Choosing the most desirable point of entry in the foreclosure process

Walking through the steps of buying a foreclosure property

Raising your profile to get more leads

Foreclosure is an unfortunate necessity that often wipes out any equity built up in the home, injures the homeowner’s credit rating, and forces the homeowner and perhaps an entire family out of their home. The upside, if there is an upside, is that foreclosure provides an opportunity for the lender to recover the unpaid debt (or at least a portion of it), for homeowners to relieve themselves of their financial burdens and perhaps salvage some of the equity in their homes, and for you to purchase properties below market value.

As a real estate investor, you should know the basics of the foreclosure process so you can survive a foreclosure, if it ever happens to you, and profit from flipping foreclosure properties, if you choose to explore this area. And why should you explore it? Because foreclosures can be some of the best real estate deals in town.

This chapter introduces you to the foreclosure process, outlines the local rules you need to understand, and leads you step by step through the course of locating and purchasing foreclosure properties.

When dealing in foreclosure properties, you may or may not purchase the property through a real estate agent, depending on the point in the foreclosure process at which you decide to make your offer. You may purchase the property directly from the homeowners, at an auction, or from a bank. However, an agent who knows the foreclosure process in your area can be a valuable mentor and even present you with opportunities for purchasing pre-foreclosure properties.

Getting Up to Speed on the Foreclosure Process

A common misconception of foreclosure is that after the homeowner misses a payment or two, the bank immediately takes possession of the home and then turns around and auctions it off at a foreclosure sale. Actually, the process is more drawn out than that, typically falling in line with the following scenario:

Homeowner stops making mortgage payments.

After about 15 to 30 days, bank sends a gentle reminder.

Homeowner still doesn’t make payments.

Bank continues to send notices.

Homeowner still isn’t making payments.

Bank turns the matter over to its collectors, who continue to harass the homeowner with letters and phone calls.

After about three missed monthly payments, the bank gets pretty steamed and sends an official notice, typically written and signed by an attorney, warning that foreclosure proceedings are about to commence.

Homeowner doesn’t reply or presents a solution that the bank deems unsatisfactory.

Bank posts a foreclosure notice in the local newspaper.

Property goes on the auction block for sale to the highest bidder.

Highest bidder pays for property and becomes official owner, or the bank buys the property and transfers it to its REO (Real Estate Owned) department, which prepares it for sale.

In some states, the high bidder immediately takes possession of the property. Other states have a redemption period, during which the homeowner can buy back the property by paying the full amount of the sheriff’s deed price, which can be significantly less than the original loan amount, along with any property taxes, insurance, and any accrued interest on the amount the auction winner paid for the property. This period can last up to a year.

Previous owner moves out or is evicted.

Lenders generally don’t like to foreclose on properties. They prefer that homeowners pay their bills. At any point before the foreclosure sale, the lender may, if the homeowner cooperates, set up an alternative payment plan commonly called a loan modification. With a loan modification, the lender may extend the term, lower the interest rate, forgive any payment penalties, and possibly even reduce the principal balance in order to reduce the monthly payments.

If you or a loved one is ever facing a foreclosure, contact the lender immediately to explore your options. Seek help sooner rather than later. Shame, anger, and denial may discourage you from seeking assistance, but the longer you wait, the fewer your options. As with any relationship, communication is key. Educate yourself and communicate with your lender. Check out Foreclosure Self-Defense For Dummies, by Ralph R. Roberts, Lois Maljak, and Paul Doroh, with Joe Kraynak (Wiley), and Loan Modification For Dummies, by Ralph R. Roberts and Lois Maljak, with Joe Kraynak (Wiley), for additional guidance.

Brushing Up on Local Rules and Regulations

Although the foreclosure process is similar in all states, laws and other details vary, as I explain in the following sections. Before you join in the game, know the rules and find out where to go for additional information and assistance. You can gather most of the information you need by visiting your county’s Register of Deeds office or by talking to a real estate agent or other professional who’s familiar with the foreclosure process in your area.

You can profit from foreclosures, but you have to invest some time in learning the ropes and establishing the right connections.

Procedural stuff

Because the foreclosure process varies from state to state and from one locale to another, I can’t describe the foreclosure process for your jurisdiction, but I can tell you what you need to find out:

Where to find foreclosure notices: Foreclosure notices are often posted on properties or printed in a local newspaper or in a county’s legal newspaper. You may also be able to register with your county’s Register of Deeds to get on its mailing list.

You may be able to find county-specific foreclosure information, including foreclosure notices, online. Search the web for “sheriff sale” followed by the name of your county and state. If the information you need isn’t online, your search is likely to lead you to contact information for someone who can supply the information.

In states that require or offer judicial foreclosure as an option, all judicial foreclosures go through the courts, so you can search the court dockets for pre-foreclosure notices. (Judicial foreclosure, allowed in all states, requires that foreclosures go through the courts. With a non-judicial foreclosure, allowed only in certain states, the lender advertises and sells the property at a public auction without the courts being involved.)

