68 percent of mutual fund–owning households will own them through 401(k) plans, but the sales channel outside of retirement accounts is still highly important to fund families.

68 percent of mutual fund–owning households will own them through 401(k) plans, but the sales channel outside of retirement accounts is still highly important to fund families.If the majority of mutual funds are unable to do what their marketing professes they can, who is it that keeps throwing their money at these things? Good question.

According to the Investment Company Institute (ICI), mutual funds now account for 20 percent of all American households’ financial assets. ICI reports that “between mid-year 1989 and mid-year 2010, assets held in mutual funds have increased from $899 billion to $10.5 trillion. The number of U.S. households that owned mutual funds rose from 23.2 million to 51.6 million over the same period.” ICI goes on to tell us that “as of mid-year 2010, 43.9 percent of U.S. households owned mutual funds, representing 90.2 million individual mutual fund shareholders.”

Using data from 2010, we see that typical mutual fund investors are middle aged, employed, and married. They are making about $80,000 a year, and their household net worth is in the neighborhood of $200,000. Mutual funds make up about half of their portfolios. They also tend to have some kind of a retirement account, like a 401(k) or an IRA. The 401(k) or other qualified plan account will be dominated by mutual funds unless the holder is the employee of a public corporation, in which case company stock will be a big part of the mix. The statistics show that:

68 percent of mutual fund–owning households will own them through 401(k) plans, but the sales channel outside of retirement accounts is still highly important to fund families.

72 percent of mutual fund investors will also own them outside of the plan.

58 percent of mutual fund–owning households have been sold their funds by brokers, financial planners, insurance agents, accountants, or bank employees.

36 percent—a smaller but still significant number of investors—have bought fund shares of their own volition, either directly from a mutual fund company or in their discount brokerage accounts.

As for income levels:

39 percent of households holding mutual funds had an income level somewhere between $50,000 and $99,000 by 2010.

21 percent of fund-owning households earned somewhere around $100,000 a year.

44 percent had assets of more than $250,000.

In other words, mutual fund investors make good customers for other investment products and services.

As can be expected, the majority of mutual fund households are headed by members of the baby-boomer generation. They’ve been treated well by their involvement with funds over the years, at least until the year 2000 when the bull market in stocks that began in 1982 came to an abrupt and shocking end. Even still, boomers make up 44 percent of fund-owning households, followed by the Gen Xers, who make up only 24 percent of the total. A big piece of the current mutual fund ownership pie consists of investors who first got involved with funds prior to 1990 (38 percent). Another large chunk of holders (21 percent) first bought mutual funds during the “Irrational Exuberance” Era between 1995 and 1999. Finally, 26 percent of fund investors have come in after the year 2000, and many of these have little or nothing to show for their purchases since stocks have essentially round-tripped during the last decade.

And now, much to the chagrin of the fund complex (and thousands of Boston Red Sox fans, thankfully), this dynasty over the investment business is coming to an end.

The fact that the boomers will be liquidating their equity funds over the next decade as they settle into retirement is lost on no one in the industry. About 58 percent of mutual fund–owning heads of household are between 40 and 64, and the median is tilting further toward 64 with every passing day. Boomers were the perfect buy-and-hold, bread-and-butter investors that mutual funds lived off for the last three decades. Fund families learned how to market to them and what made them tick. And now they are going away.

The first baby boomers were born in 1946 when the war ended and America’s sailors and soldiers came home filled with, well, let’s just say spirit. If you add 65 years to 1946, you arrive at 2011—which means the first boomers have just started to hit retirement age now. Beginning in January 2011, there were 10,000 boomers per day who started turning age 65. This will continue until the year 2030 or when the robots enslave us, whichever comes first (I’m betting robots).

According to statistics supplied before the U.S. House of Representatives by Vanguard’s John Bogle, more than 30 percent of investors in their sixties have greater than 80 percent of their 401(k) invested in equities, most of which is through mutual funds. The fund families will not be able to count on these assets for much longer, as required minimum distributions trigger the redemptions that our ongoing bear market couldn’t. Fixed-income funds will likely hold onto assets better than their equity fund cousins but with low rates. The mass exodus will leave no corner of the fund industry untouched. And while 40 percent of baby boomers surveyed by the AARP recently said they’d be working until they drop, the reality will probably turn out to be somewhat different.

In addition to the aging of their best customers, mutual funds face new competition from the nimbler ETF products that have been seeing stratospheric rates of growth and adoption regardless of market conditions. As more stockbrokers transition to the advisory model, less mutual funds will be sold to investors and more ETFs will be bought on their behalf (we’ll be looking at the rise of the ETF model later on).

The bottom line is that while the total assets under management at mutual fund companies has never been higher, it is unlikely to grow much from current levels ever again. Demographics have a funny and unstoppable way of thwarting the best-laid plans of entire industries at times. This is one of those inevitable scenarios. What it will mean is ever-fiercer competition among the funds themselves. This will manifest itself in lower management fees, consolidation among the providers, a transitioning toward exchange-traded products, and the slow, steady decline of the once mighty product that ruled the American investment landscape for 70 years.

One thing I’ll miss when the mutual funds begin to disappear is the marketing. It’s all so adorable. Open up any financial magazine, and you feel as though you’re walking through a carnival midway. There is fencing, juggling, and even a strong man hefting obscenely heavy objects to the delight of the crowd. There are exotic animals and all manner of outrageous claims being made in front of each tent on the fairgrounds.

