FIGURE 6.1. Massachusetts bill of credit, February 3, 1690. Source: National Numismatic Collection, National Museum of American History, Smithsonian Institution.

CHAPTER 6

The Constitutional Approach to Money

MONETARY DESIGN AND THE PRODUCTION OF THE MODERN WORLD

Christine Desan

Money objectifies the external activities of the subject, which are represented in general by economic transactions, and money has therefore developed as its content the most objective practices, the most logical, purely mathematical norms, the absolute freedom from everything personal.

(SIMMEL [1907] 2004: 128)1

[Gold coin] ceased to be recycled through the economy and was fossilised in great royal hoards, which were … all too often seized by rival kings with great violence and bloodshed…. The pages of Gregory of Tours drip with blood and gold, but it was gold not in circulation and use, but clotted and hoarded.

(SPUFFORD 1988: 15, ON THE DECLINE

OF THE FRANKISH EMPIRE)2

For as bills issued upon money security are money, so bills issued upon land are, in effect, coined land.

(FRANKLIN 1729: 24)

“IT IS A POWERFUL IDEOLOGY OF OUR TIME,” wrote Viviana Zelizer in 1994, “that money is a single, interchangeable, absolutely impersonal instrument” (Zelizer [1994] 1997: 1). According to that intuition, money’s character has transformed modern life. As Georg Simmel argued in The Philosophy of Money, first published in turn-of-the-century Germany, “The money economy enforces the necessity of continuous mathematical operations in our daily transactions.” That characteristic pervasively affects the lives of people—they spend their time “evaluating, weighing, calculating and reducing … qualitative values to quantitative ones” (Simmel 2004: 444). As Simmel described it, “the commercial treatment of things” becomes preeminent. Money can be liberating: it frees people from the relations of mutual obligation that characterized more informal credit relations. But money is also alienating: as it dissolves dependency, it also renders reciprocity irrelevant. Material culture flourishes, but the social sensibility and moral judgment that could make sense of it falters. Social theory by scholars like Talcott Parsons, James Coleman, Anthony Giddens, and Jürgen Habermas reiterated Simmel’s argument in the decades that followed (Simmel 2004: 445; Zelizer [1994] 1997: 1–2, 10–11).3

Despite the evocative power of Simmel’s intuition, Zelizer noted that it failed fully to capture the modern experience. Her argument was arresting. Rejecting a century of sociological writing, Zelizer demonstrated that ordinary people constantly disrupt “monetary uniformity.” Most notably, they “earmark” the apparently homogenous money made by the state, creating conventions of use that compartmentalize money in myriad ways. The woman wage-earner sets aside supplemental income as domestic “pin” money; the beneficiary of a payment ending a feud refuses to use that “blood money” to pay for life’s ordinary expenses; a family establishes a special bank account to hold money saved for college tuition (Zelizer [1994] 1997). Zelizer’s pioneering work opened up a field of study. Scholars have found that people embed and organize money—officially an abstract and fungible item—in ways that differentiate its sources, uses, and meaning (Velthuis 2005; Healy 2006; Fourcade and Healy 2007; Singh 2013; Bandelj et al. in chapter 2 of this volume; Morduch in chapter 1 of this volume; Wherry in chapter 3 of this volume).

The constitutional approach to money shares Zelizer’s target—the notion that money is a “single, interchangeable, absolutely impersonal instrument.” Rather than coming at money from the outside, however, the constitutional approach comes at it from the inside. Viviana Zelizer assumed that money is an apparently colorless object in order to show how people infused it with personality when they manipulated it. The constitutional approach asserts that money is colored from the start. Money has never been an “absolutely impersonal instrument”; it has never approximated Simmel’s pure form. To the contrary, money has an internal design: societies produce it by structuring claims of value in ways that make those claims commensurable, transferable, and available for certain private as well as public uses. That architecture, in all its intricacy, determines the way money works in the world. Moreover, that architecture varies. As societies change the way they engineer money, they change its character and the market it makes.

The claim that money has an internal design contradicts a tenet basic to modern economics. According to that discipline, trade in real things produces the market—and by real things, economists mean stuff you can “buy, sell, and drop on your foot” (Blyth 2002: 127, quoting the Economist). Money by contrast has only an expressive role: it supplies a term that people use to estimate and compare values, but it does not affect the substance of the trade. Money makes exchange easier, to be sure, but the relative prices that people assign to goods (and services), and the allocations of labor and capital that result from competitive markets, remain the same (see, e.g., Morduch in chapter 1 of this volume, and cf. Tobin 2008: 10). Indeed, much of modern equilibrium theory is built on the assumption that money is a neutral factor. Otherwise, the kind of money used would affect the outcome at equilibrium.

That possibility—that the kind of money used would affect the outcome—opens up a very big can of worms. If societies design money and that design affects prices, then we cannot coherently conceptualize general equilibrium as a trade among individual and independent agents. Rather, the collective processes that make money—processes that involve political, social, and conceptual practices—are relevant and require including in the model. In fact, we may not be able to use the model at all; perhaps casting the competitive market as a giant and instantaneous auction over goods and services misstates economic exchange altogether.

So we return to Viviana Zelizer’s initial observation. The ideology that defines money as “a single, interchangeable, absolutely impersonal instrument” is powerful indeed. First, it produces an approach to modernity in much of social theory, including sociology, that obscures the way people animate money and the market with meaning. Second, the ideology informs a discipline—economics—that neglects the collective processes underlying money creation, conceptualizing the market instead as “multilateral barter” between free-floating actors who express price in a neutral technology (Tobin 2008: 10). That oddly contrived paradigm (and ideal) informs the discipline’s prescriptions for public policy and human well-being. Given its influence, money’s modern ideology deserves critical analysis both from inside and from out.

Balancing Zelizer’s approach to money from the outside, in the next pages I suggest how we might look at money from the inside. I describe, first, the challenges that societies confront when they begin creating money and how they engineer solutions at a constitutional (small “c”) level—the level that configures public authority and its relationship to individuals. The next section samples design decisions; it compares the monies made in medieval England and in early America on several key elements of design to highlight their impact. The last section contrasts those methods with the modern money first produced in late-seventeenth-century England. That money, radically revised from its predecessors, arguably inaugurated capitalism as a market form. Far from being a neutral or abstract matter, money deeply conditions the exchange made in it. The chapter concludes by circling back to the ideology flagged by Viviana Zelizer at the outset: part of money’s modern design operates precisely to render its influential work invisible.