The number of times a foreclosure notice is published before the property actually goes up for sale: This number differs from state to state; Michigan, for example, follows a five-week process in which the foreclosure notice must be posted at least four times in a qualified legal publication.

Where, when, and by whom the foreclosure sales (auctions) are held: Foreclosure sales are always held at the courthouse, by either the local sheriff or someone the sheriff hires. Get the location of the courthouse and the dates and times of foreclosure sales.

Terms of sale at the foreclosure sale, such as acceptable forms of payment and the amount of time you have to come up with the money: For example, you may be required to pay for any property you win at auction immediately after the auction.

Whether the state has a mandatory redemption period, and if it does, how long it is: A redemption period (the amount of time the current homeowners have to buy back the property) can be as long as 365 days.

How liens (claims against property as security for repayment) are handled: Senior liens wipe out junior liens. For example, a house may have three liens — the mortgage (the senior lien or first position), a home equity line of credit (the first junior lien), and another junior lien from a contractor or homeowner’s association. After the foreclosure and redemption period, the two junior liens are wiped out. (The holders of the junior liens have a right to redeem the senior lien to protect themselves, so that their liens aren’t wiped out by the foreclosure. Redeeming the senior lien consists of buying out the senior lienholder.)

How evictions are handled and how long they typically take: Evictions may take 30 days or more. Offering homeowners cash for keys (a financial incentive for moving out) often expedites the process.

Be very careful not to bid on a junior lien. Sometimes, a junior lienholder can foreclose on a property before the senior lienholder forecloses. A foreclosure ad announces the foreclosure (looking no different than a foreclosure notice for a senior lien), and you can bid on the junior lien just as if it were a senior lien. If your bid wins, you end up the loser in many cases, because when the senior lienholder forecloses on the property, your junior lien is wiped out, and you end up with a worthless piece of paper. I’ve seen unwary investors lose more than $100,000 buying a single junior lien. Sure, you have the right to redeem the senior lien, but that option is often cost prohibitive.

Different types of foreclosures

The foreclosure process varies depending on whether your state performs judicial or non-judicial foreclosures:

Judicial foreclosure: This type of foreclosure passes through the justice system — the state or district court. The bank or lender files a claim to recover the unpaid balance of the loan from the borrower. The courts decide the case, and, as you may guess, typically take a long time to resolve the issue — usually four to six months, but sometimes a year or longer.

Non-judicial foreclosure: In so-called deed of trust states, a third-party trustee (typically a bank or trust company) holds the first lien position on the mortgage until the loan is paid in full. If the borrower defaults on the loan, the lender works through the trustee to foreclose on the property, and the entire process is typically wrapped up in the course of two to four months.

Taxes

Before purchasing a foreclosure property, you should also be aware of any taxes that the property owner owes and how those taxes are paid. Note the following:

Property taxes follow the property. If you purchase a property on which taxes are owed, you owe them.

Federal income taxes may be wiped off the records by the foreclosure. Attorneys for the lenders put the Internal Revenue Service on notice that the property is going through foreclosure. The IRS has a certain number of days to respond and has the right to pay off the senior lien, but it rarely does. In most cases, the IRS releases its lien.

State tax liens pretty much follow suit with the IRS. Attorneys notify the state, and the foreclosure wipes any taxes owed off the books.

Picking Your Point of Entry into the Foreclosure Process

Foreclosures are drawn-out ordeals that typically span a period of several months to more than a year. As an investor, you’re free to choose your point of entry. You can deal with homeowners directly before the foreclosure proceedings begin, wait around for the foreclosure auction to place your bid, or acquire the property from the bank’s REO department or from the new owner after the messiness of the foreclosure has passed. The following sections explore the pros and cons of the available entry points.

Understand all phases of the foreclosure process before trying to carve out your niche. Flexibility and creativity are often key ingredients in working out a deal that’s beneficial for all parties involved, and until you understand all phases, you can’t put together an effective strategy.

Pre-foreclosure

Inserting yourself early in the foreclosure process, before it begins in earnest, is the most effective way to eliminate your competition and acquire the property for a decent price. After the foreclosure notice is posted, the competition begins to swarm, and other investors attempt to strike a deal with the homeowners, which can drive up the price. Of course, you have to be able to approach homeowners tactfully and be prepared to deal with heated emotions and plenty of complications. It’s not for everyone.

In the following sections, I show you how to search for pre-foreclosure properties and work with homeowners tactfully.

Finding pre-foreclosure properties

When a lender initiates the foreclosure process, the foreclosure goes public. To get a jump on the competition, try these heads-up strategies:

Interact with friends and neighbors. You often obtain your best leads by talking with friends, neighbors, fellow church members, and others. Let them know that you buy homes. Let everybody know who you are and what you do, and let them come to you. (See “Advertising to Generate More Leads,” later in this chapter, for more advice on networking your way to leads.)

