Monetization or: The Romance of the Click

By developing a fundamentally new way for people to create, distribute and discover content, we have democratized content creation and distribution, enabling any voice to echo around the world instantly and unfiltered.

Twitter S-1, October 20131

Among the ruins of the dot-com bubble were the dreams of banner advertisements paving the path toward a new life. A few inches at the top of the page were supposed to be incredibly valuable. The idea of a simple technology providing an income for millions of people is appealing; build it and they will come. Space on websites could be more tightly targeted, more interactive, and more direct than any advertisement that came before. New advertising products would seem to be much more valuable than their analog predecessors. Viewers can’t click a bus ad—it drives away, leaving a cloud of smoke. Internet advertisements don’t smell and won’t make you cough. Any sliver of space where an advertisement could appear was presented as an opportunity for monetization. This is no mere buzzword—“monetize” appears in legal documents, popular press articles, technical descriptions, and everyday life. Monetization has become the stand-in for a host of business processes, including advertising sales, lead generation, inventory management, and customer service, among many others. It is unclear exactly what monetization is and what it isn’t; we know that it is the thing that generates wealth. Wealth is good. Visions of infinite wealth inflate bubbles.

Money is the root word of monetization. Writing the history of money is not a topic for a book chapter; several volumes would be inadequate. The review of the history of money and monetization literature in this chapter reveals an important emptiness. Instead of a smooth, linear trajectory from barter to the electronic market, the actual assemblage of facts seems to unfold in a contradictory and herky-jerky way. Unlike the smooth stories of monetary development repeated so easily in economic literature, the story is very complicated. Monetization is often defined as either the rapid expansion of the production of official money or the expansion of money to ever-expanding realms of social life: these don’t improve clarity in understanding the use of the term in the world of social media. Money is tricky, it means but it doesn’t mean, it has the weight of soldier’s steel, but is as light as linen.

From this poor anchor point, the chapter will unfold the meanings of monetization in the political economy of social media. Monetization appears as arbitrage, extraction, and alchemy. Metaphor makes the actual business distant, yet intelligible. Just as an affiliate link makes the idea of a referral less banal, the extraction of key of “influencers” makes the idea of advertising less boring. The unstable, amorphous, and shifting sands of monetization are the grounding point of the bubble world. Once declared found, or at least deferred, a monetization strategy adds texture to the entire scene of the business. Beyond the idea of what a business might be, dreams of monetization carry the logic of the romantic individual self as a central theme. It is not simply that they claim to secure value from people, their attention, or their clicks, but they must also theorize who those people are, and what it means to be a person with attention. Monetization is the defining concept of this era.

This chapter covers quite a bit of territory. The ideas can be broken down into a few useful clusters:

• The story of monetization requires a discussion of money itself. More than a simple social construction or mere transaction moderator, money interacts in any number of curious ways with culture. Monetization introduces any number of slippages and surpluses that need to be accounted for in understanding social media.

• Monetization Metaphors. Each of the three primary metaphors for monetization—arbitrage, extraction, and alchemy—be presented at length with allied examples of how they are literalized in the media industries. The meaning of money itself shifts depending on the metaphor.

• Monetization schemes will be situated in the dominant language of the social media companies for selling advertisements, specifically in the idea of the social graph (Facebook) and the interest graph (Twitter) and what these different models of monetization, market segmentation analysis, advertising, and public relations say about the larger structure of the media industries.

• Pinterest will be considered as an outlier, as the network should be considered a prime property as per social media industry discourses, but is often ignored or even maligned.

A brief history of monetization

Money is tricky. In one sense it is incredibly simple; money is a transaction moderator that is more efficient than barter. This story is not untrue. Money is durable, easy to transport, and, if emblazoned with the markings of a strong state, authoritative. Money is more than an effective transaction moderator; it is a thing that is valuable in and of itself. Scrooge McDuck, Disney’s extension of the Donald Duck archetype for the Regan generation, loved to swim in gold. Scrooge’s pool of bullion, his money bin, is a central narrative device in many episodes as access to it is the highest priority. A giant box full of gold is the most valuable thing in the world, aside from his nephews and their friend Webby. Money is magical; it is a metal that flows.

A surprising number of theories are willing to take barter story for granted as the basis of the authority of money. The barter story is persuasive for a number of theorists in politics, economics, sociology, and communication as it seems to provide an elegant description of a social process with a very small number of assumptions. If the role of money in society is simple in the context of the theory presented, the barter theory might be enough; if money plays any larger role a more complete accounting is called for. There are a few considerations in the history and theory of money that weigh heavily in this book. First, the historical trajectory from barter to Bitcoin is by no means linear or clear. Second, on a personal level, conceptions of money exceed the boundaries of mere transaction moderation. People love money; they hoard it. Third, theories that depend on the barter theory of money provide it with power beyond the mere extension of barter: the ostensible evil of money is taken as a powerful starting point in many social theories. Money is described as being more than a mere transaction moderator on the structural level; it is an agent of either salvation or destruction.

The use of money and money-like instruments has waxed and waned over the course of history, with money taking different forms, and transforming different societies along the way.2 David Schaps argues that the earliest society to use coin money was Athenian Greece.3 Before this, payment standards existed, but came in the form of specified amounts of grain, metal, or other local materials.4 Accounts transacted in silver could be measured in barley, for example. Relationships between money types were difficult as the properties of different money like things were very different.5 This stands in contrast to historical theories that might deny that money transactions existed before coinage. Transaction forms other than pure barter preceded the existence of money proper. The technology of money does not have a single origin and was likely invented autonomously in at least three places.6 Kublai Kahn transitioned his empire of the thirteenth century to purely paper money.7 The earliest forms of paper money in the United States were tobacco-backed notes in the nineteenth century, with many states allowing wildcat banks to issue their own currencies.8 Theories of money that begin with the United States miss almost the entire history of currency.

A contemporary economy with money is an economy with serial numbers, standardization, and more easily transmitted pricing information—which is not to say that money drove the development of new market technologies. Electronic trading via telegraph came before the standardization of money.9 Instead of an even historical evolution of exchange relationships, the very thing that facilitates exchange is unstable and highly political. Without belaboring the point, it is fair to say that the story of barter quickly giving way to money is an occasionally useful counterfactual.

In his account of the history of money and desire, What Money Wants, Noam Yuran argues that the history of money is a counterfactual shibboleth—tales of the rise of money are necessarily false, and their expression ties the teller to a community.10 Telling the story of the rise of money sets the parameters for a theory of the economy. Money is worthy of consideration in its own right, specifically the ways in which the desire for money shapes the ostensibly rational world of economics. Values and aesthetics are focused by money like a lens. Yuran’s central contention is that money is not a historical communication technology, but as desire itself. What does this mean for this analysis? The desire for money is detached from what it actually is. Monetization is the prospect of making more, more reality, more power.

