The Real Estate Way

A Fast Lane Guide to Financial Freedom and a Secure Retirement

Justin Woodall

Kindle Edition

Copyright 2019, Justin Woodall

All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in reviews and certain other non-commercial uses permitted by copyright law.

Disclaimer

This book is written from the context of my own personal experiences and those that I’ve observed by being a real estate broker for well over a decade. The scenarios and examples used are just examples. Any given expenses, like repairs, management, taxes, insurance, etc., are estimates. And, I don’t always include tax consequences of sales, income tax implications, commissions, fees, etc. To do so would make the examples too confusing and difficult to understand. My goal in the examples is to keep it simple, and their purpose is to teach you how to think. I want you to be able to think and analyze, beyond just “Diversify and hold stocks for the long term,” “Invest in your 401K,” or “Put money in savings,” and hope for the best. The aim is to help you to really evaluate opportunities and see which is best for you and your family. Real estate has accelerated my wealth and passive income much more quickly and easily than I personally could do in stocks or any other way that I know of, other than building a business. I hope it is the beginning of a lucrative and fun journey to building your own portfolio of real estate so that you can be financially free and have more time to spend doing the things you love.

The opinions and statements herein are mine. There is no guarantee that by utilizing the tips, strategies, or information contained in this book you will be profitable. People have made millions in real estate and lost millions in real estate. So, before investing, I recommend that you seek advice of individuals, like CPAs, attorneys, or other people you trust. I am not a CPA, attorney, or financial advisor qualified to give you investing advice. I am a real estate broker licensed in the state of Georgia. Real estate markets are very local, and prices and rents will vary from state to state, city to city, and town to town. So, I recommend you seek the council of trusted advisors before you invest your hard-earned money, but allow this book to entertain you and open your mind to the possibilities of income-producing real estate as a superior way to fund your retirement and your life.

ISBN: 978-1-7339951-1-5

Ninety percent of all millionaires become so through owning real estate. More money has been made in real estate than in all industrial investments combined. The wise young man or wage earner of today invests his money in real estate.

—Andrew Carnegie

FREE RESOURCES

For more resources related to real estate investing, to find a top investment real estate agent in your area or for a link to a FREE Rental Property ROI Analyzer tool, visit us online at:

INTRODUCTION: The Fast Lane to Financial Freedom through Real Estate

CHAPTER 2: Is Real Estate Right for You?

CHAPTER 3: The Financial Prerequisites

CHAPTER 4: Choosing Niches: Key to Riches

CHAPTER 5: Analyzing Investment Properties

CHAPTER 7: Funding Deals: Part 1—Going Traditional

CHAPTER 8: Funding Deals: Part 2—Going Alternative

CHAPTER 10: Harnessing Tax Advantages

CHAPTER 11: Managing Properties

CHAPTER 13: Upping the Pace with Your Dream Team

CHAPTER 14: Scaling to Multiple Properties

CHAPTER 15: Leasing Structures for Maximum Returns

CHAPTER 16: Riding the Ups and Downs

CHAPTER 17: Finding Freedom Faster

CHAPTER 18: Making It Happen: Mindset

INTRODUCTION

The Fast Lane to Financial Freedom through Real Estate

Real estate is that vehicle. So many people run away from it because they don’t understand it. My aim with this book is to deepen your understanding of real estate, help you determine if it’s a vehicle you want to utilize, and be a guide for you as you begin your journey to financial freedom. So, when the title says, “fast lane,” it doesn’t mean you’ll get rich overnight, but the methods in this book can get you to financial freedom much faster than the traditional means of investing in a 401K and a traditional retirement account of stocks and mutual funds.

Many Years and Thousands of Transactions

I began working in the real estate industry in 2004. At that time, I worked as an individual real estate agent with the largest company in town at that time, Coldwell Banker. Starting out, I was simply helping buyers to buy and sellers to sell real estate. Over time, I met real estate investors and began to see the possibilities and the freedom that income-producing property can deliver to the owners … and to me.

As my past client list grew and demands on my time became greater and greater due to the number of clients that needed my help, I began to grow a team of agents. I then transferred my license to Keller Williams Realty where running and growing a team was a better fit. After spending four years there, I left to open my own real estate business, Woodall Realty Group, and brought my team with me. Our business has grown year over year, and we continue to gain market share in the Athens, Georgia, and surrounding areas. The majority of our business is helping homeowners to buy and sell their primary residences, but we also work with builders and investors. By working in all of the sectors of residential real estate, we have a great overview and understanding of all types of real estate, especially residential.

Through developing this understanding and seeing the possibilities, I, myself, have been able to invest and accumulate income-producing properties that provide a nice annual income for my family and continue to build my wealth. The best thing about it is that the majority of the wealth building is funded by the tenants in my rental properties, rather than out of my own pocket. Because I want you and many, many others to enjoy the same steady income and wealth-building that real estate can provide, I am writing this book. Let’s take a moment looking at all you’ll learn.

The Real Estate Way—An Overview

The aim of this book is to show you how you can create your own customized “portfolio” of income-producing real estate to achieve your financial goals, build streams of monthly cash flow, and realize the freedom that can come through real estate.

We’ll begin with a comparison of real estate vs. traditional retirement investing, like IRAs and 401Ks, to show the higher returns, the predictability, and the stability that real estate can give in the long-term over these traditional investment routes. We then take a quick look at the work and attitude needed to invest in real estate profitably. For any readers not yet financially set to get started in real estate, I supply some solid recommendations on how to revamp your finances and mindset around money, so that you are prepared to get in the game.

With that groundwork established, we next move into the “what” of real estate investment properties. There are different types of properties you could invest in as well as different classes within each type. We’ll look at those and discuss the pros and cons, so you can start figuring out where your interests lie. Next, you’ll learn my formula for analyzing a property to determine whether or not it’s going to give good returns. Yes, I’m talking return on investment (ROI) here. One key to great returns is finding the right properties. As a long-time real estate agent who also invests in my own properties, I reveal ways to find those hidden gems.

Once you find your deal, you’ve got to be able to pay for it. You’ll learn the traditional means of financing a real estate investment as well as some creative options that can allow you to buy more properties faster and with little or no cash out of your own pocket. Sometimes a little creativity can skyrocket your returns. We’ll also discuss the upsides and downsides of different types of ownership.

One bonus of owning real estate is the tax advantages that come along with it. Understanding how to legally take advantage of the tax write-offs can boost your ROI in big ways, so we’ll look at this too.

Once you understand the benefits of owning income-producing real estate and determine that it’s right for you, in order to really make it work, it must be managed properly. Both the property itself and the tenant must be managed well. This can make or break a real estate investment. We’ll look at the costs and benefits of “do it yourself” versus working with a team of professionals and how to scale to the next level. Then we’ll consider different types of leasing options that can be utilized in different situations and how to ride the waves of a shifting real estate market. While the value of your real estate may go up or down in a period of years, the annual returns typically will rise consistently regardless of the value—and you’ll learn why in this book.

Real estate investing can be a fast lane to financial freedom and a tremendous wealth builder once you see the possibilities and have the belief in yourself that you can make it happen. It can happen faster than most people think. We’ll close the book with an examination of the proper mindset for building your portfolio quickly and finding financial freedom.

Take Charge of Your Future

In a day and time when many people are afraid they may not have enough resources to retire, that their retirement savings may run out, or that the stock market may plummet at the very time they decide to stop working, you don’t have to be in that position. Instead, you can be making a consistent and steady income each and every month when you own income-producing real estate. You don’t have to live in uncertainty, and you don’t have to depend on the government or the whims of world markets to take care of you.