Talk with lawyers. The first person a homeowner contacts when the foreclosure process begins is often a lawyer. The lawyer may recommend that her client sell the property and can refer the client to you.

Talk with real estate professionals. Real estate agents and other real estate professionals often know about foreclosures before they’re made public.

Contact condo or homeowner associations. Condo and homeowner associations frequently hear about a homeowner’s financial woes long before the news becomes a matter of public record.

Advertise in the paper and online. A small ad in a newspaper or online classified service such as Craigslist with your phone number and a statement such as “I pay cash for homes” or “We buy ugly homes” can lead distressed homeowners to you.

Approaching the homeowners gingerly

Attaining success at the pre-foreclosure stage hinges on your ability to establish trust with the homeowner. If you swoop down like a ravenous vulture, the homeowner is likely to hang up, slam the door in your face, and fling a few choice words in your direction. You have to build credibility. Ninety percent of the people who go into foreclosure lose less and benefit most by selling the house. It’s the best option they have. Let them know this fact and help them decide whether their situation falls into that 90 percent category.

Stepping in at the pre-foreclosure stage isn’t for everyone. The homeowners are often embarrassed, bitter, and reluctant to trust anyone … especially someone offering to help by buying their house out from under them. Approach gently and follow these guidelines:

Be honest. If the homeowner has gobs of equity built up in the home and can refinance his way out of the problem, say so. You may not get this property, but you make a friend who can recommend you to others. Steering distressed homeowners into making a decision that’s in your best interest and not in their best interest is wrong. The deal is good only if it’s good for both of you.

Add a personal touch. If you have the person’s address, pay him a visit or hand-deliver a letter introducing yourself and explaining how you can help.

Take notes and pictures. Getting past the front door to inspect the property is perhaps the biggest challenge you face. If the homeowner invites you in, ask to look at the property. Take notes and photographs, unless you get the feeling that it would upset the homeowner too much. In that case, take good mental notes. You need all the information you can get to determine the right price to offer.

Verify the facts. What the homeowners tell you isn’t necessarily true. Inspect the property as closely as possible, determine its true market value, and research the title closely, as you would before purchasing any property. (See Chapter 10 for more about researching distressed properties.)

Make a decision. The longer you waffle, the more time another investor has to make her move. Decide quickly whether you want the property, and if you want it, make your offer … after checking the title and inspecting the property, of course.

In some areas, the purchaser of a foreclosure property has the right to schedule an inspection of the interior and exterior. Such is the case in Michigan, where I buy foreclosure properties.

Pitching your offer for a pre-foreclosure property is very similar to making an offer on any home that’s on the market. If the homeowner listed the property for sale, your agent should present your offer in the form of a written purchase agreement to the listing agent. If the property is not yet listed, have your agent present the purchase agreement to the homeowner for consideration.

The more you assist homeowners through a difficult situation, the better your chance of acquiring the property and establishing yourself as an investor with integrity. When people hear that you helped so-and-so out of a tough jam, they’re more likely to seek your assistance when they run into similar problems.

To keep yourself honest, take off your investor shoes and put yourself in the homeowner’s shoes. Ask yourself whether what you say, suggest, and propose is in the homeowner’s best interest. If it’s not, don’t do the deal.

Negotiating a short sale

A short sale occurs when a lender agrees to allow the homeowner to sell the home for less than the balance due on the loan and accepts the proceeds as full payment. For example, suppose a homeowner owes $175,000 to a bank and can no longer afford the payments on that loan. The homeowner wants to “get out from under the home” — sell it, pay off the mortgage balance, and move to more-affordable accommodations. Unfortunately, the best offer the homeowner gets on the home is $135,000. With a short sale, the mortgage lender allows the homeowner to sell the property for $135,000 and fork over that money to the lender as payment in full; the lender forgives the other $40,000 due on the loan.

That’s the simple version of a short sale. More complicated versions arise when multiple lenders have claims against the property (liens on the property). For example, a homeowner may owe back taxes on the property and have a first mortgage with one lender, a home equity loan from another lender, and financing from one or more contractors for new windows, new carpeting, and a host of other goodies. When several parties have liens against a property, they must get in line to collect their money. In the event of a foreclosure, certain lienholders are paid before others: Property taxes are paid first, followed by the first-mortgage holder, followed by the second-mortgage holder, followed by any contractors. If no money is left after paying the first lienholder, the junior lienholders are likely to receive nothing. (Because of changes in how these situations are resolved, the second lienholder may receive some portion of the proceeds of the short sale.)

To further complicate matters, junior lienholders who stand to lose everything they’re owed in the event of foreclosure have the opportunity to buy out the senior lienholder through redemption — paying that lienholder the total owed to the lienholder or by negotiating a payout of a lesser amount.

