Risk means more things can happen than will happen.

ELROY DIMSON

Investing consists of exactly one thing: dealing with the future. And because none of us can know the future with certainty, risk is inescapable. Thus, dealing with risk is an essential—I think the essential—element in investing. It’s not hard to find investments that might go up. If you can find enough of these, you’ll have moved in the right direction. But you’re unlikely to succeed for long if you haven’t dealt explicitly with risk. The first step consists of understanding it. The second step is recognizing when it’s high. The critical final step is controlling it. Because the issue is so complex and so important, I devote three chapters to examining risk in depth.

PAUL JOHNSON: Marks’s discussion of risk in chapters 5, 6, and 7 is the most comprehensive and complete I have ever seen in an investment book. Furthermore, his is the best articulation of risk I have encountered in any discussion or publication. These three chapters are the highlight of the book for me.

Why do I say risk assessment is such an essential element in the investment process? There are three powerful reasons.

First, risk is a bad thing, and most level-headed people want to avoid or minimize it. It is an underlying assumption in financial theory that people are naturally risk-averse, meaning they’d rather take less risk than more. Thus, for starters, an investor considering a given investment has to make judgments about how risky it is and whether he or she can live with the absolute quantum of risk.

Second, when you’re considering an investment, your decision should be a function of the risk entailed as well as the potential return. Because of their dislike for risk, investors have to be bribed with higher prospective returns to take incremental risks. Put simply, if both a U.S. Treasury note and small company stock appeared likely to return 7 percent per year, everyone would rush to buy the former (driving up its price and reducing its prospective return) and dump the latter (driving down its price and thus increasing its return). This process of adjusting relative prices, which economists call equilibration, is supposed to render prospective returns proportional to risk.

So, going beyond determining whether he or she can bear the absolute amount of risk that is attendant, the investor’s second job is to determine whether the return on a given investment justifies taking the risk. Clearly, return tells just half of the story, and risk assessment is required.

Third, when you consider investment results, the return means only so much by itself; the risk taken has to be assessed as well. Was the return achieved in safe instruments or risky ones? In fixed income securities or stocks? In large, established companies or smaller, shakier ones? In liquid stocks and bonds or illiquid private placements? With help from leverage or without it? In a concentrated portfolio or a diversified one?

Surely investors who get their statements and find that their accounts made 10 percent for the year don’t know whether their money managers did a good job or a bad one. In order to reach a conclusion, they have to have some idea about how much risk their managers took. In other words, they have to have a feeling for “risk-adjusted return.”

JOEL GREENBLATT: However, many individual and institutional investor decisions are based on this number, which has little explanatory or predictive value.

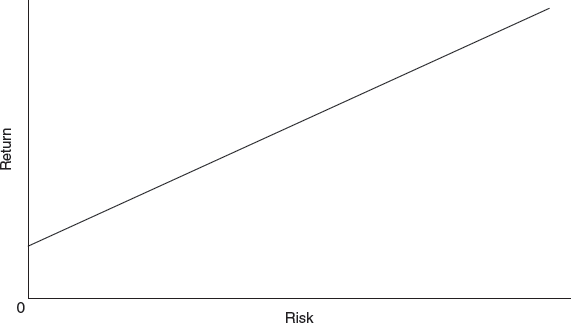

Figure 5.1

It is from the relationship between risk and return that arises the graphic representation that has become ubiquitous in the investment world (figure 5.1). It shows a “capital market line” that slopes upward to the right, indicating the positive relationship between risk and return. Markets set themselves up so that riskier assets appear to offer higher returns. If that weren’t the case, who would buy them?

The familiar graph of the risk-return relationship is elegant in its simplicity. Unfortunately, many have drawn from it an erroneous conclusion that gets them into trouble.

Especially in good times, far too many people can be overheard saying, “Riskier investments provide higher returns. If you want to make more money, the answer is to take more risk.” But riskier investments absolutely cannot be counted on to deliver higher returns. Why not? It’s simple: if riskier investments reliably produced higher returns, they wouldn’t be riskier!

The correct formulation is that in order to attract capital, riskier investments have to offer the prospect of higher returns, or higher promised returns, or higher expected returns. But there’s absolutely nothing to say those higher prospective returns have to materialize.