Take charge of your own future, and don’t wait to get started! You can make wise choices and decisions when you are equipped with the right information. Learn all you can about the topic. This book is a great place to start learning. Then—take action! With the right knowledge and the right team to help you, it really can happen faster than you can imagine!

If you would like more information or have specific questions on the information provided in this book, you can find me online at any of the following websites:

Turn the page to find out why I believe real estate is your best choice for achieving financial freedom.

CHAPTER 1

Why Real Estate?

Real estate. It’s one of those topics almost everyone wants to talk about or is interested in at some level. And since you are reading this book, you are probably one of them. Why is it that real estate seems to have an appeal to so many people? Perhaps because it’s real. You can see it, touch it, feel it, walk on it, smell it. It’s different from other investments, and it’s different from personal property.

My Real Estate Aha

Real estate has always intrigued me. I did not grow up in a real estate family. My parents owned our house, and my grandfather owned some land that was the old family farm. Otherwise, I didn’t know much about it. No one in my family owned any rental property or investment property that produced income.

My parents both worked hard, but what we had came from their toils. It was a family of two working parents who worked hard and gave us all they could. They never made a lot of money, but they made enough. We didn’t have designer clothes, shoes, and extravagant vacations, but we had what we needed. We weren’t lacking. I never missed a meal, and I was well cared for, but we didn’t have extra. I would say that I grew up in a middle-class family in a middle-class neighborhood in Georgia.

I remember when I was in college and I had my first revelation about how lucrative owning real estate and renting it out could be. You know, one of those aha moments. I remember it like it was yesterday. This was the first year that I’d really lived independently of my parents and not in a dorm. I had my own apartment with a roommate and felt like a real adult.

After I placed my monthly rent check into the drop box at my apartment complex, I turned around to see the hundreds of units there—and it hit me, “Somebody is collecting and will deposit hundreds of checks just like mine.” Then I realized they would deposit these checks this month and again next month and again the next! A money machine, the owners of that apartment complex owned a money machine!

I didn’t take any action at that time, but it was something I began to ponder. I really didn’t know how to start or what to do, and as a college student I didn’t have any money anyway. I graduated with nothing but a degree and student loan debt.

After graduation, I took a job that I hated making a salary that just barely covered the bills. I never forgot my aha moment from the apartment complex though I still didn’t act on it. Frankly, I didn’t know how to act on it or how to get started owning real estate.

After renting a house another year after college, I decided I should at least buy my first house. I thought about buying a duplex and renting one side of it. That way, the tenant next door to me would pay my mortgage for me. That might put me on the same track as the apartment owners. A grand idea, I thought!

But, for some reason, I didn’t do it. I bought a single-family house. So, guess who paid the mortgage? I did! I paid it out of my not-so-great salary that previously I’d been paying rent from. It would have been nice to have had tenants on one side of a duplex covering my payment or at least a large portion of it. That would have been a smarter thing to do from an investment perspective. I could have saved more money and begun to generate a small amount of passive income!

So, owning didn’t really feel a lot different from renting, except for the fact that it was mine. I had some pride of ownership knowing that I owned my own place. I remember at the closing table being scared to death when I signed the mortgage papers promising to make a payment to the bank every month for the next 30 years to pay back the $100K I’d just borrowed to make the purchase. But, it was my first step. And after buying that one to live in, it was easier to buy the next one and easier to buy rental properties. Since that day, I’ve personally bought a number of houses and worked directly or indirectly with clients to buy lots of houses, which I’ll detail to you later in this chapter.

I got married shortly after buying that first house, and my wife and I lived there for about four years. Because we decided to upgrade and buy a larger home before starting our family, we sold that house. I made about $10,000 on the sale. At the time, I thought I had made great money! However, looking back, keeping that house to rent out would have been really smart. Sure, I made money when I sold it, which at that time was big money for me, but I still regret selling it.

Looking back, I should have kept it. That house would most likely now rent for around $1,300 per month. My payment was only $600 per month, so I could be making $700 per month (or $8,400 per year) on it if I still owned it. So, I would be making almost as much EVERY year as I made during that one sale. That purchase did very little to move me toward owning rental property, building monthly cash flow, and achieving financial freedom.

Slow, Risky & Cumbersome: The Traditional Route

All of this was during the early years of our marriage before we had children. It wasn’t until later that I really began to see real estate as a viable retirement vehicle. All my life I’d been told to put away part of my paycheck into my employer’s 401K and to invest in IRAs every year. I’d been taught about the benefits of a ROTH IRA and taught to steadily invest and to diversify among stocks and mutual funds. My wife and I both put small portions of our paychecks into our employers’ matching 401K plans. I also had a financial advisor that I met with occasionally for future planning.

I learned that to figure out how much I would need to save for retirement, I needed to figure out when I wanted to retire, how long I thought I would live after I retired, and how much money I would need to live on and pay my bills in retirement. That’s enough to make my head spin! That’s a lot to figure out with a lot of unknowns a long time into the future. It seemed like chasing a moving target. Not having any clarity and not being able to see a clear path just didn’t seem like a good idea.

Ideally, you would want to save enough money for retirement that you could live off of the growth and interest of that retirement account each year. If you start pulling out principal, then your returns will decrease each year. If you are healthy and live a long life, you run a high risk of outliving your retirement.

So how much would you need to save in a traditional retirement account to replace your income? Vanguard has an online calculator that I found. I don’t know how accurate it is, but I ran these calculations, assuming you begin investing at age 30 and retire at age 65. This means you are saving money for 35 years.

If you get returns of 8%, you need to save 28% of your income each year in order to have the same paycheck you have while you are working. These percentages apply regardless of your income. For the examples, I used $5,000 per month, or $60K per year. In order to match that same income when you retire, you need to save $16,500 per year, which is about $1,400 per month for 35 years! That’s to have $5000 per month when you retire.

If you can consistently get a return of 10%, you’ll need to save 18% of your income or $900 every single month for 35 years ($11,000 per year).

At a 6% return, you would need to save almost 42% of your income or $25K of your $60K salary each year for 35 years!

Stop reading for a moment and click on this Vanguard Retirement Calculator link to plug your own figures into the calculation.

If for some reason the website link above isn’t working, then do a search of the following words to find it: “Vanguard retirement income calculator.”

In a nutshell, according to Vanguard, you need to be saving 18% to 42% of your income each year, depending on the return you are going to get, in order to replace the income you currently have unless you have other investments or income streams you can depend on. These calculations also do not factor in social security. Frankly, I just don’t know how reliable that source will be either in future years.

Honestly, this calculator doesn’t even really make sense to me. When I do simple math, and assume I save $25K per year for 35 years, that equals $875K without any interest during the 35 years. Just straight math. At a 6% return, it would equal $52,500 per year that could be drawn. They are calculating 3% for inflation, but it’s still difficult to understand. This is coming from the money managers, so I can only assume it’s accurate. But again, it’s confusing and difficult to figure out just how much you really need to be saving.

The takeaway: real estate is much simpler, and I’ll show you why—and how—throughout this book. But first we’ll continue to consider the traditional way.

