At this stage of the transaction, both the seller and the buyer (and their respective advisors) have developed a strategic plan and a tentative timetable for completion of the deal, have completed their analysis as to why the transaction is a strong financial and strategic fit for each party, and hopefully have taken the time to understand each other’s perspective and the competing as well as aligned objectives.

Buyers may enlist a financial advisor to assist in getting to this stage and helping the buyer ensure it is making decisions consistent with its financial and business goals. Thus, often the first agreement the buyer enters into in preparation of an acquisition is with its financial advisor, traditionally in the form of an engagement letter. The terms in an engagement letter must be carefully negotiated to account for the myriad of possible outcomes a buyer could encounter in the early stages of an acquisition. The engagement letter may contain an assortment of fees covering the full range of the transaction, including retainer fees, interim fees, success fees, and termination fees. Thus, the buyer should also build in key provisions to protect itself, similar to the “binding terms” discussed in more detail below. Such provisions include confidentiality, conflicts of interest, exclusivity provisions, and termination provisions (e.g., notice to the advisor if the buyer wants to terminate and the obligation to pay termination fees). These are essential given that at the early stages of a transaction the buyer is interacting with and disclosing information to its financial advisor at an even deeper level than it does with a potential seller.

Eventually the parties reach the point at which the field of available candidates has been narrowed, the preliminary “get to know each other” meetings have been completed, and a tentative selection has been made. After the completion of the presale review, the next step involves the preparation and negotiation of an interim agreement that will guide and govern the conduct of the parties up until closing.

Although there are certain valid legal arguments against the execution of any type of interim document, especially since some courts have interpreted such documents as being binding legal documents (even if one or more of the parties did not initially intend to be bound), it has been my experience that a letter of intent (LOI), which includes a set of binding and nonbinding terms as a road map for the transaction, is a necessary step in virtually all mergers and acquisitions. In lieu of a formal LOI, parties may prepare an unexecuted term sheet or, alternatively, enter into definitive agreements directly. I have found, however, that most parties prefer the organizational framework and psychological comfort of knowing that there is some type of written document in place before proceeding further and before significant expenses are incurred. It is also critical to deal with as many of the potential due diligence problems or surprises as possible at this early stage. The ability to resolve problems that may derail a transaction is much stronger at the outset of the deal, before each party has incurred significant expenses and becomes more entrenched in its position. The advantages and disadvantages of a letter of intent are discussed in Figure 4-1.

In addition to creating a framework for any potential deal with the prospective buyer, an LOI is a catalyzing event in most deals. Receiving an LOI, even one that has unacceptable terms, gives the investment banker the opportunity to reach out to each of the target buyers and accelerate the “go/no-go” decision. In a normal process, the investment banker strives to keep the potential buyers on a common time frame. However, the first LOI drives the timing of the process and, furthermore, provides a solid framework for more specific price negotiations.

Figure 4-1. Advantages and Disadvantages of Executing a Letter of Intent

Advantages

Tests the parties’ seriousness.

Tests the parties’ seriousness.

Mentally commits the parties to the sale.

Sets out in writing certain key areas of agreement. Important since there may be a long delay before a definitive purchase agreement is negotiated and executed.

Highlights the remaining open issues, challenges to closing, valuation gaps, and other related matters needing further negotiation.

Discourages the seller from shopping around for a better deal (especially if “no-slip” penalties are included).

Disadvantages

May be considered a binding agreement. It is important to articulate whether or not a letter of intent is meant to constitute an enforceable agreement.

Public announcement of the prospective sale may have to be made due to federal securities law if either company is publicly held.

Finally, if the LOI received is at an acceptable price, the investment banker can now be more aggressive in price negotiations with the other interested parties. There is no event that allows the banker to create an auction more easily than an LOI, and as such, it is a tool that is welcomed, carefully managed, and ultimately used to obtain more value for the seller.

