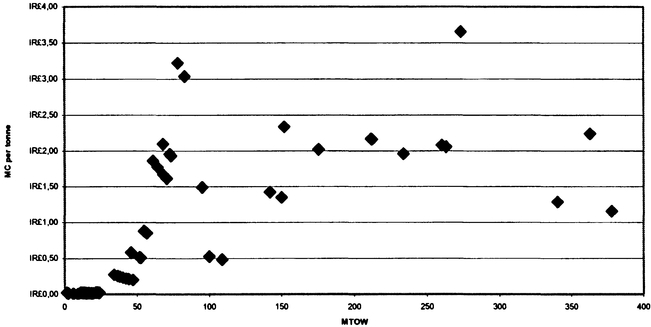

Figure 5.1 Relationship between aircraft weight and calculated marginal cost per tonne

Oliver Hogan and David Starkie

The airport industry has been slow to adopt a structure of charges based on economic principles such as marginal cost pricing. There are two particular reasons for this. First, motivation on the part of the traditional public sector airport companies, which have often lacked a commercial drive, has been absent. Second, such an approach has been viewed, perhaps mistakenly, as contrary to the principles on charging set out in Article 15 of the Chicago Convention. That Article has encouraged the setting of charges to reflect average accounting costs.

The world has now moved on. In the 21st century, a number of significant airports have been privatised and many others have been transformed into commercial enterprises with an incentive to make an efficient use of their assets. In recognition of these pressures, new text has now been added to the ICAO Airport Economics Manual (DOC 9562) and the Manual of Air Navigational Services Economics (DOC 9161), which permits airport and air navigational charges to reflect economic principles, providing their application is non-discriminatory.

The focus of this paper is on the application of economic principles to derive the (short run) marginal infrastructure costs of runway use. Central to these costs are the costs of damage or wear and tear imposed on runways and related taxiways by the movement of aircraft. Such costs have taken on added significance in recent times because of the growing practice of airports to encourage the development of new routes, by offering discounted airport charges. These discounted charges should, at a minimum, cover the specific cost of wear and tear caused by each aircraft movement. The cost calculations in this paper are based on data for Dublin Airport, Ireland and form the basis of a schedule of charges introduced as part of the Irish Commission for Aviation Regulations' statutory Determination of charges.1

By focusing on damage costs, the analysis differs from the few previous applications to airports of marginal cost pricing principles. These latter applications have emphasised the need for peak charges at congested airports at, or nearing, capacity and have given less attention to the issue of an efficient level of charge reflecting the wear and tear imposed on runway infrastructure. Although other studies have considered charging principles at non-congested airports, their pre-occupation has been to design a structure of prices for the efficient recovery of capital and other fixed costs (see, for example, Morrison, 1982). One exception to this general picture was a study of Birmingham airport in the UK by Littlechild and Thompson (1977). Although its focus remained one of efficient recovery of capital and other fixed costs (using a game theoretical approach) it, nevertheless, did consider runway maintenance costs and their allocation to different types of aircraft.

Runway, taxiway and apron pavements sustain damage from the pressure imposed by the combined weight and speed of aircraft landing, taking off, taxiing and parking at an airport. The resulting cracks and damage to the sealing of joints require "routine" repair and maintenance to maintain the quality of the assets and it is this expenditure that forms the initial measure of the costs of use.

These routine expenditures do not, however, capture all of the damage costs associated with additional aircraft movements. There is also damage to the basic structure of runways, taxiways and aprons that leads eventually to their reconstruction2. This gradual loss of structural load-carrying capacity over time is the fundamental principle underpinning pavement design. With concrete pavements, the chief structural failure is through fatigue cracking of the concrete, which is induced by many repetitions of the loading and unloading cycle as aircraft move towards, over and away from the point of (un)loading.

Once the sum of both the 'routine' and the structural damage costs has been determined, a methodology is required for allocating this total damage cost across different aircraft types on a causation basis. Aircraft weight is one factor contributing to pavement damage, but it is not the only factor; configuration of the aircraft landing gear and tyre pressures also play a significant part. All these factors are summarised in an ICAO rating called an Aircraft Classification Number (ACN). A higher ACN indicates a more damaging aircraft and, for the same gross weight, more wheels and lower tyre pressures usually result in a lower ACN. The ACN value also varies according to ground conditions and according to whether pavements are rigid (concrete) or flexible (bitumen).

