In the first chapter we saw that innovation, defined as the creation of new value that serves your organization’s mission and customer, must be woven into the fabric of the organization and sustained over time. In order to survive and prosper, your organization needs to innovate consistently and methodically. There are many ways to do it—you need to find the methods that work best for your company.

Having laid the groundwork, now is the time to take action and embrace the Innovation Mandate in your organization.

Luckily, human beings are born innovators—so you’re already halfway there. And you probably have pockets of innovation happening right now in your company. That’s good!

But you want consistency and quality. As a leader, it’s your job to set up a system to take your employees’ sparks and collect them, evaluate them, and treat them as potential assets. To exploit their profit potential, selected innovations need to be transformed from theory to reality.

This transformation will not happen on its own or by accident. Profiting from innovation takes a structured effort.

Unfortunately, too many sparks of innovation are ignored, overlooked, or allowed to get cold and die. Sometimes they seem attractive when first proposed, but there’s no will or process to take the first small spark and turn it into real energy.

Any reluctance to hammer out the details is insidious and dangerous to organizational success. To win at innovation you first need to build leadership skills that drive innovation as a core competency, while making innovation understandable to each and every stakeholder across the enterprise. To make your plan to foster and encourage innovation easy to understand and remember, our team created a simple acronym. The REAL method consists of the following:

Let’s examine this concept in detail.

REVIEW

Leaders who become enamored with the idea of innovation often plunge ahead pell-mell without ensuring that their organization is ready to embrace a culture of sustained innovation. If they do this, they run the risk that the spark will fall on damp wood and fail to ignite. This is not the outcome you want.

Without a robust innovation operating system, things like hosting quarterly hackathons, buying Ping-Pong tables, making an unused room into an “innovation lab,” installing whiteboards, and making jeans acceptable work attire are nothing more than quick-fix solutions. Leaders sometimes see these measures and become convinced they’re ready for innovation when, in fact, the critical ingredients for sustained, profitable innovation are missing.

The Two Critical Questions

The first question to ask is, “As the leader, am I personally ready to embrace new ideas that can be shown to have merit and are worth investing in?”

The answer needs to be, “Yes, I’m ready.”

The second question is, “Are our employees in a psychological place where they will trust leadership to treat their new ideas with respect? Will they respond to our call for innovation and new ideas, or think it’s a ploy?”

Again, the answer needs to be, “Yes, they’re ready.”

Fractional, piecemeal innovation initiatives aren’t enough. To fully leverage the Innovation Mandate, you need to review the current state of the business before designing an innovation operating system touching every corner of the organization and providing a step-by-step template aimed at building profit power. This should be done with input and ownership from all levels and across all business units.

Your Innovation Mandate needs a clear direction. Set goals, both large and small, long term and short term. For any type of innovation—from saving time in a process to improving a product—identify what you want to achieve, how long you have to get it accomplished, and what constitutes success.

ENCOURAGE

After an organization builds out a credible innovation strategy, leaders need to approve, endorse, and fund the systems and tools necessary for successful execution. In other words, the formation and acceptance of a theory must be followed by clear directives supported by leadership.

Leaders are the key players in fostering a culture of innovation, including modeling behaviors to ensure that the walk matches the talk. Because failure is a built-in component of innovation, this can often mean showing support for untested, new, or disruptive ideas. It’s imperative that leaders consistently communicate the vision of innovation so that no one misses the message.

An effective Innovation Mandate comprises a range of activities and systems that encourage your team members to participate in the game of innovation. (And yes, it is like a game, with really good prizes for the winners!) These processes are designed to increase the volume of ideas that go into the innovation pipeline. Remember, innovation is a high-volume, low-yield proposition. Put more simply, failure is a fundamental part of innovation. For every ten sparks your people ignite, perhaps one will survive and show itself to be profitable. That’s to be expected!

It’s no different from the standard project development process that you already know. In any project development cycle, the steps are:

1. Brainstorming

2. Collaborating

3. Planning

4. Implementation

5. Evaluation

6. Completion (unless it’s ongoing)

During the brainstorming phase, a premium is placed on ideas. Good ideas, bad ideas, crazy ideas—almost every project development expert on earth will tell you that during this important first phase, every participant must have permission to offer any far-fetched notion. When everyone’s had a chance to contribute, the inventory of ideas is discussed, and the ones that are promising are retained while the impractical ones are discarded, with no judgment passed on the people who offered them.