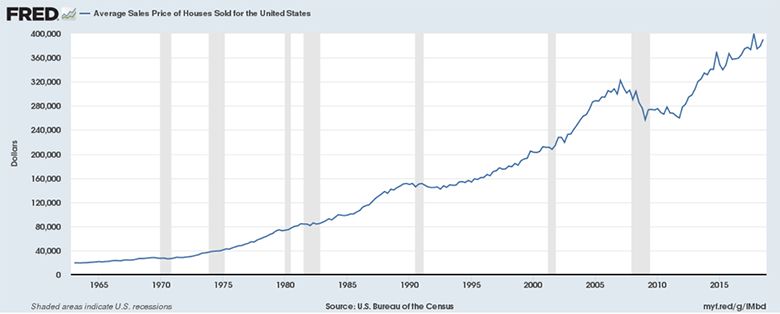

In order to calculate how much you need to be saving each month, you need to know what your return will be. So, what kind of return is realistic? Will you get 6% return or 8% return? Who knows with the stock market? It has had years of boom and years of bust. You can be doing great one year and then lose 20% to 30% in a year. I’m not sure why, but the Vanguard calculator does not allow the user to plug in a return beyond 10%. I think it’s because they don’t expect a return higher than 10% on average for the long term. Several sources indicate the S&P 500 has gained around 7% on average for the past 20 years. Who knows if the next 20 years will be more or less?

The following chart[1] shows the S&P 500 returns each year over the past 20 years.

The returns have soared in some years and tanked in others. My problem with this is that it’s simply unpredictable. What if you were planning to stop working and retire at the end of 2002? You would have lost 46% of your portfolio in the past 3 years! You would have to continue working and eventually gain it back in 2006. But what if you then decided to work a little longer until the end of 2008 since things were looking better? Then you would have lost over 38% in that one year! Ouch!

My point to all of this—how can anyone really know how well their stocks will perform or how much they will really need to save to be ready for retirement?

According to the AARP, a couple will have needed to save $1.18 million when they retire in order to have a $40K income each year and that would last them for 30 years after retirement.[2]

Can you save $1.18 million? If you can save $1.18M, can you live off of $40K in retirement? According to CNN Money, most Americans are spending more than $40K in retirement.[3] I understand that some believe that retirees don’t need the same amount of money they did when they were working because they will have less expenses. I don’t buy that. How will their expenses be less? Because they get the senior discount at Denny’s? I think not! I think expenses will be the same or more. Using this same principle, to have $80K income, you would need to save twice as much, or $2.36M. If you make $80K per year now and want to continue your lifestyle in retirement, is it realistic to think you can save $2.36M between now and then? How?

Several sources online indicate that healthcare costs are rising, and many estimate healthcare costs to be $200K to $275K out of pocket in retirement.[4],[5] I also don’t think that most predictions take into account leisure and travel during their retirement years. How boring would it be to retire and just sit at home watching Wheel of Fortune and watering your flowers? That’s not the kind of retirement that I want.

Personally, I want to continue living in retirement! If I’m going to be healthy and live to be 95, I want to be traveling, going to the beach and lake, spending time with family, volunteering and doing mission work, and enjoying life during those early retirement years. Honestly, I’m so driven I may never really truly retire in the sense that I stop working. I can’t sit still, so I’ll be doing something. But, I don’t want to have to rely on working for an income. I want a passive income, so that I’m free to do whatever I choose to do later in life. Don’t you?

One of the problems with traditional retirement planning is that most Americans are living paycheck-to-paycheck and simply aren’t saving at all for retirement. And when they see the huge amounts they’ll need to be storing away to lead to anything substantial in retirement, it just doesn’t seem realistic. It’s discouraging. There has to be a better way.

There is a better way—and that’s what I’ll be showing you in this book!

Another problem is that for most, as their income rises, their spending adjusts to absorb the additional amount of money they are making. We’ll discuss this more in future chapters, but do all you can to keep your expenses low, even when your income rises. Then you can put that additional income to work for you and your future. And whether you choose the traditional stock-investing route for retirement or the real estate route, you’ll need funds to do it. This book will show you how you can do it much more easily and quickly and with less of your own money through real estate.

Most Americans don’t have enough money saved for retirement and many will struggle. Social Security benefits will be questionable in coming years, especially for younger generations. Those funds are likely to run out in my opinion.

However, let’s say you are a saver and you can save $900 to $2100 per month as the Vanguard site recommends in order to have $60K per year income. This is an estimated $11,000 to $25,000 per year in savings. If you can do this, then I can show you how you can replace your income much more quickly than 35 years with income-producing real estate. This book will teach you how to do it in less than half the time. Or if you invest at this rate in the right real estate for 35 years, you’ll see how you can have an exponentially higher income and a much better retirement than you would if investing in traditional stocks and bonds.

If you can’t save this amount, real estate may still be a viable option for you. It will take you longer to replace your income, but it’s still much better than stocks and bonds, and will result in you having a much more lucrative retirement. It is a better path than traditional stocks, bonds, mutual funds, and IRAs.

So, you have the option of sticking with traditional means of saving for retirement, which, in my opinion, does more to help the financial managers make commissions than helping you be ready for retirement. Or you can look for a new vehicle. That new vehicle is income-producing rental property! It’s reaps returns for you faster, requires you to invest less of your own money, and, based on my experience, is more secure.

More Simple, More Certain, More Reasonable: The Real Estate Way

After seeing what would be required of us to save for retirement the traditional way and comparing that to investing in real estate, I quickly and easily chose my path. I became a real estate agent in 2004 and began to get an inside look at how others were creating financial freedom for themselves in their 30s and 40s. They didn’t have to wait until they are 65 to retire. Most are still working because they want to.

Around this time, I also read Robert Kiyosaki’s Rich Dad, Poor Dad, and that book changed my thinking. In it, Kiyosaki compares the differences in how his “two dads” (one who was actually his best friend’s dad) thought about and acted with money. While both made a good income, one constantly struggled with money while the other grew wealthy. If you haven’t read it, I highly recommend it.

The inside look at real estate investors that I personally met, combined with what I learned from Rich Dad, Poor Dad, acted as huge eye-openers for me. Suddenly, I could see the incredible possibilities of income-producing real estate, and the freedom it could create. And now, I’ve experienced it personally.

You don’t have to become a real estate agent in order to make real estate investments work for you. You can continue in your current job and simply have a real estate agent help you find and purchase the investment properties. I just happened to change careers because I hated my previous job and it helped me get an inside look at the possibilities.

I like to think that I’m smarter now and that I manage money and assets more wisely. Since buying that first house, I’ve bought and sold several. Some homes I’ve bought and kept as rental properties. Others I’ve flipped for a quick profit and used those profits to buy and hold other properties. In fact, I’ve invested in enough properties that I now receive a sizeable annual income from my real estate investments. However, I won’t consider myself officially free until the debt is paid off on all of these properties, which is what I’m working toward now. Proverbs 22:7 states, “The borrower is slave to the lender.” Since my goal is complete freedom in life, I’ve got to get the debt paid off. In addition, once the debt payments are gone, my net income will rise even more because the payments are gone. This kind of knowledge and financial freedom is what I want for you too, and it’s what I lay out for you in this book.

The only regret I have at this stage in my life is not buying more houses to rent and not buying more of them when I was younger. The houses I bought 13 to 15 years ago are now paid down to almost half of what I originally paid, and they are worth quite a bit more than what I paid for them. And, technically, tenants made those monthly payments, not me. Of course, I made them, but I did it with monthly rent payments received from someone else. It’s incredible really. The bank loaned me most of the money that I’ve used to purchase these properties, and complete strangers, the tenants, have given me the money each month to pay back the bank, plus extra money each month. They get up every morning and go to work, so they can send me a monthly check that I use to buy an asset for myself and my family. The property is in my name, and I own it while its equity (equity refers to the difference between a home’s value and the amount of debt on it) is rising, yet the tenants provide the funds to pay for it. I can choose to sell the properties or continue to rent them and reap the benefits. To top it off, the rents have increased significantly over the past 10 years. When equity grows and rents increase, the magic really starts to happen!