Yuran positions John Searle’s theory of money as social agreement as an alternative to this view.11 Much like the barter story, the social agreement story supposes that people came to accept one day that money was valuable. If money were to simply be a unit of exchange that exists as much as it socially agreed upon, more money would be produced, allocations of wealth would be overthrown, and the underlying agreement changed. Searle’s account of money as agreement would need to account for the processes by which the agreement is made and maintained; it is not enough to posit an explanation of how money works; a theory would need to account for the ways that money appears legitimate.12 After establishing that money is an agreement the turn to the quick historical narrative covers the rest of the history.13 Money is more than a mere effect of other desires: it is co-productive with desire. Fetishistic attachments to money would make little sense as it would merely be one of many possible transaction mediators.14 In overcoming many possible challenges, both practical and intersubjective, money proves that it has value as much as it can disavow challenges to its own authority. Yuran’s approach requires that theories of money that are affectively sophisticated be woven into theories of economic systems. There is no magical solution in this conception of the market, but a new insistence on affect from the lowest level up. After all, to say that all the social functions and positions of power related to money are tied to mere agreement loses the monotheism of money—there is no money but money, except all the other money.

Consider a common accusation in right Libertarian political discourse of the United States: the Left will debase the nation’s money. The accusation is a response to plans to build social programs or infrastructures through government spending. It supposes that in order to finance programs, additional currency would need to be created and this currency would not be backed by gold. There are many problems with this argument. Few currencies have been backed by convertible gold. Some inflation can be healthy, while deflation is associated with depressions. Gold convertibility is an idea from the late nineteenth century. The period of time when private persons in the United States could demand payment in gold, keep bullion, with no alternative money, was very short. Events during this apparently auspicious era include numerous panics, recessions, and depressions. Yet for some, the end of the gold standard was a capital crime. It removed the stable referent from the value that made the world coherent. There are many factual problems with the debasement narrative, which may be an important part of how it continues to be persuasive. Joining the movement of people invested in the story would confirm accession to that ideological matrix. Campaigns against debasement retroactively legitimate a currency that was never legitimate in their framework to begin with. These alternate histories posit the past as stable and harmonious, a key reactionary fantasy.15 Everything was awesome: objects had clear and transcendental meanings, until these people and their words got in the way. It should be no surprise that the economic histories offered by gold bugs have particular pathologies—since everything was better in the fantasy space of the gold economy; the real problems with a rapid boom-bust cycles are ignored.

Turning to the social scene of money, the presentation of money as a social force is complex. In The Social Meaning of Money, sociologist Viviana Zelizer emphasizes the point that most histories of money overplay stability. Zelizer argues that even important accounts like Simmel’s History of Money overstate the stability of currency.16 Simmel’s “colorlessness”, a nineteenth-century theory of the colonization of the lifeworld, demonstrates the problem with the assumption of a happy, stable money in the nineteenth century.17 It is new money that causes problems, not the old money. Things became too stable, too commoditized when exposed to money for Simmel, an argument common across critical theory. Zelizer’s approach is important as the social meaning of money is independent of the function of the currency—money is not a neutral transaction mediator and it never was. Zelizer defined monetization as the increasing use of money.18 Zelizer’s money was transformative, strategically reversible, and unstable. The use of money brings social change. Although money may flatten some relationships, the idea that money is always already corrupting is conceptually too simple to deal with the strategic reversal of power relationships that transactional arraignments might produce. It is not always a loss or flattening when uncompensated labor is remunerated. Values constantly shift around money, and if the analysis in this chapter is persuasive, money is often defined by the idea of things that it purchases or prices, just as they are redefined by it.

Zelizer’s history focuses on the late nineteenth century and the practice of earmarking, or delineating pools of money to be used for different purposes. Once in a pool, money would be appropriate only for certain tasks. Money from gambling would be dirty, while money from digging a ditch would be virtuous and clean. Expanding the use of money produced new social dynamics and possibilities; the story of rationalization or colorlessness, to use Simmel’s term, is not born out in the history of the nineteenth century.19 The attention to the actual affective dimension of the use of money that comes from Zelizer is something that this book aspires to and thus I try to avoid recourse to positions that assume the stability of money, the cross-cultural power of money, the preference for noncommercial values, or the automatic corruption that comes with monetization.20 Just as these conceptual errors drive poor theory in orthodox economics and business, they also lead to faulty media studies research. This is not to say that there are not times when money can be corrupting, but to assume this as axiomatic in cultural critique is too simple and too quick a move for a deep and foundational problem. This is one of the most important melodramatic assumptions in media studies. Disciplines turn to fables when the stakes are high.

In other sociological work, money often appears in a relatively conventional vein. Monetization functions in this original context as a speech act, as money’s value is performatively produced.21 Anthony Giddens and Clifford Geertz both use monetization to refer to the process of rationalization.22 Marx posed monetization as one of the advanced phases of capitalism; money is alienation.23 Money in this sense distorts the relationships between the worker and their labor by providing world-making power that should have instead been derived from the distribution of material.24 John Durham Peters juxtaposed Lockean and Marxian conceptions of money as concepts of dissemination: Locke welcoming dissemination and Marx despising it.25 The limits on the economy that would be essential to the stability of a Lockean system, mainly concepts of propriety and stewardship, are mitigated by money as it does not spoil. The Marxist critique supposes a transparent theory of communication. For Peters, this calls called for a more serious consideration of the sources of power in communication as dissemination might be more productive than it at first appears.26

In Debt: The First 5,000 Years anthropologist David Graeber argues that the process of monetization is the redistribution of debt under different symbolic codes.27 Debt prefigures money. Money in this sense is not created by the government, but by a network of financial institutions (of many eras and types) ad hoc, and that this structure is underwritten by the need to finance the basic business of military operation, or, in Graeber’s terms, “tribute.”28 Crises for the modern state come in the seeming incapacity for monetization to expand membership in the middle class to the population as a whole, that the strategic reversibility of power relations noted by Zelizer would not be maintained. Monetization would expand, but money wouldn’t be well distributed. People like monetization schemes if they get a share. In much the same way, the story of the turn to hard money for Graeber fits with the psychoanalytic account of the retro-causal effect of the gold standard for Yuan; foundational metaphors help things make sense. Graeber’s idea that money is always inadequate, that it only stands in when a debt cannot be paid, is insightful as it speaks to the impossibility of exchange—something also true of language itself.29

Money isn’t just a convenient way to transact business, but a great place to store pent-up feelings. Money both flattens and acknowledges their facticity. The story of money could be even more complicated than we know. Something is denominated, transformed, cooked, split, acidulated, transferred, or somehow manipulated into another state. Even if we were to take money as a dynamic stabilizer for social systems, the social structure created by that force is very real—money shifts and changes, friends and enemies blend. The “sharing economy” is perhaps the most perverse version of this idea; sharing can exist only if a cut is sent to San Francisco. Arjun Appadurai’s juxtaposition of the gift and consumer economies has become a doppelganger.30 Remaking the world through the disavowal of transactionality is romantic—the idea of money polluting otherwise pure relations is a comfortable idea. Yet all of the examples of sharing that have become so fashionable involve the exchange of money.