There are many different styles of drafting letters of intent, which vary from law firm to law firm and from business lawyer to business lawyer. These styles usually fall into one of three categories: (1) binding, (2) nonbinding, and (3) hybrids, like the model in Figure 4-2. In general, the type to be selected will depend upon (1) the timing and the scope of the information to be released publicly concerning the transaction (if any), (2) the degree to which negotiations have been definitive and the necessary information has been gathered, (3) the cost to the buyer and the seller of proceeding with the transaction prior to the making of binding commitments, (4) the rapidity with which the parties estimate that a final agreement can be signed, (5) the valuation ranges for the seller’s company that have been discussed to date, (6) the degree to which the buyer needs or wants a period of exclusivity (and the degree to which the seller is willing to grant an exclusivity period, (7) the relative status of the parties and leverage that both the buyer and seller have, and (8) the degree of confidence each party has in the good faith of the other party and the absence (or presence) of still other parties that are competing for the transaction. In most cases, the hybrid format, which contains both binding and nonbinding terms, is the most effective format to protect the interests of both parties and to level the playing field from a negotiations perspective.

Although it is formally executed by the buyer and the seller, a letter of intent is often considered to be an agreement in principle. As a result, the parties should be very clear as to whether the letter of intent is a binding preliminary contract or merely a memorandum from which a more definitive legal document may be drafted upon completion of due diligence. Regardless of the legal implications involved, however, by executing a letter of intent, the parties make a psychological commitment to the transaction and provide a road map for expediting more formal negotiations.

In addition, a well-drafted letter of intent will provide an overview of matters that require further discussion and consideration, such as the exact purchase price. Although an exact and final purchase price cannot realistically be established until due diligence has been completed, the seller may hesitate to proceed without a price commitment. Instead of creating a fixed price, however, the letter of intent will typically incorporate a price range that is qualified by a clause or provision setting forth all of the factors that will influence and affect the calculation of a final fixed price, such as balance sheet adjustments, due diligence surprises or problems, a change in the health of the company, or overall market conditions during the transaction period, and sometimes even an “upside surprise” in favor of the seller when a significant positive development occurs during the transaction period (e.g., the settlement of litigation, the award of important intellectual property rights, or a big new contract or customer commitment) that had not been included when the valuation range was established. The purchase price may also be affected by the tax implications of the transaction, which is generally a key factor in determining whether the transaction is structured as an asset purchase or stock purchase. The LOI also sets the framework for ancillary agreements to be negotiated later, such as licensing agreements, employment and shareholder agreements, management agreements, and non-competition agreements. Some of these agreements are discussed in more detail in Chapter 7.

As you can see from the sample letter of intent in Figure 4-2, the first section addresses certain key deal terms, such as price and method of payment. These terms are usually nonbinding so that the parties have an opportunity to complete the due diligence and analysis and have room for further negotiation, depending on the specific problems uncovered during the investigative process.

Figure 4-2. Sample Letter of Intent

Ms. Prospective Seller

SellCo, Inc.

{address}

Re: Letter of Intent Between BuyCo, Inc. and SellCo, Inc.

Dear Ms. Prospective Seller:

This letter (“Letter Agreement”) sets forth the terms by which BuyCo, Inc. (“BCI”) agrees to purchase all of the issued and outstanding common stock of SellCo, Inc. (the “Company”) in accordance with the terms set forth below. BCI and the Company are hereinafter collectively referred to as the “Parties.”

Section I of this Letter Agreement summarizes the principal terms proposed in our earlier discussions and is not an agreement binding upon either of the Parties. These principal terms are subject to the execution and delivery by the Parties of a definitive Stock Purchase Agreement and other documents related to these transactions.

Section II of this Letter Agreement contains a number of covenants by the Parties, which shall be legally binding upon the execution of this Letter Agreement by the Parties. The binding terms in Section II below are enforceable against the Parties, regardless of whether or not the aforementioned agreements are executed or the reasons for non-execution.

1. Stock Purchase. The Parties will execute a Stock Purchase Agreement, pursuant to which, BCI will purchase __________ shares of the Company’s Common Stock (the “Shares”), from the schedule of Shareholders attached hereto for a total purchase price of not less than $__________ for the Company’s Common Stock.

2. Employment Agreements. Prior to closing, the Company will enter into an individual employment agreement with __________ and __________ who are employed by the Seller for year-terms at the compensation levels of $__________ and bonus plan eligibility of between $__________ and $__________. The Employment Agreement will contain such other terms and conditions as are reasonable and customary in the type of transaction contemplated hereby.

3. Closing and Documentation. The Parties intend that a closing of the agreements shall occur on or before __________, 20___, at a time and place that is mutually acceptable to the Parties. BCI or its representatives will prepare and revise the initial and subsequent drafts of the necessary agreements.