Real Estate: The Best Investment for the Long Term

I personally believe that almost everyone should have real estate for at least a portion of their investment and retirement strategy. For some people, it’s just not right for them, and we’ll discuss that in the next chapter. But, if you are reading this, you are intrigued by the idea, so it should be something you consider. Personally, I have very little stock, no 401K, and no commodities. I don’t actively invest in stocks, bonds, currencies, or commodities. My retirement plan is real estate. Plain and simple.

After just 15 years of investing in real estate, I’m already producing more passive income from it than the average salary. I don’t say this to boast or to brag. Deuteronomy 8:18 states that it is God who gives us the power to gain wealth, so I fully acknowledge that all I have comes from Him. Without Him giving me the knowledge and ability to do what I do, I would have nothing. Even the air I breathe comes from Him. So, I’m not boasting about what I’ve done. I’m only illustrating it to show you that you can do it too if you follow the instructions in this book. I feel it is my duty to help others with the knowledge I have been given.

So, what makes real estate such a great investment?

Several reasons. All of these may or may not apply in your situation, and we’ll go into these deeper later in this book, but consider the following:

1. It’s real. It’s a piece of the earth. In my opinion, real estate is simply a better investment because it’s real. You can see it, touch it, smell it, walk on it. And you have more control over its performance because you own it. You can’t do anything to control whether a stock price goes up or down unless you have a majority ownership in the company.

2. It’s secure. Specifically, residential real estate because people always need a place to live. Providing a place for your family to stay warm in winter, cool in summer, and dry in the rain is more important than automobiles, vacations, etc. Housing is a necessity. In fact, it’s the second tier on Maslow’s hierarchy of needs,[6] and it comes right after the basic need of food. If the economy gets really bad, people will pay for housing before they pay for other things.

3. It’s stable. In a down economy, the value of real estate may go down. Stocks and other assets will also go down in a bad economy. However, the real estate will always be there and will always provide value to whoever is living in it. It will still produce rental income. Stocks can literally go to zero.

4. You don’t have to sell real estate to get paid. Unless a stock pays a dividend, and many don’t, you must sell shares to get cash. If a stock does pay a dividend, it’s usually a small one. Real estate pumps out cash every month without you having to sell it. You keep the asset that over time goes up in value, and it still pays you every single month.

5. It provides you leverage. Will your bank give you a loan for 80% of your stock purchase? No. They will with real estate. And with leverage, if done properly, the tenant actually covers the mortgage with their monthly rent payment, and you STILL collect cash each month. This allows you to build momentum and grow your portfolio on your way to retirement.

6. Tax benefits. You can depreciate real estate (take tax deductions) while it appreciates (goes up) in value. The interest if you have a mortgage is also tax deductible. Chapter 10 addresses these tax advantages in more detail.

7. It is very forgiving. I’ve made mistakes and seen others make mistakes in real estate, but because of the investment itself, it’s easier to be creative and find a way to make the investment work rather than losing it all. A stock can literally go to zero if the company you are investing in goes under. It’s not likely for real estate to go to zero.

8. More people are renting. This trend means a higher demand for rental units. Even more seniors are now choosing to rent. Since 2006, the number of homeowners in the US has declined and the number of renters has increased.[7]

9. My favorite reason—monthly CASH FLOW.

I get paid passive income every single month from the properties I own. I don’t have to wait for the values to up in order to make money.

Reaping Big

Most people who are homeowners would agree that their house has been their “best investment.” Or at least one of their best investments. You hear it all the time. If one house is their best investment, what would multiple houses mean? Wouldn’t it be wise to own more than one?

A home is a tax shelter and a forced savings account for most Americans. What I mean by that is that each month as you pay that mortgage, the balance gets smaller and smaller, building what is called equity. Over time, the equity grows and eventually, once the loan is paid off, the owner’s equity is the full value of the home. To repeat, equity is defined as the difference between the value of a home and the amount of debt on it. For example, if you own a home that’s worth $200K, and you have a loan of $150K, then you have $50K equity in the home. If you sold it and paid off the mortgage, you are left with the equity of $50K, which can be converted to cash. Over time as you pay down that $150K mortgage, the debt gets smaller and the equity gets larger. Additionally, if the home appreciates in value, then the homeowner’s equity grows as well. With rental property, it’s not even the owner who pays off the loan. The tenant pays it off with rent payments made to the owner. So, when I say it’s wise to own more than one home, I don’t mean a vacation home or second home. I mean an income-producing property that someone else pays for because it provides them a place to live.

While cars, clothing, food, and everything else that’s real have gone up in price over the years, so has real estate. Yes, we did have a recession recently, but the only people that lost in real estate during that recession are the people who sold their homes for less than they paid or those who let their homes go back to the bank. No one else lost money. And now, 2018, generally home values are higher than they were pre-recession.

As a real estate agent, I helped several buyers, many who were first-time homebuyers, to purchase homes during the recession. They were buying them for literally half of their pre-recession value. Now, many have sold and doubled their money. It’s nice to see young couples sell their homes and walk away with $50K to $100K tax-free. It’s because they bought real estate. Those who rented a place to live for the past 10 to 15 years don’t have that opportunity.

Investors have also sold homes they bought during those time periods and made a lot of money. For the investors, the payments were covered by the tenants, but they can now sell for large profits. Just imagine what it’s like for those who bought 10, 20, or even hundreds of homes during the downturn. There are those who did it, and they are reaping big benefits now.

Personally, I bought a few houses prior to the recession. When the values plummeted, I wondered if I had made a mistake. However, I held on, let the tenants continue to make the payments, and I’ve got great equity in those homes now. Even if the equity didn’t come back, those houses continue to pay me every single month. And they paid me every month during the recession. I would have lost if I had lost sight of my long-term vision, became fearful, and sold when prices were low. Actually, I was able to refinance those mortgages to shorter terms, lower interest rates, and lower payments during the recession.

I wish I had bought homes in 2010 and 2011 when prices were at the bottom. Hindsight being 20/20, I would be in a much better financial situation now. I was actually digging into savings just to pay bills during those years. There was no commission money left over to invest in real estate even though it was the best time in decades to buy. If I had known more about the alternative funding strategies discussed in Chapter 8 at that time, I would likely own more houses now.

My income was actually negative in 2010. That’s right, the income on my tax return was a negative number, meaning it went backwards for that year. My business expenses were higher than the income I received. However, now, less than 10 years later, I am earning more than an average salary through passive income-producing real estate. When done properly, income-producing real estate is a powerful wealth builder and monthly cash-flow builder.

If you have money sitting in the stock market, a savings account, or CDs, and you are not happy with the performance, consider moving some or all of it to real estate. Even if you are happy with your returns, consider diversifying it. At the time of this writing in 2018, the stock market is soaring. However, we could see a correction at any time. What would happen if you saw the stock market adjust downward 30% to 35% over the next year? How would that affect your net worth and your retirement plans?

I think you’ll find that, when done correctly, your real estate investment(s) will outperform most other simple investment vehicles. To find out how, continue reading.

CHAPTER 2

Is Real Estate Right for You?

You must decide if investing in real estate is right for you and your personal situation. We are going to get into the pros and cons throughout this book. As you go through it, either you’ll get really excited about real estate or you won’t. If you do, real estate may be for you. If you don’t, quite honestly, you might want to find another investment vehicle. In my opinion, income-producing real estate is a better investment than most other options, but if you aren’t excited about it, don’t do it. While it’s a mostly passive investment, it will require some action on your part and you’ll need to be willing to take that action, which we’ll review in the coming chapters.

