ADVOCACY ALERT

Like everyone else, you need money to keep a roof over your head, pay your taxes, tide you through emergencies, get medical care, send your kids to college, kick back in retirement—and help some of your dreams come true.

But freelancers lack the economic protections millions rely on: unemployment insurance, group health insurance, company-matched retirement savings, as well as access to credit.

Let’s get you started on weaving your safety net. These are big subjects that fluctuate with changing laws and policies. Your needs, too, are unique and may change over time. So see this chapter as just the beginning of your explorations, ideally lessening some of the scary unknowns and prepping you for a deeper dive.

ADVOCACY ALERT

WE NEED A NEW NEW DEAL

When America moved from agriculture to industry in the mid-nineteenth century, work hours were limitless and conditions appalling. Eventually workers organized and by the 1930s leveraged change via President Franklin Delano Roosevelt’s New Deal. These laws linked the fortunes of worker and employer and spawned many worker safety nets, from minimum pay and work hours to antidiscrimination, unemployment protection, and Social Security.

But work has changed. Work relationships are fluid, not fixed. Businesses expand and contract as markets fluctuate. Workers move from job to job or gig to gig. With independent workers now some 42 million strong, we need safety nets for the new, fluid workforce. They need to be portable with the worker and affordable to the worker. Otherwise this huge and growing economic sector won’t be self-sustaining—a disaster for them and the economy.

As medicine advanced in the early twentieth century, so did medical costs. The solution? Share the burden: Healthy people could regularly pay a certain amount, or premium, to help defray costs for the sick, ensuring the same for themselves when they needed care. This distributed costs over a large group, or risk pool, to help the subgroup needing the care.

Businesses eventually bought into these plans to attract workers. Thus were born the private health insurance industry and the employer health benefit system.

The two keys here: a large enough risk pool to keep premiums affordable, and employers helping absorb costs. You can see how the system becomes strained as people live longer, requiring more medical care; costs for treating chronic illnesses and for preventive care are added; the healthy stop buying coverage when job loss or rising premiums make it unaffordable; and the risk pool shrinks, driving prices even higher. Insurers handled these pressures by reducing coverage for preventive care, raising premiums and deductibles (the amount you pay before insurance kicks in), restricting choices, and raising prices or denying coverage for the sick (preexisting conditions).

The result was high-deductible “catastrophic care” insurance mainly covering only major medical issues, exorbitant plans for those with preexisting conditions, mazes of exceptions and limitations, and lots of people with inadequate, unaffordable, or no coverage.

Independent, temp, and part-time workers have had to navigate this maze alone and have generally paid much higher premiums than employees, whose costs (even if rising) are shared by their employers. Unless you live in a state with lower premiums or have a partner with employer-sponsored coverage, you’re on your own. Many have rolled the dice and gone without.

Few disagree that we need an affordable model that better covers routine care and major medical problems. But that’s where consensus ends. Here is a snapshot of where things are today, the changes afoot, and the imperfect choices facing freelancers. Note: The system is undergoing major changes, so keep abreast of the news and verify when you research plans. And check the Appendix for some useful insurance resources to help you along.

Heraclitus was one wise old Greek, but even he probably couldn’t have imagined how well his words would describe our health insurance situation. When the Patient Protection and Affordable Care Act (PPACA), aka the Affordable Care Act (ACA) became law in March 2010, this huge, heatedly debated piece of legislation mandated phased-in changes over a four-year period aimed at overhauling the mammoth U.S. health insurance system.

The law’s too big to detail fully here, but significant features include greater oversight of insurance rate increases; start-up loans to fund nonprofit, “consumer operated and oriented plans” called CO-OPs (Freelancers Union received funding to set up CO-OPs in New York, New Jersey, and Oregon); the creation of health insurance exchanges where consumers can comparison shop for plans, encouraging competition among insurers (each state will have an exchange, so look up yours and check to see if your state has a CO-OP); prohibition against insurers denying coverage to those with preexisting conditions; tax credits for small business and individuals to encourage coverage; and, in 2014, mandatory health insurance for all.

Although debate continues about the Affordable Care Act and its final form is uncertain, the phase-in has begun, and some say those effects are irreversible.

For complete information about the Affordable Care Act and much else on health insurance (including options for the self-employed), log onto HealthCare.gov (healthcare.gov), a federal government website managed by the U.S. Department of Health and Human Services.

New law or no, here are some ways to think about your health insurance needs and handle costs.

Talk their talk. Check these glossaries: one via the Bureau of Labor Statistics: Definitions of Health Insurance Terms (bls.gov) and a Health Insurance Glossary from the Health Insurance Resource Center (healthinsurance.org).

Get specific about your health and medical needs. Some examples:

List the medical care you’ve received in recent years: what, how often, and the cost.

List your doctors. How important is it to you to have free choice of docs and/or keep the ones you have?

Are you hoping to have kids in the not-too-distant future? You’ll need a plan with maternity coverage.

Already have a family or getting on in midlife? You may want good prescription coverage.

Consider your location. Living costs and risk factors from state to state affect premium costs. Thinking about moving? Check out health insurance alongside real estate listings. One place to research health insurance info state by state is on the Health Insurance Resource Center website: State-specific Health Insurance Resources (healthinsurance.org).