SECTION II - BINDING TERMS

In consideration of the costs to be incurred by the Parties in undertaking actions toward the negotiation and consummation of the Stock Purchase Agreement and the related agreements, the Parties hereby agree to the following binding terms (“Binding Terms”):

4. Refundable Deposit. BCI will provide a refundable deposit in the amount of $__________ to the Company at the time of the execution of this Letter Agreement. All sums paid hereunder shall be deductible from the purchase price to be paid for the Shares as described in Paragraph 1. In the event that BCI does not complete the purchase of the Shares, the sums payable hereunder shall be referred to BCI (less __________ to be retained by the Seller for its expenses), with interest at the rate of 1.5% above the highest U.S. prime rate published in The Wall Street Journal from the date of execution of this Agreement to the date of repayment. In the event that the closing is delayed beyond __________, 20___, BCI will make an additional deposit of $__________ on __________, 20___ and $ __________ on__________, 20___.

5. Due Diligence. The directors, officers, shareholders, employees, agents and other representatives (collectively, the “Representatives”) of the Company shall (a) grant to BCI and its Representatives full access to the Company’s properties, personnel, facilities, books and records, financial and operating data, contracts and other documents; and (b) furnish all such books and records, financial and operating data, contracts and other documents or information as BCI or its Representatives may reasonably request.

6. No Material Changes. The Company agrees that, from and after the execution of this Agreement until the earlier of the termination of the Binding Terms in accordance with Paragraph 12 below or the execution and delivery of the agreements described herein, the Company’s business and operations will be conducted in the ordinary course and in substantially the same manner as such business and operations have been conducted in the past and the Company will notify BCI of any extraordinary transactions, financing, or business involving the Company or its affiliates.

7. No-Shop Provision. The Company agrees that, from and after the execution of this Agreement until the termination of the Binding Terms in accordance with Paragraph 12 below, the Company will not initiate or conclude, through its Representatives or otherwise, any negotiations with any corporation, person, or other entity regarding the sale of all or substantially all of the assets or the shares of the Company. The Company will immediately notify the other Parties regarding any such contact described above.

8. Lock-Up Provision. The Company agrees that, from and after the execution of this Agreement until (a) the consummation of the transactions contemplated in Section I and the execution of definitive agreements thereby, or (b) in the event that definitive agreements are not executed, until the repayment of all amounts advanced hereunder, plus accrued interest, that without the prior written approval of BCI and subject to any anti-dilution provisions imposed hereunder, (x) no shares of any currently issued Common Stock of the Company shall be issued, sold, transferred, or assigned to any party; (y) no such shares of Common Stock shall be pledged as security, hypothecated, or in any other way encumbered; and (z) the Company shall issue no additional shares of capital stock of any class, whether now or hereafter authorized.

9. Confidentiality. Prior to Closing, neither Party nor any of their Representatives shall make any public statement or issue any press releases regarding the agreements, the proposed transactions described herein or this Agreement without the prior written consent of the other Party, except as such disclosure may be required by law. If the law requires such disclosure, the disclosing party shall notify the other Party in advance and furnish to the other Party a copy of the proposed disclosure. Notwithstanding the foregoing, the Parties acknowledge that certain disclosures regarding the agreements, the proposed transactions or this Agreement may be required to be made to each Party’s representatives or certain of them, and to any other party whose consent or approval may be required to complete the agreements and the transactions provided for thereunder, and that such disclosures shall not require prior written consent. BCI and its employees, affiliates, and associates will (a) treat all information received from the Company confidentially, (b) not disclose such information to third parties without the prior written consent of the Company, except as such disclosure may be required by law, (c) not use such information for any purpose other than the consideration of the matters contemplated by this Letter of Intent, including related due diligence, and (d) return to the Company any such information if this Agreement terminates pursuant to Paragraph 12 below.

10. Expenses; Finder’s Fee. The Parties are responsible for and will bear all of their own costs and expenses incurred at any time in connection with the transaction proposed hereunder up to $__________. Any additional or extraordinary expenses above this amount shall be borne by BCI; provided, however, the Company shall be responsible for any finder’s fees payable in connection with the transactions contemplated hereby.

