XIII

There I was, once more broke, which was bad, and dead wrong in my trading, which was a sight worse. I was sick, nervous, upset and unable to reason calmly. That is, I was in the frame of mind in which no speculator should be when he is trading. Everything went wrong with me. Indeed, I began to think that I could not recover my departed sense of proportion. Having grown accustomed to swinging a big line—say, more than a hundred thousand shares of stock—I feared I would not show good judgment trading in a small way. It scarcely seemed worth while being right when all you carried was a hundred shares of stock. After the habit of taking a big profit on a big line I wasn’t sure I would know when to take my profit on a small line. I can’t describe to you how weaponless I felt.

Broke again and incapable of assuming the offensive vigorously. In debt and wrong! After all those long years of successes, tempered by mistakes that really served to pave the way for greater successes, I was now worse off than when I began in the bucket shops. I had learned a great deal about the game of stock speculation, but I had not learned quite so much about the play of human weaknesses. There is no mind so machinelike that you can depend upon it to function with equal efficiency at all times. I now learned that I could not trust myself to remain equally unaffected by men and misfortunes at all times.

Money losses have never worried me in the slightest. But other troubles could and did. I studied my disaster in detail and of course found no difficulty in seeing just where I had been silly. I spotted the exact time and place. A man must know himself thoroughly if he is going to make a good job out of trading in the speculative markets. To know what I was capable of in the line of folly was a long educational step. I sometimes think that no price is too high for a speculator to pay to learn that which will keep him from getting the swelled head. A great many smashes by brilliant men can be traced directly to the swelled head—an expensive disease everywhere to everybody, but particularly in Wall Street to a speculator.

3.1 Chicago had been around for only about 70 years by the time Livermore arrived in the early 1910s. It had been incorporated in 1833 with a population of 350 and boundaries that extended only half a square mile. By 1840, the population had risen to 4,000, but a real influx of trade didn’t arrive until the Illinois & Michigan Canal opened in 1848 to permit shipping from the Great Lakes through Chicago to the Mississippi River and beyond to the Gulf of Mexico.

Soon after that the first railroad arrived—and by the 1860s the city was the ninth most populous city in the nation and the main transportation hub of the region then known as the Northwest, connecting grains and mills of the Great Plains to the cities of the eastern seaboard. In the first year of the decade, the Republican National Convention took place in the city and nominated for president a fiery orator, attorney, and state politician named Abraham Lincoln.

Modern Chicago grew out of a tragedy: In 1871, a massive fire leveled the city, destroying nearly 20,000 wooden buildings and leaving a third of the 300,000 residents homeless. Because the lakeside ground was too unstable to rebuild on with masonry, architects innovated with steel and invented the skyscraper. A building boom emerged that created a dense, modern city with innovative architecture on par with New York, and the first underground sewage system. By 1900, the city had grown at an astonishing rate to house 1.7 million people, including tens of thousands of European immigrants and migrants from the southern United States.

The city grew to dominate the livestock and grain trades, which is what attracted commodity traders like Livermore; the beautiful art deco style Chicago Board of Trade Building opened in 1930, and was the city’s tallest building until 1965. The CBOT merged with the Chicago Mercantile Exchange in 2007 and the New York Mercantile Exchange in 2008, becoming the commod ity and fi nancial futures powerhouse known now as the CME Group.

I was not happy in New York, feeling the way I did. I didn’t want to trade, because I wasn’t in good trading trim. I decided to go away and seek a stake elsewhere. The change of scene could help me to find myself again, I thought. So once more I left New York, beaten by the game of speculation. I was worse than broke, since I owed over one hundred thousand I dollars spread among various brokers.

I went to Chicago and there found a stake. 13.1 It was not a very substantial stake, but that merely meant that I would need a little more time to win back my fortune. A house that I once had done business with had faith in my ability as a trader and they were willing to prove it by allowing me to trade in their office in a small way.

I began very conservatively. I don’t know how I might have fared had I stayed there. But one of the most remarkable experiences in my career cut short my stay in Chicago. It is an almost incredible story.