Consider your finances. High-deductible insurance with lower monthly premiums shifts more of the everyday medical expenses to you while covering more of the costs for medical events that can devastate your finances. You might consider a high-deductible plan if you don’t need to see doctors much and mainly want to ensure coverage for major medical situations. While you don’t want to undershoot your coverage, you don’t want to pay for coverage you won’t be using.

Comparison shop. That’s easier than it used to be, thanks to websites—eHealthInsurance (ehealthinsurance.com), GoHealth (gohealthinsurance.com), or InsureMonkey (insuremonkey.com), for example—that can help you start looking at your options. Absolutely read the fine print. If you use an insurance broker, find someone you trust—ask close friends and family for recommendations.

Take your tax breaks. See Chapter 15 for details, talk to your accountant, and see Health Savings Accounts (HSAs): Pay Your Medical Bills and Save on Taxes, below.

Haggle some; check their math. Let your docs know you’re open to discussing ways to save. Research costs (obviously price isn’t the only factor). If you’re hit with a charge you have reason to think is high, talk it through, and/or see if they’re open to a payment arrangement.

Do an annual insurance checkup. Have your health status or medical needs changed? Are better plans available?

If you have a high-deductible health plan, you may qualify to open an HSA, which can help you save in two expensive areas of freelance life. Briefly:

You set up the account with a bank, insurance company, or brokerage firm offering HSAs. You fund it with money you use purely for paying medical expenses (not your plan deductible). That money is tax-deductible and its earnings tax-free. Any leftover balance carries over to the next year(s).

There are caps on contributions (and penalties if you break any of the rules). Check out offerings, compare fees, and talk to your accountant and to people who have HSAs. For important information about HSAs and more, see IRS Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans.

Since they bring a large risk group under one plan, large employers have leverage to get competitive costs and choices. They foot a big chunk of the costs, too. Group plans require that everyone be covered at the same cost, including those with preexisting conditions. Employees might also have access to dental, disability, and life insurance.

The difference between small employer group insurance and large employer group insurance is the difference between small and large risk pools. The smaller the group, the more costly the entire plan becomes, should there be significant illness in the group. Result: possibly fewer plan options and higher overall costs.

Some professional and other groups (alumni groups, unions, et cetera) offer health insurance to members through an insurer. These can include what some call affinity plans. Rates may or may not be lower and choices may be narrower, so research the insurer, do your comparison shopping, and weigh the fit with your needs.

Also check whether your local chamber of commerce or other local nonprofits offer plans.

If you, private citizen, buy health insurance on the open market, as a tiny risk pool of one, you’ll generally pay higher premiums, have more limited choices, and you may have a harder time being accepted.

You may be able to qualify as a small employer (or “group-of-one”) in some states. Check your state department of insurance. To find yours, try the state web map on the National Association of Insurance Commissioners (NAIC) State Web Map (naic.org). Or check the Kaiser Family Foundation’s State Health Facts website (statehealthfacts.org; search term: Small Group Health Insurance Market Guaranteed Issue).

ANOTHER GROUP OPTION

Offering affordable health insurance to freelancers was one of the Freelancers Union’s first goals. Today, we’re proud to offer health insurance to Freelancers Union members in New York state through our own social-purpose insurance company called Freelancers Insurance Company (FIC). We also are starting the first “medical home” for freelancers, slated to open in January 2013. This new model emphasizes primary care, in which your doctor, nurse practitioner, or health coach work as a team to keep you healthy. In addition, they will reach out to any specialist you might see to help coordinate your care and medications.

Our risk pool size lets us offer competitive rates and options to low- and high-risk participants, similar to large employers. (We also offer dental and disability insurance, which you generally can’t get on the open market without significant added expense.) Because the risk pool is a specific group—freelancers—we also work to tailor the program to their needs.

We aim to combine the lower costs and greater choice of large-employer plans with the member-focused aspects of association models. And since FIC has no private shareholders, it’s answerable only to the nonprofit Freelancers Union, its members, and the funders who hold it accountable for fulfilling specific principles of social entrepreneurship. While it’s not perfect, it’s an impressively large working model of a community-based, privately funded system of health insurance delivery that’s more responsive to members’ needs, more comprehensive and affordable than they’d find elsewhere, and portable with the worker.

This year Freelancers Union was chosen to receive loans to establish nonprofit health insurance companies called CO-OPs (consumer operated and oriented plans) in New York, New Jersey, and Oregon. We’re excited to offer health care to even more consumers—freelancers and nonfreelancers alike.

If finances stress you out, join the crowd. Lots of us aren’t great with money—and maybe less rational than we think.

In his book Predictably Irrational, behavioral economist Dan Ariely tells how he and two colleagues asked people to choose between a delectable Lindt chocolate truffle for fifteen cents or a tasty but more commonplace Hershey’s Kiss for one cent. Approximately 73 percent chose the truffle, correctly surmising an excellent value for the price. Around 27 percent chose the Hershey’s Kiss.

Then the researchers lowered each price by one cent: truffle for fourteen cents; Kiss for free. And logic promptly fled: The 27 percent choosing the Kiss ballooned to around 69 percent, while the truffle’s popularity plummeted to 31 percent. These results may not surprise you if you’ve ever shopped Black Friday and know firsthand how quickly humans can ditch rational thought about money.