The Constitutional Approach to Money

In most modern explanations, money is a matter known by its functions: it is the unit of account, the medium of exchange, and the mode of payment used in a society (Levine 1997: 690–703).4 Having identified what it does, few accounts ask what money is. If they do, they often hypothesize a moment of origin, one that identifies money as a commodity or a convention inaugurated to ease exchange in the mists of time (Samuelson and Nordhaus 1973: 274–76; Timberlake 2013: 4–7).5 The accounts end there, as if once discovered, money is simply captured and released. It continues in the modern world and across many different communities with little else than inertia to recommend it.

In fact, societies engineer money rather than discover it.6 Their work is constant and collective, a matter that involves both public initiative and individual decision making. The reason that money requires careful construction becomes clear once we take another look at its astonishing capacities. Money’s function as a “unit of account” sounds, at first mention, like a simple matter: we choose an abstract measure, like an inch or an ounce, but one that measures value rather than length or weight. Yet on further consideration, the challenge is evident. An inch represents, in fact, a substantive length; it can be transposed over space. An ounce represents a substantive weight; it can be compared across matter. But what is the substantive value captured by a dollar, one that convinces people with different needs and means to understand it as a common measure? And how, if they do, can it be applied to assess goods, labor, and even time?

The mystery is compounded by considering money’s other capacities. How does a measure transfer value from hand to hand, delivering it unconditionally between strangers and those who will never meet again, as well as friends or partners who can reciprocate at a later time? Why should people trust a coin or a token, let alone a note or the transfer of a reserve between banks? If money’s value depends on how it is used in exchange, how does the unit of account instantiate worth to start with? How far does money reach as a mode of payment? Can you count on a coin to take you across a foreign land, accepted at face value rather than analyzed for its worth in metal or another currency? And how can societies effectively expand their money supplies if money is a commodity or a convention?

The mystery evaporates once when we consider money as a practice orchestrated among a group to produce just the functions that economists assume. Consider, first, a community’s motivation to create money. Economists imagine individuals bartering awkwardly across barriers—but communities have a much harder time operating without money. They could conceivably collect, store, organize, and distribute in-kind contributions in order to mobilize armies, build infrastructure, enforce laws, and manage the complexities of the modern welfare state—but it would be enormously difficult. Governments magnify their ability to mobilize resources when they produce a uniform medium to use both when they spend and when they take in revenue. Money is, at an elemental level, a governance strategy.

Just as they have particular motivation to create money, communities have an unparalleled capacity to do so. Polities depend on the contributions of members—taxes, tithes, fees, and other payments—to survive. Those communities that use money have invented a way to assess and certify those contributions with a unit, creating a unique marker of commensurable value as they go. Commonly, officials recognize contributions given early with tokens, giving them out like receipts. The receipts hold value because officials agree to take those tokens in lieu of further work when communal contributions are due. That is, authorities spend by allocating units for the kind of goods they need from people and tax back units in the same measure. Officials can make the strategy sweeter for everyone if they agree to take back the tokens from anyone’s hand. That commitment makes the tokens transferable: people can pass them on for value, and others can take them, confident in their value to pay off obligations due to the polity.

“Money” made by such a strategy entails substantive value that is recognizable to each person who owes debts to the community or who deals with those who do. Because taxes epitomize such obligations, we can say that the arrangement confers “fiscal value” on the unit. But money is more than a fiscal device. Its quality as a medium of exchange between individuals adds to its value. Money gains a “cash premium” because it has an exclusive appeal; it operates between individuals when it is accepted by a creditor common to all of them and endorsed for travel in the meantime. In the end, money holds value for paying off obligations due to the public (fiscal value) as enhanced by its worth as the most liquid resource individuals can hold (the cash premium).7

Unpacking how societies identify a “unit of account” and enable that unit to act as a “medium of exchange” illuminates money’s character. We can understand why and how groups would invent money again and again in different places and ages: it is an ingenious and attainable mode for organizing a community. Moreover, we can understand why and how individuals would appropriate money for their own use: it is uniquely efficacious in facilitating exchange. Indeed, money’s capacities build on each other: a group (or those acting for it) could decide that money made for public purposes becomes a stronger and more acceptable device when it furnishes an effective medium for individuals in private life.8 They will take the community’s token more happily, attribute more value to it, and extend its use to more occasions.

Money’s function as a “mode of payment” follows. Economic accounts often assume that exchanges between people are arms-length and final, cleanly allocating goods and services. The anthropological record, by contrast, suggests a dramatically different world—one of relation, reciprocation, and enmity; family and clan; gift, repossession, and outright theft (Graeber 2012: 21–41). In light of that rich mix, making an item work as a mode of payment cannot be taken for granted, any more than creating the other capacities of money. But public authorities can set their unit apart from all others by privileging its use as the only enforceable way to pay: if public tribunals recognize the official unit alone as the way of settling debts and other obligations, it will become the means of choice. Doing so allows officials to endorse certain exchanges and not others, to condition deals, and to police commitment. In other words, it allows them to make a market in the image they ordain. At the same time, individuals gain the backing of the group for those deals it finds acceptable. Again, we can see how money’s innovation would bring the public and private worlds together.

The constitutional approach to money makes sense of money’s early history in England. Money appeared there with political authority; that circumstance and the activity of individuals supported its increasing use in everyday exchange; markets grew in the units demarcated and enabled by sovereign tribunals.9 The constitutional approach illuminates as well money’s reinvention by European settlers in early America. When imperial officials left colonists short of specie, those provincials creatively engineered replacements: they constructed money out of tax credits, allowed it to circulate, and enforced its use in local courts (Ferguson 1953; Brock 1975; Grubb 2016).

As much to the point, the constitutional approach explains money’s modern identity and operation. The dollar is no simple commodity or convention—it is a sovereign liability, institutionalized in concrete ways and recognized at law. The United States spends in a unit that it accepts as a set-off against obligations to it, primarily taxes. In turn, the government privileges the dollar’s passage between individuals and the state, and enforces its use in the tribunals that order private exchange.10 Other sovereigns also engineer domestic money as a sovereign IOU and work to enable its other capacities (Goodhart 1988; Bank for International Settlements 2003: 102–3).

The analysis can be expanded. While this chapter focuses on states and governments because of their stature as the dominant monetary engineers in so many societies, other collectives can make money by establishing stakeholders for their members and innovating a unit. But the job is a complex one, generally done by anchoring demand for a medium by collecting regular contributions in it and enforcing its use within a payment community, among other enabling acts. A constitutional approach could help us sort out the extent to which Bitcoin and other alternative payment regimes achieve status as “money” and how they do so (see Dodd in chapter 14 of this volume; Maurer in chapter 13 of this volume).