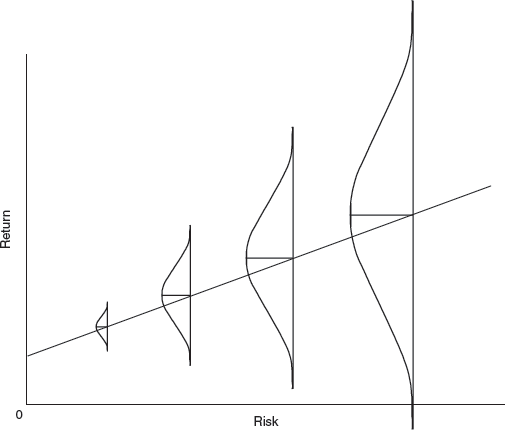

The way I conceptualize the capital market line makes it easier for me to relate to the relationship underlying it all (figure 5.2).

Figure 5.2

JOEL GREENBLATT: This graph is a helpful way to visualize risk vs. return. Another helpful way to think about the probability distribution of future returns is to remember that the outcome distribution of these possible returns is not, in reality, normally distributed.

HOWARD MARKS: Investing requires us to deal with the future. If the future were knowable by all, investing wouldn’t be very challenging (or, consequently, very profitable). Because it’s not, my final key theme surrounds the importance of understanding uncertainty. The graphic above illustrates the essence of “riskier” investments. This isn’t an abstraction; riskier investments involve greater uncertainty regarding the outcome, as well as the increased likelihood of some painful ones.

Riskier investments are those for which the outcome is less certain. That is, the probability distribution of returns is wider. When priced fairly, riskier investments should entail:

• higher expected returns,

• the possibility of lower returns, and

• in some cases the possibility of losses.

The traditional risk/return graph (figure 5.1) is deceptive because it communicates the positive connection between risk and return but fails to suggest the uncertainty involved. It has brought a lot of people a lot of misery through its unwavering intimation that taking more risk leads to making more money.

I hope my version of the graph is more helpful.

PAUL JOHNSON: Marks’s discussion of the relationship between risk and return offers important clarity, particularly in this comparison of figures 5.1 and 5.2. The additional insight offered by figure 5.2 leads to a much clearer view of the proper way to relate risk and return than that presented in the more common figure 5.1.

It’s meant to suggest both the positive relationship between risk and expected return and the fact that uncertainty about the return and the possibility of loss increase as risk increases.

“RISK,” JANUARY 19, 2006

PAUL JOHNSON: So well said! Marks’s dismissal of risk’s equaling volatility, favored by academics and some practitioners, is excellent. Instead, Marks offers a much more insightful definition of risk.

JOEL GREENBLATT: Comparing the risk of permanent loss of capital to potential reward is one of the most important concepts in investing. Yet Marks points out that many academic versions of risk, which are merely the measure of volatility relative to returns, miss much of the point. They do not reflect most investors’ perception of risk.

Our next major task is to define risk. What exactly does it involve? We can get an idea from its synonyms: danger, hazard, jeopardy, peril. They all sound like reasonable candidates, and pretty undesirable.

And yet, finance theory (the same theory that contributed the risk-return graph shown in figure 5.1 and the concept of risk-adjustment) defines risk very precisely as volatility (or variability or deviation). None of these conveys the necessary sense of “peril.”

According to the academicians who developed capital market theory, risk equals volatility, because volatility indicates the unreliability of an investment. I take great issue with this definition of risk.

It’s my view that—knowingly or unknowingly—academicians settled on volatility as the proxy for risk as a matter of convenience. They needed a number for their calculations that was objective and could be ascertained historically and extrapolated into the future. Volatility fits the bill, and most of the other types of risk do not. The problem with all of this, however, is that I just don’t think volatility is the risk most investors care about.