Don’t know much about personal finance? Join the crowd again. Most of us are self-taught. Yet we all need financial stability—especially freelancers working without a net—and especially if you want the things financial health can buy, such as a home mortgage or a business loan (both harder for freelancers to get with their irregular income).

The financial health equation is the inverse of the (only slightly more dreaded) weight loss equation:

less input (eat fewer calories) + more output (get more exercise) = weight loss

more input (earn and save more) + less output (spend less) = financial gain

Financial decisions are hugely personal and depend on multiple factors, but we’ll unpack some key financial stability principles that can help make the peaks and valleys of freelancing less frequent and steep. You’ll also find selected finance resources in the Appendix. It’s just the tip of the iceberg, so take things step by step and know you can find whatever you need to know.

To take better control of your finances and make money decisions from a calm, clear place, try keeping accounts at one bank to streamline tracking and transferring funds. Or have a physical-bank checking account and several online-bank accounts. Compare services and interest rates. Some people find that using an online budget site such as Mint (mint.com) that aggregates their account info in one place really helps them oversee things.

Personal finance software and online budgeting services and tools can also help eliminate guesswork and calculations. Read reviews and ask other freelancers what they use. Often you can just plug in numbers without personal info, but in cases where you do need to share more info, make sure you feel comfortable providing any account data an online service may require, vet its reputation and security record, and understand its security and privacy policies and practices (remember, these can change). Speaking of security, don’t instruct your personal computer to remember passwords for financial accounts, and keep your computer security software current.

Also, set aside a little time each week to deal with money issues. Do your bookkeeping, and then a little more: Read something about money or check out some financial tools online. You’ll learn a lot over time.

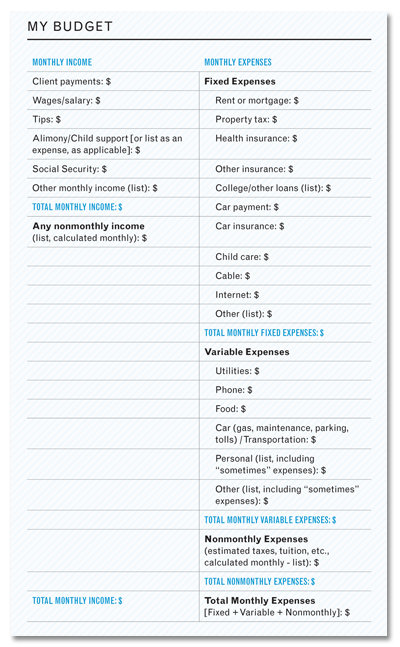

Your budget will tell you exactly how much you need to meet your expenses and how much you can green-light for treats. It’s key to managing money stress. What follows is one approach.

This is the output part. The My Budget chart below will help you chart where your money goes. Customize it with your own categories or do a couples version. Look at examples of budgets online. You can work pencil-to-paper or use digital budgeting tools (type “budgeting software” or “online budget tools” into your browser for some options).

Expenses fall in two big buckets:

1 fixed expenses, where the amounts don’t change (example: mortgage or rent payment); and

2 variable expenses (example: food bill), which do.

Many expenses are paid monthly. Some, such as estimated taxes or tuition, might be paid quarterly, semiannually, or annually. Some, such as child care, may be paid weekly.

For longer-cycle payments, calculate a monthly amount. For weekly fixed expenses, multiply by four for a monthly total.

For variable expenses, average several weeks’ or months’ worth of bills or receipts.

Finally, there are “sometimes” expenses: They don’t happen regularly, but they happen! A few examples: haircuts (yours; the dog’s), travel, medical bills (yours; the dog’s), gifts, eating out. Look at half a year’s worth or more of your bank and credit card records. Make a list. Calculate an average for each.

Fill in your chart.

Total everything up.

Uncover your eyes.

This is the minimum amount (assuming no changes in your spending habits and no unanticipated expenses . . . right) you need each month to meet your living expenses.

Now for the input part. Do you know what you’ve earned so far this year? With your budget, you can stay on top of your income.

Want an estimated version? Average your earnings over the past several months or pull last year’s tax return and figure a monthly average.

Want a real-time version? Enter your income so far this month. For a family budget, include your mate’s income, too.

If you keep a running tab of your income over the month, you’ll spot any looming shortfall between your income and your expenses. Does that happen a lot? Good to know. Maybe you need to:

• Reduce expenses

• Raise rates

• Increase client volume

• Negotiate more frequent payments

• Prospect for Blue Chips

• Develop a higher-paying specialty or

• All of the above

Keeping a monthly budget lets you see how your career is going. You can compare by month or year (trending up? down? busy season better or worse?). You can even forecast income/saving needs (how much money will I need per month to hire a babysitter three afternoons a week . . . or what about taking scuba lessons?). Need some help getting a handle on things? Maybe a professional bookkeeper can help you get your budgeting and record keeping system up and rolling, and work with you on how to monitor it.

I hear you saying, “A monthly budget won’t work for me, because my freelance income is so inconsistent from month to month.” Sit tight. We’re getting to that.

Please download a PDF of this monthly budget here:

workman.com/ebookdownloads

MONEY ALERT

YOUR WEEKLY ALLOWANCE

In your monthly budget, you calculated personal and “sometimes” expenses. These include necessities like toothpaste—and niceties like clothes, going out, ordering in, and gifts. You’ve also budgeted for groceries. If your numbers are based in reality, you should be able to figure a weekly spending budget and keep to it. Obviously, charged and debited purchases count against it, too.