You can profit from short sales in various ways. For example, suppose three lienholders have a claim against a property, with A being the senior lienholder, B being the second-position junior lienholder, and C being in the third position. Depending on how much equity is built up in the property, the following scenarios are possible:

You buy A’s position (either at auction or directly from A) and wait for the redemption period to expire. B and C take no action, if you’re very lucky, and their positions are wiped out.

When you’re first getting started, I strongly recommend that you buy only A’s so you own the controlling position. You’re much less likely to lose your investment if you own A’s. You can still profit by purchasing junior lienholder positions, but you usually buy out a junior lienholder only for the right to buy out the senior lienholder.

You buy A’s position. B buys you out to protect its position and waits for the redemption period to expire to wipe out C’s position. You have to sell, but you don’t have to discount, so you should at least get your money back. You get more money if you bought A’s position for less than A’s claim against the property; for example, if A holds a mortgage of $125,000, which you’re able to get for $100,000, then B must pay you $125,000 to buy you out, and you earn a tidy $25,000.

You buy A’s position. C buys out both you and B to protect its position. Again, you have to sell, but C must pay you the balance on the loan you have claim to.

Another investor buys A’s position. You buy B’s position, giving you the right to buy A’s position from the other investor, which you do, forcing C to either buy you out or lose out entirely.

You buy A’s position and then buy B’s and C’s positions (typically by paying them less than the total of what they’re owed via a short-sale agreement). Why buy out B and C? If the property has a lot of equity in it, buying out B and C prevents them from buying your position and prevents other investors from buying B’s or C’s position and then attempting to buy you out.

You buy A’s position, and then, during the redemption period, the homeowner redeems the property (buys you out). Again, assuming you paid less for A’s position than the balance owed that position, you stand to receive the difference. For example, if A has a lien on the property for $125,000, and you bought A’s position for $100,000, then the homeowner has to pay you $125,000 to redeem the property, and you earn $25,000.

Success in short sales requires a lot of wheeling and dealing and jockeying for position. Start by contacting all parties that have liens against the property to find out the payoff amount for each loan. After you know the position of each lienholder, the total payoff amount of all loans, and the maximum amount you’re willing to pay for the property (see Chapter 12), you can begin to negotiate with the lienholders. For example, suppose the payoff amounts look like this:

Lienholder

Payoff amount

City Mortgage (first mortgage)

$84,349.42

Capital Source (second mortgage)

$39,208.16

Jackson Heating and Cooling

$10,680.00

Internal Revenue Service

$16,803.43

Total

$151,041.01

You decide the maximum amount you can pay for the property is $111,600. Now you’re ready to plan your strategy for wheeling and dealing with the lienholders:

The balance on the first mortgage from City Mortgage is $84,349.42. Because the estimated property value is $144,000, City Mortgage is highly unlikely to agree to a short sale. It would be better off owning the property. You’re going to have to pay the full $84,349.42. That leaves you about $27,251 for paying off the other lienholders without exceeding your top offer of $111,600.

Capital Source holds the second mortgage of $39,208.16. This is a perfect opportunity for a short sale. Capital Source stands to lose the entire amount if the foreclosure proceeds to conclusion and the homeowners fail to redeem the property. They may be willing to accept $24,000 to assign the lien to you, in which case the homeowners owe you the $39,208.16. This places you in a prime position to buy the first mortgage at auction. See the following section for details.

Jackson Heating and Cooling holds a construction lien of $10,680. It’s in a very weak position and is unlikely to buy the first mortgage of $84,349.42 to protect its position. It would be very likely to sell you its position for $2,000–$3,000.

The IRS is also unlikely to invest $84,349.42 to protect its $16,803.43 position. However, if the IRS has a lien on the property, make sure the law firm handling the foreclosure gives the IRS 30 days’ notice prior to the sale. Assuming notice was given, after the redemption period, this lien is dropped. If you don’t check this, you could end up owning a property with the IRS lien still attached.

Assuming your negotiations unfold according to plan, you pay City Mortgage $84,349.42, Capital Source $24,000, and Jackson Heating and Cooling a cool $3,000 (at the most), for a grand total of $111,349.42, slightly below your target of $111,600.

A variation on this scenario arises if you short the first mortgage — that is, pay the bank less than the principal remaining on the first mortgage. As of the writing of this book, if the first mortgage is shorted, the second lienholder is entitled to 6 percent or $6,000, whichever is less. For example, suppose you’re buying a property that you can sell for $175,000 after fixing it up. The current value of the property is $125,000, and the owners owe $150,000 on the first mortgage and $50,000 on the second mortgage. You short the first mortgage for $125,000, and the bank holding the first mortgage pays all commissions, closing costs, and $6,000 to the second lienholder.