There are many kinds of risk. … But volatility may be the least relevant of them all. Theory says investors demand more return from investments that are more volatile. But for the market to set the prices for investments such that more volatile investments will appear likely to produce higher returns, there have to be people demanding that relationship, and I haven’t met them yet. I’ve never heard anyone at Oaktree—or anywhere else, for that matter—say, “I won’t buy it, because its price might show big fluctuations,” or “I won’t buy it, because it might have a down quarter.” Thus, it’s hard for me to believe volatility is the risk investors factor in when setting prices and prospective returns.

Rather than volatility, I think people decline to make investments primarily because they’re worried about a loss of capital or an unacceptably low return. To me, “I need more upside potential because I’m afraid I could lose money” makes an awful lot more sense than “I need more upside potential because I’m afraid the price may fluctuate.” No, I’m sure “risk” is—first and foremost—the likelihood of losing money.

“RISK,” JANUARY 19, 2006

The possibility of permanent loss is the risk I worry about, Oaktree worries about and every practical investor I know worries about.

PAUL JOHNSON: I would go so far as to say that the risk of permanent capital loss is the only risk to worry about.

But there are many other kinds of risk, and you should be conscious of them, because they can either (a) affect you or (b) affect others and thus present you with opportunities for profit.

Investment risk comes in many forms. Many risks matter to some investors but not to others, and they may make a given investment seem safe for some investors but risky for others.

• Falling short of one’s goal—Investors have differing needs, and for each investor the failure to meet those needs poses a risk. A retired executive may need 4 percent per year to pay the bills, whereas 6 percent would represent a windfall. But for a pension fund that has to average 8 percent per year, a prolonged period returning 6 percent would entail serious risk. Obviously this risk is personal and subjective, as opposed to absolute and objective. A given investment may be risky in this regard for some people but riskless for others. Thus this cannot be the risk for which “the market” demands compensation in the form of higher prospective returns.

• Underperformance—Let’s say an investment manager knows there won’t be more money forthcoming no matter how well a client’s account performs, but it’s clear the account will be lost if it fails to keep up with some index. That’s “benchmark risk,” and the manager can eliminate it by emulating the index. But every investor who’s unwilling to throw in the towel on outperformance, and who chooses to deviate from the index in its pursuit, will have periods of significant underperformance. In fact, since many of the best investors stick most strongly to their approach—and since no approach will work all the time—the best investors can have some of the greatest periods of underperformance. Specifically, in crazy times, disciplined investors willingly accept the risk of not taking enough risk to keep up. (See Warren Buffett and Julian Robertson in 1999. That year, underperformance was a badge of courage because it denoted a refusal to participate in the tech bubble.)

JOEL GREENBLATT: In the decade of the 2000s, 79 percent of the investment managers who ended up in the top quartile of performance spent at least three years in the bottom quartile (source: Davis Advisors). Most investors chase the hot fund and don’t stick with managers who underperform over the short term.

• Career risk—This is the extreme form of underperformance risk: the risk that arises when the people who manage money and the people whose money it is are different people. In those cases, the managers (or “agents”) may not care much about gains, in which they won’t share, but may be deathly afraid of losses that could cost them their jobs. The implication is clear: risk that could jeopardize return to an agent’s firing point is rarely worth taking.

• Unconventionality—Along similar lines, there’s the risk of being different. Stewards of other people’s money can be more comfortable turning in average performance, regardless of where it stands in absolute terms, than with the possibility that unconventional actions will prove unsuccessful and get them fired. … Concern over this risk keeps many people from superior results, but it also creates opportunities in unorthodox investments for those who dare to be different.

• Illiquidity—If an investor needs money with which to pay for surgery in three months or buy a home in a year, he or she may be unable to make an investment that can’t be counted on for liquidity that meets the schedule. Thus, for this investor, risk isn’t just losing money or volatility, or any of the above. It’s being unable when needed to turn an investment into cash at a reasonable price. This, too, is a personal risk.

“RISK,” JANUARY 19, 2006

Now I want to spend a little time on the subject of what gives rise to the risk of loss.

First, risk of loss does not necessarily stem from weak fundamentals. A fundamentally weak asset—a less-than-stellar company’s stock, a speculative-grade bond or a building in the wrong part of town—can make for a very successful investment if bought at a low-enough price.