And don’t thank the banks for putting ATMs on every corner. They profit from your spending. “I hate paying ATM fees, so I walk to a branch where I can use the ATM for free. Just going that extra distance makes me more cautious about spending.”

OK, so somehow with your episodic income, you need to pay your monthly bills, save for taxes, build a safety net for dry time and emergencies, save for your retirement—oh, and have some fun.

If you’ve already got a method that’s working for you, great! The approach below is one way to organize your finances so you’re paying your expenses and saving for your future. To explore others, check out personal finance books and resources, or assign a few among your freelancers group and have folks report on them.

To achieve financial stability, you need to continually fund these four accounts:

1 Expenses

2 Taxes

3 Emergencies

4 Retirement

When a payment comes in, deposit a percentage into each account. You might keep your expenses account at a physical bank for check writing and ATM access. Depending on that bank’s minimums, fees, and interest rates and your comfort level with having accounts online, you might decide to make others online bank accounts that you transfer money into (the retirement money will eventually be parked in retirement investments—see Retirement, below).

The percentages you choose are up to you and might change. But taxes are a certainty, so get that percentage nailed down. Absolutely, positively attend to funding your tax account. The last thing you want after working hard to earn your income is to be in debt to the IRS. They tend to keep track of these things, meaning that the interest and penalties will just accrue . . . and accrue . . . as will what you’ll pay an accountant to untangle the mess. So find out your tax bracket from your accountant. He or she might approximate this based on your tax returns of the past several years and your anticipated income. You could even fine-tune it quarterly, as you pay your estimated taxes.

If your expenses include debt to pay down, that takes precedence and will affect your allocations. Still, really try to put some amount, however small, into your emergencies and retirement accounts. Those two accounts are your future debt fighters.

Initially, you might focus on building your expenses and emergencies accounts, with a smaller amount for retirement; then change the mix as the accounts grow or reach goal amounts.

Goal amounts depend on your situation. Your emergencies account goal might depend on the economy, your worst-case dry-time scenario, your industry’s payment schedules, and your personal needs. Opinions vary, but imagine how amazing you’d feel to have at least six to nine months’ worth of expenses on tap for emergencies.

For your retirement account, your goals may depend on which retirement options you choose and your age, among other factors.

If your income is very episodic and you get a fat check that’ll cover your monthly expenses, you might deposit the necessary amount in your expenses account, fund your taxes account, and divvy up the remainder over the other two. This can be a great peace-of-mind strategy.

If you’re waiting for a big payment, you can anticipate and bridge the income gap by changing your percentages ahead of time, shifting more paycheck income to your expenses account.

Things might still be touch and go while you build your accounts, but in time you’ll have enough in your expenses account to pay your bills even if the actual checks received in a given month don’t actually do that. If really lean times or a major unanticipated expense hit, your emergencies account can cushion you temporarily (which you then replenish!).

The more flush you feel in good times, the more you should stick with your plan for funding your accounts. That’s your prime time for building the safety net that’ll carry you through dry time. You can even set up additional accounts to fund other goals (new computer? honeymoon?).

With this approach, you’re building the economic freedom and security essential to freelance success and well-being.

• You’re saving money, not just making ends meet.

• You’ll know when you’ve met your monthly expenses and can save extra dough or have a splurge.

• You’re building a financial safety net that empowers you to turn down crappy gigs and crazy clients, and walk away from a negotiation where you’re getting screwed.

• You’ll be better able to bounce back from a deadbeat client versus suffering deprivation, stress, and credit score harm if you can’t pay your bills.

ADVOCACY ALERT

UNEMPLOYMENT FUND FOR FREELANCERS?

While employees have unemployment insurance to help tide them over between jobs, there’s no comparable safety net to help freelancers weather a dry spell of not enough or no work—which happened to 79 percent of freelancers in our 2011 survey. Why not set up tax-advantaged unemployment savings plans through professional associations that freelancers could contribute to, lowering their tax burden while building savings they could draw on in dry time?

Avoiding credit card debt is easier said than done, and paying down debt takes patience and perseverance. Although debt issues are complex and debt recovery is a subject unto itself, here are some strategies to help you prevent debt problems or take steps to prevail.

Dump the bad old spending habits. It’s your ultimate long-term stealth move to defend against or defray debt. If you’ve got a credit card balance, quit using your credit cards. Debit cards, too. Return to a simpler, more direct relationship with your money.

Be choosy. Compare credit card services and terms (including looking for a card with no annual fee or one with a permanent lower interest rate). Visit a website that lets you compare cards, such as Bankrate (bankrate.com) or CardTrak (cardtrak.com).

Try negotiating a lower interest rate. If you’ve incurred some interest charges but have a good credit history and payment record, try negotiating a better interest rate as a valued client.

Call. If you realize you’ve missed a bill payment deadline, send payment ASAP, call to let them know, and ask if they’ll waive any late charges. If you’ve been a reliable paying client, they might.

Shun store credit cards. They tend to have high interest rates.

Go to cash. You’ll get up close and personal with how often you throw down the plastic when you’re not throwing it down anymore.

Calculate your rate. To calculate various debt repayment scenarios—such as how long it would take to pay off X amount in credit card debt, at Y interest rate, if you pay Z amount per month, and how much would be paid in interest—plug numbers into an online debt calculator. Bankrate.com and CNNMoney.com have good ones.

