For every probability distribution function f(x), there is a corresponding cumulative distribution function (CDF), denoted by F(x) and defined as:

Table 4-3. Dice example

The expression on the right means to sum all the values of f(u) for u ≤ x.

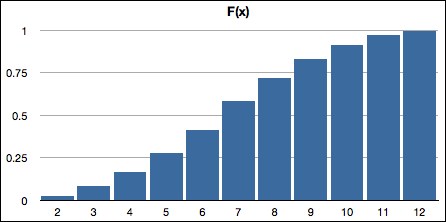

The CDF for the dice example is shown in Table 4-3, and its histogram is shown in Figure 4-6:

|

x |

fX (x) |

|---|---|

|

2 |

1/36 |

|

3 |

3/36 |

|

4 |

6/36 |

|

5 |

10/36 |

|

6 |

15/36 |

|

7 |

21/36 |

|

8 |

26/36 |

|

9 |

30/36 |

|

10 |

33/36 |

|

11 |

35/36 |

|

12 |

36/36 |

Figure 4-6. Dice cumulative distribution

The properties of a cumulative distribution follow directly from those governing probability distributions. They are:

- 0 ≤ F(x) ≤ 1, for every x ∈ X(S)

- F(x) is monotonically increasing; that is, F(u) ≤ F(v) for u < v

- F(xmax) = 1

Here, xmax is the maximum x value.

The CDF can be used to compute interval probabilities more easily that the PDF. For example, consider the event that 3 < X < 9; that is, that the sum of the two dice is between 3 and 9. Using the PDF, the probability is computed as:

But computing it using the CDF is simpler:

Of course, this assumes that the CDF (in Table 4-3) has already been generated from the PDF.