Second, risk can be present even without weakness in the macroenvironment. The combination of arrogance, failure to understand and allow for risk, and a small adverse development can be enough to wreak havoc. It can happen to anyone who doesn’t spend the time and effort required to understand the processes underlying his or her portfolio.

Mostly it comes down to psychology that’s too positive and thus prices that are too high. Investors tend to associate exciting stories and pizzazz with high potential returns. They also expect high returns from things that have been doing well lately. These souped-up investments may deliver on people’s expectations for a while, but they certainly entail high risk. Having been borne aloft on the crowd’s excitement and elevated to what I call the “pedestal of popularity,” they offer the possibility of continued high returns, but also of low or negative ones.

HOWARD MARKS: The riskiest things: The most dangerous investment conditions generally stem from psychology that’s too positive. For this reason, fundamentals don’t have to deteriorate in order for losses to occur; a downgrading of investor opinion will suffice. High prices often collapse of their own weight.

Theory says high return is associated with high risk because the former exists to compensate for the latter. But pragmatic value investors feel just the opposite: They believe high return and low risk can be achieved simultaneously by buying things for less than they’re worth. In the same way, overpaying implies both low return and high risk.

Dull, ignored, possibly tarnished and beaten-down securities—often bargains exactly because they haven’t been performing well—are often the ones value investors favor for high returns. Their returns in bull markets are rarely at the top of the heap, but their performance is generally excellent on average, more consistent than that of “hot” stocks and characterized by low variability, low fundamental risk and smaller losses when markets do badly. Much of the time, the greatest risk in these low-luster bargains lies in the possibility of underperforming in heated bull markets. That’s something the risk-conscious value investor is willing to live with.

I’m sure we agree that investors should and do demand higher prospective returns on the investments they perceive as riskier. And hopefully we can agree that losing money is the risk people care about most in demanding prospective returns and thus in setting prices for investments. An important question remains: how do they measure that risk?

First, it clearly is nothing but a matter of opinion: hopefully an educated, skillful estimate of the future, but still just an estimate.

Second, the standard for quantification is nonexistent. With any given investment, some people will think the risk is high and others will think it’s low. Some will state it as the probability of not making money, and some as the probability of losing a given fraction of their money (and so forth). Some will think of it as the risk of losing money over one year, and some as the risk of losing money over the entire holding period. Clearly, even if all the investors involved met in a room and showed their cards, they’d never agree on a single number representing an investment’s riskiness. And even if they could, that number wouldn’t likely be capable of being compared against another number, set by another group of investors, for another investment. This is one of the reasons why I say risk and the risk/return decision aren’t “machinable,” or capable of being turned over to a computer.

Ben Graham and David Dodd put it this way more than sixty years ago in the second edition of Security Analysis, the bible of value investors: “the relation between different kinds of investments and the risk of loss is entirely too indefinite, and too variable with changing conditions, to permit of sound mathematical formulation.”

Third, risk is deceptive. Conventional considerations are easy to factor in, like the likelihood that normally recurring events will recur. But freakish, once-in-a-lifetime events are hard to quantify. The fact that an investment is susceptible to a particularly serious risk that will occur infrequently if at all—what I call the improbable disaster—means it can seem safer than it really is.

The bottom line is that, looked at prospectively, much of risk is subjective, hidden and unquantifiable.

Where does that leave us? If the risk of loss can’t be measured, quantified or even observed—and if it’s consigned to subjectivity—how can it be dealt with? Skillful investors can get a sense for the risk present in a given situation. They make that judgment primarily based on (a) the stability and dependability of value and (b) the relationship between price and value. Other things will enter into their thinking, but most will be subsumed under these two.

There have been many efforts of late to make risk assessment more scientific. Financial institutions routinely employ quantitative “risk managers” separate from their asset management teams and have adopted computer models such as “value at risk” to measure the risk in a portfolio. But the results produced by these people and their tools will be no better than the inputs they rely on and the judgments they make about how to process the inputs. In my opinion, they’ll never be as good as the best investors’ subjective judgments.