Try Triple-A troubleshooting. Debt is a tough customer, so try Chapter 7’s tactic for handling tough clients:

1 Acknowledge the problem, laying out all the facts.

2 Analyze your situation.

3 Act to formulate a plan to pay down the debt, budget yourself through the crisis, and repair your credit over time.

Think of your credit report as your financial report card and your credit score as your grade. Your credit report documents your bill-paying reliability, among other aspects of your credit history. Your credit score, called a FICO score after its originator, the Fair Isaac Corporation, is a calculation of your credit risk based on multiple elements, including how much debt you’re carrying and how you’ve paid past debts. The score tops out at 850. These days, you’re wise to shoot for a score of more than 750.

While getting your credit score entails paying a fee, the Fair Credit Reporting Act (FCRA) mandates that you be allowed to obtain a free copy of your credit report from each of the three nationwide credit reporting companies (Equifax, Experian, and TransUnion) once every twelve months. You can get all three at once (it can be useful to compare them) or order one at a time, over time (useful for tracking changes)—your call. The companies have centralized this process:

Online: Visit AnnualCreditReport.com (annualcreditreport.com) and follow the instructions to complete and submit the request form.

By phone: Call (toll-free) 877-322-8228

By mail: Complete the Annual Credit Report Request Form and mail to:

Annual Credit Report Request Service

P.O. Box 105281

Atlanta, GA 30348-5281

If you need another copy within a twelve-month period, you can buy one by contacting:

Equifax 800-685-1111 (equifax.com)

Experian 888-397-3742 (experian.com)

TransUnion 800-888-4213 (transunion.com)

There are other circumstances when you can get a free report, including if you’re denied credit or insurance because of material in the report. For details, see the Federal Trade Commission website (“Facts for Consumers: How to Dispute Credit Report Errors”; ftc.gov).

Note: Getting your report too often can actually lower your score. Tip: If you’re getting a loan or refinancing, see if you can get a copy of your report from the lender (since they’ll have one), rather than requesting your own.

If the report contains negative-but-true material, the unfortunate reality is that much of it can stay on the report for around seven years (some items longer, or with no time limit).

If there’s information in a credit report that’s inaccurate or incomplete, the FCRA says the credit reporting company and the entity that provided the information are responsible for correcting it. For basic guidelines on how to proceed, visit the Federal Trade Commission website: “Facts for Consumers: How to Dispute Credit Report Errors.” (ftc.gov/bcp/edu/pubs/consumer/credit/cre21.shtm). Since this process can take time, it’s a good idea to review your reports well ahead of any activity that would involve a credit check (for example, applying for a loan or buying insurance).

Bottom line, this is the report lenders will see, whether or not you agree with it. So handle any issues you find and do what you can to improve your score.

If you’re denied credit or offered less favorable terms on the basis of your credit history, you should receive written notification, including of your right to receive a free credit report and your credit score if it was a factor in the evaluation.

For additional resources, see the Appendix.

Whether you never want to retire, fear you can’t afford to, or retirement’s still decades away, there’s a four-letter word for it: save. According to findings from the 2011 Freelancers Union Annual Independent Worker Survey of more than 2,500 independent workers from each of the fifty states, 27 percent said they had not saved anything for retirement, citing these as some of the reasons:

• 78 percent didn’t make enough money.

• 39 percent were not paid regularly.

• 19 percent didn’t understand retirement account options or how to choose one.

• 15 percent didn’t know how to choose a financial services company/provider.

You can see how pay scale and erratic payment schedules are strong factors in freelancers’ retirement savings challenges. That’s why it’s important to do your market research and skill upgrades so you can land the best clients and charge as much as possible, why we need to stop late-paying and deadbeat clients, and why budgeting to set aside some portion of your payments for retirement, even if your income is small, is an essential habit to cultivate.

Myth 1: I can’t save enough to make a difference. Truth: Wrong approach. Every deposit makes a difference, because earnings on invested income compound over time. If you’re young and have debts, saving might feel overwhelming, but time is on your side and small amounts add up.

Myth 2: It’s too late to save. Truth: Not true. Anything trumps nothing. And anything, invested and earning dividends or interest, amounts to something. Just start. Now. Adjust your retirement time line if necessary (how many people actually retire at sixty-five anymore, anyway—or even want to, if they’re doing what they love?). When I worked on a kibbutz, it was inspiring to see people joyfully working far into their late years. Freelancers, able to live and work holistically, can do that. Saving puts you in control of your future work and can mean the difference between having to work full-out forever and being able to be selective about your projects or work only as much as you want.

To play with savings scenarios, try plugging numbers into a compound interest calculator like those from Moneychimp (moneychimp.com) or Bankrate (bankrate.com).

Many employees can enroll in employer retirement funds that make money while they work. Sign a form or two, and the account is set up and contributions are carved from their paychecks before they can spend that money, executing a flawless, perfectly legal end run around the Tax Man, too. Sometimes the employer matches some portion of the contribution. If all goes well, those employees wake up at age 59½ (when they can withdraw the money without penalty) to a tidy nest egg.

Obviously, it’s not quite that simple, but it’s pretty sweet. As your own boss, you have to pull that money out of your paychecks, set up the investment accounts, and monitor them. The good news is, you have access to the same investments employers do, and, depending on your income, you might be able to save more in your tax-deferred accounts than the W-2 crowd can in their retirement plans.