Recognizing that each of money’s capacities is a matter orchestrated among a group opens up a world of design previously obscured. Every engineering challenge identified above—taxing and spending to create a commensurable unit, supporting money’s private use as a medium, enforcing it as a mode of payment—can be institutionalized in different ways and by different actors, legitimated by diverse methods, reinforced with various strategies. For example, money creation can be the prerogative of a monarch who controls all issues, or it can be a matter mandated to a democratic assembly that allocates spending and taxing according to electoral results. Sovereigns can charge individuals for money’s creation, or they can subsidize it out of general revenues. Societies can advertise their commitment to withdraw the tokens they issue (and so support their value) by various means, each of which changes the standing of those holding money. Some polities give people collateral: the commodity content of medieval coin suggested (although it did not ensure) the stability and reliability of political authority. By contrast, modern polities often issue new cash on the basis of government debt: the obligation to repay government debt, an obligation policed by public creditors, functions to promote taxation that retires the newly expanded currency.

The variations above fuse political authority with certain monetary forms, distribute costs in ways that shape money’s value, and build regimes of commitment that condition individual property. Other variations determine access to money and the shape of the market itself. Thus communities can stratify the way money circulates by configuring its denominations and patterns of issue. They can enforce money’s use to purchase very few items—food, perhaps, but not land or labor. Or they can recognize money as a method that transfigures people into commodities, endorsing slavery and slave markets.

The examples are real ones, drawn from the repertoire of monies made in the Anglo-American world over the past several centuries. The basic point is straightforward. Money is a complex project, one that creates and maintains a common resource held by individuals. The effort configures public authority, its relationship to members of the group, and the way people relate to each other. It defines what can be sold and what cannot, as well as the way we conceptualize the market. The next pages compare a few of the design decisions that have distinguished monies and the communities that made them.

Communities face design decisions from the very outset, the moment they decide to create a unit of account. They have represented those units in many ways—silver, paper, or entries in an accounting ledger. At first glance, money’s content seems to be an issue of form alone—but the choice matters because it molds how money enters circulation. It can also affect the legitimacy of a system; a regime offering silver coin may require less trust than one offering paper notes, for example. Each kind of token produces different side effects as well, from the way people conceptualize money to the way they negotiate it across borders. An issue that appears merely technical, in other words, actually shapes interactions over value. Comparing the silver pennies of medieval England with the paper bills of early America provides an example.

Recall from above that a group can create a unit of account by issuing it to mark contributions given early and taking it back later when the bearer offers it in lieu of a contribution otherwise due. The principle of equivalence between units issued and units redeemed—credits created and credits canceled—is the magic that constructs a measure with substantive and uniform value.11 That is the reason the unit of account can be represented by anything, from a coin to a bill. But the system will work only if the equivalence is credible. The promise of fiscal value fails if people holding the units can multiply them without authority and flood authorities with counterfeits. Problems also arise if the units fall apart or decay, leaving people without evidence of their claim. Finally, units that circulate physically internalize their own verification, a great advantage in many societies including (still) our own.

Under the circumstances, making money out of a precious metal is a promising strategy. Those acting for the community can monopolize the critical ingredient more easily, given its scarcity. It is durable and yet difficult to refine. Early English sovereigns set up mints where they produced coin that was distinctive and hard to replicate. They imposed taxes in coin, requiring their subjects to scour the land for silver, bring it in for minting, and pay their dues in pennies. Accounts that assume money evolved out of barter imagine subsistence households putting aside quantities of silver or gold until it becomes a shared medium. In fact, monarchs made money out of metal not because it was common but because it was rare, hard to work, and almost impossible for ordinary people to assess (Desan 2014: 52–58).

The system tied money conspicuously to the sovereign. English rulers centralized authority as they centralized minting, advertising their power on the face of the coin (Mayhew 1992). Traditional sources from Roman law to a canonical English case in the early seventeenth century located power over money as one that “inhered in the bones of princes” (Case of Mixed Money 1605: 118). The practical and ideological effects shaped high politics across Europe, which turned on elite efforts to control royal authority over commodity money. Kings could deploy debasements to raise revenue given the way coin tied together commodity and currency values (Bisson 1979; Spufford 1988: 289–318).

At the same time, the metal content of money gave those holding it a kind of collateral. Commodity money identified stability with a natural item, a material guarantee. That security may have been particularly important in legitimating royal rule early on. Should a regime fail and, with it, the counted quality of money, people would still hold its commodity value if not its monetary value.12 Short of that rather desperate end, the system implied a connection between political stability and the physical content of money. Medieval thinkers did not separate money conceptually from the sovereign as do modern theorists who divorce “market” and “state”—but money’s identity as a material commitment may have informed the medieval approach to politics as a matter ideally static rather than productive, balanced and ordained rather than participatory.

The same identity may also have constricted European approaches to money (and politics). As Adam Smith and others famously note, the fact that English monarchs made coin out of full-weight silver and gold severely limited its supply for centuries (Smith [1776] 1937). European kingdoms struggled to attract precious metals to their mints; the competition regularly destabilized exchange and drove the harshly extractive efforts of early colonization. At home, the value of pennies remained high. The scant supply of fractional change left many of the most ordinary purchases—a cup of ale or a piece of cheese—below the monetary floor. Exchange separated into circuits; people at the bottom used credit pervasively to get by, a practice that pervaded village life with opportunities and risks (Sargent and Velde 2002; Desan 2014).13

In fact, chronic scarcity of coin was the phenomenon that triggered money’s redesign in early America. As we have seen, money with commodity content—coin—was a strategic decision about how to control the path of money’s flow in, out, and around a society. Neither trivial nor technical, the method had political, social, and conceptual consequence. Early Americans had no option to repeat the experience. The mercantilist policies of the British Empire, including the unfavorable terms of trade experienced by the colonies, drew specie relentlessly back to the mother country. Left without a sufficient circulating medium, Americans invented their own (Mather 1691; Franklin 1729).