A culture of innovation is no different. In the earliest phase, quantity equals quality. The more sparks, the better!

ACT

Following reviewing and encouraging, leaders and employees must act upon their stated innovation strategy. The goal is to identify, evaluate, nurture, and underwrite new ideas from all sources. Keeping the innovation pipeline full needs to be a priority. If the company is big enough, this may require an innovation director or department to manage and track the innovations that will come streaming in.

A well-designed employee suggestion program, supported by organizational commitment, leadership clarity, and ongoing communication, can positively impact your employee motivation and enthusiasm, your innovation pipeline, and ultimately your bottom line. You can also schedule departmental brainstorming sessions, or solicit ideas during a few minutes of your weekly staff meeting. Some companies set aside one day a month for a lunch meeting at which every employee is asked to submit at least one idea.

If your people need a structure that will help them get started, digital platforms such as Spigit, which enable leaders to tap into the collective intelligence of employees, partners, and customers to find the best ideas and make the right decisions, can help engage stakeholders to participate in well-defined innovation challenges. Be sure to prepare by conducting a comprehensive innovation gap analysis, and prior to identifying any technology tools, you’ll need a high-level innovation mission. Innovation is a people-powered process, and while it can be optimized through a range of technology tools, you should use them with great care and thoughtfulness.

Respond Decisively

Having assembled an inventory of new ideas—or, even better, having facilitated a steady stream—the next action step is to evaluate each one and then take one of these decisive actions:

1. Accept it.

2. Reject it.

3. Send it back for more study, which may include funding it.

Remember, to the employee who submits an idea to “the bosses,” nothing—repeat, nothing—is more disheartening than receiving no reply. Every idea should be acknowledged within twenty-four hours, even to just say, “Thank you, we appreciate your idea.” If possible, the employee should be notified as to the dispensation of their idea—yes, no, or further study.

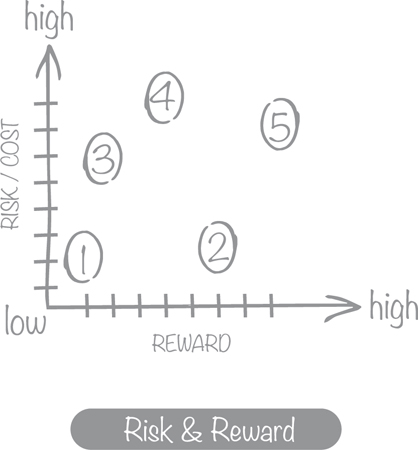

In your inventory of new ideas, you’ll quickly see that they tend to fall along a spectrum of risk (or cost) and reward. If you created a coordinate grid, you’d plot the vertical X-axis with low risk (or cost) to high risk (or cost), and the horizontal Y-axis with low reward to high reward. At the lower left corner you’d find the ideas that were low risk and low reward. In the upper right corner would be the ideas that are both high risk and high reward.

In this example, Idea 1 is low risk/cost and low reward. It may not look like much, but if this idea were one of a constant stream of low-risk, low-reward ideas in a program of continuous incremental innovation (kaizen), then it would be valuable. Remember, as Katsuaki Watanabe of Toyota said, if you keep innovating like that for seventy years, you’ll have a revolution!1

Idea 2 is low risk/cost and high reward. What are you waiting for? Grab it and go!

Ideas 3 and 4 are higher risk/cost with low expected reward. You may want to pass on them.

Idea 5 is high risk/cost and high reward. These are the breathtaking innovative gambles that make headlines, like Elon Musk shooting a rocket carrying his electric car into orbit around the sun, or a movie studio wagering hundreds of millions of dollars on a summertime superhero blockbuster. If you gamble big, then you win—or lose—big.

But massive gambles can take less-obvious forms, like in 2010 when Domino’s Pizza created television ads known as the “Our pizza sucks” campaign. The ads featured clips of Domino’s employees reading terrible comments made by customers: “Worst excuse for pizza I ever had,” a company executive said grimly, quoting a customer’s comment. “Totally devoid of flavor.” A woman in a clip taken from a focus-group panel said, “Domino’s pizza crust to me is like cardboard.” An employee tearfully reads another review: “The sauce tastes like ketchup.”