Graber notes the importance of the theology of monetization through George Gilder’s 1981 bestseller Wealth and Poverty.31 Gilder’s theology of wealth posed that money was the extension of the creativity granted by God—this theory of money creation and double theology drove the relationship between the Evangelical right and supply-side economics. Who would doubt the will of God to make some people rich? Separating the theologies of the rich and the poor shows the affective power of money as a thing itself—the state of being of contemporary money can be found in divinity. The money of the poor, money from labor, is different from the money presented as the reward of investments for the rich—higher taxation rates for regular income and lower tax rates for dividend income are only a reflection of a pseudo-Calvinist doctrine of taxation for the preordained.32

Consider the leading alternative form of money: Bitcoin. The relative appeal of computationalism, the price of Bitcoin, and the Winklevoss Bitcoin exchange-traded fund (ETF) in particular, function as an index of paranoia.33 ETFs suppose that an investment manager could craft a portfolio that follows the public perception of a particular asset, industry, or quality. A gold ETF would include a variety of investments in companies that handle gold or gold-processing technologies. Mining equipment can easily be a better investment prospect than mining. If the fate of gold improves, the underlying assets should increase in value and thus shares of the ETF should increase in value; the opposite is also true. The block chain does not transcend the psyche of the investor. Mr. Market is more persistent than the most unyielding zombie. If Bitcoin is not money, it is something akin to a social network of money producers, with their own bubble world, which hinges on money.

Bitcoin is a metaphor for the larger case of legitimation in the early twenty-first century—value is more than allocated or managed; it is imagined. This is not the first time that value has come from the affective dimension of currency; this is in fact one of the clearest aspects of the history of money. Money means and feels. In the case of computational money, this deeply personal aspect of value creation is wrapped into the fantasy structure of capital itself. Legitimacy is performatively backstopped through computation. Instead of the coup de force of a state or government the raw gravitas of waste heat and wanton electrical consumption serve their purpose in providing the narrative of value for the money. Supercomputing clusters will drive the bubble in alt-currency. Even with payments in an alternative currency, the businesses that use this money and the contracts they make will still be party to law. Dreams of escape from the law and government fail at scale. Secrecy is for small organizations, more on this in Chapter 3. In this sense, the dream that Bitcoin could become money without money is not false because of the failure of the currency, but because of its success. What is subject to monetization becomes money.

In everyday life, “monetization” can be something of a cynical term referring to the failed models that circulate so freely in the public sphere. “How are you going to monetize that?” would carry by the implication that the person you are conversing with believes your business to be flawed. Explaining a monetization plan would be a matter of providing a justification or an explanation, rather than just some additional details. In the act of asking for details it seems likely, if not probable, that an interlocutor is looking for more than a gloss on a business plan, but a metaphor as well. Confident expressions that future monetization is assured confirms that one knows they are among the monetized few. Rejecting a billion-dollar buyout from Google or Facebook is no act of hubris: it is an act of witness in the power of money.

Financialization, the tendency for the economies of great powers to increasingly focus on financial products to the exclusion of basic research or commerce, hollows out the marrow of an exchange network just as it reaches peak value.34 Financing a car sale is more lucrative than selling or building the car. Monetization is seductive. A crude critique of the instrumental rationality of the machine or the market does little other than confirm bourgeois morality. Money is dirty, awful, wonderful, and everywhere.

Monetization as arbitrage

Monetization often means arbitrage. One guru has gone as far as to name his entire concept after the linkage, “lead generation arbitrage.”35 For the uninitiated, “lead generation” is a sales term for a referral. Typically, leads that are cultivated (spoken to with regularly) are far more likely to convert (make a purchase) than customers browsing the internet organically or bluebirds. Making a sale takes time and effort. Brick-and-mortal retailers commit to developing a relationship. Wasted time is wasted money. Online there is less of a risk of wasting time when selling consumer goods, but there is a real risk that nothing will happen. If you were to enter your information on a real estate agent’s website, you would get a call quickly. A small percentage of people browsing housing websites actually intend to make a transaction. Houses are interesting to look at. Leads are valuable. Web-based models make this waiting process cheaper.

The underlying assumption made in arbitrage is that the identity of one quantity can be substituted for another. Simple arbitrage involves selling a single good on two markets. If one is buying and selling pigs, they could exploit price differences to buy and sell pigs on different markets to be delivered at a later date. You have the pigs in Detroit to sell on Tuesday; you take the best price available between New York and Chicago. Arbitrage is a pure price play. It is a classic business.

Small changes in communication technology make these opportunities particularly attractive. Telegraph-based commodities arbitrage began in the 1850s between Cincinnati and New York.36 Some products tend to be particularly well suited for this type of transaction. Pork bellies, frozen orange juice concentrate, and oil are all relatively standard, durable, and easily tradable. Alissa Hamilton has detailed the ways in which orange juice production has been crafted to ensure a constant supply of goods; deoxygenating standardization offers the orange juice industry a unique measure of stability in product production that is not present in other markets.37 To be well suited for arbitrage a product would need to have a stable identity that can be transported. Web browser cookies and clicks are particularly good in this regard. Online products are made for trade. They are already similar and their transportation is as easy as pressing a button. Beyond simple spatial arbitrage, futures contracts allow arbitrage to occur across time.

Buying beef in Chicago and selling in New York is no longer the most common form of arbitrage activity. Pork belly arbitrage ended because there simply was not enough hedging activity to keep the market running.38 Futures and options allow agricultural firms to manage risk and secure future cash flows. Insurance programs and other subsidies blunt the impact of price fluctuations on the market. Futures contracts can become objects for arbitrage in their own right if they are mispriced. Similarly, this idea of arbitrage includes short selling stocks. To sell short, one would need to rent stock to sell now and rebuy at a lower price. The original shares would be returned to the lender with rent. Naked shorting is this very practice, although without the benefit of having pre-arraigned to rent shares to sell and repurchase. One could easily attempt this practice and find that the owner of shares to repurchase charges an exorbitant price; this is called a short squeeze.

A typical exchange in a forum would pose an arbitrage scheme where one would create a website with content and ads, join an advertising network, and route artificial traffic to secure payment from a major advertising network.39 The business plan: if the advertising revenue generated by the traffic is fifty dollars and the cost of the traffic is only twenty-five dollars, the person running the website makes twenty-five dollars. In this world the user “sends” traffic to a website. As long as the network recognizes that traffic, it counts.

Artificial traffic is the ultimate arbitrage play: substituting fake clicks for real clicks. Clicks are clicks after all. At least, until the ad network detects the robots producing them. The arbitrage occurs on the side of the advertising network; the person using this system is claiming that a click is a click regardless of the source. Traffic sales companies can easily route large click numbers to websites and the creators expect to generate a substantial yield if the advertising network cannot accurately determine the kind of traffic hitting the website and seeing the ads. Often, sources of traffic for hire are not reputable.40 More legitimate sources of traffic include accidental clicks or even occasionally well-written headlines on pages intended for arbitrage. As of the writing of this book, a page intended for arbitrage will have between thirty and forty ads wrapped around little to no human created content. These products bask in the warm glow of pure traffic.

Why do major players tolerate this? Ad networks are a low-margin business. Any transaction is a good transaction. Companies in the social space are layered with one backing up others. The initial arbitrage may use Google Ad Words to secure traffic to generate clicks via Taboola or Outbrain as the actual paying party. If the sponsored content link is slightly more valuable than the Ad Words click, the arbitrageur makes money. As long as an ad network attached to the next page will pay more for the click than the page prior, the click could be passed on for eternity. Or, at least until the user tires of viewing poorly designed pages and clicking advertisements. Then the last site with the user loses as they paid for the user to be brought to the page assuming they could sell that user to the next page for a larger sum of money, assuming there was even a user in the first place. This repeated selection process could be an effective strategy to sort false positives from a potential victim pool. Microsoft’s Cormac Herley has described the idea that the biggest problem for scammers is the false positive.41 If someone can be passed between garbage pages, they might be a viable victim for a more vicious operation. Losses on individuals bouncing between initial arbitrage pages can be tolerated if the final payoff is large enough.