11. Breakup Fee. The Company agrees to pay BCI a breakup fee of $__________ in the event that the sale and purchase of the shares contemplated in Section I is not accomplished by__________, 20___ as a result of the Company’s failure or refusal to close pursuant to the terms set forth above and not due to any refusal or delay on the part of BCI to close by that date.

12. Effective Date. The foregoing obligations of the Parties under Section II of this Agreement shall be effective as of the date of execution by the Company, and shall terminate upon the completion of the transactions contemplated in Section I above or, if such transactions are not completed, then at such time as all of the obligations under Section II have been satisfied, unless otherwise extended by all of the Parties or specifically extended by the terms of the foregoing provisions; provided, however, that such termination shall not relieve the Parties of liability for the breach of any obligation occurring prior to such termination.

Please indicate your agreement to the Binding Terms set forth in Section II above by executing and returning a copy of this Agreement to the undersigned no later than close of business on __________, 20___. Following receipt, we will instruct legal counsel to prepare the agreements contemplated herein. The Binding Terms shall become binding on the Company upon the advance of deposit pursuant to Paragraph 4 and the execution of Promissory Note in consideration therefor.

Very truly yours,

/s/ Prospective Buyer

Prospective Buyer, President

BuyCo, Inc.

ACKNOWLEDGED AND ACCEPTED:

SellCo, Inc.

By: Prospective Seller, President |

Dated |

The sample letter of intent in Figure 4-2 also includes certain binding terms that will not be subject to further negotiation. These are certain issues that at least one side, and usually both sides, will want to ensure are binding, regardless of whether the deal is actually consummated. These include:

Legal ability of the seller to consummate the transaction. Before wasting too much time or money, the buyer will want to know that the seller has the power and the authority to close the deal.

Legal ability of the seller to consummate the transaction. Before wasting too much time or money, the buyer will want to know that the seller has the power and the authority to close the deal.

Protection of confidential information. The seller in particular, and both parties in general, will want to ensure that all information provided in the initial presentation and during due diligence remains confidential.

Access to books and records. The buyer will want to ensure that the seller and its advisors will fully cooperate in the due diligence process.

Breakup or walkaway fees. The buyer may want to include a clause in the letter of intent to attempt to recoup some of its expenses if the seller tries to walk away from the deal, either because of a change in circumstances or because of the desire to accept a more attractive offer from a different potential buyer. The seller may want a reciprocal clause to cover its own expenses if the buyer walks away or defaults on a preliminary obligation or condition to closing, such as an inability to raise acquisition capital.

No-shop/standstill provisions. The buyer may want a period of exclusivity during which it can be confident that the seller is not entertaining any other offers. The seller will want to place a limit or “outside date” on this provision in order to allow it to begin entertaining other offers if the buyer is unduly dragging its feet.

Good-faith deposit—refundable versus nonrefundable. In some cases, the seller will request a deposit or option fee, and the parties must determine to what extent, if at all, this deposit will be refundable and under what conditions. There are often timing problems with this provision that can be difficult to resolve. For example, the buyer will want the deposit to remain 100 percent refundable if the seller is being uncooperative, or at least until the buyer and its team complete the initial round of due diligence to ensure that there are no major problems discovered that might cause the buyer to walk away from the deal. The seller will want to set a limit on the due diligence and review period, after which point the buyer forfeits all or a part of its deposit. The end result is often a progressive downward scale of refundability as the due diligence and the overall deal reach various checkpoints toward closing. In the event that the buyer forfeits some or all of the deposit and the deal never closes, the buyer may want to negotiate an eventual full or partial refund if the seller finds an alternative buyer within a certain period of time, such as 180 days.

Impact on employees. Perhaps one of the most challenging issues faced by sellers is the decision as to who within the company is told what, when, and why. Sellers will typically want to “play their cards close to the vest,” whereas buyers, as part of their due diligence perspective, may want access to key executives and employees who are not yet in the loop. From a human capital management perspective, if team members are told too soon, then it may be hard to keep them from running out the door (because of their uncertainty), and if they are told too late, it may lead to resentment and frustration. If the communication of the possible sale is mishandled, then the employees may get the message that their jobs are unimportant or in jeopardy, or both. Supervisory personnel should be briefed first, and all of their questions should be answered so that they can inform their subordinates. After the closing, it is imperative that the top management of the acquiring company meet with the employees of the target company to discuss their post-closing roles, compensation, and benefits. If there will be job cuts, discuss the methods by which this will be determined and whether any training, instruction on résumé-writing skills, or outplacement services will be offered.

