhattan’s Upper East Side and goes to school in the evening. She beams when she tells us her younger brother is in college, and that her sister will be starting this fall.

The dysfunction that characterizes the consumer financial services industry is the product of decades of policy and practice and it will not be changed overnight. Creating an atmosphere that once again delivers on the social contract Americans can count on to reward their work and give them the confidence and resources to invest in themselves and their families will require significant changes in the public and private sectors. It also calls for collective, grassroots action. It requires a movement.

Policy makers must reframe the conversation based on a better, more complete understanding of what consumers actually do and why they do it. The policy conversation about “financial inclusion” needs to extend beyond banks, payday lenders and check cashers to informal practices and new products that don’t fit neatly into the old categories. Further, any regulation of consumer financial services must be accompanied by policy that reverses the decline in real wages and addresses increasingly entrenched income inequality.

Fix the regulation. The alphabet soup of current bank regulation is opaque, confusing, and may be inhibiting innovation. Change has been incremental, and the result is a patchwork quilt of policy that is difficult to understand.

When banks are evaluated to determine whether they’re serving consumers well, the process generally consists of regulators doing a lot of box-checking. The problem is that checklists often fail when we really want to know the answer to questions like, “Is this practice fair?” and “Would I sell this product to my mother?”

Make it easier for consumers to get quality information. Financial decision-making is wrapped in a veil of mystery, and the topic of personal finances triggers a range of emotions in us, the majority of them unpleasant. Suze Orman has built her career by recognizing how deeply past experience and perceptions of self-esteem shape the way we deal with our money. Typing the term “Money Shame” into Google yields 164 million results.

The consumer financial services industry is much more complex than it used to be. This is good news and bad news. The good news is that I should be able to find a credit card that meets my needs and a budgeting tool to help me keep track of my spending. The bad news is that it’s incredibly difficult to wade through the information available in order to make decisions, and to figure out which information is reliable. Montel Williams is the celebrity spokesperson for Money Mutual, a payday lender. He also has close to 78,000 Twitter followers. Nerd Wallet has 11,000 followers. If I’m a Montel Williams fan and I’ve never heard of Nerd Wallet, whom do I trust?

Make work pay. This recommendation has nothing to do with consumer financial services, at least on the surface. But the market, in the form of alternative financial services, is responding to the condition consumers find themselves in. Declining wages, escalating costs of education, healthcare, and childcare, and extreme income volatility have combined to create a triple whammy that lies at the root of the crisis in consumer financial services. When we focus solely on rules and regulations, we are treating only the symptoms of the problem rather than working to find a cure.

Broaden capital ownership. One way to ensure people can deal with the inevitable ups and downs life brings is to enable everyone to build a nest egg from an early age. The American Saving for Personal Investment, Retirement and Education (ASPIRE) Act of 2013 proposes to establish a savings account for every American at birth. Each account would be endowed with a one time, $500 contribution ($1,000 for children in households earning below the national median income) from the federal government. The accounts would incentivize savings, and account holders would not be able to withdraw funds until they reached the age of 18. The UK has had a system of children’s savings accounts in place for many years.

This chapter demonstrates that the “banked/unbanked” frame currently applied to consumer financial services is inaccurate. Instead of categorizing people according to whether and how much they use a bank, we need to understand whether they have access to safe, affordable financial services. Too many people are lacking this asset, which is critical for fully functioning in the economy and in civil society.

{kind=link}