Don’t start negotiating short sales until you’ve done your research on the property, as discussed in Chapter 12. Carefully research the title so you know all parties that have a lien on the property. For more about short sales, check out Foreclosure Investing For Dummies, by Ralph R. Roberts with Joe Kraynak (Wiley).

Foreclosure

The foreclosure process begins with the posting of the Notice of Default (NOD) in the county’s legal newspaper, proceeds through the sale (typically at auction), and ends with the transfer of property from the previous owner to the new owner. At any step along this journey, you have the opportunity to acquire the property. The following sections show you how to acquire properties after the NOD is posted or at a foreclosure sale.

Perusing foreclosure notices

When a lender initiates foreclosure proceedings, the lender posts a foreclosure notice in the county’s legal newspaper. (See Chapter 10 for more on foreclosure notices.) Contact your county’s Register of Deeds office and ask where it posts foreclosure notices. You may be able to subscribe to the paper or register to receive the postings via e-mail.

The posting of the foreclosure notice provides you with another entry point into the process. With the foreclosure notice in hand, you now have more information at your fingertips, including the following useful tidbits:

Mortgagors’ names (who owes the money): This bit of information can help you track down the property owners and perhaps approach them before the property ends up on the auction block.

Lender’s name (bank or mortgage company): You may not need this information right away, but it could come in handy in the future if the lender ends up with the property after the auction and needs to sell it.

The amount that remains to be paid on the loan: By knowing the amount remaining to be paid on the loan, you have a clear idea of what may be considered a reasonable opening bid.

The interest rate: If the interest rate on the first mortgage is high, and you buy the first mortgage, you stand to gain a decent return on your investment even if someone redeems the property after the sale because whoever redeems the property must pay you back the amount of money you paid for the first mortgage plus interest. If the interest rate is 8 percent, that’s higher than most banks pay.

Legal description of the property: The notice doesn’t provide you with a mailing address, but through the Register of Deeds office or your agent, you can figure out the mailing address from the legal description. After you know where the property is located, you can drive by or possibly even get inside to inspect it.

Length of the redemption period, if any: This tells you how long the current owners have to buy back the house after the sale … and how long you’ll probably have to wait before you can place the house back on the market.

If you live in a county that sees a fair share of foreclosures, the foreclosure listings may seem overwhelming at first. The trick to making the listings less cumbersome is to know what you’re looking for and then weed out any listings that raise red flags. For example, if you find a property on Main Street with a mortgage of $200,000, and you know of no property on Main Street that you’d pay more than $150,000 for, you know that property isn’t for you. If the same property is listed for $75,000, it may be worth investigating.

After you find a property that interests you, double-check to make sure that it’s going to be sold. Sometimes, the foreclosure notice is posted, and then the homeowner files for bankruptcy or takes some other action to cancel or postpone the sale. Call the attorney listed in the foreclosure notice before you waste a lot of time researching the property (see Chapter 10 for more about conducting research). You may be able to obtain additional information from the attorney, such as the exact price, but don’t count on it — the attorney is acting as a debt collector on behalf of the lender.

Hurry. The clock’s ticking. You have about 30 to 90 days from the time the foreclosure notice appears in the paper before the property goes on the auction block. You also have more competition now that the foreclosure is public knowledge.

Taking part in the foreclosure sale

Many real estate investors choose to wait until the foreclosure sale to make their move, trusting that they can successfully outbid the competition. Before you choose to make your entrance at the foreclosure sale, sit in on a few auctions to get a feel for how they work. Talk to one or two veterans who actually purchase properties at auctions, and place your bid only after taking the following precautions:

Research the title thoroughly to check for any liens on the property. (See Chapter 10 to find out how to research the title.)

Make sure that you’re bidding on a first mortgage or senior lien, not on a second mortgage or junior lien. (This information is also on the title.)

Accurately estimate the value of the property by researching recent sales of comparable properties.

Inspect the property as thoroughly as possible with your own two eyes (as I explain in Chapter 10).

Settle on the maximum amount to bid and don’t exceed this amount no matter how keyed up you get over the property. (I show you how to rein in your impulses in the later section “Settling on a maximum bid.”)

Don’t assume you’re getting a good deal just because you’re acquiring the property at an auction. Research a property and its title thoroughly before placing a bid. You can really get burned by not doing your homework.

Post-foreclosure

You may think that your chance of purchasing a property ends when the auctioneer hollers “Sold!” but the property can still change hands. Jumping in this late in the process may mean that you have to pay more for the property than you could have gotten it for by acting more aggressively early on, but after the property is sold or passed back to the lender, you can deal directly with the new owner … without a lot of emotional baggage. In the following sections, I show you how to contact the new owner: the lender or the investor who purchased the property.

Buying an REO property

In most cases, the lender buys back the property and, after the redemption period, transfers the property to its REO (Real Estate Owned) department, which prepares the property for resale. The lender may be willing to sell you the property before or after transferring it to its REO department. From the foreclosure notice (discussed earlier in this chapter), you can obtain the lender’s name and the amount owed on the mortgage.