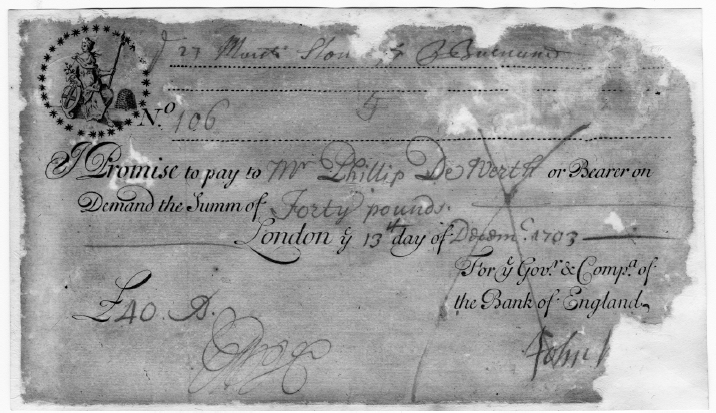

Bills of credit were provincial IOUs written on paper, first issued by assemblies to pay soldiers when colonial coffers were empty. The notes stated a face value in traditional English denominations—two shillings, for example. The notes promised to be acceptable instead of coin when the soldier—or any bearer—needed to pay provincial taxes. Secondarily, the colony pledged to swap the bill for “any stock” in the colonial treasury—but that promise was negligible. The text’s qualified tone accommodated, perhaps even advertised, the fact that the colonial treasury would remain empty of silver and gold coin. In other words, a bill of credit created a provincial liability in a particular unit of account that would be set off against an individual’s debt to the colony (Ferguson 1953; Brock 1975; Grubb 2016) (fig. 6.1).

FIGURE 6.1. Massachusetts bill of credit, February 3, 1690. Source: National Numismatic Collection, National Museum of American History, Smithsonian Institution.

Again, the system tied money conspicuously to the party that issued it, but here, the connection recast sovereignty in remarkable ways. Provincial assemblies were acting for the settlers, but they were subordinate to royal governors in imperial theory. Over the course of the eighteenth century, that would change, influenced in part by the expanding American claim to make indigenous money. When colonial legislatures asserted that authority, they drew power away from the governors. After all, the assemblies’ new role, spending notes into circulation, allowed them to control appropriations as well as levy taxes. Their activity put them at the center of provincial life as they increasingly determined the political economic course of their colonies. As one royal governor put it, “They that have control of the money will certainly have the power; I take the single question on this head to be, whether the king shall appoint his own governor, or whether the House of Representatives shall be governor of the Province” (Spencer 1905: 110, quoting Jonathon Belcher, governor of Massachusetts, 1733). The answer was increasingly clear to settler elites; they aspired to larger and more significant governing roles. Americans more generally began developing notions of self-determination (Greene 1972).14

Bills of credit carried no material collateral, unlike commodity money. Rather, legislators represented the security of money in other ways. Cotton Mather, an eminent figure in Massachusetts, the colony that pioneered paper money, published a pamphlet propounding the logic behind it. It was propaganda in favor of the new currency, an argument that emphasized taxes as a sacred and collective duty (Mather 1691). Officials reiterated by statute and in statements that they would burn money brought in, upholding the pairing of credit issued and credit canceled that underlay the IOUs.15 While the monetary systems of medieval Europe suggested an ideal of natural political balance, money creation in early America directed attention to the sound fiscal functioning of the province.

The system created other corollaries, practices that fused monetary, political, and economic experience. Perhaps most notably, money became an electoral issue. Provincial voters mobilized around campaigns in favor of money’s expansion. Legislators now controlled access to easy money, and proponents often pitched their arguments in class terms, castigating the rich for hoarding specie and cash (Dialogue 1725).16 There were also opportunities for change at the level of the everyday economy. Assemblies issued provincial notes in many small denominations, like pence and shillings, for example. That innovation lubricated petty exchange in many American colonies, thus resolving the mundane but devastating problem that had haunted the medieval world (Hanson 1980: 411–20).

Unpacking money from the inside demonstrates that currency is a matter of constitutional magnitude. The medieval English and the early Americans differentiated their worlds according to the way they constructed their unit of account. And that decision—to build a penny out of silver or paper—was just the beginning. Each group developed its monetary order on the basis it had designed. As each extended its system, it continued shaping exchange and the conditions around it. A last example briefly conveys the dimension of the effect.

The strategies described above created a core for the monetary system, a set of units that entailed substantive value for fiscal payments enhanced by the premium they held to individuals as cash.17 Communities could limit their money supplies to that minimum, issuing only the amount of money necessary to finance public activities; the credit unit of the Sumerian temples may have been such a money (Graeber 2012: 38–40).18 But since money has value to individuals as well as the public, communities could also decide to innovate supplementary monies, opening streams that added to the money stock because of private demand. Both medieval English and the early American chose to do so, and their methods further characterized their systems.

“Free minting,” the means engineered by the English and many European polities, traded on the fact that when people wanted more money, their demand would be acted out in the price level. Sellers valuing the ease of transacting in coin would lower their prices in pennies, and buyers would conclude that holding coin was better than holding an equivalent amount of raw silver. The rise in pennies’ purchasing power would bring people to the mint with bullion, ready to buy coin for their own use even at a fee and in addition to what they might need to pay taxes. The mints complied, supplying coin “freely,” at least in the sense that they bought as much bullion as people brought to the mint. The system posed no problems for the sovereign because as minting sated private demand, prices in coin rose. At a certain point, people would decline to take more silver to the mint, preferring to keep it rather than buy coin. The system thus shut off any oversupply the moment that private demand ceased to sop up extra coin. The government lost nothing because its tax revenues retained their value; meanwhile, it supported popular desire for easier exchange.19

But the system produced very selective results, only suggested here. On the one hand, it reinforced European competition for the precious metals and, perhaps, the mercantilist mindset that prioritized their possession as the sine qua non of wealth. On the other hand, free minting appears never to have produced an adequate money stock. Individuals had always to procure valuable bullion in order to get more coin, and few besides merchants could make that work. Moreover, the method imposed the costs of enlarging the money supply on individuals rather than defining money as a resource that the public should finance, a strategy that failed when the benefits to individuals were less than to the group. Supplementary money succeeded, in other words, but in ways that fed important patterns and problems in the medieval world generally (Cipolla 1963; Spufford 1988; Mayhew 1995).

Compare the early American approach to supplementary money. Colonists innovated an additional inflow because public spending in the provinces—and therefore paper money creation—occurred only episodically, mostly for reasons of defense. When a war or military effort wound down, taxes would contract the money stock. As people ran short of cash, prices would often drop, skewering debtors who scrambled to repay obligations in currency that was worth more than when they had borrowed it. Thus provincial authorities improvised an approach to supplementing the money supply in the absence of public spending: they offered bills of credit to inhabitants who might like to borrow them. The idea had been floating around since the mid-seventeenth century in Massachusetts, drawn from earlier English sources. Provincial governments could establish land banks that lent paper money on the security of land, with interest and principal repayable in the same bills. Individual demand would pull money into circulation independent of a colony’s fiscal needs (Lester 1938; Ferguson 1953: 168–71; Thayer 1953: 148–52).