Arbitrage also occurs between advertising networks. This could include placing advertisements of inferior quality, or even attack sites, through some other firms advertising network or other means devised after this book was written.42 Hackers affiliated with the Syrian Electronic Army have had success using third-party advertising inserts as a source of bots for their net.43 There are a number of different advertising networks that share basic sources of traffic; these networks often place ads from affiliates. In this sense, an advertising network is an advertising network is an advertising network. Anyone willing to pay to include their content on a page is a potential source of cash. Given that the categorical identity of the advertisement is assumed to be stable, anything that can be named an advertisement should seemingly qualify.

On the other hand, the Yieldbot blog formulates arbitrage not as substituting user for user, but intent for intent.44 At the end of the day someone needs to be making a purchase to support the business ecosystem. The intent of a person reading a website is likely distinct from the intent of a person looking to purchase shoes. While Yieldbot’s approach is an improvement, it does little more than any established path for advertising communications, which is why as Yieldbot concludes, “the future of the web looks a lot like the past.” The future: affiliate link exchanges.

According to MonetizePros the process has two steps: buy cheap clicks and max out ads.45 Pages designed in this tradition look like the classified advertisements of the 1990s. Small boxes litter the screen, with tiny writing, and garish colors. Sexy, disgusting, and otherwise provocative images are commonly served by the site designer’s third-party ad network. Social network firms know that these pseudo-news products damage the user experience and actively work to deemphasize them in the feed. Click page specialists attempt to design around their efforts to suppress them.46 Or, as another click page designer put it, “Cheap clicks + High Pageviews per Visitor + Lots of Ads = Arbitrage Profit.”47

Although these descriptions seem strange at first, they are ultimately not dissimilar from the attention arbitrage that underwrote the broadcast era. Television had an established business model depending on a combination of revenues from advertising, subscription payments, and product placement. The program provider is selling the audience, a concept much akin to the pricing of banner ads. The arbitrage idea, if applied to television, works through the metaphorical bond between the chance to access one audience and treat it as if it is another audience. An audience tuning in for a show is not necessarily the audience for the advertisement, although some of them could be.

While convergence theory has rightly demonstrated the importance of televisuality to the internet, the relationship between the revenue structures of the industries is less than clear.48 The underlying relationship is also under unique stress. Advertising revenues on television are decreasing and the reliance of television systems on carriage fees is breaking the business. The great fear in the screen industry is that users might arbitrage the past for the future, disconnecting their cable and satellite systems so that they might watch Cheers from now until the end of time. Sam and Diane had the greatest romance.

Affective products are tricky for arbitrage. In the literal sense, this is the distinction between a small farmer and a beanie baby boutique buyer. The 1998 Beanie Baby buyers’ guide armed purchasers with prospective future values for their plush novelties.49 Buyers were promised outlandish returns for storing beanie babies for a number of years. Antique toys become valuable because the objects were loved, not because of the idea of the future value of the novelty. Affective investment in the object often precedes affective investment in the price tag, although not always. Treating the beanie baby as a potential investment object changed the underlying affective conditions that drove people to love these toys in the first place.

Demand for media products is inelastic; there is only so much money for entertainment, shoes, or propaganda. Clicks outstrip coins. The fantasy image of media economics hinges on the presence of an apparently stable normal state for an industry that has been seemingly upended by new technologies. Instability is the norm. There were never more than a few years without some upheaval in the television industries. Click-through rates for online advertisements are already known to be extremely low; the most effective advertisements on Facebook are those which feed on already generated sales leads.50 These leads are typically worth three times more than initial advertisements.51 Completing the conversion process is where the money really is. Monetization as arbitrage relies on the idea that there is value in some other industry that can simply be transferred into a business form like those in the new company. The metaphor becomes a simile, and the relationship strains under examination.

Arbitrage, program planning, and re-runs

Network television traditionally sold advertising time during programs well in advance. Every spring during “upfronts” networks would put on a show to convince media buyers to purchase packages during top programs for the next spring.52 Billions of dollars changed hands. The underlying relationship is very similar to the arbitrage relationship described in the online advertising segment. An important idea from this media industry is retained in the sale of advertising today—that nobody knows what will be a hit. This idea informs key works in media industries theory. Richard Caves formalized the nobody knows principle in his grand theory of the creative industries. Caves derived his principle from empirical studies of the television programming and industry lore.53 It does not take a trove of hacked e-mails to conclude that studio executives are adapting to the market at best, and randomly guessing at worst.54 Researchers in media industries thrive when they are positioned to avoid demand modeling of the industry, focusing instead on the actual discourse and business practice of the media.

Econometric work in demand modeling faces a second hurdle, even if demand was easily modeled; executives make decisions based on factors other than demand. The most important and award-winning television shows are not those that fit existing models, but those that play with and even break those models. All in the Family pushed on the conventions of the sitcom, Murphy Brown and The Simpsons changed the assumptions of what would be considered to be inoffensive content. Great television does not attempt to mine existing demand; it goes further to take the next step produce demand for a new product. Visionary leaders in television take risks that stay slightly ahead of the market. Backward-looking models are not well positioned to develop future hits.

On the other side come the long-running staples. Chris Anderson described the phenomena of the “long tail,” the sum revenue generated by products not in the head of the distribution.55 Anderson pushed on the distinction between relative and absolute value. A combination of mid-tier products can accumulate the same value as the products at the very top. On-demand video services like Netflix and Hulu work on this principal stockpiling old television series to fill their menu while only producing a few new offerings. Scrubs has been a mainstay of Netflix, in the older television industry; stripped episodes (five days a week at the same time) of The Simpsons were a tent pole. Caves got at the heart of this problem with the ars longa principle—a new media product competes against all stored and reproducible media products, not merely those that are new. An important issue with the long tail is that it does not continue forever, eventually either the cost of storage and delivery for an information product will exceed any possible access revenue or demand will simply drop to zero.56 Which is not to say that there are not fascinating business opportunities in the down-market space. Down-market spaces and social media will be discussed at length in Chapter 3.

Much of the basic content of any given social feed is boring or old. Cheng, Adamic, Kleinberg, and Leskovec have found that low-level news events tend to exhibit recurrent cascades; they reappear and recirculate on the feeds years after they took place.57 The death of Andy Griffith makes fairly regular rounds in the feed despite his death in 2006. Stories that tend to recirculate in this respect are those that are mildly affectively engaging and slow in their initial onset. Real news is a one-time deal, and secondary cascades tied to products like Facebook’s “Memories” would not have the same intensity of something like an election. Mid-level human interest news is the Scrubs of the social feed, interesting enough but not wildly engrossing. When interesting content does come along, it makes sense that Facebook distributes it widely and persistently.