Owning rental property is not for everyone. In this chapter, I’m going to outline the aspects that some people find difficult. I’m not sharing this with you to scare you. I simply want you to have a good idea of what you’re getting into and show you the full picture.

Eyes Wide Open: The Risks

There are risks involved. These risks are numerous. These risks include things like making unexpected repairs, making mortgage payments, and dealing with tenants.

Homes and their systems are man-made and mechanical, so things will fail. Homes must be maintained, or they will deteriorate and cost more money to repair later. You must be able to make decisions about caring for the properties. And you must have the cash on hand to make these repairs when they are necessary.

If you purchase with financing, then you must make a monthly mortgage payment even when the property is vacant. If you don’t make that payment, you’ll lose the property in foreclosure. You are exposed to the volatility of the market. If the market goes down, can you handle it? I don’t expect real estate values to fall again like they did during the Great Recession. However, no one knows. It could happen again. It’s bad enough to see one property you own go down 40%. What if you own multiple properties, and all of their values go down 40%? Losing 40% on ten homes is worse than losing 40% on one. Again, this is only a paper loss unless you sell. But, it’s a loss in your mind, your balance sheet, and a loss to your financial net worth either way. If you have loans, the banks could ask for more cash, depending on your loan structure. If you are going to invest in real estate, you must have the guts and the will to get through these tough times without losing your sanity.

There are people involved when it comes to owning real estate. These people include tenants who must be handled and dealt with properly. Some of the situations with tenants can be very uncomfortable. Can you handle it when they have a pet they aren’t supposed to have? Can you have the hard conversation when they don’t pay the rent? Do you have the backbone to evict them when necessary? You must be willing to treat real estate investing as a business because that’s what it is.

Will you be able to handle repairs that are needed from time to time like leaky faucets, replacing a ceiling fan, or repairing a heating and air unit? On that rare occasion, when a tenant moves out and the walls are busted up and the carpet is stained and smells like pet urine, are you going to keep a level head? Are you going to be able to restore the property, put it back in service, and keep going? Or, will you be too upset to even function? Some people are too upset and simply can’t handle it mentally. I’ve worked with these kinds of clients, and they end up making irrational and emotional decisions that aren’t good for them. It causes them to make mistakes. You have to go into it realizing that these kinds of things happen occasionally and are just part of the business. A myth is that tenants always leave houses completely trashed and in disrepair, but reality is they rarely do. As you gain experience or have an experienced manager, you can greatly minimize these kinds of events.

Some landlords don’t know how to handle tenants and repairs, and these are the ones who complain about owning real estate. These are the ones that will tell you it’s a bad investment and to stay away from it. Not managing the property and the tenants properly can be the difference in making a great profit from owning real estate and losing it all.

You need to make sure that owning real estate is something you want to do. Some owners get around these issues by hiring professional management. This way, they don’t have to deal with the tenants or the repairs or damages. They simply see the financial side of it and entrust the management of the property and tenants to someone else.

By hiring a top-notch property management firm, a lot of these headaches are removed from you. While you are still involved to a degree, it makes it a more “passive” investment, like your stock portfolio. And honestly, if you are a busy individual, who owns a business, works a lot of hours, has a family, or generally does not have a lot of free time, I definitely recommend you turn your property over to a management company. We’ll talk more about finding and hiring a property manager later in chapters 11 and 12.

Unless you have plenty of time and enjoy the tedious tasks that come along with owning and leasing property, hiring a manager is what you need to do. Relatively speaking, property management is cheap compared to the value you will get from it. Even with professional property management, you must be prepared for expenses to arise related to owning the property. This should be expected and not surprise you. Owning rental real estate can be messy, but it can be lucrative.

So, if you don’t think you can mentally handle dealing with expenses and tenants, then you may want to avoid investing in real estate. If you can’t do it yourself or trust a property manager to handle things for you, then it may not be for you. However, if you are able to see the big picture, understand how lucrative owning rental property can be, and navigate the challenges of it, then keep reading because this book is for you.

Besides making sure you can face the not-so-easy part of owning real estate, you need to make sure you are prepared financially. That’s what the next chapter is all about.

CHAPTER 3

The Financial Prerequisites

If you aren’t in the right place with your finances, you can fail before you even get started. I strongly recommend you take the advice of this chapter before you buy your first property.

Before you can begin buying real estate, you need to make sure your personal finances are in order. If you have loads of cash, then this chapter may not apply to you. But, if you are trying to buy your first rental house, you need to consider these four prerequisites.

One—if you are living paycheck-to-paycheck and spending 100% of what you make every month, in my opinion, you are not ready to buy rental property. You need to either find a way to increase your income or reduce your monthly expenses.

Two—if you have credit card debt or other consumer debt, in my opinion, you need to eliminate those before investing in real estate. The more you can eliminate other debt, the faster you will get to your goal of being financially free, and the funds that are currently going toward those payments can be put toward your investing. Also, as you pay off this consumer debt, your credit score will be higher, which will enable you to get a loan from the bank more easily and with better terms.

Three—you need to have some funds set aside to cover unexpected property repairs or surprises as they come along. So, in addition to your down payment for the property, or the purchase price if you are paying cash, you need to have some funds set aside in case you need to replace a heating and air unit, water heater, roof, etc. Repairs can often be unexpected, so make sure you have a back-up plan. The back-up plan is funds set aside ONLY for unexpected surprises like major repairs or vacancies.

Four—if you are planning to finance the purchase with a traditional bank, you’ll need a minimum of 20% as your down payment. There will also be loan and closing fees that will typically be in the range of 3% to 5% for the average property. If you are paying cash, your closing fees will be less, but you’ll need 100% of the purchase price.

In chapters 7 and 8, we’ll discuss options for buying homes without a down payment. It’s more difficult, but there are ways to do it. However, in my opinion, you’ll be in a much better position to be successful in the long run if you start with some money in the bank.

Why these four prerequisites? While it’s not imperative that you have 20% cash on hand, I still recommend minimizing your other expenses and ridding yourself of consumer debt before buying real estate. Otherwise, it will add a ton of additional stress and you’re setting yourself up for failure if even one little thing goes wrong. If you have too much money going out each month and not enough coming in, you will not be prepared to weather the storms as they come.

So, if you already have at least 20% of the purchase price to put down, funds for reserve, and have no consumer debt, you can move to the next chapter, although reading to the end of this chapter may give you some additional insights and ideas. If you are not financially prepared, read on and focus on getting yourself ready to become a real estate investor and find your financial freedom.

Not Quite There Yet?

If you currently are living paycheck-to-paycheck and struggling just to pay bills, I understand. I’ve been there. But, you absolutely cannot remain in this place. It’s imperative that you figure out ways to cut your expenses and increase your income, so you can invest. A small amount of discipline in this area now will reward you handsomely in years to come. You must commit to it. You must have the willpower and self-discipline to make changes.

This may seem like a huge obstacle to get to a place where all of your consumer debts are gone, you have a reserve account, and you have 20% down. It seemed like a big step to me as well before I bought my first rental house. Remember, you’ve got to start somewhere and once you start, you’ll have more income, which will pay down more debt, which will increase your income. It’s a snowball effect once you get going. But, you must start.

To start, you’ve got to have the discipline, hustle, and desire to make it happen. So, how do you get to a place you can start?