One day I got a telegram from Lucius Tucker. I had known him when he was the office manager of a Stock Exchange firm that I had at times given some business to, but I had lost track of him. The telegram read:

Come to New York at once. L. TUCKER.

I knew that he knew from mutual friends how I was fixed and therefore it was certain he had something up his sleeve. At the same time I had no money to throw away on an unnecessary trip to New York; so instead of doing what he asked me to do I got him on the long distance.

“I got your telegram,” I said. “What does it mean?”

“It means that a big banker in New York wants to see you,” he answered.

“Who is it?” I asked. I couldn’t imagine who it could be.

“I’ll tell you when you get to New York. No use otherwise.”

“You say he wants to see me?”

“He does.”

“What about?”

“He’ll tell you that in person if you give him a chance,” said Lucius.

“Can’t you write me?”

“No.”

“Then tell me more plainly,” I said.

“I don’t want to.”

“Look here, Lucius,” I said, “just tell me this much: Is this a fool trip?”

“Certainly not. It will be to your advantage to come.”

“Can’t you give me an inkling?”

“No,” he said. “It wouldn’t be fair to him. And besides, I don’t know just how much he wants to do for you. But take my advice: Come, and come quick.”

“Are you sure it is I that he wishes to see?”

“Nobody else but you will do. Better come, I tell you. Telegraph me what train you take and I’ll meet you at the station.”

“Very well,” I said, and hung up.

I didn’t like quite so much mystery, but I knew that Lucius was friendly and that he must have a good reason for talking the way he did. I wasn’t faring so sumptuously in Chicago that it would break my heart to leave it. At the rate I was trading it would be a long time before I could get together enough money to operate on the old scale.

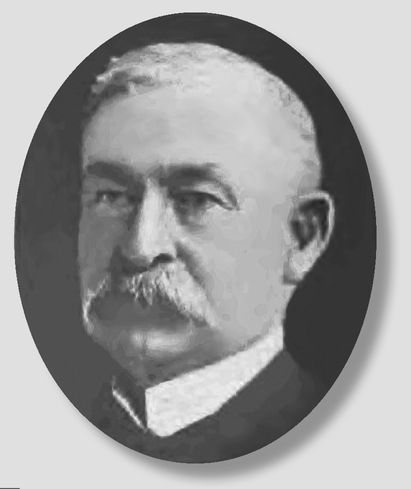

3.2This appears to be a pseudonym for

Charles E. Pugh, who died in 1914 after a long career in railroads.

1 Pugh was born in 1841 and got his start in the railroad business in 1859 as a station agent for the Pennsylvania Railroad. He climbed the ranks, with successive turns as passenger conductor, train dispatcher, and general agent before becoming president of the Baltimore, Chesapeake & Atlantic Railway and vice president of the Pennsylvania system. Pugh was also on the board of various banking and insurance institutions, including the Manor Real Estate and Trust Co., Centennial National Bank, Mutual Fire, and the Marina and Inland Insurance Co.

2

I came back to New York, not knowing what would happen. Indeed, more than once during the trip I feared nothing at all would happen and that I’d be out my railroad fare and my time. I could not guess that I was about to have the most curious experience of my entire life.

Lucius met me at the station and did not waste any time in telling me that he had sent for me at the urgent request of Mr. Daniel Williamson, of the well-known Stock Exchange house of Williamson & Brown. Mr. Williamson told Lucius to tell me that he had a business proposition to make to me that he was sure I would accept since it would be very profitable for me. Lucius swore he didn’t know what the proposition was. The character of the firm was a guaranty that nothing improper would be demanded of me.

Dan Williamson was the senior member of the firm, which was founded by Egbert Williamson way back in the ’70’s. There was no Brown and hadn’t been one in the firm for years. The house had been very prominent in Dan’s father’s time and Dan had inherited a considerable fortune and didn’t go after much outside business. They had one customer who was worth a hundred average customers and that was Alvin Marquand, 13.2 Williamson’s brother-in-law, who in addition to being a director in a dozen banks and trust companies was the president of the great Chesapeake and Atlantic Railroad system. He was the most picturesque personality in the railroad world after James J. Hill, and was the spokesman and dominant member of the powerful banking coterie known as the Fort Dawson gang. 3.3 He was worth from fifty million to five hundred million dollars, the estimate depending upon the state of the speaker’s liver. When he died they found out that he was worth two hundred and fifty million dollars, all made in Wall Street. So you see he was some customer.