Where the medieval supplementary system necessitated the acquisition of bullion, the American strategy linked money creation to land. The shift had ideological and distributive implications. It recognized, first, the agrarian bases of settler culture, prioritizing the resource prized by many as their route to independence and well-being. Second, the system empowered a much wider swath of lay people to supplement the money supply by their actions. Records from the Pennsylvania land office indicated that 75 percent of those who took out loans in 1774 were yeoman farmers; many of the rest were mechanics—including shoemakers, blacksmiths, carpenters, and millers (Thayer 1953: 155). More generally, legislators could shape access to loans according to an array of governing principles. They assigned the authority to make loans to towns, counties, or provincial bodies; they set ceilings on loan amounts and therefore enforced the spread of funds; they established policies on the amount of security required, interest levels, enforcement, and foreclosure procedures (Thayer 1953; Brock 1975: 70–71, 77–84, 87–99). As provincials worked out their approaches, land banking added to their power and ambition. That development, along with constant controversies over enforcement and implementation, led to ferment at home and, ultimately, fed discord in the empire.

When the medieval English or the American colonists extended their systems, they were working in a constitutional register. Their strategies for making supplementary money altered the roles of individuals, the access of those people to credit, and political features in their governing systems. It turns out that making money was a project continually under way and constitutive of basic relations in those societies.

Money Design and the Production of the Modern World

In fact even as the Americans innovated paper money, the British were radically reordering their system. Their monetary revision institutionalized capitalism: it put the self-interest of commercial actors at the heart of money creation and established the networked liquidity that supports modern finance. The development took centuries; indeed, as the 2008 financial crisis taught us, it is still ongoing. But we can get a rudimentary sense of the redesign from the same elements considered above—the strategies adopted to create and to supplement the unit of account.

A new approach to creating the unit of account in England appeared at the end of the seventeenth century. The technique innovated at many levels: it changed the parties involved in money creation, their pay, motivation, and legal rights. Once established, the method would spread across the globe (Goodhart 1988; Bank for International Settlements 2003). But reduced to its basics, the story was deceptively simple.

It began in wartime, when the English government was short on funds and very long on need. England’s robust tradition of full-weight metal coin ruled out severe debasement as a legitimate strategy for raising money. By contrast, the English had experimented for some time with different forms of public credit and, in 1694, king and Parliament converged on a scheme to borrow £1.5 million from a group of investors. So far, so familiar—but this time, the government agreed to charter the investors as the Bank of England. Rather than taking the money it had borrowed in gold or silver coin, the government then accepted its loan in the form of Bank of England notes. The government thus held promises-to-pay specie issued by the Bank (fig. 6.2.).

When it spent, the government paid people with the new banknotes. Those people now held a promise-to-pay that they could redeem at the Bank of England for coin. But the government added several properties to the paper. First, it made the paper transferable. Holders could use banknotes to pay each other; anyone holding a note could take it to the bank for face value.20 Second, sometime in the following years, officials agreed to take banknotes back in taxes. After all, authorities had been spending in the notes; it would have undermined the legitimacy of that payment if they refused to take them back again (Desan 2014: 311–20). Further, the government owed the Bank of England for the loan; it could return the notes to the bank to pay off its debt without any inconvenience.

By that mundane and possibly unintended route, the worldly magic that makes money (in the elemental sense of creating the unit of account) occurred. The government had engineered a way to put IOUs into circulation and withdraw them later. No recourse to gold or silver coin was necessary. Anyone holding a banknote was also holding a government liability; he or she could simply return it to cancel his or her own obligations in taxes or other fees. By borrowing from the Bank of England—the first lasting “bank of issue”—the English government could effectively expand the money supply. Central banks today create “high-powered money,” also called the monetary base, in essentially the same way.21

But while the English had replicated the old magic (creating units of credit and then canceling them), their method was novel. Authorities for the first time shared their monopoly over money creation, and they chose commercial actors as their partners. Medieval sovereigns in England had controlled minting; American legislatures had directed the issue or loan of provincial paper money. By contrast, the English government now borrowed from a group of investors and spent the notes that group produced. Thus in order to create money, the government depended on the profit calculus made by the directors of the Bank of England.22

FIGURE 6.2. Early Bank of England note with a visible promise-to-pay. Source: Derrick Byatt, Promises to Pay: The First Three Hundred Years of Bank of England Notes (London: Spink, 1994), 19. Courtesy of the Bank of England Museum.

Second, the government now paid rather than charged for money creation. As we have seen, medieval sovereigns had imposed a fee at the mint. American legislators had spent bills of credit at face value and taxed them in later, effectively obtaining an interest-free loan.23 Governments could justify the charge because they were, in fact, supplying a resource they had the singular capacity to create—a circulating unit with substantive and commensurable value relevant to everyone (Desan 2014: 48–50). But now, the English government borrowed in notes from the Bank of England, granted those bills the capacity to circulate and be received for taxes, and paid the Bank for the package deal.24

In just the same period, English attitudes toward self-interest shifted. Religious and moral discourse had condemned greed and material striving for centuries. The ascendance of these qualities to status as legitimate motivators drew from diverse sources—but money’s redesign literally put the state’s imprimatur on lending at interest. The new method identified that kind of profit, called usury in earlier days, with patriotic action that benefited the public because as they lent, investors supported the government and created a circulating medium—the new money. The practice grew from earlier experiments at borrowing, first in the form of government bonds that could circulate. George Downing, Charles II, and others had appealed to public creditors as early as the 1660s as citizens who helped the polity while reaping material rewards at the same time (Desan 2014: 250–51, 279–81; State of the Case 1666).25 The Bank of England’s promoters picked up and amplified that pitch. Its members were “under this happy circumstance,” one pamphlet announced, “That they cannot do good to themselves but by doing good to others” (Godfrey 1695: 304, italics in the original).26

In a related development and within a few years of the Bank of England’s chartering, English law on public obligation also changed. In The Case of the Bankers, the House of Lords expanded the rights of public creditors, securing their claims in case of sovereign default. Because taxpayers were (and remain) on the hook to repair such default, the unprecedented law strengthened the position of those holding public bonds relative to a more diffuse public (Case of the Bankers [1696, 1700] 1812).

Although many details of the design remained undeveloped, the English had installed a modern motor at the heart of exchange. When they established a national bank as the source of money, they communicated the logic that would come to characterize capitalism. Rather than a sovereign ruler or a legislature, the market and its experts would determine the pace and purposes of money creation. Indeed, the ascending culture of a powerful and increasingly commercial market fairly compels attention to the issue of private demand, the issue that moved both medieval sovereigns and colonial legislature to extend their systems. I look at that design decision last.