Spend Less

The first step is to begin living below your means. In simple terms, you need to spend less than you make. And if you are carrying a credit card balance right now, then either you are not living below your means or you have not lived below your means in the past. You must pay more than the monthly minimum on those cards, and you must stop adding new charges. Cut up those cards or lock them away.

There are only two ways to get ahead financially. One way is to cut expenses. The other way is to increase income. That’s it. Only two ways!

My preferred method is to increase income. That’s proven to be a better path for me. It’s easier for some than it is for others, but you must do one or, even better, a combination of both cutting expenses and raising income at the same time!

A Budget

Create a budget. Go through all of your expenses and see where you can cut out some unnecessary expenditures. Can you do without cable TV with the extra sports package, eat out less, or take a cheaper vacation? Stop spending your money on unnecessary things. Find out where you can make cuts and make them. Be disciplined enough now so that you can reap the rewards later. It’s called delayed gratification. The more you can delay now, the more you can be grateful for later.

Discipline or Regret: Your Choice

I’m reminded of a study I read about regarding kids and delayed gratification.[8] The study was conducted by a psychologist with a major university decades ago. Children were placed in a room and given the choice of having one treat now, a marshmallow, cookie, etc., or they had a second option that would reap them more rewards: not eat the treat immediately, and instead wait for a few minutes to receive two treats. The follow-up study proved that the children who could exercise the willpower, self-discipline, and delayed gratification to wait a few minutes to get two treats proved to be more successful in testing and generally more successful later in life.

This self-discipline will translate to all areas of life, not just finances. It takes self-discipline to stay healthy, to eat right, and to exercise. It takes self-discipline to learn a new skill. Those who can exercise proper self-discipline and willpower can get ahead.

The late Jim Rohn, one of my favorite motivational speakers, said, “We must all suffer from one of two pains: the pain of discipline or the pain of regret. The difference is discipline weighs ounces while regret weighs tons.”

So, you can either exercise discipline and willpower now to have a better future, or you can regret not having the discipline when you are actually in the future and can’t afford to take care of yourself.

I encourage you to stop reading right now, sit down, go through your bank account, and itemize all of your expenditures for the past month. Then go through with a different colored pen and start marking which ones you could have done without. Then total that figure. That’s how much you could save each month. Use that amount to start paying off your consumer debts and getting your finances in order for a better future.

I can guarantee you that there is someone, somewhere, living on less income than you are. They may not be as comfortable as you are, but they are doing it nonetheless.

The more you can cut from your expense column, the faster you can get to your financial goals. If you can only cut a small amount, that’s OK. It just might take you longer to get there unless you are able to increase your income.

Dave Ramsey, businessman and author, likes to say, “Live life now like no one else, so you can live later like no one else.” What he means is live without as much now, so you can be wealthy and live better than everyone else later. And by the way, he has some great resources about getting out of debt, creating a budget, etc. Let me add that while he gives great advice and I follow many of his teachings, I don’t agree with him 100% on everything he says. For example, he is very anti-debt. I believe there is good debt and bad debt, and I think debt has its place and can be used as a tool. (We’ll discuss this more later as well.) Debt is often misused, and that’s when people get into trouble. So, while I follow his teachings and agree with him on most points, I don’t agree with him on every point. That’s OK. His ideas have helped me a lot, and he makes a lot of sense. So, read his books or take his courses. You may find some insight as well.

More Cost-Cutting Ideas

If you have credit cards, cut them up or put them where you no longer have access to them. If the numbers are saved on your favorite websites, delete them out. If you have an automobile and you are making payments, you might consider selling it and buying an older, but well-maintained used car for cash, so you eliminate that payment. Find ways to free up cash each month so that you can knock out the debt and save for your down payment and future investing.

While cutting expenses is one method, it’s hard! It’s really hard! And, you have to make a lot of cuts and a lot of sacrifices to save a little bit of money. And it takes a long time of saving just a little bit of money to add up to enough to put 20% down on a property.

If you make $60K per year, and you are able to cut expenses by 10%, that’s $6,000. That’s a lot of money, but at that pace, it will take a few years for you to save enough for a down payment. But, if you remember from the previous chapter about saving for retirement, you need to be putting this money away and investing it somewhere anyway to secure your future.

I really think this is the main reason people give up and don’t even try to invest. They throw their hands up and decide it’s just not worth it. They aren’t committed for the long haul, and they lose sight of their future. They would rather live paycheck-to-paycheck and figure out their future later. But really that’s like sticking your head in the sand and pretending it doesn’t matter. It does matter. I know it’s hard to do without things you like when you see others having them. I get it. And there is an alternative to pinching every penny. It takes a lot of work too, but it is my preferred method.

Upping Your Income

My preferred method is to increase income. I’ve found that if you are creative and work hard, it can be easier to increase income than it is to cut expenses. If you work an hourly or salaried job, it’s not going to be easy for you to increase your income because you are not in control of it. However, I’ve seen employees who work really hard move up the ranks and see rapid rises in income. This happens when they are working for an employer who really sees what they are contributing and appreciates it.

Well-Compensated for Your Worth—if you are providing lots of value for the company you work for, they should see it and reward you for it. If not, go provide the value to another company that will appreciate you or go create your own way by working for yourself. If you feel you are really contributing to your company and not being paid what you are worth, go ask for a raise!

The only way you can have complete control of your income is to become self-employed, build a business, or find a commission sales job. Improve your skills and go make more money! Find something you can excel at where your income is not capped.

Side Hustle—another option would be to create a side hustle where you are selling a product or service either online or through multilevel marketing or something of that sort. I’m not a huge fan of multilevel marketing, but I’ve seen people do really well with the right product, the right team, and the right support.

If you can’t bear the thought of working for yourself, you might just consider a part-time job working for someone else and then pay off debt or save all of the money you earn from the extra job. You will have a guaranteed income this way, and it will be steady. There is less risk this way. However, when working for yourself, if you are successful, you can move the needle much faster.

Second Income—if your spouse doesn’t work, let your spouse get a job and earn the extra income. Then all of this new income can go toward investing or getting yourself prepared to invest.

Invest One Salary—in fact, if you are newly married, I recommend you start out learning to live off of one income. If you are single and not yet married, but plan to be in the future, let that be a goal. Live off only one income even after you get married and you are both earning incomes. That will put you and your new spouse years ahead of your peers when it comes to investing and getting ahead. You can save and invest one salary every year!

When my wife and I were first married, she had a part-time job and I had the full-time job, so we learned to live on less. Once she got hired full-time (and was actually making more than me), we continued to live off of the same income, which allowed us to completely save almost all of what she made. Do you think that made it easier for us to get started investing? Yes, it did!

Play Defense—a mistake that most people make is as they begin making more money or as they get a higher paying job, they immediately find something to spend the extra income on. They either buy a new house to live in, a new car, new boat, new clothes, or something. And within a few months they are back to living paycheck-to-paycheck. This is a huge mistake. So, when you get that extra job, that raise, or you start making money from a side hustle, don’t spend it! Don’t earn extra income in order to spend more. Earn more, so you can invest more!

Figure out how to increase your income but continue to live off of the same amount. This is what I call playing defense. It allows you to keep some funds to invest in assets that will produce income back to you.

The average salary in the US is $81,400 per year. So, if you can live off that and your spouse also makes $80K per year, then you can get out of debt and get started buying investment property fast! The problem for most people is that if the household income is $160K, they spend $160K, or sometimes even $170K, every year. If you can learn to live off of one income, then you can really make huge strides with your investments and replace that income very quickly.

In Georgia, where I live and work, the average income is $59,100. How different could things be if you could save that amount of money each year to invest?