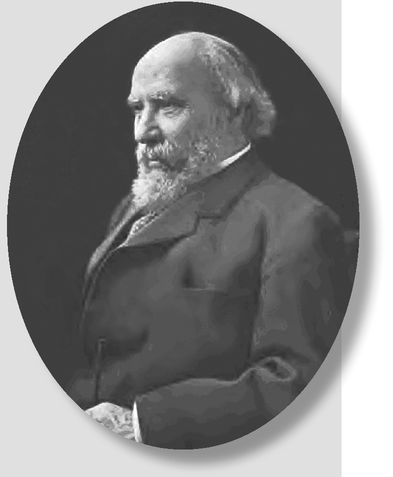

3.3 James Hill, nicknamed the “Empire Builder” by the media, was an ally of J. P. Morgan and a rival of E. H. Harriman and the Standard Oil crowd in the infamous Northern Pacific corner of 1901.

3 Born in 1836 in a village outside of Toronto, Canada, Hill immigrated to Minnesota in 1856 after his father died and ultimately built a $75 million fortune. His decision to leave home is the stuff of legend:

According to the story, a way-worn traveler stopped at the Hill farm for dinner, leaving his horse tied at the gate. The boy saw that the animal was tired and carried it a pail of water. The stranger was pleased at his thoughtfulness, and as he rode off tossed him a newspaper from the United States and called out gravely, “Go there young man. That country needs youngsters of your spirit.”

4

After studying the paper carefully and finding it rich with stories of opportunities and success, Hill decided to investigate. He traveled to St. Paul, which was then a frontier town of 5,000. Hill got a job as a stevedore and clerk with a local river transportation company. By 1865, after studying the fi ner points of his business and realizing the great potential to service the unsettled Northwest interior, Hill became an agent of the Northwest Packet Co. before becoming a representative of the St. Paul and Pacific Railroad. In 1869, he started his own transportation and fuel firm, notable for being the first to bring coal to the St. Paul area.

This was period of intense growth for the railroad industry. The promise of a new technology encouraged overinvestment not unlike the Internet technology bubble of the late 1990s. At the time, St. Paul was having its first experience with railroads. It was unsuccessful, with 100 miles of track built “into space which were said to begin and end nowhere,”

5 according to one account. After the venture went bankrupt for debts of $30 million and “a few streaks of rust and a right of way” as its only assets, Hill swooped in and acquired the property in 1878 for $100,000.

6 So was born the railroad that would eventually become the Great Northern.

Within five years, Hill was elected president of the Great Northern and immediately began work to fulfill his dream of building a transportation network that reached over the Pacific Ocean to Asia via steamships. It was this ambition that put him in league with Morgan and resulted in the confrontation with E.H. Harriman that ended in the May 1901 panic. At that time, he was described as “[s]omewhat below the average height but built like a buffalo, with a prodigious chest and neck and head; his arms long, sinewy, powerful; his feet large and firm planted and his legs as solid as steel columns—truly a massive, imposing figure of a man.”

7In April 1907, Hill retired as president of the Great Northern, then resigned from the board of directors five years later. In the interim he wrote a book, Highways of Progress. In it, besides discussing the importance of resource conservation and railroad operations, he notes the importance of global trade to American farmers and businessmen: “Chinese and Japanese could be made customers for our flour in increasing quantity. A people once accustomed to wheat are slow to give it up. And the dense population would make consumption large.”

8 Hill died in 1916 at the age of 77 at home in St. Paul.

Lucius told me he had just accepted a position with Williamson & Brown—one that was made for him. He was supposed to be a sort of circulating general business getter. The firm was after a general commission business and Lucius had induced Mr. Williamson to open a couple of branch offices, one in one of the big hotels uptown and the other in Chicago. I rather gathered that I was going to be offered a position in the latter place, possibly as office manager, which was something I would not accept. I didn’t jump on Lucius because I thought I’d better wait until the offer was made before I refused it.