In the following analysis, we have combined aircraft ratings based on their ACN with estimates of routine maintenance expenditure, together with estimates of structural damage costs, to derive a cost-related set of charges that reflect the principles of marginal cost pricing.

To represent structural damage costs, we used the annualised cost of the airport operators' planned airfield upgrade projects over the ten years, 2001-2010, which included apron reconstruction and runway and taxiway overlays3. For the analysis, it was assumed that Dublin's pavements were rigid and that the sub-grade classification was C.4

Based on the most recent year for which all aircraft movements (number and aircraft type) were available (calendar year 2000), aircraft were grouped according to the damage that they impose (represented by ACN numbers) with aircraft in each group inducing a similar amount of damage per landing. The results are presented in Table 5.1.

To calculate the proportion of damage attributable to each of the 18 aircraft-damage categories, the following formula was used:

where iε I = {1,...,n}, which is the set of aircraft types that landed at Dublin airport during the calendar year 2000; and jεJ = {1,...,18}, which is the set of 18 aircraft damage categories. Note that each j is a subset of I. This formula and its constituent parts can be explained and interpreted in the following way. The 4th power law for pavements states that the damage induced by aircraft A relative to aircraft B is the ratio of the ACN of aircraft A to the ACN of aircraft B, all raised to the 4th power. By selecting a 'design' aircraft with a specified ACN (ACNd) and calculating the damage induced by each aircraft type relative to the design aircraft, we established a consistent basis for the allocation of damage costs.

Table 5.1 Aircraft Damage Categories and ACN. Ranges

| Aircraft damage category | Aircraft types | Minimum | Maximum |

|---|---|---|---|

| 1 | < 10t | 2 | 7 |

| 2 | 10 - 20t | 7 | 12 |

| 3 | 20 - 30t | 12 | 12 |

| 4 | CRJ; FK70; BAel46; BA11; RJ85; TU134 | 16 | 28 |

| 5 | FK100; RJ100; B717; B737-200, 500 | 31 | 35 |

| 6 | TU154; B757 | 32 | 38 |

| 7 | B737-300, 600; DC9 | 36 | 39 |

| 8 | A319; AN12; B737-400, 700, 800 | 41 | 46 |

| 9 | A320; B727; MD80 | 48 | 49 |

| 10 | A321; MD90 | 52 | 58 |

| 11 | A300; A310 | 52 | 58 |

| 12 | B747-100, -200 | 59 | 66 |

| 13 | B767-200, 300; DC8 | 61 | 63 |

| 14 | B727-200 | 63 | 63 |

| 15 | A330; B777; L1011 | 63 | 66 |

| 16 | A340; DC10 | 67 | 68 |

| 17 | B747-400 | 75 | 75 |

| 18 | MD11 | 79 | 79 |

For each aircraft type i, the relative damage factor was multiplied by the corresponding number of landings to give the equivalent number of landings of the design aircraft. The proportion of damage attributable to each damage category, j, was then calculated as the sum (over the subset of aircraft types contained in that damage category, that is, all iεj) of the equivalent number of landings of the design aircraft, divided by the total equivalent number of those landings (summed over all aircraft types). Table 5.2 presents the proportion of damage attributable to each of the aircraft damage categories. Although the resulting schedule of 18 levels of marginal cost (one for each damage category) provided the basis for a relatively simple and more practical charging schedule, it was decided that in view of the traditional approach of charging aircraft on the basis of their weight, the administrative burden on the airport operator could be further reduced by converting the schedule based on damage categories into a per-tonne-schedule.

For each aircraft type i, the marginal damage cost per landing of the relevant damage category j (where iεj) was divided by the MTOW tonnage to give a marginal cost per tonne. That is,

where MCtiis the marginal cost per tonne for aircraft type i, MClj is the marginal cost per landing of aircraft in the relevant damage category j, and MTOWi is the Maximum Take-Off Weight of aircraft type i. It can be seen from this equation that if two aircraft types, for example, i = 1,2 form part of the same damage category j (such that the marginal cost per landing is the same) but have different weights, such that MTOW1 > MTOW2, the heavier aircraft has a lower marginal cost per tonne, MCtl< MCt2.