Key terms for the definitive documents. The letter of intent will often provide that it is subject to the definitive documents, such as the purchase agreement, and that those definitive documents will address certain key matters or include certain key sections, such as covenants, indemnification, representations and warranties, and key conditions for closing.

Conditions to closing. Both parties will want to articulate a set of conditions or circumstances such that they will not be bound to proceed with the transaction if certain contingencies are not met or if certain events happen after the execution of the letter of intent, such as third-party approvals, regulatory permissions, or related potential barriers to closing. Be sure to articulate these conditions clearly so that there are no surprises down the road.

Conduct of the business prior to closing. The buyer usually wants some guarantee that the general state of the company that it sees today will be there tomorrow. Thus, the seller will be obligated to operate its business in the ordinary course, so that assets, customers, and employees will not start disappearing from the premises; equipment will not be left in disrepair; the company will not fail to pursue new customers; bonuses will not be magically declared; personal expenses will not be paid the night before; and other steps that will deplete the value of the company prior to closing will not be taken. If these things do occur, then the parties should provide a mechanism for adjusting the price based on the relative valuation of the lost contracts, relationships, or human resources. These “negative covenants” help protect the buyer against unpleasant surprises at, or after, closing.

Limitations on publicity and press releases. The parties may want to place certain restrictions on the content and timing of any press releases or public announcements of the transaction, and in some cases may need to follow Securities and Exchange Commission (SEC) guidelines. If either or both of the parties to the transaction are publicly traded, then the general rule is that once the essential terms of the transaction are agreed to in principle, such as through the execution of the letter of intent, there must be a public announcement. The timing and content of this announcement must be weighed carefully by the parties, including an analysis of how the announcement will affect the price of the stock. The announcement should not be made too early, or it may be viewed by the SEC as an attempt to influence the price of the stock.

Expenses/brokers. The parties should identify, where applicable, who shall bear responsibility for investment bankers’ fees, finders’ fees, legal expenses, and other costs pertaining to the transaction.

Obviously, not all deals materialize, and it is useful to know some of the reasons for failure in the early stages. Here are some of the common ones:

![]() The seller has not prepared adequate financial statements (e.g., going back at least two years and reflecting the company’s current condition).

The seller has not prepared adequate financial statements (e.g., going back at least two years and reflecting the company’s current condition).

![]() The seller and its team are uncooperative during the due diligence process.

The seller and its team are uncooperative during the due diligence process.

![]() The buyer and its team discover a “deal breaker” in the course of the due diligence (e.g., large unknown or hidden actual or contingent liabilities, such as an EPA cleanup matter).

The buyer and its team discover a “deal breaker” in the course of the due diligence (e.g., large unknown or hidden actual or contingent liabilities, such as an EPA cleanup matter).

![]() The seller has “seller’s remorse,” gets “cold feet,” or has not properly thought through its after-tax consideration or compensation.

The seller has “seller’s remorse,” gets “cold feet,” or has not properly thought through its after-tax consideration or compensation.

![]() The seller suffers from “don’t call my baby ugly” syndrome and becomes defensive when the buyer and its team find flaws (and then focus on them in the negotiation) in the operations of the business, the valuation, the loyalty of the customers, the quality of the accounts receivable, the skills of the personnel, and so on.

The seller suffers from “don’t call my baby ugly” syndrome and becomes defensive when the buyer and its team find flaws (and then focus on them in the negotiation) in the operations of the business, the valuation, the loyalty of the customers, the quality of the accounts receivable, the skills of the personnel, and so on.

![]() A strategic shift (or extenuating set of circumstances) affecting the acquisition strategy or criteria of the buyer occurs (e.g., a change in the buyer’s management team during the due diligence process).

A strategic shift (or extenuating set of circumstances) affecting the acquisition strategy or criteria of the buyer occurs (e.g., a change in the buyer’s management team during the due diligence process).

![]() The seller is inflexible on price and valuation when the buyer and its team discover problems during due diligence.

The seller is inflexible on price and valuation when the buyer and its team discover problems during due diligence.