Unlike television products, social products tend to age a bit more rapidly. Everyday comments on news or the weather from a few years back are not interesting or useful; particularly interesting emotional moments can be recirculated repeatedly. What social network feeds have in their favor is sure volume.

The nobody knows principle is becoming increasingly apparent in social media management as well. Some social media companies recklessly change their products without doing diligence to see that the newly formed affective equilibrium is positive. Others maintain their products in configurations that are self-destructive despite repeated warnings. Twitter attempting to make their feed pleasant in 2017 is too little, too late. A visionary leader for a social network firm would provide the basic substance that both users and advertisers want with a little more by way of features that smooth the underlying affective logic of the network. This is not how these networks tend to be managed.

Much like the executives of television, social media executives engage in ham-handed adaptive decision making. Features are added and withdrawn. The whims of Mr. Market are taken as more important than the needs of the actual users. A list of these errors could take several pages; some of these were discussed in the introduction to this book such as Google+ missing the actual nature of privacy or Facebook overreaching with the use of images. One of the most frequently told stories in this vein comes from the fall of Friendster. Before Facebook, Myspace, Twitter, and the rest, Friendster was the king of social networking. Users of Friendster created a number of fake accounts that were both playful and useful as they allowed greater network integration.58 The management of Friendster was less interested in this as it begged the question of the site as a place for friends or people with strong ties. They purged the fake accounts: angering users while simultaneously eroding the structure of their network. Friendster never recovered. Although large social network firms rarely make choices this dramatic with regard to network affiliation and structure, firms make many risky decisions that could easily be the turning point in their demise.

Much like a well-run television network, it is possible, if not likely, that a firm in this industry will arrive at a steady state. It does not take a visionary economist to recognize that demand for advertising products is inelastic. The budgets for buying will not expand to meet the possible slots to be filled. Eventually the average spot price would fall toward zero, or entire classes of advertisements would have no value and others would retain their value. Steady-state media management is unthinkable in a world of monetization. Metaphysically, money is more.

On the topic of artificial demand, when Facebook began to value their video advertising inventory, they considered that every second of viewing would matter to advertisers, and divided this by the number of engaged viewers.59 The quantity of waste viewing is mind boggling. Spare seconds that add up to a lifetime. Surely wasted viewing and fleeting impressions were worth something; counting that remainder is difficult. A spot in the feed is just like a spot during prime time: nobody knows exactly what you want to see.

Programmatic advertising and the hint of arbitrage

Arbitrage is not simply a practice associated with nefarious black hat forums, junk mail styled pages, and Facebook; it is also big business. Safety is important in any industry, risk mitigation is the foundation of academic media industry studies, and arbitrage is one of the lowest risk models.60 This sort of opportunity is not lost on the advertising industry. Agencies established trading desks to arbitrage buying opportunities. If a brand client were promised social placements at a certain price and the firm could secure those placements or clicks at a lower cost, the firm might keep the residual, instead of money being paid to vendors. Why let money flow away? Veteran advertising reporter Mike Shields reported in Ad Week that adoption of the desks was slow as clients were skeptical of the sunk costs and the potential for the appearance of conflicts of interest.61 Research and development are expensive; an ad trading desk needs people and computing power. Building an ad network system is not cheap. This figured to be a great strategy, until the brands opted for greater control.62

Figure 1.1 The flow of advertising exchange.

Unless an advertiser reaches around intermediaries, the completion of their interaction with the public is seven steps away.

At the Digiday Summit in January 2013, Kellogg, a major cereal producer, announced that they had begun working on custom campaigns with demand-side platforms.63 Tony the Tiger could buy ads without agency help. Why can’t you? Many clients are reconsidering the role of desks and even building their own.64 Facebook also sees these arbitrage operations as parasitic with their basic premise, price opacity, being explicitly prohibited in the terms of use for the Application Programming Interface (API).65 Facebook prefers to be transparent. Some established firms like, Ogilvy, have gone the other direction by increasing transparency. Clients are increasingly bold in leaving old relationships, as they already have robust internal creative divisions.66 Creativity is everywhere. There is no shortage of creative talent on the client side; after all they dreamed up this great business that has money to spend on advertising. There is no special sauce that only exists in one city, one office, or one agency.

Within two years, Publicis had disbanded their centralized trading desk.67 Changing Vivaki would improve the client experience. If fees aren’t transparent, clients will stop paying them. A major figure in this industry has defended the practice with the idea that prices were “transparent but not disclosed.”68 One of the best-known trading desks insists that the arbitrage characterization is not accurate. CEO Brian Lesser argues that Xaxis never agreed to provide underlying bulk prices to customers and that complaints based on a lack of transparency are unfair.69 The idea of bulk pricing of online advertising begs the question of online advertising in the first place. If these technologies isolate the intent or demographic profile of individual users on a multiplicity of networked sites, why would the best possible placements be sold on a bulk basis? The firms should be targeting more precisely. In the most positive light, bulk priced buys from publishers would likely be plain display advertisements. There are only so many site sponsorships, and firms selling ad space may be willing to take a lower price to sell larger volumes of inventory upfront. Xaxis has thrived as the other trading operations have waned as they focused on inventory development, rather than momentary opportunity.70 At the same time, the magic is gone. The trading desks pulled back the curtain and revealed Oz, the man.

As buyers would take an increased interest in controlling their ad purchasing programs, new business opportunities formed with the offer of greater control. An important concept for selling inventory is known as “waterfalling.”71 In the waterfall concept, the publisher sequentially offers inventory to possible preferred partners. At the same time, waterfalling causes an old problem to return: latency.72 Progressing from one potential buyer to the next takes time. Some particularly strong publishers might find this to be an ideal arraignment. If the best quality advertising space is sold to strong advertisers, everyone wins as the publisher quickly sells inventory to a reputable partner with reduced risk of arbitrage by intermediaries. For niche publishers or those down market, there may not be an advertising network that provides an optimal opportunity, or the prospect of higher return through an auction process that is more open. Header trading offers an opportunity for sites to compare a few simultaneous offers, often using a second price auction method.73 Opaque second price auctions tend to increase the total value by encouraging higher bids that would clear other bids as the Price Is Right strategy of bidding slightly higher than another bidder would be unavailable. Those involved in header bidding must carefully tune the benefits of opening up their inventory for bids to the damage to the user experience caused by latency—every bidder slows down the load of the site.74 If site load times drag enough, Google will downgrade the site for search rankings.

Advertising firms run from the word “arbitrage.”75 Properly named, transaction facilitation is unromantic. High concept becomes opening price point. Keeping the dream alive takes work, complex public relations, and an ongoing commitment to the fantasy. Amazon debuted the delivery drone to continue the dream logic of Prime, not to introduce the robotic delivery droid.

In the header bidding method, advertisers compete in limited access auctions, capturing some of the benefits of markets without the drawbacks.

In the header bidding method, advertisers compete in limited access auctions, capturing some of the benefits of markets without the drawbacks.