Table 5.2 Proportion of Damage to Rigid Pavements Attributable to each of the 18 Aircraft Damage Categories

| Aircraft damage category | Aircraft types | % damage to rigid pavements |

|---|---|---|

| 1 | < 10t or similar | 0.00 |

| 2 | 10 - 20t or similar | 0.04 |

| 3 | 20 - 30t or similar | 0.02 |

| 4 | CRJ; FK70; BAel46; BA11; RJ85; TU134 or similar | 2.08 |

| 5 | FK100; RJ100; B717; B737-200, 500 or similar | 11.98 |

| 6 | TU154; B757 or similar | 1.09 |

| 7 | B737-300, 600; DC9 or similar | 1.25 |

| 8 | A319; AN12; B737-400, 700, 800 or similar | 10.62 |

| 9 | A320; B727; MD80 or similar | 7.69 |

| 10 | A321; MD90 or similar | 36.74 |

| 11 | A300; A310 or similar | 1.00 |

| 12 | B747-100, -200 or similar | 0.14 |

| 13 | B767-200, 300; DC8 or similar | 4.71 |

| 14 | B727-200 or similar | 2.38 |

| 15 | A330; B777; L1011 or similar | 17.83 |

| 16 | A340; DC10 or similar | 0.32 |

| 17 | B747-400 or similar | 0.01 |

| 18 | MD11 or similar | 2.15 |

Significant increments in marginal cost per tonne were identified to establish a suitable set of bands for the purpose of categorising aircraft according to the per tonne cost that they impose (called aircraft cost categories). The result was five cost categories and a weighted marginal cost per tonne was found for each of these by dividing the total cost of landings of all aircraft within each of the categories by the total weight of those landings. That is,

where kεK = {1,...,5} is the set of aircraft cost categories.

The schedule of tariffs adopted by the Commission for Aviation Regulation therefore consisted of five charges, one for each of the five cost categories (see Table 5.3). The movement charge is half of the landing charge, which is based on the assumption that each landing has a corresponding departure.

Table 5.3 The weighted per tonne marginal cost per landing and per movement

| Aircraft Cost Category (k) | Weighted per tonne marginal cost per landing | Weighted per tonne marginal cost per movement |

|---|---|---|

| 1 | € 0.50 | € 0.25 |

| 2 | € 1.59 | € 0.79 |

| 3 | € 2.52 | € 1.26 |

| 4 | € 3.88 | € 1.94 |

| 5 | € 5.38 | € 2.69 |

Most of the worlds' airports have a weight-related landing charge based on the MTOW of the aircraft concerned. This relationship is usually expressed as a constant charge per unit weight although, as at Dublin, it is frequently subject to a minimum threshold so that smaller aircraft pay a fixed sum Graham (2001) notes that some airports have a charging rate that declines or increases with the weight of the aircraft. Various reasons have been given for this weight-based approach. It is argued that it reflects both willingness-to-pay (and is, therefore, a form of Ramsay Pricing) and the damage that individual aircraft impose on airfield infrastructure. It is worthwhile, therefore, to reflect on the relationship between MTOW and damage costs on the basis of the Dublin data.

Figure 5.1 provides an overall picture from which it can be seen that the relationship is imprecise with notable outliers. To take a specific example, a DC8-62 freighter with a quoted ACN of 64 and MTOW of 152 metric tonnes causes approximately the same amount of damage per movement as an A321-200 with an ACN of 62 and a considerably smaller MTOW of 79. Application of traditional weight-related charging would result in a charge for the DC8-62 that was twice that for the A321-200. However, for the purposes of a cost-related charging schedule, the greater tonnage of the DC8-62 requires the per tonne charge for that aircraft to be less than that of the A321-200. The tariff structure and aircraft categorization for Dublin has been designed to effect this. The A321-200 lies in cost category 4 with a charge per tonne per landing of €3.88, approximately twice that of the DC8-62 which lies in Aircraft Cost Category 2 and incurs a charge of €1.59. Therefore, the aircraft that is twice as heavy but causes the same damage pays a charge per tonne about half that of the lighter aircraft.