Like their counterparts, the architects of modern money engineered a way for individuals to supplement the monetary base. The government allowed the Bank of England and, in turn, commercial banks, to lend to private individuals and businesses by issuing notes that promised-to-pay the official unit of account on demand. Because they issued notes in excess of the coin they held, the bankers were de facto creating cash, not only collecting and advancing existing funds. The practice depended on an accumulating number of supporting rules. The government enabled the notes to circulate easily.27 It categorized lending in the public unit of account on a fractional reserve as common law “debt”—not impermissible fraud.28 It undergirded the development of interbank lending and the London money market (Pressnell 1956; Bagehot [1873] 1999; Desan 2014: 360–403).29 Eventually, it assigned to the Bank of England the responsibility to stabilize the system as a central bank.30

As participants elaborated the system, its effects became more and more striking. Consider the sheer impact of commercial banking on money’s production. Commercial banking decentralized the process; it dispersed the privilege of cash creation to numerous agents in the field. By comparison, medieval mints did respond to private demand for more assets in money form; entrepreneurs could bring in bullion and acquire coin. In early America, they could put up land and get bills of credit. But according to the modern method, if individuals made (or make) a promise of future productivity that is good enough to convince a local banker, they could (can) get cash. The process realigned and eased eligibility, inviting all those credible to a commercial lender and able to meet his or her terms to influence money production.

The money stock skyrocketed. Adjusted for inflation, it was about sixty-five times larger in 2009 than it had been on the eve of the Bank of England’s establishment. (Unadjusted, the money stock has expanded something like eight thousand–fold [Desan 2014: 2–3]). Moreover, commercial banks provide more than 95 percent of that supply; our cash mainly takes the form of commercial bank deposits, as opposed to the “high-powered” money represented by commercial bank reserves or deposits (Ryan-Collins et al. 2011: 23). Indeed, the private role in the process we have constructed to make money is so dominant that it amounts to a qualitative change. Money no longer appears to be a publicly produced resource. Instead, it looks like the means that business entities arrange to facilitate individual exchange. They become the appropriate experts in the field, dispensing access to credit in accord with their estimates of economic productivity. The market and its money come more and more to look like the modern models of them.

Conclusion

The image that emerges returns us to Georg Simmel’s observation at the outset. In the modern world, the market seems a separate sphere from the state. Money flows from entrepreneurs, specialists in an industry of lending. They respond to private demand for a means to make exchange; the profit calculus guides both bankers and their clients. To all appearances, money arises from individual transactions and reduces everything to a trade for comparative value. In those circumstances, Simmel could remark on money’s “colorless-ness,” its ability to paint the world in an “evenly flat and gray tone.” “Since money is nothing but the indifferent means for concrete and infinitely varied purposes,” he wrote, “its quantity is its only important determination as far as we are concerned” (Simmel [1907] 2004: 259). With reference to money, we do not ask “what and how,” but “how much” (Zelizer [1994] 1997: 1–2).

Medieval commentators might have read Simmel as condemning avarice, but they would never suspect that he was describing the medium of acquisition. Because for them, money was anything but “colorless.” It was “the second blood” according to the sixteenth-century Italian economist Bernardo Davanzati, “as blood is the sap and nutritive substance in the natural body,” so money “maintains the body of the republic” (Davanzati quoted in Johnson 1966: 120). The metaphor recurred throughout the era.

Gold was at the center of its own set of fables. Dante, for example, recycled the classical story of Midas, casting a king whose touch turned everything to gold as the poster child for greed (Dante [ca. 1314] 2003, canto 20, l. 106). In the modern world, money is feared for its ability to capture all things in monotone, but in the Middle Ages, the danger was different. Rather than reducing all things to quantity, the rich might hoard the metal, starving themselves and others. In fact, medieval commentators both Aristotelian and religious celebrated money for its ability to generate commensurable values. That capacity held the promise of just exchange; Aristotle thus put money at the heart of his most sustained discussion of justice (Kaye 2014: 20–47).

Early Americans wrote copiously about money in their colonial experiment. There, as well, no complaints that it was colorless occur. To the contrary, settlers picked up the blood metaphor for money—it made sense of a money visibly crafted for local circulation and tied to provincial taxes. As in the medieval case, the danger colonists attributed to money flowed from their own circumstances. Specie left the country too easily; by contrast paper money could “never be carried away from us” (Essay 1734: 7). It amounted to “coined land,” as Franklin put it (Franklin 1729: 24) and “the produce of our country” as another wrote (Dialogue 1725: 2). The rich, elaborated one commentator, were those divisive spirits “who want to send money away” (Dialogue 1725: 2). The goal of most paper money advocates was not to humanize an impersonal medium but to increase access to money, a liquidity they hoped would irrigate a growing land (Lester 1938, 1939; Desan 2008).

Simmel’s critique is not, then, an intuitively obvious observation about money, nor even a high degree of monetization. Rather, it is the product of a particular kind of money, a historically specific medium engineered in a distinctive way. Modern money, issued by a commercial industry that sorts individuals in terms of economic productivity, generates an image of itself as expressing “the purely commercial element in the commercial treatment of things … the abstract form that represents the immanent value of objects” (Simmel [1907] 2004: 445).

We must, however, see beyond the self-referential image of the machinery we have created. Money is not an abstraction but a constitutional phenomenon; it is a malleable practice loaded with determinations that selectively institutionalize certain relations, assign roles, and distribute profits. Modern money released those who designed it from certain problems, but it has created others, including oppressive approaches to sovereign debt cycles, credit-induced booms and busts, the grant of enormous and largely unconsidered privileges to the banking sector, and trends toward inequality that destroy the archaic dream of money as a path toward just exchange. Acknowledging money’s internal design helps illuminate the way toward its reform.

Notes

For their comments and insights, I am grateful to Nina Bandelj, Frederick F. Wherry, and Viviana Zelizer, as well as the participants at the Money Talks Symposium.

1. With permission from Taylor & Francis Group.

2. With permission from Cambridge University Press.

3. On the simultaneously liberatory but alienating effects of money according to Simmel, see Dodd (1994).

4. Keynesian sources also emphasize money’s role as a store of value (Tobin 2008).

5. For a review of the barter myth, see Graeber (2012).

6. For a more detailed exposition of the argument made in this section, and its grounding in the history of the early English world, see Desan (2014).

7. An explanation of the way economics quantifies such values is in Desan (2014). Underemphasized here is money’s dependence on time for value: as a form of credit, it holds value given an expected future use. The discount toward that use may be offset by money’s advantages as a medium in the present.

8. As discussed below, the power to create and control money can be allocated in ways democratic or dictatorial. That allocation is part of money’s interior design—its constitution.