Given the difficulty of quantifying the probability of loss, investors who want some objective measure of risk-adjusted return—and they are many—can only look to the so-called Sharpe ratio. This is the ratio of a portfolio’s excess return (its return above the “riskless rate,” or the rate on short-term Treasury bills) to the standard deviation of the return. This calculation seems serviceable for public market securities that trade and price often; there is some logic, and it truly is the best we have. While it says nothing explicitly about the likelihood of loss, there may be reason to believe that the prices of fundamentally riskier securities fluctuate more than those of safer ones, and thus that the Sharpe ratio has some relevance.

JOEL GREENBLATT: In a similar light, a Sortino ratio looks at only downside volatility rather than both upside and downside volatility. However, neither measure does a good job of measuring risk of future loss.

For private assets lacking market prices—like real estate and whole companies—there’s no alternative to subjective risk adjustment.

A few years ago, while considering the difficulty of measuring risk prospectively, I realized that because of its latent, nonquantitative and subjective nature, the risk of an investment—defined as the likelihood of loss—can’t be measured in retrospect any more than it can a priori.

Let’s say you make an investment that works out as expected. Does that mean it wasn’t risky? Maybe you buy something for $100 and sell it a year later for $200. Was it risky? Who knows? Perhaps it exposed you to great potential uncertainties that didn’t materialize. Thus, its real riskiness might have been high. Or let’s say the investment produces a loss. Does that mean it was risky? Or that it should have been perceived as risky at the time it was analyzed and entered into?

If you think about it, the response to these questions is simple: The fact that something—in this case, loss—happened doesn’t mean it was bound to happen, and the fact that something didn’t happen doesn’t mean it was unlikely.

Fooled by Randomness, by Nassim Nicholas Taleb, is the authority on this subject as far as I’m concerned, and in it he talks about the “alternative histories” that could have unfolded but didn’t. There’s more about this important book in chapter 16, but at the moment I am interested in how the idea of alternative histories relates to risk.

SETH KLARMAN: This is where top-notch management may also make a difference. Astute managers will be aware of the many risks that could threaten their businesses and will take action to mitigate or avoid them. Poor managers will fail to notice risks or fail to act, thereby subjecting their firms to avoidable loss.

In the investing world, one can live for years off one great coup or one extreme but eventually accurate forecast. But what’s proved by one success? When markets are booming, the best results often go to those who take the most risk. Were they smart to anticipate good times and bulk up on beta, or just congenitally aggressive types who were bailed out by events? Most simply put, how often in our business are people right for the wrong reason? These are the people Nassim Nicholas Taleb calls “lucky idiots,” and in the short run it’s certainly hard to tell them from skilled investors.

The point is that even after an investment has been closed out, it’s impossible to tell how much risk it entailed. Certainly the fact that an investment worked doesn’t mean it wasn’t risky, and vice versa. With regard to a successful investment, where do you look to learn whether the favorable outcome was inescapable or just one of a hundred possibilities (many of them unpleasant)? And ditto for a loser: how do we ascertain whether it was a reasonable but ill-fated venture, or just a wild stab that deserved to be punished?

Did the investor do a good job of assessing the risk entailed? That’s another good question that’s hard to answer. Need a model? Think of the weatherman. He says there’s a 70 percent chance of rain tomorrow. It rains; was he right or wrong? Or it doesn’t rain; was he right or wrong? It’s impossible to assess the accuracy of probability estimates other than 0 and 100 except over a very large number of trials.

“RISK,” JANUARY 19, 2006

And that brings me to the quotation from Elroy Dimson that led off this chapter: “Risk means more things can happen than will happen.” Now we move toward the metaphysical aspects of risk.

HOWARD MARKS: Understanding uncertainty: Dimson’s formulation reminds us of a very simple concept: that many things are possible in the future. We can’t know which of the possibilities will occur, and this uncertainty contributes to the challenge of investing. “Single-scenario” investors ignore this fact, oversimplify the task, and need fortuitous outcomes to produce good results.

Perhaps you recall the opening sentence of this chapter: Investing consists of exactly one thing: dealing with the future. Yet clearly it’s impossible to “know” anything about the future. If we’re farsighted we can have an idea of the range of future outcomes and their relative likelihood of occurring—that is, we can fashion a rough probability distribution. (On the other hand, if we’re not, we won’t know these things and it’ll be pure guesswork.)