When you’re ready to make an offer, have your agent draw up a purchase agreement to submit to the lender. Many times, the lender stipulates that you must add some standard addendums to the purchase agreement, such as a statement that you agree to purchase the property as is, subject to inspections. Your agent can help you determine which addendums to add.

You may have better luck purchasing a property from the REO department at the end of a month or quarter. In an attempt to make its numbers for a particular month or quarter, the REO department may be under pressure to clear bad loans off its books. It may accept an offer on June 25 that it rejected on June 3.

Contacting another investor

If another real estate investor won the bid, she may be willing to sell the property after she takes possession of it or even during the redemption period. If you purchase the property before the redemption period expires, keep in mind that the property owner can buy back the home at any time during the redemption period by paying the loan balance and any property taxes, insurance, and accrued interest.

In all real estate transactions, presenting an offer in writing (as a purchase agreement) is best. Sometimes an investor has a property already tied up with the seller through a purchase agreement, but the investor doesn’t have the funds to close and wants to pass it off to another investor. This is called a pass through transaction, typically accompanied by a bird dog fee (a finder’s fee), which can range from $5,000 to $10,000.

Paying a bird dog fee isn’t something I recommend. You’re better off putting that $5,000 to $10,000 to work on another property that you can buy directly from a homeowner or at auction.

Purchasing Foreclosure Properties Step by Step

Profiting from foreclosures isn’t the slam-dunk proposition that many perceive it to be. For every story of someone buying a property and selling it at a 500 percent profit, I can tell three stories of rank beginners who lost their shirts making ill-informed decisions. The truth is that investing in foreclosure properties is risky.

Although you can’t eliminate the risk, you can whittle it down to the point at which success becomes more probable than failure. The following sections present a step-by-step process for finding, researching, and purchasing foreclosure properties that reduces the risk.

Step 1: Find a property

The method for finding foreclosure properties depends on where in the foreclosure process you decide to look (I cover these stages in more detail earlier in this chapter):

Pre-foreclosure: A homeowner may contact you directly, knowing that you’re an investor who buys houses, or you may obtain leads from lawyers, real estate agents, friends, or acquaintances.

Foreclosure: Search through the foreclosure notices in your county’s legal newspaper or register to get on the mailing list.

Post-foreclosure: Contact the lender’s REO department or the investor who purchased the property at the foreclosure sale.

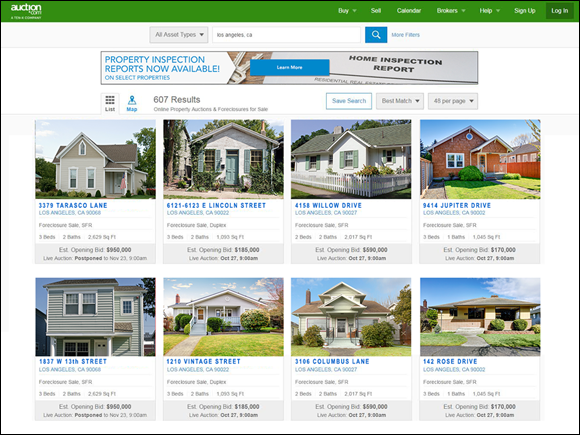

Since the previous edition of this book, the Internet has continued to have a huge effect on simplifying the way people discover foreclosed properties. Various auction sites, including Auction.com (see Figure 8-1), allow you to search for residential real estate throughout the country.

Figure courtesy of Ten-X, LLC

FIGURE 8-1: You can bid on residential real estate for sale at Auction.com.

Step 2: Follow the paper trail

After you locate a property that looks promising, it’s time to do your homework. Begin by researching the title to make sure that it doesn’t contain any hidden surprises, and then dig a little deeper, especially if you’re purchasing the property in a pre-foreclosure deal, to uncover additional details that can help you during negotiations. See Chapter 10 for details.

Step 3: Inspect the property

The first rule in flipping houses is to never buy a property without looking at it first, but that can be a bit tricky. In a foreclosure situation, the property owner may be less than enthusiastic about showing his home to someone who’s ultimately going to take possession of it and evict him.

The least you should do is drive past the property, get a look at it from all sides, and snap some photos. The care and handling of the house’s exterior and landscaping are often pretty good indications of how well the owner cared for the inside of the house. A house with a perfectly manicured lawn, trimmed hedges, and a freshly painted garage reflects a pride of ownership that generally permeates the house.

If you can establish a good rapport with the homeowners, they may invite you in to look around, especially if you need to meet with them to go over some paperwork or explain their options to them. Do what you can to get inside the house, short of breaking in or appearing too pushy. After you’re inside, follow the guidelines for inspecting a property, as I suggest in Chapter 11, to whatever degree possible.