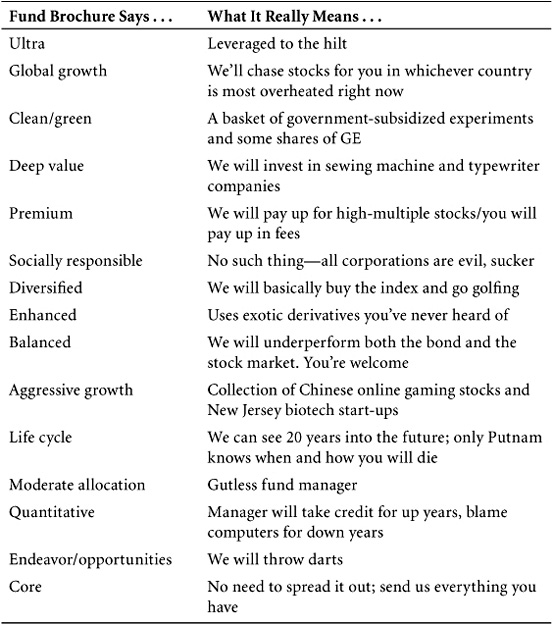

And the names of the funds themselves! “Opportunity” and “Discovery” and “Endeavor”! Are these mutual funds or spaceships? “Our mission is to provide investors with …” A mission? I love missions! There are so many mutual fund types, it can all be disorienting, and so I’ve put together the chart in Table 12.1 to help you parse the various names and what they mean,

Table 12.1

Now you may be saying to yourself, “But Josh, didn’t you say earlier that you do use some mutual funds?” Why yes, yes I did. And while this isn’t a “how to invest” book, there are a few things I’ll mention in this regard.

There are certain styles and strategies that I simply cannot replicate on my own that I want my clients to have exposure to. As an investment advisor representative at a good-sized shop, I am able to purchase I-class (institutional class) mutual funds for my clients which carry the lowest possible internal expenses and have no brokerage fees or commissions associated with them. I suppose in some cases I could bring in an outside separately managed account (SMA) solution, but the fees of these SMAs are not much lower at most asset-level thresholds. And besides, I work with a handful of mutual funds that have done incredibly well in a variety of market environments, and so if the expenses are in line with other solutions, why mess with success?

The short list of mutual funds I tend to use consists of the multiasset-class, global allocation variety. My clients don’t want me trying to pick convertible bonds in Asia for them, nor do they want me making currency decisions between the Brazilian real and the Swiss franc. If I can bring in a powerhouse fund management team to do that and deploy their expertise on behalf of the clients I serve, everybody wins.

But these funds are few and far between. The vast majority of mutual funds are lucky to be alive in my estimation. There are thousands of them that serve no discernible purpose at this point.

We already know that most managers don’t even meet the S&P 500’s return in a given year, and let me assure you that the track records for the limitless number of sector funds are no more impressive versus the funds’ own benchmarks. The reality is that most investors don’t need exposure to one specific sector, and those who truly want it are almost always better off with a passive product like a sector ETF. You want exposure to the gold miners? Just buy the gold miner index. It’s been my experience that most sector-fund managers are merely hugging their sector’s benchmark anyway.

There are some sectors where stock picking is very important, such as biotechnology. Biotech stocks are the ultimate binary bets—total feast or famine. Now you might say to yourself that having a professional fund manager who reads all the clinical papers and talks to the doctors and knows the science would be a good guy to bet on. But no matter how skilled and knowledgeable that manager is, a fund holding 100 different biotech stocks is not going to give you enough exposure to the one or two big winners in the sector; your returns will be diluted by all the also-rans he or she has you invested in.

In general, if there is a trade to be had by being long or short a particular sector, then the ETF is a more efficient way of expressing the trade, certainly not the actively managed sector mutual fund. I predict that these funds will gradually disappear over the next few years.

And I don’t mean to pick on sector funds exclusively; most actively managed foreign stock funds are equally pointless. Don’t think that because a fund family has analysts in-country or “boots on the ground” that it will really matter—it won’t over the long term. If you want overseas exposure, buy the low-cost country-specific fund or some kind of passive, fundamentally weighted index.

Wherever possible with overseas stock funds, I look for an equal-weighted option (as opposed to market cap–weighted). The reason I do this is that many developing countries end up with two or three mega-cap stocks that dominate the averages. A good case in point to illustrate this problem would be Brazil. The most commonly used vehicle for Brazilian exposure is not a mutual fund but a country-specific iShares ETF, ticker symbol EWZ. The problem with this index fund is that most of the holdings are overshadowed by exceedingly large positions in the country’s big commodities exporters, Petro-bras and Vale. Essentially, you end up with a portfolio that is highly levered to the prices of iron ore and oil, not the Brazilian economy. I’ve eschewed the EWZ fund and have opted for BRF, a more evenly distributed index of small- and mid-cap companies that tend to be a better play on the emerging Brazilian middle-class consumer. I see no need to bet on (and pay for) an active manager who may or may not “do a good job.” If I want Brazil, I just buy Brazil, not a picker of Brazilian stocks.

As more investors come around to my way of thinking (and they will), the mutual fund complex will stop churning out actively managed mutual funds and will focus more on market analytics and quantitative methods of stock categorization. This will mean less mutual funds overall and many more ETFs. Costs will go down; so will profits for the investment companies, and some will be bought or die. But the options for both investors and their advisors will get even more specific and specialized. We’ll look at the ETF market in the next chapter.