HOWARD MARKS: Understanding uncertainty: The possibility of a variety of outcomes means we mustn’t think of the future in terms of a single result but rather as a range of possibilities. The best we can do is fashion a probability distribution that summarizes the possibilities and describes their relative likelihood. We must think about the full range, not just the ones that are most likely to materialize. Some of the greatest losses arise when investors ignore the improbable possibilities.

If we have a sense for the future, we’ll be able to say which outcome is most likely, what other outcomes also have a good chance of occurring, how broad the range of possible outcomes is and thus what the “expected result” is. The expected result is calculated by weighting each outcome by its probability of occurring; it’s a figure that says a lot—but not everything—about the likely future.

But even when we know the shape of the probability distribution, which outcome is most likely and what the expected result is—and even if our expectations are reasonably correct—we know about only likelihoods or tendencies. I’ve spent hours playing gin and backgammon with my good friend Bruce Newberg. Our time spent with cards and dice, where the odds are absolutely knowable, demonstrates the significant role played by randomness, and thus the vagary of probabilities. Bruce has put it admirably into words: “There’s a big difference between probability and outcome. Probable things fail to happen—and improbable things happen—all the time.” That’s one of the most important things you can know about investment risk.

JOEL GREENBLATT: When thinking about a portfolio of investments, one thing to keep in mind is that the correlation of these improbable occurrences can affect many of your investments at the same time.

While on the subject of probability distributions, I want to take a moment to make special mention of the normal distribution. Obviously investors are required to make judgments about future events. To do that, we settle on a central value around which we think events are likely to cluster. This may be the mean or expected value (the outcome that on average is expected to occur), the median (the outcome with half the possibilities above and half below) or the mode (the single most likely outcome). But to cope with the future it’s not sufficient to have a central expectation; we have to have a sense for the other possible outcomes and their likelihood. We need a distribution that describes all of the possibilities.

Most phenomena that cluster around a central value—for example, the heights of people—form the familiar bell-shaped curve, with the probability of a given observation peaking at the center and trailing off toward the extremes, or “tails.” There may be more men of five feet ten inches than any other height, somewhat fewer of five feet nine inches or five feet eleven inches, a lot less of five feet three inches or six feet five inches, and almost none of four feet eight inches or seven feet. Rather than enumerating the probability of each observation individually, standard distributions provide a convenient way to summarize the probabilities, such that a few statistics can tell you everything you have to know about the shape of things to come.

The most common bell-shaped distribution is called the “normal” distribution. However, people often use the terms bell-shaped and normal interchangeably, and they’re not the same. The former is a general type of distribution, while the latter is a specific bell-shaped distribution with very definite statistical properties. Failure to distinguish between the two doubtless made an important contribution to the recent credit crisis.

In the years leading up to the crisis, financial engineers, or “quants,” played a big part in creating and evaluating financial products such as derivatives and structured entities. In many cases they made the assumption that future events would be normally distributed. But the normal distribution assumes events in the distant tails will happen extremely infrequently, while the distribution of financial developments—shaped by humans, with their tendency to go to emotion-driven extremes of behavior—should probably be seen as having “fatter” tails. Thus, when widespread mortgage defaults began to occur, events thought to be unlikely befell mortgage-related vehicles on a regular basis. Investors in vehicles that had been constructed on the basis of normal distributions, without much allowance for “tail events” (some might borrow Nassim Nicholas Taleb’s term “black swans”), often saw the wheels come off.

Now that investing has become so reliant on higher math, we have to be on the lookout for occasions when people wrongly apply simplifying assumptions to a complex world. Quantification often lends excessive authority to statements that should be taken with a grain of salt. That creates significant potential for trouble.

Here’s the key to understanding risk: it’s largely a matter of opinion. It’s hard to be definitive about risk, even after the fact. You can see that one investor lost less than another in bad times and conclude that that investor took less risk. Or you can note that one investment declined more than another in a given environment and thus say it was riskier. Are these statements necessarily accurate?