A Caveat

I also want to give you one word of caution. While having money to invest is important, keeping your family together and spending time with your spouse and your children is even more important. So, before you go get a second job or your spouse gets another job, weigh the cost and make sure you are not sacrificing your family for a dollar. If you strongly believe that one spouse needs to be home with young children, then don’t sacrifice that conviction in order to gain financially. Your family and children will always be more important than finances.

Please read that previous paragraph again. Do not sacrifice your family just so you can get ahead financially. If you have millions and millions of dollars, but no family to spend it with, what have you gained? In my opinion, you lose.

Good vs. Bad Debt

Earlier, I mentioned good debt and bad debt. It’s interesting, but in some cases, I can agree with using debt; in the other cases, I hate it.

I hate consumer debt. I hate credit card payments. I hate car payments. I just don’t like having extra payments each month. They are such a burden and weigh heavy. And they come up every month. It’s enough to pay for electricity, food, cell phones, Internet, entertainment, etc. I don’t want to also pay a credit card, car payment, time-share payment, and boat payment too! It’s just too much.

To look at the flip side of that coin, I like recurring money coming in every month (in the form of rent), but I don’t like it going out every month in the form of payments. If you can flip the equation, so you have more and more people paying you each month and you are paying fewer and fewer bills each month, you are on the right track. I hope this is a light bulb moment for you.

Change your thinking and think of it this way: money is always flowing one way or another. You need to figure out how to make more of it flow into your account than flows out of your account. As more money flows in and less money flows out, that margin will grow and your bank account will grow. As you have more money, it can be invested to multiply and create more. It’s like your money having babies and making more money.

When it comes to borrowing money to buy a house or condo to rent to someone else, I like using debt. Why? Because I can increase my income. Even though I have a new payment, and more cash going out, I like it. Because if I buy a rental property, add a new mortgage and new payment as an expense, I know I’m also increasing the amount coming in in the form of rent. If I have a new mortgage payment of $800 per month, but a new income stream of $1,200 per month, I’m adding $400 per month to my account. This is unlike new car payment of $800 per month, which does not add to my income. It only subtracts $800 per month from my account. I only want to add an expense IF I can add more income at the same time. Make sense? That’s what I call good debt.

Borrowing to buy rental properties gives me leverage to buy more properties, so that I’m technically not the one paying for that debt. Who is paying it? The tenant, of course.

Every day, that tenant wakes up, goes to work, and earns a paycheck so that they can send me a payment each month for providing them a place to live. This increases my income. When I receive their check, I make the mortgage payment and put the extra cash in the bank for repairs, surprise expenses, and save it up so that I can buy more property. When I do this, the amount that I owe to the bank decreases little by little. And after 180 or 360 months, depending on how it’s financed, it’s paid off. Does the tenant then have title to the property? No! I do! And it’s been covered by usually several different tenants over the years.

Think about this.

Read this next paragraph and let it sink in:

To invest in real estate, you can get money from a bank to purchase it, then get money from someone else that you don’t even know (the tenant) to pay back the bank, yet you get to own the property and enjoy the cash flow, appreciation, and tax benefits that come with owning it. What other investment offers this? The tenant contributes to your net worth and eventually pays off the property for you.

I know what you are thinking—there are taxes, insurance, new roofs, new water heaters, and all kinds of expenses. Of course, the popular statement, “I don’t want tenants calling me in the middle of the night because their toilet is stopped up,” stops many people from buying real estate. However, I’ve never had one of my tenants call me in the middle of the night for a stopped-up toilet. That’s just an excuse people make. And as we’ll discuss later, by hiring a property manager, you never meet or ever speak with the tenant about anything. You just collect their money.

Yes, there are expenses, but when structured properly, the tenant covers those too and there is still money left over each month. That’s how you get to a place of financial freedom. And, after 30 years, the house is likely going to be worth more than twice it’s purchase price, and you’ll own it free and clear.

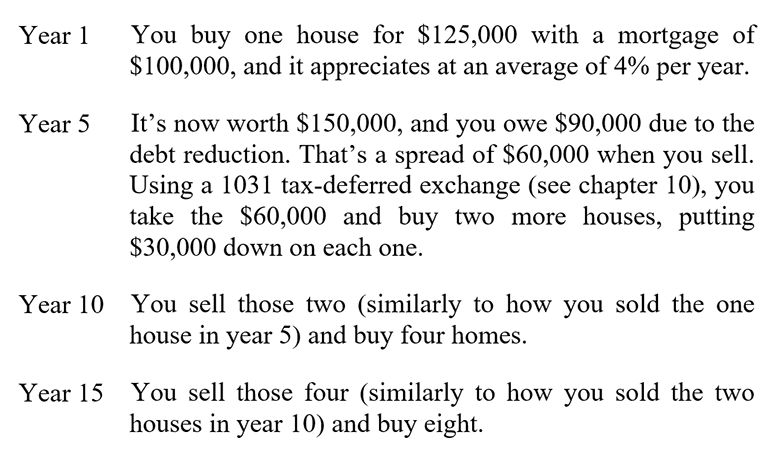

I currently own a property that is worth more than twice what I paid for it, and I’ve only owned it for 10 years. The mortgage is not paid off, but I have way more equity in it than what I owe. If I sold it now, I would put more money in my bank account than I originally paid for it.

So, yes, it’s hard work to get into a position where you can make your first investment. But, it’s totally worth it. Can you imagine how your life could look if you owned ten homes free and clear when you are ready to retire? Or twenty homes? Or fifty homes? Or hundreds?

I only mention the larger numbers because I want to show you that it’s doable. However, for most, just having enough to cover expenses will be the goal. And to acquire 10 homes prior to retirement is not hard to do and that could be enough to give you a six-figure retirement income. To me, that sounds much better and much easier than trying to save and invest $2M to $3M out of your paycheck into stocks and mutual funds to achieve the same lifestyle in retirement.

I know owning multiple homes may seem like a hard concept for you to imagine. It was for me 10 to 15 years ago as well, but as I bought the first one, then the second one, then more and more, it became more of a reality. And because each property makes you money, every time you add another one, your income rises. Because you keep expenses low as your income rises, each new house gives you more funds to buy another house, which gives you more funds to buy another house.

In chapters 7 and 8, we’ll discuss options for buying properties and how to get the funding. However, before you can get the funding to make a purchase, you need to get those four prerequisites out of the way. These include paying off consumer debt and having some money in the bank.

Once your finances are in order, you are ready to go shopping for a property. Real estate is real estate, but there are several different types of real estate and they are all different. Within the different types, there are different classes as well, so before you can go shopping, you must know what you are shopping for. In the next chapter, we’ll discuss the different kinds of income-producing real estate and the pros and cons of each.

CHAPTER 4

Choosing Niches: Key to Riches

When someone thinks of investing in real estate, that could mean a lot of things. There are a lot of directions and a lot of different kinds of real estate that can be purchased. While the context of this book is written primarily for investing in single-family residential properties, which is my personal focus, I want you to have an understanding of the other niches as well. And the general principle of income-producing real estate applies to all different areas and niches, but the nuances of each are different.

In this chapter, we’ll discuss some of the more common types of real estate and the pros and cons of investing in each. For example, owning a single-family home is very different than owning a retail shopping center, which is very different than owning a mobile home park. They can all produce cash flow and income but are all quite different. You’ll need to learn about the various types and determine which is best for you.

This chapter discusses the following property types:

- Single-Family Homes

- Condos/Townhomes

- Mobile/Modular Homes

- Mobile Home Parks

- Small Multifamily Homes

- Large Multifamily Homes

- Student Housing

- Commercial Property

- Land

Then among these different niches and property types, there are asset classes A, B, C, and D, which is a grading system to help you niche down even further. We’ll take a look at these asset classes in this chapter as well.