Stamp the following rule on your forehead: Your eyes or no buys. Never buy a property that you haven’t visited and inspected yourself. If you decide to have someone else inspect the property, don’t blame them if they miss something.

Step 4: Bid on a property (when buying at an auction)

You performed your due diligence. The price is right, the house looks great, and the title is clear. You’re one bid away from financial freedom. Now it’s time to place that winning bid, right? Not so fast. Assuming that you’re entering the process at the foreclosure stage, read through the following sections to prepare for auction day.

Settling on a maximum bid

The single most important step in bidding on foreclosure properties is to establish your maximum bid — an amount you’re not to exceed no matter what happens.

To determine your maximum bid, use the same system I present in Chapter 12 to ensure that you stand to earn at least 20 percent.

If you’re unable to get inside the house to inspect it, estimating the costs of repairs and renovations can be tricky. Use the following techniques to come up with some rough estimates:

Assume the house needs painting inside and out and new carpet from wall to wall.

Estimate high for older homes because they generally have more costly surprises, such as substandard plumbing and electrical systems.

Remain cautious of brand-new homes that may not be finished on the inside.

When in doubt, overestimate expenses.

Always commit to a maximum bid before the auction begins. Otherwise, you may get caught up in a bidding war, win the bid, and lose your shirt. I take an assistant with me to keep me from bidding away my future profit.

Testing the waters

Sit in on a few auctions before placing your first bid. Observe other bidders to size up your future competition and discover their techniques and strategies. Bring your list of properties along with your maximum high bids and compare your bids with the winning bids. If your bids are way out of line, you may want to tweak the process you use to arrive at your estimates before you do any serious bidding. Don’t talk yourself into raising the price you think you can sell the property for in an attempt to justify bidding higher than your maximum bid.

Surveying bidding strategies

Foreclosure auctions are like poker tournaments. Every bidder has a unique strategy and various techniques for psyching out the competition. Here are some common strategies you may want to look out for and try yourself:

Bore ’em into submission. Keep outbidding the highest bidder by the minimum bid. If the minimum increment is $100, whenever someone makes a bid, bid $100 more. Just don’t exceed your maximum.

Speak softly and carry a big wad of cash. Quiet bidding often conveys confidence and can undercut the high-energy, emotional tone of the auction. It forces other bidders to ask, “What did he bid?” which can be a little unsettling and give you the edge you need.

Crank the volume. Bark your bids as if you’re a mad dog in control of the room. If you’ve ever had your parents yell at you, you know the effect this technique can have. It can rattle your opponent just enough to make him back off or make him think that you’ve lost your mind. Either way, you’re in control.

Mix it up. Go erratic, random. Don’t follow a pattern. As long as your bids make sense to you without exceeding your cap, experiment and see what works best.

I was once at a sheriff’s sale and someone bid a dollar, I bid $500, then he bid $1,000, then I went to $1,500. He went to $2,000. My maximum bid was four grand. I jumped my bid to $4,000 instead of going to $2,500. He just shook his head and said, “No more.” You can scare people off with this tactic.

Performing post-auction chores

Assuming you submitted the winning bid, you have to take several steps to pay for the property and protect your interest in it. Proceed through the following checklist to make sure that you’ve attended to all the details:

Follow through on the conditions of the sale. Ask the Register of Deeds or whoever is holding the auction to supply you with a list of conditions to finalize the sale, and then attend to those conditions.

Pay any remaining balance due. You must pay the entire balance right then and there.

Record the deed. Upon payment, you receive the deed to the property. As soon as possible, take the deed to the county clerk’s office or Register of Deeds and have it recorded to protect your legal claim to the property. In some counties the sheriff may record the deed, but make sure it gets done quickly.

Ask the Register of Deeds or your real estate attorney to explain the recording requirements in your area.

Obtain title insurance. Visit your title company and obtain title insurance for the property.

Obtain property insurance. If any major damage occurs to the property during the redemption period, you want to have an insurance policy to pay for it. Contact your insurance agent as soon as possible to obtain a policy for the home.

Notify any taxing authorities who have liens on the property. If the IRS or the state has an income-tax lien on the property, the foreclosing attorney usually notifies the IRS prior to the sale. Make sure the IRS notice accompanies the bidding paperwork. If the foreclosing attorney did not notify a taxing authority that has a lien on the property, consult the foreclosing attorney and your own attorney, if necessary.

Return any overbid money to the homeowners. An overbid situation occurs if you bid more than is required to cover any and all liens on the property. When a buyer submits an overbid, the homeowners have the right to claim the overbid amount. All they have to do is go down to the courthouse and file a claim for the money, and it’s theirs.

If someone outbids you at the auction, if your area has a redemption period, and if you’re still interested in buying the property, consider writing a letter to the homeowners informing them of their redemption rights. You may be able to help the homeowners redeem the property, and then you can buy the property from them. Or, better yet, knock on their door, make sure you know what you’re talking about, and try to swing a deal.