9. For a detailed reconstruction, see Desan (2014).

10. See 12 U.S.C. §§411, 412, and 464, and associated regulations; 31 U.S.C. §5103; see also Knox v. Lee, 79 U.S. 457, 544 (1870); Knox, 79 U.S. at 556–58, 560, 563–64 (Bradley, J., concurring); Julliard v. Greenman, 110 U.S. at 444–46, 447–48, 450; Norman v. Baltimore & Ohio R.R., 294 U.S. 240, 303 (1935).

11. The shorthand should be read to include the working force of time and the importance of the cash premium. See note 7 above and related text.

12. The English regime was emphatically nominalist: as a legal form of payment, coin moved by count, not by weight or commodity content. See Desan (2014). Remember that coin was worth more than its equivalent in bullion: it carried a cash premium because it was easier to use. See note 7 above and related text; see also Sargent and Velde (2002).

13. For an exploration of similar problems in other money regimes and the plethora of responses to it, see Kuroda (2008).

14. For the influence of money’s engineering on that rise, consider Borden (1746) and Desan (2008).

15. See, e.g., “An Act for a Supply to Be Granted to His Majesty, Nov. 19, 1720,” reprinted in Colonial Laws of New York (1894).

16. For a response condemning the populist rhetoric, see “Letter from a Gentleman in Boston to His Friend in Connecticut” (1744).

17. The same principle creates what is called “high-powered money” today. High-powered money includes currency and bank reserves held by commercial banks at the Federal Reserve. These are sovereign liabilities that will be taken at face value to cancel public obligations. See Mishkin (2010: 411–13).

18. In fact, individuals may not have used that accounting unit at all, rendering it less than a full-purpose money as we think of it today.

19. For extended discussions of free minting, including problems with the neat mechanism implied here, see Spufford (1988); Mayhew (2000); Sargent and Velde (2002).

20. Bank of England Act of 1694, 5 & 6 W & M c 20 s 28.

21. See note 17 above.

22. Private actors were susceptible to public pressure. But for recent work that emphasizes the importance of (private) demand in determining the money stock and power held by bankers in the modern day, see Jackson and Dyson (2013) and Lavoie (2014).

23. Some Americans protested the arrangement, and some provinces experimented with attaching interest to their notes. Most notes, however, were issued interest-free, to the protest of opponents (Douglass 1740; Grubb 2016).

24. Often before the end of the seventeenth century, the English government had borrowed for conventional loans, getting coin from wealthy lenders. The government paid interest on those loans. Just as a conventional (private) debtor would, the government was receiving existing money, not granting the banks the power to create new money.

25. David Singh Grewal (in chapter 7 of this volume) explores arguments for the “providential” character of “enlightened self-interest” developed by French Jansenists in approximately the same period. Like the English approach, Jansenists theorized that “self-love” could motivate people to take actions that were ultimately good for the larger community.

26. Albert Hirschman (1997) estimates that the critical shift in attitudes toward self-interest occurred during the decades when the English were innovating circulating public debt, an ingredient that contributed to money’s redesign at the end of the century.

27. 3 & 4 Ann c 8 s 1 (1704).

28. Foley v. Hill (1848) 2 HL 28, 38–39, 9 ER 1002, 1006–1007; Carr v. Carr (1811), 1 Mer 625; 35 ER 799, 800; cf. Miller v. Race (1758) 1 Burr 452, 459; 97 ER 398, 402.

29. For a rich exploration of the need for clearing and coordination mechanisms in modern fraction reserve systems, see Nadav Orian Peer, “A Constitutional Approach to Shadow Banking: The Early Shadow System.” SJD diss., Harvard Law School, 2016.

30. For the case that the bank was necessary, see the classic: Bagehot ([1873] 1999). For a history reconstructing the bank’s expanding role, see Knafo (2013).

References

“An Act for a Supply to Be Granted to His Majesty, Nov. 19, 1720.” 1720. Reprinted in Colonial Laws of New York. Albany, NY: J. B. Lyon, State Printer, 1894.

Bagehot, Walter. [1873] 1999. Lombard Street: A Description of the Money Market. New York: John Wiley and Sons.

Bank for International Settlements. 2003. The Role of Central Bank Money in Payment Systems. Basel: Bank for International Settlements. http://www.bis.org/cpmi/publ/d55.pdf.

Bisson, Thomas N. 1979. Conservation of Coinage: Monetary Exploitation and Its Restraint in France, Catalonia, and Aragon (C.A.D.1000–C.1225). Oxford: Clarendon Press.

Blyth, Mark. 2002. Great Transformations: Economic Ideas and Institutional Change in the Twentieth Century. New York: Cambridge University Press.

Borden, William. 1746. An Address to the Inhabitants of North-Carolina, Occasioned by the Difficult Circumstances the Government Seems to Labour Under…. Williamsburg, VA: William Parks.

Brock, Leslie V. 1975. The Currency of the American Colonies, 1700–1764: A Study in Colonial Finance and Imperial Relations. New York: Arno Press.

The Case of Mixed Money (Privy Council). 1605. In Cobbett’s Complete Collection of State Trials and Proceedingsfor High Treason and Other Crimes and Misdemeanorsfrom the Earliest Period to the Present Time, edited by T. B. Howell, vol. 7. London: R. Bagshaw, 1811.

The Case of the Bankers (Privy Council). 1696, 1700. In Cobbett’s Complete Collection of State Trials and Proceedings for High Treason and Other Crimes and Misdemeanors from the Earliest Period to the Present Time, edited by T. B. Howell, vol. 14. London: R. Bagshaw, 1812.

Cipolla, Carlo M. 1963. “Currency Depreciation in Medieval Europe.” Economic History Review 15(3): 413–22.

Dante Alighieri. [ca. 1314] 2003. The Divine Comedy of Dante Alighieri. Vol. 2, Purgatorio. Edited and translated by Robert M. Durling. Oxford: Oxford University Press.

Desan, Christine A. 2008. “From Blood to Profit: Making Money in the Practice and Imagery of Early America.” Journal of Policy History 20(1): 26–46.

———. 2014. Making Money: Coin, Currency, and the Coming of Capitalism. Oxford: Oxford University Press.

A Dialogue between Mr. Robert Rich, and Roger Plowman. 1725. Philadelphia: Samuel Keimer.

Dodd, Nigel. 1994. The Sociology of Money: Economics, Reason and Contemporary Society. New York: Continuum Publishing.

Douglass, William. 1740. “Discourse on the Currencies of the American Plantations.” In Colonial Currency Reprints, edited by A. M. Davis, 3:308–56. Boston: Prince Society, 1911.

An Essay on Currency. 1734. Charlestown, SC: Lewis Timothy.