Let’s assume you’ve started dividing up your checks and steadily depositing a percentage for retirement. There is a lot more you can do besides let it sit there earning the bank’s low interest rate. And, just like the employer who whisks that dough into a retirement instrument, you want to get it off-limits for spending.

Retirement plans motivate retirement saving by offering a tax advantage for setting aside money in a special account that’s invested and accrues to become your nest egg. Generally, you contribute money from your income without paying income tax on some or all of it. Generally, it stays in that account until it’s distributed to you in your later years—presumably when needed in retirement—when you pay taxes on your pretax contributions and the earnings. This reduces your taxable income in your peak earning years, deferring the tax to your later years, the assumption being that you’ll be earning less then, so your overall tax burden will be lower.

Some retirement contributions can be made after-tax, with no tax paid on the income or earnings when the money is later distributed.

With certain important exceptions, if you withdraw monies early, there are penalties atop any taxes owed.

You may have more than one retirement account so you can make more contributions. While this may restrict your ability to make some contributions or might affect their deductibility, it can give you options and flexibility in your financial planning. Some accounts allow you to take loans or early distributions for very specific reasons.

Which accounts are best for you, and how much to contribute, depends on your unique situation and how much you’re able to set aside per year (some retirement accounts let you save more; some less). There are numerous retirement plan options, but really a handful that are meaningful for most of us, and for freelancers. A selective overview follows. Use it as a jumping-off point for your own research and discussions with your accountant about your needs. See the Appendix for some useful resources.

Note: These plans are detailed, so the encapsulations below are just that. Also, the terms of these plans can and do change, so be sure to verify all terms before proceeding.

Maximum contribution per year: $5,000, plus $1,000 if you’re fifty or older.

Tax highlights: Contributions may be completely or partially tax-deductible. You pay tax on the earnings upon distribution, and on any part of the contribution that was deductible.

Withdrawal age: 59½, with a 10 percent penalty tax for early withdrawal, atop any income tax owed, with some exceptions.

Note: The IRA is essentially the government’s way of offering a retirement savings instrument to people who don’t have access to a 401(k) through employment. If your spouse (or you) has or is eligible for a 401(k) through employment, there may be limits on the deductibility of your contributions to an IRA. If you make any nondeductible contributions, talk to your accountant about the proper documentation and keep track of it, since you’ll need it later to prove that income tax isn’t due on those amounts when you withdraw them.

Maximum contribution per year: Generally $11,500, plus $2,500 if you’re fifty or older.

Matching contributions: Employer matches up to 3 percent. (See Note.)

Tax highlights: Taxes are paid when the monies are withdrawn.

Withdrawal age: 59½ with a 10 percent additional tax on early withdrawals (with some exceptions), which rises to 25 percent if done within the first two years.

Note: You can set up a SIMPLE IRA for yourself and your employees if you have 100 employees or fewer.

Maximum contribution per year: Up to 25 percent of your compensation (if a salary), or calculate your allowable contribution from your self-employment income by referring to the rate tables or worksheets in IRS Publication 560, Retirement Plans for Small Business, or discussing with your accountant. Total maximum contribution: $50,000.

Tax highlights: Your contributions are tax-deductible. Taxes are paid when the monies are withdrawn.

Withdrawal age: 59½, with a 10 percent penalty tax for early withdrawal, atop any income tax owed, with some exceptions.

Note: While there are limits if you have another defined contribution plan, in general, this plan allows you to save a sizable amount of money, so give it a close look. Setup is easy. Note that if you have employees and contribute to your own SEP IRA, you have to contribute a proportional amount for them.

Maximum contribution per year: $5,000, plus $1,000 if you’re fifty or older, though how much you can contribute is reduced or eliminated at higher levels of income and can also depend on whether traditional IRA contributions were also made.

Tax highlights: Unlike a traditional IRA, Roth IRA contributions are after-tax contributions, i.e., not tax-deductible. But distributions (earnings included) from a Roth IRA are not taxed, whereas traditional IRA distributions may be taxed.

Withdrawal age: 59½ if you reach that age at least five years from the start of the year you first contributed to a Roth IRA. There are some other instances where distribution before 59½ is penalty-free, assuming the same time frame from first contribution.

Note: While you can’t contribute as much to a Roth as to a SEP IRA and you have to pay taxes on your Roth contributions, that might be OK with you depending on your income, your ability to take other deductions, and your tax bracket—plus, you can happily anticipate tax-free distribution on the back end. Want to really boost your aftertax advantage? Have both a Roth and a SEP. Talk with your accountant.

Maximum contribution per year: In general, $17,000, plus $5,500 if you’re fifty or older (for 2012).

Tax highlights: You pay Social Security, but not income tax, when you make the contribution. Taxes are deferred until you begin withdrawing the money, when you’re taxed on both your contributions and your earnings.

Withdrawal age: 59½ with a 10 percent penalty tax for early withdrawal, atop any income tax owed, with some exceptions.

Note: Since these accounts are fairly complex and expensive to establish and maintain, they’re mainly intended for companies. If you have a 401(k) as an employee, the company may or may not match some portion of your contribution. When you leave the company, you can take your own contributions with you, but you may or may not be able to take the employer’s contributions. How much you can take, and when (called vesting), is based on the plan’s vesting schedule.