The success of third-party arbitrage firms would make the risk appear worthwhile.76 And there is a risk: building an arbitrage business requires substantial engineering labor to connect as efficiently as possible to both demand- and supply-side platforms. If a firm could routinely scour the major advertising networks for price differentials, arbitrage would be a profitable business. The response has increasingly been to turn away from transparent exchanges, as a third of ads will be on private marketplaces by the publication of this book.77 Good arbitrage opportunities are rare; the time of simple ad arbitrage is fleeting.78 This will become increasingly clear as new programmatic models that decompile the creative text are introduced—these models will produce new advertising on the demand side that reacts to the available supply.79 It would only stand to reason that firms will appear to intermediate new arbitrage models that resell the opportunity to sell the opportunity to deploy a customized ad experience. At the same time, of course this description of arbitrage is limited as it covers only display advertising. At the same time, the business models that end in an affiliate sale are quite similar, especially if those models depend on an affiliate link exchange. Further consolidation in the online advertising industry will also continue to close the space for third parties. The end of the Facebook advertising exchange, or FBX, is the case in point: Facebook can operate on both the supply and demand sides.80 Simple arbitrage opportunities exist organically for tiny windows, during infrastructure upgrades, and when mistakes are made. The appeal of internal arbitrage is that you might stabilize the time frame as you control both sides. Walled gardens where control is complete are the future. One final note, it is important to understand that much of the advertising sold through open markets is remnant—advertising that could not be sold by optimal channels. It is entirely possible that this surplus could be more trouble than it is worth if the technology necessary to sell the final advertisements increases the latency of the page too much for the publisher and advertisers may find their returns on remnant to be null.

Arbitrage is persistent because it works, and, when it doesn’t work, the feeling of arbitrage provides an imprimatur of safety and success. Investors learn arbitrage through stories about simple commodities, especially those discussed in this section, orange juice and pork bellies. Everyday things become special sources of value; the familiar becomes magical. Margins decline with enhanced communication and information access. Prudence dictates that the lower prices will beat higher prices. Walmart wins for a reason. Just as the underlying truth of arbitrage being a simple calculation breaks the spell, the metaphor shifts.

Monetization as resource extraction

A second common usage of monetization describes the extraction of value from audiences. It is no coincidence that searching for terms like “monetization” brings a mix of results for both oil and internet companies. SuperGlossary.com, the seemingly appropriate site for understanding new media marketing terminology, goes as far as defining monetization as extraction: “To extract income from a site. Adsense ads are an easy way to do this.”81 Microsoft uses the same term in advertising a seminar on social media—the audience extracts value from content.82 Microsoft is in the extraction business. The best market position can beat the best product. Monetization in this sense implies the relationship between well-known business processes and already existing legal regimes. Most notably, the use of monetization for patent systems relies on an invention, which for the most part are physical things. What is important in this respect is that the idea of extraction is not premised on the invention but on the preexistence of the value to be captured. If this seems vague, your intuition is right.

Extraction metaphors distance actually existing business process from the act of monetization itself. Extraction typically shifts from the active voice of creating value to the passive voice of finding it. Goldenfeeds, one of many common sites to use the metaphor, accomplishes monetization as extraction by finding patterns of information that would drive sales.83 Value is positioned as already existing, like oil or timber. In panning for golden nuggets, the social network is really just sifting through the river of communication waiting for the right sands. In the American cultural context, the idea of the harvest of oil or gold is akin to a morally righteous form of gambling. Consider the television program The Beverly Hillbillies—a stray bullet causes an oil geyser to erupt and enrich the family during a hunt for food. Oil extraction appears frequently as a path to great wealth with few complications. Money only causes funny problems.

Abundance has a rich life in fantasy. New users are hard to find. Traffic in real human attention is quite expensive. If the new media business were so simple that vast riches were a banner advertisement away there would be turmoil. The arbitrage models described in the previous section are volume games with low margins. Extraction finds something valuable that is already present and sells it for the first time. Unthinkable is the Dutch disease or the resource curse, a theory that poses that a source of free value injected into an economy can cause distortions that damage the recipient.84 Inflows of money can dampen local industries, shift exchange rates, and mute expectations of participation in social development. Dutch disease is a difficult topic to broach as it is so contrary to the aestheticized vision of abundance as blessing. Consider the Norwegian Christmas butter shortage of 2011—popular audiences in the United States were incredulous that a country with such abundant fossil fuels would have a shortage of an agricultural product that they could simply purchase from Denmark.85 Protecting an economy from wealth makes little sense given the dynamics of money in this culture.

Twitter’s slow destruction is evidence of the paradox of plenty; trolls are very heavy social network users, they drive posts and attention, but a cascade of trolls disintegrates a social network. Managing abundance is unthinkable, why regulate perfection? The vision of the infinite, harvestable resource appears as a cornucopia, and in the lingering trace of manifest destiny.86 It would be un-American to suppose that a land of plenty could be economically stagnant. Found money feels deserved.

In crude extraction discourses the thing to be sucked out of the audience is understood to be money. The SuperGlossary definition was quite clear about this—the description moves straight to exchange, no conversation needed. This is about income. In more sophisticated discourses, the thing to be extracted is nebulously named value or attention. While not as crass, this view still depends on the idea that there is a great mass of money waiting to be collected like shells on a shore. In this sense, extraction is similar to, but distinct from, arbitrage. Arbitrage presumes that the businessperson is doing some kind of transformation. In extraction, the value is waiting in piles. Extraction keeps the affective life of the business moving forward.

As the extraction strategy turns from simple claims about free money now toward more advanced demographic targeting and infinite segmentation, it looks less like conventional oil drilling and more like fracking. If we just break apart the social into enough pieces money will just come bubbling out, no business plan needed. Once again the specificity of the business plan is a real downer.

Maps, dates, and two-sided markets: Balancing extractive models

If there is no user, there is no network, and absent a network, no value to extract. Balancing the business process by which the value is extracted with the engagement value of the product depends on the affective quality of the product and the means of exclusion that drive value in the first place. To get a sense of a two-sided market, we should consider the extractive monetization of a simple Facebook post.

For a standard post that simply marks that a user is active, a cadence post, neither a corporate nor an individual user would pay a substantial sum of money. Standard posts that are intended to draw some engagement would still be priced at zero dollars for the standard user and now more than zero for the power user. In the final case, an important post for a regular user would once again be priced at zero, while a corporate user might be expected to pay a substantial quantity of money. Concretely, Facebook benefits strongly when a user posts that they are going to be a parent; this drives interest and engagement. When a company posts that they are having a sale, Facebook does not benefit and perhaps loses some value as the platform appears less intimate. As such, Facebook might choose to extract some value from the power user as they are now in a separate market class from the individual user. Much like in an arbitrage scheme, the unit of analysis is the individual post; in this case we have two entire separate pools of demand. In an extractive model, the revenue secured in the most profitable box must cover the costs of all non-revenue-generating boxes. Paul Krugman used this theory to explain the economic rationale for the closure of Google Reader—a large number of users at a net negative cannot be offset by a large number of users at a low margin.87 Some combination of cost control and revenue maximization will lead an extractive firm to find a sweet spot where the high-demand, high-price side of the market can subsidize the low-demand side.

Figure 1.4 The two-sided market.

If the underlying product is similar, such as the distribution of a post, we can see different potential buyers as two sides of a single market.