For more on this topic, see Chapter 12, “Keeping M&A Deals on Track.”

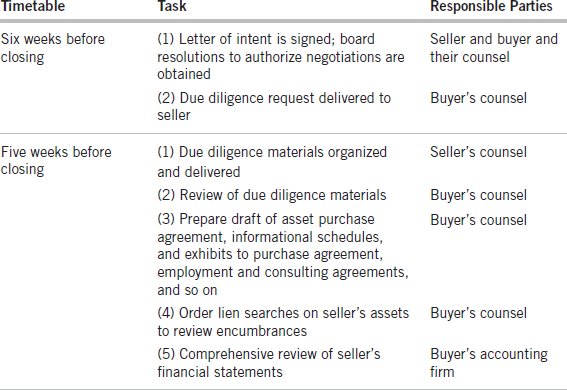

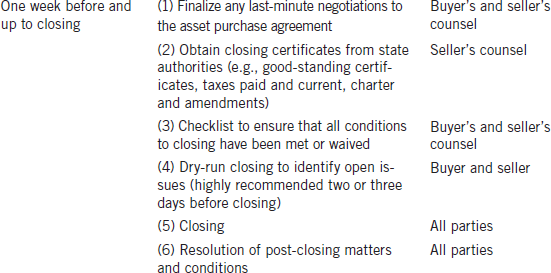

Following the execution of the letter of intent, one of the first responsibilities of the purchaser’s legal counsel is to prepare a comprehensive schedule of activities (work schedule) that will serve as a task checklist and assignment of responsibilities. This schedule should be prepared well before the due diligence discussed in Chapter 5 begins. The primary purpose of the schedule is to outline all of the events that must occur and the documents that must be prepared prior to the closing date and beyond. In this regard, purchaser’s legal counsel acts as an orchestra leader, assigning primary areas of responsibility to the various members of the acquisition team as well as to the seller and its counsel. Purchaser’s counsel must also act as a taskmaster to ensure that the timetable for closing is met. Once all tasks have been identified and assigned, and a realistic timetable for completion has been established, then a firm closing time and date can be preliminarily determined.

Naturally, the exact list of legal documents that must be prepared and the specific tasks to be outlined in the work schedule will vary from transaction to transaction, usually depending on the specific facts and circumstances of each deal, such as (1) whether the transaction is a stock or an asset purchase, (2) the form and terms of the purchase price, (3) the nature of the business being acquired, (4) the nature and extent of the assets being purchased and/or the liabilities being assumed, and (5) the sophistication of the parties and their respective legal counsel.

A sample work schedule for an asset purchase transaction that is not intended to be overly complex or comprehensive is set forth in Figure 4-3.

The collapse of Enron and the passage of Sarbanes-Oxley have forced boards of directors, particularly those at publicly traded companies, to reassess how they do M&A deals and on what basis they can represent to the shareholders that the deal is fair to all parties. Naturally, the seller’s board wants to be able to represent that it is being paid a fair price, and the buyer’s board wants to represent to its shareholders that it is not using company resources to overpay for a transaction. If the buyer intends to pay a price that is well above current market conditions, then it had better be prepared to justify its action and defend the reasons for the higher valuation. For decades, directors have sought out “fairness opinions” written by consultants, investment bankers, or accountants that justify the transaction and its price parameters in order to satisfy their duties and obligations to the shareholders. But fairness opinion practices have come under scrutiny as poor analysis, conflicts of interest, and a lack of due diligence to support the opinions have begun to surface. Some boards have tried to correct previously flawed practices by making sure that (1) the author of the fairness opinion is truly independent (i.e., is not affiliated with any party to the deal, either directly or indirectly), (2) the author of the fairness opinion is not just “telling the directors what they want to hear” in hopes of obtaining business from the company down the road (the “beholden to management” dilemma), (3) success fees as a component of the compensation paid to the author of the opinion have been removed, and (4) second and third opinions to the core fairness opinion have been obtained. The process for selecting the firm to draft the fairness opinion should be competitive and well documented and all potential conflicts should be avoided. The process should be especially rigorous if the transaction is high profile, controversial, or in any way contested, especially if key shareholders of the seller have expressed concern that their shares have been undervalued and/or if the shareholders of the buyer do not understand or agree with the underlying value proposition of the deal as proposed.