For the most part, I think it’s fair to say that investment performance is what happens when a set of developments—geopolitical, macro-economic, company-level, technical and psychological—collide with an extant portfolio. Many futures are possible, to paraphrase Dimson, but only one future occurs. The future you get may be beneficial to your portfolio or harmful, and that may be attributable to your foresight, prudence or luck.

PAUL JOHNSON: Fully understanding this insight will be a major step toward understanding investment performance and has important philosophical ramifications for investing.

The performance of your portfolio under the one scenario that unfolds says nothing about how it would have fared under the many “alternative histories” that were possible.

• A portfolio can be set up to withstand 99 percent of all scenarios but succumb because it’s the remaining 1 percent that materializes. Based on the outcome, it may seem to have been risky, whereas the investor might have been quite cautious.

• Another portfolio may be structured so that it will do very well in half the scenarios and very poorly in the other half. But if the desired environment materializes and it prospers, onlookers can conclude that it was a low-risk portfolio.

• The success of a third portfolio can be entirely contingent on one oddball development, but if it occurs, wild aggression can be mistaken for conservatism and foresight.

Return alone—and especially return over short periods of time—says very little about the quality of investment decisions. Return has to be evaluated relative to the amount of risk taken to achieve it. And yet, risk cannot be measured. Certainly it cannot be gauged on the basis of what “everybody” says at a moment in time. Risk can be judged only by sophisticated, experienced second-level thinkers.

Here’s my wrap-up on understanding risk:

Investment risk is largely invisible before the fact—except perhaps to people with unusual insight—and even after an investment has been exited. For this reason, many of the great financial disasters we’ve seen have been failures to foresee and manage risk. There are several reasons for this.

• Risk exists only in the future, and it’s impossible to know for sure what the future holds. … No ambiguity is evident when we view the past. Only the things that happened, happened. But that definiteness doesn’t mean the process that creates outcomes is clear-cut and dependable. Many things could have happened in each case in the past, and the fact that only one did happen understates the variability that existed.

• Decisions whether or not to bear risk are made in contemplation of normal patterns recurring, and they do most of the time. But once in a while, something very different happens. … Occasionally, the improbable does occur.

• Projections tend to cluster around historic norms and call for only small changes. … The point is, people usually expect the future to be like the past and underestimate the potential for change.

• We hear a lot about “worst-case” projections, but they often turn out not to be negative enough. I tell my father’s story of the gambler who lost regularly. One day he heard about a race with only one horse in it, so he bet the rent money. Halfway around the track, the horse jumped over the fence and ran away. Invariably things can get worse than people expect. Maybe “worst-case” means “the worst we’ve seen in the past.” But that doesn’t mean things can’t be worse in the future. In 2007, many people’s worst-case assumptions were exceeded.

• Risk shows up lumpily. If we say “2 percent of mortgages default” each year, and even if that’s true when we look at a multiyear average, an unusual spate of defaults can occur at a point in time, sinking a structured finance vehicle. It’s invariably the case that some investors—especially those who employ high leverage—will fail to survive at those intervals.

• People overestimate their ability to gauge risk and understand mechanisms they’ve never before seen in operation. In theory, one thing that distinguishes humans from other species is that we can figure out that something’s dangerous without experiencing it. We don’t have to burn ourselves to know we shouldn’t sit on a hot stove. But in bullish times, people tend not to perform this function. Rather than recognize risk ahead, they tend to overestimate their ability to understand how new financial inventions will work.

• Finally and importantly, most people view risk taking primarily as a way to make money. Bearing higher risk generally produces higher returns. The market has to set things up to look like that’ll be the case; if it didn’t, people wouldn’t make risky investments. But it can’t always work that way, or else risky investments wouldn’t be risky. And when risk bearing doesn’t work, it really doesn’t work, and people are reminded what risk’s all about.

“NO DIFFERENT THIS TIME,” DECEMBER 17, 2007

HOWARD MARKS: Understanding uncertainty: Investing requires us to make decisions about the future. Usually we do so by assuming it will bear a resemblance to the past. But that’s far from saying outcomes will be distributed the same as always. Unusual and unlikely things can happen, and outcomes can occur in runs (and go to extremes) that are hard to predict. Underestimating uncertainty and its consequences is a big contributor to investor difficulty.