Figure 5.1 Relationship between aircraft weight and calculated marginal cost per tonne

The approach set out in this paper is based on the premise that each aircraft movement should pay for the damage it causes to pavement infrastructure, while maintaining weight-based charging rules for administrative convenience. In pursuing this approach, the analysis illustrated that runway damage reflects a range of factors, of which weight (MTOW) is only one. Indeed, Figure 5.1 illustrates that there is a rather tenuous relationship between the marginal cost per tonne and MTOW.

In a marginal cost-based approach, damage-related charges would normally complement peak period charges that take into account either congestion costs or the long-run costs of expanded infrastructure. However, calculating the marginal costs for peak period use can be complex and the introduction of separate off-peak charges based on the marginal costs of damage to runway/taxiway infrastructure might provide a means of accelerating the introduction of peak/off-peak differentials at congested airports generally, allowing time for the more difficult task of calculating peak period marginal congestion costs.

Making airport charges reflect aircraft specific marginal damage costs should encourage, with the passage of time, the use of aircraft that cause less pavement damage, at the expense of those that cause more. Currently, the situation remains very much as it did a decade ago when Doganis (1992) pointed out that airport charging systems provided no inducement to aircraft manufacturers to develop aircraft requiring runways of lower load-bearing strength. Consequently, if the approach outlined in this paper was to be adopted more widely, aircraft manufacturers would face appropriate design incentives and airport operators should benefit from a reduction in annual maintenance and repair expenditure and from an extension to the lives of runway, taxiway and apron pavements.

The authors would like to thank Dr. Kieran Feighan of Pavement Management Services Limited for assistance with the determination of ACN values, the corresponding damage allocation and the relevant costs.

Thanks are also due to Cathal Guiomard (Head of Economic Affairs, Commission for Aviation Regulation) and Jorge Gonzalez (Infrastructure Management Group Inc.) for useful comments during drafting and to the Commissioner, William Prasifka for permission to publish this piece.

1 Because of the specifics of the Irish legislation, the schedule of damage related charges form the basis of an off-peak charge only.

2 Literature relating to the economics of road infrastructure (see, for example, Small et al. (1988) and Newbery (1988)) has drawn attention to a cost externality that might be of relevance here: pavement infrastructure, once damaged, increases vehicle or, in this current context, aircraft operating costs (through an increase in tyre wear and stresses placed on landing gear for example) and thus increased operating costs, which are borne by the aircraft operators, should perhaps be taken into account. However, we believe that this externality can be ignored in the runway context because safety considerations require surfaces to be maintained in a reasonably steady state condition. We are grateful to Ken Button for drawing our attention to this issue.

3 Details of the phased expenditure on these projects were not available, so the present value of the estimated costs were calculated based on the assumption that the capital expenditure would be averaged over the period. The assumed rate of interest was taken as Aer Rianta's pre-tax cost of capital (calculated at 7%). Dividing by the relevant annuity factors gave the annualised cost of projects planned for each of the periods 2001-2006 and 2007-2010.

4 The sub-grade classification at Dublin varies between B (medium) and D (very low). The main runway (10/28), associated taxiways and new aprons are generally B. Most other taxiways have a C classification, while older runways (16/34 and 11/29) have a D classification. Newer pavements, such as runway 10/28, its associated taxiways and aprons are rigid. Most other pavements are composite (originally rigid and subsequently overlaid with bituminous layers). Rigid pavements are considered to be representative of the majority of pavements at Dublin airport.

Doganis, R. (1992) The Airport Business, Routledge.

Graham, A. (2001) Managing Airports: an International Perspective, Butterworth Heinemann, Oxford.

International Civil Aviation Organisation (ICAO) (1997) Airport Planning Manual, Part 1: Master Planning, Second Edition, Doc 9184-AN/902 Part 1.

Littlechild, S.C. and Thompson, G.F. (1977) "Aircraft Landing Fees: A Game Theory Approach", The Bell Journal of Economics, Vol. 8. No.l, pp. 186-204

Morrison, S.A. (1982) "Landing Fees at Uncongested Airports", Journal of Transport Economics & Policy, Vol. XVI. No.2, pp 151-160.

Newbery, D.M. (1988) "Road Barrage Externalities and Road User Charges", Econometrica, Vol.56. No.2, pp. 295-316

Small, K.A., Winston, C. and Evans, C.A. (1988) Road Work: A New Highway Policy, Brookings, Washington D.C.