13.4President of the National City Bank, precursor to today’s Citigroup, James Stillman was a close friend of both E. H. Harriman and J. P. Morgan, had ties to William Rockefeller and the Standard Oil crowd, and played a role in the Northern Pacific corner of 1901, the Panic of 1907, and the public offering of Amalgamated Copper securities. In fact, Stillman’s two daughters married two of William Rockefeller’s sons.

9

Stillman was a small, dark man who dressed immaculately and was described by a contemporary as “a perfect example of the well-built man of the world, sartorially correct, soft spoken, with a tendency toward cynical humor, and with tongue capable of devastating sarcasms.”

10Stillman was born in 1850 in Brownsville, Texas. His father, Charles Stillman, a native of Connecticut, built a business empire stretching from New York to Texas and Mexico. His businesses included silver and lead mines, real estate, a cotton brokerage, shipping, textile factories, and retail outlets. During the Civil War, Charles helped smuggle Confederate cotton south to his cotton mills in Monterrey and north to the Cotton Exchange in Manhattan.

11At 18, Stillman got his start as a clerk at the cotton merchant house of Smith, Woodward & Stillman in New York. Within two years, he became a full partner and the firm was reincorporated as Woodward & Stillman. Relationships between his firm and National City Bank brought Stillman in close contact with bank president Moses Taylor. Eventually, he was made a bank director and in 1891 succeeded Taylor as president.

12 These were tumultuous years, according to a biographer:

The world was ripe for a fall. The Baring panic, the crisis of 1893, the free-silver collapse, lay just beyond the hill where man’s eyes could not see them. By chance, Mr. Stillman took the presidency. The storm broke. He showed himself the master mariner, quiet,

skilful, courageous, cold as an iceberg in panic, intuitive as a woman in the hour of action. And so he came to his inheritance.

13 Livermore mentions Stillman’s ability to embrace silence. Reporters of the day called Stillman “the coldest proposition in America.”

14 Historian Maury Klein said that few “rivaled the glacial façade of Stillman. Laughter came to his lips with the frequency of leap years. He was an iceberg whose smooth, pleasant features revealed absolutely nothing of the dark complexities swimming beneath their surface.”

15Accomplished Wall Street operator and statesman Bernard Baruch, who was also a friend of Livermore’s, told a story about Stillman returning from a trip to Europe and running into George Perkins, a J. P. Morgan partner. “I see you’re back,” Perkins remarked. When Stillman merely stared, Perkins quipped, “Oh you need not confi rm it.”

16 At home he required his family to sit silently through two-hour formal dinners.

17Stillman retired from his post as president of National City Bank in 1908. Soon after, he reportedly tried to convince E. H. Harriman, J. P. Morgan, and William Rockefeller that all four should retire for the good of the country. The idea was to put an end to the government’s campaign against the “Money Trusts” and quell the public’s apprehension about the great concentration of wealth and power controlled by these four men. Soon Stillman got his wish. Harriman died a year later. Morgan paid less and less attention to business affairs and became better known as an art collector and traveler. Rockefeller suffered from ill health and was forced to retire. Stillman died in the spring of 1918.

18

Lucius took me into Mr. Williamson’s private office, introduced me to his chief and left the room in a hurry, as though he wished to avoid being called as witness in a case in which he knew both parties. I prepared to listen and then to say no.

Mr. Williamson was very pleasant. He was a thorough gentleman, with polished manners and a kindly smile. I could see that he made friends easily and kept them. Why not? He was healthy and therefore good-humored. He had slathers of money and therefore could not be suspected of sordid motives. These things, together with his education and social training, made it easy for him to be not only polite but friendly, and not only friendly but helpful.