Maximum contribution per year: $17,000, plus $5,500 “catch-up contribution” if you’re fifty or older, plus up to 25 percent of your compensation (if a salary), or calculate your allowable contribution from your self-employment income by referring to the rate tables or worksheets in IRS Publication 560, Retirement Plans for Small Business, or discussing with your accountant. Total maximum contribution: $50,000, excluding the catch-up contribution.

Tax highlights: Contributions are made pretax.

Withdrawal age: 59½, with a probable 10 percent penalty tax for early withdrawal, atop any income tax owed.

Note: This 401(k) can cover a business owner who has no employees (such as a sole proprietor) or a business owner and spouse and lets you contribute as both boss and employee. Although it can allow you to save a large amount, there’s some complexity and expense involved in managing it.

Maximum contribution per year: There’s more than one type of plan. In general, for someone who’s self-employed and has only the Keogh plan: 25 percent of your allowable income, up to $50,000. Contributions to a defined-benefit Keogh plan can go much higher.

Tax highlights: Contributions are tax-deductible. Taxes are deferred until you start withdrawing the money, when you’re taxed on the contributions and earnings.

Withdrawal age: 59½, with a 10 percent penalty tax, atop any income tax owed, with some exceptions.

Note: While Keoghs let you put away a good amount of money, they aren’t as common since the more user-friendly SEP IRA has come along. The defined-benefit version is especially complex. Talk with your accountant about whether a Keogh makes sense for you.

Freelancers Union developed a riff on the employer 401(k) that offers members the easy administration, professionally selected offerings, and contribution levels that employees enjoy—plus special freelance-friendly features.

Maximum contribution per year: $17,000, plus a $5,500 “catch-up contribution” if you’re fifty or older, plus “profit-sharing contributions” of up to 25 percent of your earned income, less your contributions, capping at $50,000 (not including the catch-up contribution).

Tax highlights: Unless they’re Roth contributions (see Roth IRA), contributions are tax-deductible and taxes are deferred until you start withdrawing the money, when you’re taxed on the contributions and earnings. Some enrollment and contribution limitations apply.

Withdrawal age: 59½, with a possible 10 percent penalty tax for early withdrawal, atop any income tax owed, with some exceptions. Earnings from any Roth contributions are taxable unless you’ve been participating in Roth contributions for five years minimum.

Notes: Members can’t contribute to this plan and a SEP plan in the same calendar year. The plan’s designed as a retirement savings vehicle for the 1099 earnings of the self-employed. Freelancers Union handles administration and filing of certain forms. You have access to expert-monitored investments, and there are no minimums. You can choose to make monthly automated contributions—but you can easily change or stop them if your income fluctuates.

All of this is made financially possible through the members’ contributions, which are paid into a trust fund just for them, and through the trust fund’s earnings. It’s an example of how a group can independently set up viable systems that provide the positives of traditional models, offer better choices than group members could get on their own, but meet the individual’s needs.

To learn more, visit the Freelancers Union website (freelancersunion.org).

If you’re overseeing your own retirement saving and investing, here are some consumer-awares:

1 Start saving. Any amount. Use the system in this chapter or whatever works for you.

2 Start learning. Employees’ retirement plan investments are reviewed by financial professionals, but freelancers have to mentor themselves—and no matter where your money’s invested, you need to oversee it and at least once a year do a full performance evaluation. So read up on money, investing, retirement investing, and mutual funds. Get mutual fund recommendations from knowledgeable family and friends; pay a financial consultant for some sessions. Learn how investors weigh investment risk and reduce it by diversifying investments across a mix of lower-to-higher-risk investments. Understand how the mix commonly changes as you near retirement age, and discover your own risk tolerance level. P.S. If this diversification stuff sounds familiar, it’s because you’re applying the same logic to balancing your Freelance Portfolio. You’ve been investing in yourself all along.

3 Calculate how much you need to save for retirement. There are multiple variables to consider, from your age to your health and more. Online retirement calculators may help give you a general idea but can’t integrate the complexities of your situation. Ideally, a financial planning professional can work with you to customize a plan. While you figure things out, get started with Steps 1 and 2.

4 Decide where you want to set up your retirement investments. Track performance; compare the minimum contribution requirements and administrative costs and fees; look for a low expense ratio (individual investors, alas, can’t get the same cost breaks that employees, thanks to the size of the assets being invested, can). If all the decisions seem a little overwhelming, especially at first, one mutual fund company to consider is Vanguard (vanguard.com), which currently is the biggest and least expensive such company in the United States.

5 If you have a significant amount to invest, you might work with a broker or financial adviser. This is a service you pay for, so assess the quality of the service and amount of attention you’ll get. Ask about the adviser’s fees (which are charged atop any mutual fund fees). Ask how he or she will monitor your accounts, make decisions, assess performance, and communicate with you. Make sure you’re comfortable with the adviser’s investing philosophy and risk tolerance—and that he or she knows yours.

6 Consolidate. If you have retirement accounts from previous employers or in other places, pulling them all under one investment firm’s roof can make your retirement saving easier to monitor and manage, and less likely that an account might get lost (it happens).