This is a conceptual graphic showing the linear system of two different demand curves—those of a corporate user and an individual user. The number of users willing to pay declines dramatically as price increases, the curve on the left would suggest that some users are willing to pay for services, but the market space is exceedingly small. Surely some aspiring celebrity will be willing to pay for the seed on the right of the distribution. The market space for corporate users is much larger. Assuming a static consumer or individual demand curve near the axis, larger the space between the curves, the more likely a freemium business model can succeed. If this assumption is broken by a consumer demand curve moving away from the axis, a subscription business model becomes viable and this is no longer a two-sided market as that term is used to describe social networks. As you can see in the first graph, if user demand does collapse, the network effects will likely collapse demand on the corporate side as well, which explains why most, if not all, social networking products aside from job and date finding are provided free of charge.

For a subscription media business this is a very straightforward model. Consider a streaming service; in order to induce users to subscribe they must offer programming that is more appealing than rival services. This very appealing hook programming is then buffered with lower-quality, less expensive fare. A strong children’s program can be that hook, like Sesame Street for HBO Go. For a social network, the most appealing feature to draw new users is quality content and strong network effects. These are all too often not forthcoming. If a user has a desire for a thing or a connection, an extractive model is possible, although these are uncommon outside of a handful of specialty features and products. For non-advertiser users, there is no special version of Facebook or Twitter. There are special formulations for certain market classes of social networks—enter Tinder.

People enjoy romantic partnership. Partners are hard to find, so people have devised technologies for finding them. Walkabouts, church basements, match-makers, and now social apps connect possible romances. Demand is not really in question here. People are interested either in finding a partner or in the thrill of considering possibilities. Tinder can deliver a free app and then a paid version called Tinder Plus which provides superior service. Further performance can be purchased as a Tinder Boost with up to a tenfold increase in profile view performance during the boost period.88 Tinder can extract value from their users by manipulating the feed to drive interactions that their users seek. The exact balance point where the additional return will be enough for a high enough price is the key. Users of these services are typically sold through the promise of the platform and the particular technologies that drive it. EHarmony promises compatibility based on social research, while Match relies on raw volume and success.89 Dating is a hot market segment; people want to meet singles near them. On the other hand, purely locative products have struggled.

Services in a particular niche may find that maximizing the total user base is less beneficial than a targeted, higher-priced product.

Foursquare was an evolution from other social networks that hinged on the idea of co-location to drive value.90 The promise of Foursquare was that it might connect friends in real time and space; much like the story of the origin of Twitter the affective potential of meeting up is quite real. Communication researcher Lee Humphries described this process of converting ambient knowledge of connection into physical movement as molecularizaiton.91 A molecularized group of social atoms could then be steered to particular locations based on other factors like additional molecular groups of friends or deals offered at other locations. Regular flows of attention were to be produced through a social game of check-ins where the local check-in leader would be declared the mayor of a place. Mayors could then have some social standing in a place and through regular check-ins could become key nodes in different places.

Unlike other networks, the idea of being near other people, especially people you do not already know, can be uncomfortable. Unlike the overwrought privacy crisis that Google+ attempted to mitigate, the idea of strangers tracking you in real time does raise important privacy concerns. The social benefits of mayorship were not particularly enticing—aside from novelty value the local leaderboard does little for ambient awareness of either the social moment or personal social network. A second concept could be more enticing: reviews of key local landmarks. Foursquare could draw attention and traffic from those looking to either place or read reviews. This second product is distinctly a classic advertising play. In any event, these local landmarks have very small advertising budgets. Unlike mass market arbitrage plays, these are very small, specific opportunities. The final extractive business model of Foursquare (and related product Swarm) is as a business-to-business data vendor, relying on their vast dataset of real locations and movement patterns. Access to this data would be sold as a subscription service. This is not unlike other API products like Yummly or Twitter Firehose access which offer different tiers of service at particular price levels. Foursquare can be used as the case study to understand the extraction of value from social datasets that are not easily arbitraged. As a business process a data brokerage is not particularly new or innovative.

The biggest challenge for Foursquare has been the lack of excitement for the platform and the relative simplicity of integrating the product into other technologies. Locative technologies are a secondary feature that is best controlled by the user on a case-by-case basis. This poses a substantial challenge for Foursquare going forward as they have no real claim to value aside from a modest arbitrage model and a data brokerage with little or no ongoing claim for high levels of user engagement. Consider this chart of Foursquare’s value prospects for monetization.

Figure 1.6 Finding Foursquare’s quadrant.

There is no space in this market matrix where Foursquare is alone, and many where actors with stronger network effects provide superior service.

Figure 1.7 Negative interest to value.

If the value proposition (selling change in consumer behavior or conversion) is inversely related to user satisfaction, the model may not be viable.

The biggest concern in this model is that the value to the client for participation is minimal and, in the case of negative customer feedback, it is entirely possible that the arbitrage model would suggest that one might want to avoid engagement with customers on this platform. For Foursquare, the most valuable users would be those who are not predictable and use the software regularly; these are customers who are then the subject of natural experiments in molecularization. Value in this market comes from the down-market segment exclusively. Heavy, loyal users of Starbucks are not apt to change their behavior or preferences. This is a challenge for developing value for this firm as their best features are transplantable to other platforms and their upmarket space is inhabited by users who are not valuable for the platform. The curve for user interest versus value cannot be negative. This is why Foursquare transitioned to an API backbone role: although upside of the market did not form, they could sell user data and capacity as an entirely separate product class.92

The extractive model in Tinder is straightforward and successful, the model in Foursquare less so. Both depend on down-market users to provide the basic feed stock of social interaction. Tinder extracts value from high-demand power users; Foursquare extracts value by building products based on users who may not be extractable at all. Why is Foursquare in this category? There are a number of reasons. Despite a basic arbitrage model for selling advertising, Foursquare had neither a compelling story of vast future value nor a unique lock on this arbitrage product. What Foursquare has is the map and in the later passive check-in versions of the product is a last-ditch attempt to sell a dataset. Two-sided market theory offers a way of reading Foursquare as the opposite of other extractive firms that focus upmarket. There is also an issue of life cycle here; Foursquare is among the older products. If Dodgeball is considered to be a proto-form of Foursquare, it predates Facebook. The promise of alchemy is for companies far earlier in the lifecycle. Firms that tend to provide business services or secure payments from the users themselves are extractive; they have a different discourse and profile than those that arbitrage with the mass media market or alchemic unicorns. The best conclusion for Foursquare is that they never presented a two-sided market model; instead, they were in a dual-product market: a low-yield user-level game and a high-yield business-to-business service.

Over time, extractive models in social media can become confusing for users as they lose track of the actual business process of extraction. Two-sided markets can be tricky. Instead of correctly perceiving that they are chum for sharks, they believe that their attention is valuable in itself—alchemy.

Lead into gold: Monetization as alchemy

The final common formulation of monetization is alchemy, the magical process where useful, dangerous, dense lead is transformed into less useful, less dangerous, ductile gold. Mystery swirls around the alchemist. Media scholar Mimi Ito, in the context of a published discussion with Henry Jenkins and danah boyd, responded to concerns about the ascent of commercial culture in social media with the prospect that participation in labor startups like UberX could be evidence of a more fundamental transformation in the economy, “We’re seeing a complex alchemy of people participating in more transactional versus more community and values-driven ways.”93 Very real concerns about ownership, equity, and participation can be bracketed by the prospect of system changing force.