Ferguson, E. James. 1953. “Currency Finance: An Interpretation of Colonial Monetary Practices.” William and Mary Quarterly 10(2): 153–80.

Fourcade, Marion, and Kieran Healy. 2007. “Moral Views of Market Society.” Annual Review of Sociology 33: 285–311.

Franklin, Benjamin. 1729. Modest Enquiry into the Nature and Necessity of a Paper-Currency. Philadelphia. The Papers of Benjamin Franklin. http://franklinpapers.org/franklin//framedVolumes.jsp.

Godfrey, Michael. 1695. A Short Account of the Bank of England. London. Early English Books Online. http://name.umdl.umich.edu/A42905.0001.001.

Goodhart, Charles. 1988. The Evolution of Central Banks. Cambridge, MA: MIT Press.

Graeber, David. 2012. Debt: The First 5000 Years. Brooklyn, NY: Melville House Publishing.

Greene, Jack P. 1972. The Quest for Power: The Lower Houses of Assembly in the Southern Royal Colonies, 1689–1776. New York: W. W. Norton.

Grubb, Farley. 2016. “Is Paper Money Just Paper Money? Experimentation and Local Variation in the Fiat Monies Issued by the Colonial Governments of British North America, 1690–1775.” Research in Economic History 32: 147–224.

Hanson, John R., II. 1980. “Small Notes in the American Colonies.” Explorations in Economic History 17(4): 411–20.

Healy, Kieran. 2006. Last Best Gifts: Altruism and the Market for Human Blood and Organs. Chicago: University of Chicago Press.

Hirschman, Albert O. 1997. The Passions and the Interests: Political Arguments for Capitalism before Its Triumph. Princeton, NJ: Princeton University Press.

Jackson, Andrew, and Benjamin Dyson. 2013. Modernising Money: Why Our Monetary System Is Broken and How It Can Be Fixed. London: Positive Money.

Johnson, Jerah. 1966. “The Money = Blood Metaphor, 1300–1800.” Journal of Finance 21(1): 119–22.

Kaye, Joel. 2014. A History of Balance, 1250–1375: The Emergence of a New Model of Equilibrium and Its Impact on Thought. Cambridge: Cambridge University Press.

Knafo, Samuel. 2013. The Making of Modern Finance: Liberal Governance and the Gold Standard. London: Routledge.

Kuroda, Akinobu. 2008. “What Is the Complementarity among Monies? An Introductory Note.” Financial History Review 15(1): 7–15.

Lavoie, Marc. 2014. Post-Keynesian Economics: New Foundations. Cheltenham, UK: Edward Elgar.

Lester, Richard. 1938. “Currency Issues to Overcome Depressions in Pennsylvania, 1723 and 1729.” Journal of Political Economy 46(3): 324–75.

———. 1939. “Currency Issues to Overcome Depressions in Delaware, New Jersey, New York, and Maryland, 1715–1737.” Journal of Political Economy 47(2): 182–217.

“Letter from a Gentleman in Boston to His Friend in Connecticut.” 1744. Boston. Evans Early American Imprint Collection. http://quod.lib.umich.edu/e/evans/N04388.0001.001/1:2?rgn=div1;view=fulltext;q1=Currency+question+--+Massachusetts.

Levine, Ross. 1997. “Financial Development and Economic Growth: Views and Agenda.” Journal of Economic Literature 35(2): 688–726.

Mather, Cotton. 1691. “Some Considerations on the Bills of Credit Now Passing in New-England.” In Colonial Currency Reprints, edited by A. M. Davis, 1:189–96. Boston: John Wilson & Son, 1910.

Mayhew, N.J. 1992. “From Regional to Central Minting, 1158–1464.” In A New History of the Royal Mint, edited by C. E. Challis, 83–178. Cambridge: Cambridge University Press.

———. 1995. “Population, Money Supply, and the Velocity of Circulation in England, 1300–1700.” Economic History Review 48(2): 238–57.

———. 2000. Sterling: The History of a Currency. New York: Wiley.

Mishkin, Frederic S. 2010. The Economics of Money, Banking, and Financial Markets. Boston: Addison-Wesley.

Pressnell, L. S. 1956. Country Banking in the Industrial Revolution. Oxford: Oxford University Press.

Ryan-Collins, Josh, Tony Greenham, Richard Werner, and Andrew Jackson. 2011. Where Does Money Come From? London: New Economics Foundation.

Samuelson, Paul, and William D. Nordhaus. 1973. Economics. New York: McGraw-Hill.

Sargent, Thomas J., and Francois R. Velde. 2002. The Big Problem of Small Change. Princeton, NJ: Princeton University Press.

Simmel, Georg. [1907] 2004. The Philosophy of Money. Translated and edited by T. B. Bottomore and D. Frisby. London: Routledge.

Singh, Supriya. 2013. Globalization and Money: A Global South Perspective. Lanham, MD: Rowman and Littlefield.

Smith, Adam. [1776] 1937. “On Money Considered as a Particular Branch of the General Stock of the Society, or of the Expense of Maintaining the National Capital.” Chap. 2 in An Inquiry into the Nature and Causes of the Wealth of Nations. New York: Modern Library.

Spencer, Henry Russell. 1905. Constitutional Conflict in Provincial Massachusetts. Columbus, OH: Press of Fred J. Heer.

Spufford, Peter. 1988. Money and Its Use in Medieval Europe. Cambridge: Cambridge University Press.

A State of the Case, between Furnishing His Majesty with Money by Way of Loan, or by Way of Advance of the Tax of Any Particular Place, upon the Act for the £1250000, passed at Oxford, October 9, 1665. 1666. Making of the Modern World. http://find.galegroup.com/mome/infomark.do?&source=gale&prodId=MOME&userGroupName=prin7798&tabID=T001&docId=U3600201067&type=multipage&contentSet=MOMEArticles&version=1.0&docLevel=FASCIMILE.

Thayer, Theodore. 1953. “The Land-Bank System in the American Colonies.” Journal of Economic History 13(2): 145–59. doi: 10.2307/2113435.

Timberlake, Richard. 2013. Constitutional Money: A Review of the Supreme Court’s Monetary Decisions. Cambridge: Cambridge University Press.

Tobin, James. 2008. “Money.” In The New Palgrave Dictionary of Economics, edited by S. N. Durlauf and L. E. Blume. London: Palgrave Macmillan.

Velthuis, Olav. 2005. Talking Prices: Symbolic Meanings of Prices on the Market for Contemporary Art. Princeton, NJ: Princeton University Press.

Zelizer, Viviana A. [1994] 1997. The Social Meaning of Money. Princeton, NJ: Princeton University Press.