7 Get involved. Suggest that your professional association invite a financial professional to give a retirement planning talk (we have them at Freelancers Union). Raise awareness about making retirement programs available through industry organizations and community groups. We need more ways to provide individual investors with the efficiencies, economies, and investment opportunities of large employer-type models.

8 Have a financial routine and streamline it where you can. Habitually divide up those checks to put a percentage in your retirement savings account. Bookmark financial websites you visit frequently.

9 Reassess. Do an annual performance review of your retirement strategy. Are your lifestyle and finance goals still the same? If not, how does that affect your strategy?

10 Make a will. A major step in protecting your assets is deciding what happens to everything you’ve carefully built for the loved ones you leave behind. If you don’t determine how you want your assets apportioned after you leave this world, Uncle Sam will. Think it through and take care of it.

For decades, college tuition has been rising at double or triple the inflation rate annually. Below are some tax-advantaged ways you can save for education.

For federal student aid options, visit the U.S. Department of Education website ED.gov (ed.gov).

If you have student loans you’re having trouble paying, the Consumer Financial Protection Bureau “Student Debt Repayment Assistant” (consumerfinance.gov) may help you understand various repayment possibilities.

If you’re considering professional training or education, see the tax info on this in Chapter 15.

Note: As with retirement savings options, these instruments are subject to change. Also, their rules or tax advantages may change if used in conjunction with other education-related instruments, tax credits, or tax-free assistance. Talk with your accountant about coordinating your education financial strategy and verify all terms. See the Appendix for selected education resources.

For kids under eighteen, you can use ESAs to save on taxes and on certain expenses for college and (currently) elementary and secondary school at eligible institutions, from kindergarten through twelfth grade. You can find out from the school if it’s eligible.

ESA contributions are made after taxes but grow tax-free (with some contribution limits, depending on income). The child’s the beneficiary. Allowable expenses may include tuition, fees, books, supplies, tutoring, uniforms, and more. When money’s withdrawn, some tax may be due. Tax and penalty may be due if money’s withdrawn for unallowable expenses.

Multiple ESAs can be set up for a child (for example: by you, a grandparent, and an aunt or uncle), but the total maximum annual contribution to all ESAs combined for that child is $2,000. You may pay an excise tax on any excess, so make sure everyone communicates about who’s contributing how much.

If the child doesn’t go to college, you may be able to change the beneficiary to certain other family members under thirty. Any monies left in the account go to the beneficiary once he or she turns thirty—and tax and with some exceptions penalty tax will be due, so check with your accountant about the rules. Also, find out how any account fees might affect performance.

Again, thank the tax code for the sexy name. These savings plans, originally incubated at the state level, are a tax-advantaged alternative to college loans. As with the ESA, there’s a beneficiary—often your child or a grandchild, but it could be almost anyone, including you. You can put money into a 529 plan to prepay or contribute toward certain “postsecondary” expenses such as tuition, fees, books and supplies, a certain amount of room and board, and more. If you use a distribution for an unallowable expense, federal, state, and penalty tax may apply. Special rules apply if the beneficiary gets a scholarship or other tax-free educational assistance.

While the money you put in isn’t deductible on your federal taxes, you generally don’t pay federal tax on the earnings when the money’s distributed. Your state may do the same, and may offer certain extra inducements to open a plan there rather than in another state. (States administer these plans.) Using your state’s plan also means you won’t pay state taxes when the money’s withdrawn.

The maximum contribution per year free of gift tax is $13,000 for an individual or $26,000 if you’re a married couple filing jointly, if you make no other gifts to the child that year. Unused funds can be refunded to you or designated for another beneficiary, according to the plan’s rules.

529 plans have underlying investments that differ across firms and states, and the ones that advisers sell usually have a sales charge (aka a load) up-front. To learn more about specific plans’ rules, contact the state agency administering the plan, and ask the educational institution(s) you’re interested in whether they participate in a plan. An excellent resource on 529 plans and other tools and info on paying for college is savingforcollege.com. For this and other resources, see the Appendix.

You get a hero’s welcome for making it through this chapter! This part of freelancing—the off-the-grid, out-on-a-limb, without-a-net part—isn’t easy. But it’s the part we all have to face if we want a better life for freelancers now and in the future.

New Mutualism—people helping people in the new economy—starts with being an intentional freelancer, making clear decisions to help yourself live a long and sustainable life as a freelancer. They might be tough decisions. But freelancers are tough. And because the work-to-income relationship is so direct for them, they quickly know when economic truths must be faced:

“I can get as much work as I want, but it’s paying less and less.”

“I spend a lot of time finding work and less time doing it.”

“One good year doesn’t predict another one.”

“You have to be disciplined enough to sense when you have to adjust your business.”

So, ask yourself: “What did I do today for my future? For my safety nets?” Maybe you read an article about money, set up your accounts so you can start dividing up your checks, resisted buying something that wasn’t in your budget, researched a new insurance plan. Start wherever you are to take control of your freelance life for your own peace of mind.

Peace of mind is also knowing you can afford the life you’re living, in good years and in lean. It’s knowing how to budget, save, invest, and work your Freelance Portfolio so you can make a plan and track your progress. Or change the plan when your goals change—for example, when you want to move, travel, have a baby, retire.

I believe freelancers, who’ve always had to do for themselves, can help themselves and one another learn, adapt, and grow through anything. So make your freelance life choices consciously. Proudly. Be an intentional freelancer. You deserve no less.