John Lucker, writing in Information Week, describes alchemy as “companies buy, sell, or trade data for mutual benefit.”94 Isn’t that synergy? The business process of monetization would involve the exchange of the information related to the formation of possible products. The strength of alchemy is that someone else is doing the business. A blogger described alchemy-based monetization as finding something to monetize and then doing that.95 One link to an arbitrage ad page combined the name of a popular media design professor with buzzwords including “alchemy” to drive traffic.

It is most depressing that the alchemy metaphor finds additional credence not on the cluttered pages of a hastily made website, but through the venerable pink pages of the Financial Times. The Alchemy section of the Financial Times webpage was no accident: with the figure of the chemist standing abreast of a background of currency denominations used as arcane symbols and a splash of money green.96 As pink liquid was poured into a new Erlenmeyer flask labeled alpha it becomes gold. Alpha, for the uninitiated, is the glyph for return above reference performance on the stock market. The topic of this page is not social media monetization, but alternative investing writ large. Perhaps the board could have been retitled “Magic Today.” Monetize the monetization. A favorite example company for the alchemy set is Zynga.97

In casino gambling, high rollers who bet thousands of dollars (or more) are known as whales.98 Whales are hard to find. There are only so many rich people who enjoy losing a fortune. Build more casinos; each will have fewer whales. The same is true of virtual goods—there are only so many people who want to spend a large amount of money on badges and in-game playables.99 It is a matter of magical thinking that drives publics to believe that there are either wealthy locals or eager tourists to support their casinos. Zynga, the leader in this market segment, calculates their relative success using a custom metric called ABPU, meaning average bookings per unique: this metric divides total booking revenue by the number of days in the billing period by the number of average daily unique users.100 In very literal terms this divides their income (mostly virtual goods) by the number of people playing per day. This metric has a substantial drawback, as the total number of users plummets the whales continuing to spend can keep the number high or even grow it. Facebook’s early experience with virtual goods is telling; in their first quarter of processing transactions they earned just over one billion dollars from under 2 percent of users.101 This was not sustainable.

This is not to say that Zynga is involved in gambling, but that the underlying market for the alchemy-based market faces different challenges than the extractive two-sided balance. A well-developed customer buying virtual goods is an extremely high-margin revenue source. Virtual goods have almost no cost to produce aside from some coding and graphic design. Structural costs, such as securing users and the overhead of building a social network based game, are persistent. Those users get exhausted. Magically, the users pay directly and repeatedly. In Lucker’s example, the transaction context shifts from the murky world of ad networks and front-running micro-transactions, to the clean, clear world of consumer purchases.

Historically, “alchemy” and “chemistry” were not interchangeable terms; “alchemy” was better than “chemistry.”102 The idea of alchemy as transformation and more specifically as a source of energy can be traced to the Victorian interpretation of Ancient Greece. The figure of alchemy as inherited from that period was an inspiration for those given credit for the refinement of chemistry.103 Phillipe and Newman saw the revival of the idea of alchemy as chemistry as a form of Romanticism.104 Romantic interpretations of spiritual alchemy would provide for seemingly unlimited life, energy, and persuasive force. Alchemy would make you a great public speaker. As an ontological form, alchemy would allow the conversion of one substance into another—giving publics increasingly jolted by the rise of scientism a way of understanding themselves to be the real, spiritual, and substantive. Given the context of Romanticism the idea of alchemy as fraud would not challenge the context—alchemy is seductive because it supposes that some part of your body—be that your physical self or your idealized golden Facebook tongue—is worth something.105 It wasn’t that the Victorians were looking for the secret formula to manufacture valuable metal—they were looking for a way to remake their world as a dream.

Alchemy calls for simplistic direct transaction business models combined with a romantic aesthetic as magic. This differs from arbitrage and extraction in both aesthetic sense and business practice. Just as extraction discourses decline to include the resource curse, the idea that there might be too few transactions is bracketed as well. This is not a cognitive error or positivity bias, but an underlying feature of an economic world. Pure monetization, effervescent more, the core concept of money comes to fruition in the alchemic metaphor.

Extraction, arbitrage, and alchemy in the mass market

Facebook uses each metaphor in different ways. The roadshow video used extraction. Clients can access new levels of data from the social graph. Facebook for a time subverted this value through throttling how many users could be reached via free status through a program called EdgeRank. Pruning the newsfeed was intended to improve the experience, bringing the user content they would really enjoy. EdgeRank and its descendants are discussed in a number of places in this book; it is fair to say that Facebook would prefer to be in charge of extracting and refining value from their user network—not their clients or, worse, trolls. Facebook’s curious advice for advertisers to develop large followings on their platform should be understood in that context—Facebook understands that it develops value when it can control who advertisers get access to. Over the years, Facebook has been more willing to allow users to increase the volume of content flowing through their feed. This does not mean that advertisers have gotten back their once-lucrative direct access to their publics.

The roadshow video’s deployment of more conventional marketing mix discourse and case studies captured the power of the arbitrage metaphor. When the CMO of Diageo proposed that targeted Facebook advertisements increased sales for Captain Morgan by 20 percent, Facebook made a clear argument—a well-targeted campaign on their social network has a similar conversion rate to that of a Super Bowl ad. Once combined with the power of an interface and a database system, the appeal should be clear: it wasn’t that Diageo had well positioned their brand but that there was something magic about this new kind of advertising—that they were able to get something more from advertising that would already be taking place.

The hoodie is the magic cape of the twenty-first century. What Facebook lost in detail they gained in style. The introduction of this book opens with a reading of Facebook’s Magic Maps, the dark worlds that are filled with light by the virtue of Facebook alone. The fantasy of the alchemist is the same as that of the planner and the same of that of the website designer. Through the particular logics by which Facebook operates users have found that they can transform their images and lives through the careful editing; they can make something completely new. This is not the world of middle class anxiety that would suppose that Facebook is a dangerous world racked with social change, but a carefully created romantic dream space. Social media provide important emotional resources for their users. Facebook is not a distraction or a nuisance. If anything, social networks provide users with important sources of social support. danah boyd argues persuasively that teens use social networks to fill their basic social needs when they can’t access physical sites for socialization.106 Much like the story of the oversimplification of money by early twentieth-century media sociology, the flattening of the actual use of social media should be avoided. Activity in the continuation of distant relationships and kin-keeping is the replacement of dull passivity with activity. Facebook finds real emotional connections and somehow profits; sans a secondary plan this may be the most important form of alchemy of them all. Unlike other social network firms, Facebook is willing to allow their core product to develop out of sight of market demands. Twitter, on the other hand, was not so fortunate.

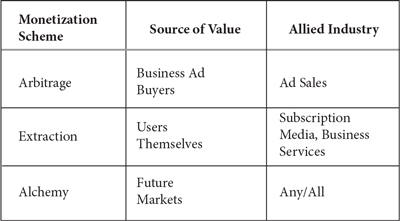

To this point, the taxonomy of monetization schemes looks like this:

Figure 1.8 Monetization matrix.

The following sections will discuss the idea of the graph, and the specific manifestations of the graph concept presented by Facebook and Twitter, followed by the great difficulty in understanding how Pinterest is positioned in this system of relationships.

The graphs