The first and most common property type we’ll discuss is the single-family home. I personally own more of these than any other type, and right now it’s my favorite.

Single-Family Homes

To start, let me give you a general definition of a single-family home. When I say single-family home, I’m referring to a detached home that one family would live in. Typically, these homes have between two and four bedrooms and between one and three bathrooms. They would have some kind of yard, large or small, and would not be attached to other structures, which differentiates them from condos, apartments, or duplexes.

In my opinion, single-family homes are the easiest and least risky types of investments you can make. They are easy because they typically attract a high-quality tenant who has a steady job, is mature, and is willing and able to pay more in rent than the cost of an apartment or condo.

Another advantage is that the tenants typically stay in single-family homes longer than they do in apartments or condos. The transition, or “turn,” between tenants can be costly. Turning entails getting a unit ready to lease after one tenant leaves and before the next one comes in. It includes painting, cleaning, replacing flooring, etc. You want to minimize this as much as possible, and my experience has been that a tenant will stay in a single-family home often longer than they will stay in an apartment or duplex. Single-family homes also rent more easily and quickly when compared to other classes of real estate, based on my experience.

I also believe that these are the easiest to sell if they are bought in the right locations and they are kept in good condition. Single-family homes have better odds of appreciating rapidly, which means rising in value. I rarely recommend selling unless you have a need to sell or if you desire to reinvest to buy other properties. However, if you find yourself in a situation where you must sell, the single-family homes that make great rentals are generally easy to sell. These are the homes that might be considered starter homes. They are easier to sell than luxury homes simply because they are affordable and typically in high demand. These homes can be sold to another investor or to someone to live in.

Typically, you’ll get the highest price by selling to someone that wants to live in it. It may be a first-time homebuyer or an empty nester. Either way, your buyer pool is larger because you have options to sell to more than just other investors whereas most of the other types of real estate we’ll discuss would most likely only be sold to investors.

When selling to a homeowner, just keep in mind that the home will need to be free of a lease, and sometimes that can be tricky. It takes some planning ahead to sell it for top dollar. It’s not as easy as selling a stock or some other paper investment, but selling a moderately priced single-family home in a good location is typically not hard to do, especially when you hire a great real estate agent to help you.

Condos/Townhomes

Condos and townhomes are typically attached units that are very similar to their neighboring units and located in a community with multiple units. Condos and townhomes are going to look very similar to apartments, but unlike apartments that all have one owner, condos and townhomes have individual ownership. The legal difference between a condo and townhome is that when you buy a townhome, you do actually own the earth beneath the townhome. With a condo, the legal description is basically the unit itself, or one way to think of it is you only own the air space within the unit. With a condo, the ground and the earth under the unit are owned by the condominium association. The condo and townhome associations will also have rules and by-laws that must be adhered to as an owner of a unit in the development.

I would consider condo/townhomes to be next of kin to single-family homes. However, condos and townhomes typically will lease for less than a similar single-family detached house in the same area. On the flip side, they can also be purchased for less, so your return on investment (ROI) on condos is similar to single-family detached.

One thing that is different with condos and townhomes is that they typically include a monthly homeowner’s association (HOA) fee. So, this fee will need to be figured into your cash flow calculation when you are considering it as an investment. This fee covers amenities that may be on the property, such as a pool, fitness center, lawn maintenance, trash pick-up, etc. These things are also very attractive to some tenants, so keep that in mind if you decide to invest in condos.

Amenities, location, and updates to the kitchen and bathroom are the things that will attract tenants. If the property has desirable amenities, the unit will be more desirable to rent as well. The location may be more or less desirable depending on what’s around it. And the updates could be things that make the unit more modern like granite countertops, stainless appliances, and modern floors.

Some other benefits to you as an owner of a townhome or condo is that there is no lawn care or exterior maintenance that you will be responsible for, as the HOA will cover it. Some owners love condos because they are largely maintenance-free and some see them as easier to own and manage.

They can sometimes be harder to resell. Because condos are so similar, they often have the same floor plan, bedroom count, and finishes, so there is very little differentiation between units. You are at the mercy of what other units are selling for because units typically sell closer in price to the other units in the development whereas single-family homes are more unique and can have differing features even within the same subdivision.

Mobile/Modular Homes

Mobile and modular homes are similar to single-family homes. However, whereas most single-family homes are going to be built on site and permanently attached to the land, mobile and modular homes are built in a factory and assembled or installed onto the property. Often, they are permanently attached to the land, but the defining difference is that they are not built on-site. Due to this fact, they can be purchased at lower costs but are also typically less desirable because they are cheaper to build and considered lower quality.

Mobile homes are more common in some areas of the country than in others. In some areas, they are very common and you see them throughout town while in other places, they are only found in rural areas or less desirable or high-crime areas. So, choosing whether or not to invest in mobile homes is very likely location-specific. You’ll need to make this determination.

Some things to consider are the fact that mobile homes are not built the same way that other structures are built. Since they are built in a factory, often with sub-par materials, and then taken to a location and set up on blocks or a concrete foundation, they can be less desirable. The positive thing about mobile homes is that they can be purchased less expensively than a single-family home. And, if the mobile home is on a lot in the country or even in a subdivision, it offers a lot of the same draws as a single-family home but will likely rent for less per month. It can also be purchased for less.

Financing can sometimes be difficult with mobile homes. It’s difficult to get a long-term fixed-rate loan on a mobile home like you can with houses or condos. The Federal Housing Administration (FHA) will finance them for owner occupants if they have the proper tie-downs and meet their specifications for a permanent foundation along with other engineering guidelines.

Mobile homes actually have titles like automobiles when they are first manufactured. The only way to get financing through the FHA is for this title to be retired, which means the mobile home is considered permanently attached to the land. This is a process that you must go through and is state-specific, so do your research before investing in mobile homes. The FHA only provides financing for owner occupants, so it’s not an option for investors. The only option for investors to purchase is to pay cash or work with a local bank for a short-term loan. We’ll discuss financing options in more detail in chapters 7 and 8.

Since mobile homes are more difficult to finance, even for owners, keep that in mind as part of your exit strategy. They can be more difficult to sell conventionally. Some investors love mobile homes because the investor owners will owner finance them or sell them under a lease/purchase or lease/option. Chapter 15 will cover this in more detail.

The important thing for you to know is that mobile homes are different, so you need to go deep on understanding them before you invest. They can be great moneymakers and produce a great monthly cash flow if you have the right strategy.

Mobile Home Parks

While we are on the topic of mobile homes, I’ll go ahead and mention mobile home parks. Mobile home parks are communities of several mobile homes where all of the land (and sometimes the mobile homes also) is owned by one individual or entity. These are very much a niche and something that I personally don’t have a lot of experience with. However, I do know that these can also be very lucrative if you know what you are doing.

There are two ways to make money with a mobile home park. One is to lease the structure on the lot just like any other dwelling. The other is to only lease the lot or the land that the mobile home sits on.

By leasing only the lot, as the landlord, you are not responsible for any repairs to the mobile home. You don’t even own the home itself. So, when the AC breaks or the water heater fails or the roof leaks, you don’t get phone calls. It’s the tenant’s property, so it’s on them to repair. By owning the lot, you just have to make sure utilities are there, either sewer or septic, and that water is available. This hands-off approach is attractive to some investors. It’s similar to a ground lease, billboard lease, or cell-phone tower lease.