Step 5: Survive the redemption period

If you win the bid in some states, you pay off the mortgage and any taxes due on the property and immediately take possession of the property. In other states, you have to sit on the property until the redemption period passes, which can last up to 365 days.

While you’re waiting, you may be tempted to start working on the house. Don’t. You may invest $10,000 in renovations only to have the property owner decide to redeem the property just before you wrap up the project.

During the redemption period, the deed holder (homeowner) still has control of the real estate. You can, however, gain a sense of security by offering the seller cash for keys and having them execute a non-redemption certificate. A non-redemption certificate is an agreement by the homeowner to not redeem the property.

Be very cautious when working with homeowners. You don’t want to be accused later of taking advantage of homeowners while they were under duress.

You can also work to shorten the redemption on a property, assuming the property is abandoned. If the property is vacant, try your luck at going to your county’s court and getting a court ruling stating that the property is abandoned. With this document in hand, you can report your findings to the county register of deeds. This court ruling can shorten the redemption period from a year or six months down to 30 days; however, this process can take 75 days to complete, so patience is key!

Never spend money on a house you don’t own or that doesn’t have a clear title. You can pay taxes and insurance and file an affidavit to add that amount to the balance required to redeem the property, but don’t spend money on renovations until you take possession.

Advertising to Generate More Leads

At this point, you likely have more opportunities to explore than you have time to research, but after you have a solid support team in place, you may find that your flippable property pool becomes overfished. To continue expanding your real estate investment business, you can either widen your net by reaching out to other neighborhoods (see Chapter 6 for details) or fish a little deeper by advertising for leads.

Unless you’re afflicted with a bad case of tunnel vision, you’ve probably noticed ads, signs tacked to telephone poles, and billboards advertising in big bold letters We Buy Homes. Well-established real estate investors often post these ads to draw sellers to them instead of having to search for properties on their own. You can follow their lead by doing a little of your own guerilla marketing:

Tack up flyers at local stores, but don’t post them on telephone poles, vacant buildings, or lawns, because it’s against city ordinances.

Print and distribute business cards to people you meet in the area.

Network with others by telling everyone what you’re doing and by asking lots of questions.

Visit neighborhood churches; they often know people in the neighborhood who need to dispose of property.

Post an ad in the neighborhood newspaper or on Craigslist or other online venues — Private Lender Looking for Properties.

Post your own billboard ad after you become well established.

Advertise only after you become well established and are comfortable flipping multiple properties at once. Otherwise, you may be overwhelmed with calls that you’re unable to follow up on. This inability to get back with potential leads can quickly damage your reputation as someone who can help distressed homeowners get out from under a house.

Understanding the overall foreclosure process

Understanding the overall foreclosure process When dealing in foreclosure properties, you may or may not purchase the property through a real estate agent, depending on the point in the foreclosure process at which you decide to make your offer. You may purchase the property directly from the homeowners, at an auction, or from a bank. However, an agent who knows the foreclosure process in your area can be a valuable mentor and even present you with opportunities for purchasing pre-foreclosure properties.

When dealing in foreclosure properties, you may or may not purchase the property through a real estate agent, depending on the point in the foreclosure process at which you decide to make your offer. You may purchase the property directly from the homeowners, at an auction, or from a bank. However, an agent who knows the foreclosure process in your area can be a valuable mentor and even present you with opportunities for purchasing pre-foreclosure properties. If you or a loved one is ever facing a foreclosure, contact the lender immediately to explore your options. Seek help sooner rather than later. Shame, anger, and denial may discourage you from seeking assistance, but the longer you wait, the fewer your options. As with any relationship, communication is key. Educate yourself and communicate with your lender. Check out Foreclosure Self-Defense For Dummies, by Ralph R. Roberts, Lois Maljak, and Paul Doroh, with Joe Kraynak (Wiley), and Loan Modification For Dummies, by Ralph R. Roberts and Lois Maljak, with Joe Kraynak (Wiley), for additional guidance.

If you or a loved one is ever facing a foreclosure, contact the lender immediately to explore your options. Seek help sooner rather than later. Shame, anger, and denial may discourage you from seeking assistance, but the longer you wait, the fewer your options. As with any relationship, communication is key. Educate yourself and communicate with your lender. Check out Foreclosure Self-Defense For Dummies, by Ralph R. Roberts, Lois Maljak, and Paul Doroh, with Joe Kraynak (Wiley), and Loan Modification For Dummies, by Ralph R. Roberts and Lois Maljak, with Joe Kraynak (Wiley), for additional guidance. You can profit from foreclosures, but you have to invest some time in learning the ropes and establishing the right connections.

You can profit from foreclosures, but you have to invest some time in learning the ropes and establishing the right connections.