Risky? Yes. Innovative? Also yes. As the Washington Post reported, Domino’s said its ad strategy wasn’t prompted by crisis or underperformance. Rather, the company said it was knocking its own pizza as a way to show its commitment to doing better: “We’re proving to our customers that we are listening to them by brutally accepting the criticism that’s out there,” said Patrick Doyle, the company’s incoming chief executive.2

Domino’s stock price? In 2010 it was hovering at $13 per share. Since then it has steadily climbed, and in March 2018 traded at $230 per share. Not bad!3

But going back to our risk/reward graph, it would seem obvious that Idea 2, which was both low risk and high reward, would be highly desirable! But amazingly, even ideas that have landed in this sweet spot have been rejected by leaders who didn’t recognize or value innovation.

There are so many juicy examples . . . Here are just a few:

• “Who the hell wants to hear actors talk?” Harry Warner, a founder of Warner Brothers movie studio, said this in 1927, when movies were silent.4

• “There is no reason anyone would want a computer in their home.” Ken Olsen, president, chairman, and founder of Digital Equipment Corp., said this in 1977.5

• “So we went to Atari and said, ‘Hey, we’ve got this amazing thing, even built with some of your parts, and what do you think about funding us? Or we’ll give it to you. We just want to do it. Pay our salary, we’ll come work for you.’ And they said, ‘No.’ So then we went to Hewlett-Packard, and they said, ‘Hey we don’t need you. You haven’t got through college yet.’” Apple Computer Inc. founder Steve Jobs shared this about his early attempts to interest big tech companies in his personal computer.6

• “On June 26, 2008, our friend Michael Seibel introduced us to seven prominent investors in Silicon Valley. We were attempting to raise $150,000 at a $1.5M valuation. That means for $150,000 you could have bought 10 percent of Airbnb. Below you will see five rejections. The other two did not reply.” Brian Chesky, co-founder and CEO of Airbnb, wrote this in a 2015 blog post.7

Yes, even smart people are fallible. As a leader, you need to be open to new ideas, know how to evaluate the risk and reward of an idea, and take action when necessary.

Remember, you can’t focus exclusively on risk! Over the years, consultants and leaders have created many types of processes for innovation evaluation and management. Most are incredibly complicated and definitely risk centered. In fact, the overwhelming majority of organizations use systems that are virtually exclusively centered around risk management. This approach is like playing the game not to lose rather than playing the game to win.

The innovations that come out of risk-centric evaluation and management processes are rarely disruptive or breakthrough innovations that have big opportunities. These types of processes typically incubate incremental improvements. The best way to look at the Innovation Mandate is that it’s a stock portfolio comprised of a range of high-risk, high-reward innovations and lower-risk, lower-reward innovations. But you know the rule that risk and reward increase together, so if you want the big hit, you’re likely going to take a big risk. Afraid of taking a big risk likely means you will see only incremental innovations.

LEAD

According to the Center for Creative Leadership, “Studies have shown that 20 to 67 percent of the variance on measures of the climate for creativity in organizations is directly attributable to leadership behavior. What this means is that leaders must act in ways that promote and support organizational innovation.” Day in and day out, innovation requires sustained and powerful leadership. The best innovation strategy in the world will fail without committed leadership. Innovation requires savvy leaders who possess a core competency around innovation and a commitment to make innovation part of the enterprise of DNA and reap the rewards, day after day, quarter after quarter, year after year.8

The Center for Creative Leadership describes the three tasks of leadership as setting direction, creating alignment, and building commitment. When these core tasks are centered around innovation, organizations become more innovative and more productive.

Your Innovation Mandate needs to be capable of transforming ideas into reality. Your new process improvement, technology, marketing innovation, or other enterprise innovation needs to be plugged into your organization’s product lineup or everyday operations so its worth can be proven or disproven.

This requires the endorsement and support of leaders, because they are the ones who typically control the allocation of resources in the form of both money and time.

Innovation—whether it’s a new invention, new product, or new business process—represents change. A change from the way things are being done now. If you know anything about people, then you know that most people in their day-to-day work don’t seek out changes in their routine.

Innovation Champion

Whether it’s for a particular project or to manage a culture of innovation, you may need an innovation champion. This is someone who, when necessary, can get the endorsement of leaders when it’s time to put an idea into practice.

An innovation champion is passionate about making innovation thrive within their organization. Champions may not necessarily be the top idea generators or creative geniuses; rather they are the inspirers, facilitators, and connectors. A critical player in the success of the deployment, the innovation champion acts well beyond the initial market launch. He or she complements the role of the project development leader. During successive launches, they progressively develop a keen understanding of the benefits valued by customers and employees alike, guiding those who adopt the innovation by providing them with logistical, technical, and economic support.

THE CSAA INSURANCE GROUP SPARKS INNOVATION

We often think that creating a sustained stream of sparks is the sole province of trendy hi-tech companies like Apple and Google.

In reality, nothing could be further from the truth.

No matter what industry you’re in, your organization can and should innovate. Remember, innovation doesn’t just mean creating a new shiny object to excite consumers of digital gadgets. You can innovate in your supply chain, in human resources, in facilities operations, in customer service, or in any other facet of your business. Innovation can both earn money and save money—and both are equally good for your bottom line.

Headquartered in Walnut Creek, California, CSAA Insurance Group sells insurance to household members of the American Automobile Association (AAA). Each year their 3,800 employees write $4 billion worth of insurance premiums in thirty states. At this venerable company founded in 1914, they take innovation seriously; it’s even included in the corporate vision document: “Our innovation: We are building the agility and ability to adapt to—and drive—change in the face of disruptive trends and technologies that influence cars, homes, and the marketplace. Innovation at CSAA Insurance Group means finding new and better ways to improve service, create outstanding member experiences, develop new products and services, and grow partnerships and revenue.”9

Please note that the last word in the statement is “revenue.” At CSAA IG, innovation isn’t just a feel-good exercise. It helps the company make more money.

CSAA IG recognizes and embraces three specific types of innovation: continuous, sustaining, and disruptive.

Since it’s neither a pharmaceutical giant nor a Silicon Valley hi-tech company, the company’s innovation strategy recognizes that the majority of the innovations developed by its employees involve continuous improvements that, when accumulated over time, significantly advance the core business. Because they’re on the front lines, ordinary employees, from claims adjusters in the field to call center employees, offer ideas for continuous improvements to everyday business processes, the customer experience, and the company’s insurance products.

But even at an insurance company, sustaining and disruptive innovations are possible. For example, a sustaining innovation could involve a new product or new customer digital experiences, such as offering a smartphone app. A disruptive innovation would be introducing auto insurance for driverless cars—which is something every auto insurer needs to figure out!

CSAA IG backs up its professed dedication to innovation with real commitment. As Harvard Business Review reported in August 2017, CSAA IG provides innovation training to all employees. With a program that provides tools and practical exercises grounded in design thinking, the company encourages everyone to contribute new ideas for product offerings, customer experiences, and improved business processes. The company arranges half-day sessions during which employees are asked to brainstorm about issues affecting their business areas, with the goal of coming up with solutions. As HBR noted, this modest investment produces real results. In one session, a team of insurance underwriters reviewed call data and suggested changes to incoming voice prompts that reduced erroneous phone transfers to their department by 40 percent. Another team simplified the process for issuing proof of insurance cards and spearheaded efforts to develop “smart claims” systems, allowing claimants to submit digital images of damaged property for online assessment.10

Employees also have access to CSAA IG’s “Innovation Hub,” an online portal, which includes a variety of resources including articles from innovation experts, self-paced training materials, a calendar of innovation-related events, a design thinking toolkit, and more.

In her “CEO’s Message,” published in the CSAA IG Innovation Toolkit, CSAA IG leader Paula F. Downey wrote, “Given that innovation is the focus of one of our strategic initiatives, you probably know that it’s important to us—but how important is it? Simply put, it’s our future. In fact, we have accelerated our approach to innovation on three fronts: through the everyday work we all do, in the new products and services we develop, and by putting an organization in place to proactively seek out the next insurance industry breakthrough.”11

Innovation is the future of CSAA IG . . . and it should be yours too.