I said nothing. I had nothing to say and, besides, I always let the other man have his say in full before I do any talking. Somebody told me that the late James Stillman, 3.4 president of the National City Bank 13.5—who, by the way, was an intimate friend of Williamson’s—made it his practice to listen in silence, with an impassive face, to anybody who brought a proposition to him. After the man got through Mr. Stillman continued to look at him, as though the man had not finished. So the man, feeling urged to say something more, did so. Simply by looking and listening Stillman often made the man offer terms much more advantageous to the bank than he had meant to offer when he began to speak.

I don’t keep silent just to induce people to offer a better bargain, but because I like to know all the facts of the case. By letting a man have his say in full you are able to decide at once. It is a great time-saver. It averts debates and prolonged discussions that get nowhere. Nearly every business proposition that is brought to me can be settled, as far as my participation in it is concerned, by my saying yes or no. But I cannot say yes or no right off unless I have the complete proposition before me.

Dan Williamson did the talking and I did the listening. He told me he had heard a great deal about my operations in the stock market and how he regretted that I had gone outside of my bailiwick and come a cropper in cotton. Still it was to my bad luck that he owed the pleasure of that interview with me. He thought my forte was the stock market, that I was born for it and that I should not stray from it.

3.5 National City Bank, or City Bank as it was popularly called, was chartered in 1812 by the New York Legislature and reorganized as a national bank in 1865. Moses Taylor held the offi ce of president for 34 years, until his death. The original capitalization of $1 million rose to $25 million by 1904.

19

When James Stillman took the reins of City Bank, he pushed the firm into investment banking, then the fastest-growing and most profitable area of finance.

20 Although Morgan dominated the business of security underwriting and marketing, Stillman was able to secure a foothold by teaming with Jacob Schiff of Kuhn, Loeb. One of their first efforts together was to help E. H. Harriman reorganize Union Pacific Railroad in 1895.

Soon Stillman focused on building City Bank into an institution that could provide any service that the new large corporations needed. He also notably expanded the bank’s reach into foreign markets, especially South America, with branches in Rio de Janeiro and Buenos Aires. In 1907, Stillman wrote to his associate:

I firmly believe…that the most successful banks will be the ones that can do something else than the mere receiving and loaning of money. That does not require a very high order of ability, but devising methods of serving people and [of] attracting business without resorting to unconservative or unprofitable methods, that opens limited fields for study, ability and resourcefulness and

few only will be found to do it.

21In 1955, National City Bank merged with the First National Bank of New York to form Citibank. After merging with Travelers Insurance in 1998, Citigroup was formed. Before nearly collapsing in the credit crisis of 2007-2009, Citigroup was America’s largest financial institution for decades.

“And that is the reason, Mr. Livingston,” he concluded pleasantly, “why we wish to do business with you.”

“Do business how?” I asked him.

“Be your brokers,” he said. “My firm would like to do your stock business.”

“I’d like to give it to you,” I said, “but I can’t.”

“Why not?” he asked.

“I haven’t any money,” I answered.

“That part is all right,” he said with a friendly smile. “I’ll furnish it.” He took out a pocket check book, wrote out a check for twenty-five thousand dollars to my order, and gave it to me.

“What’s this for?” I asked.

“For you to deposit in your own bank. You will draw your own checks. I want you to do your trading in our office. I don’t care whether you win or lose. If that money goes I will give you another personal check. So you don’t have to be so very careful with this one. See?”

I knew that the firm was too rich and prosperous to need anybody’s business, much less to give a fellow the money to put up as margin. And then he was so nice about it! Instead of giving me a credit with the house he gave me the actual cash, so that he alone knew where it came from, the only string being that if I traded I should do so through his firm. And then the promise that there would be more if that went! Still, there must be a reason.

“What’s the idea?” I asked him.

“The idea is simply that we want to have a customer in this office who is known as a big active trader. Everybody knows that you swing a big line on the short side, which is what I particularly like about you. You are known as a plunger.”

“I still don’t get it,” I said.

“I’ll be frank with you, Mr. Livingston. We have two or three very wealthy customers who buy and sell stocks in a big way. I don’t want the Street to suspect them of selling long stock every time we sell ten or twenty thousand shares of any stock. If the Street knows that you are trading in our office it will not know whether it is your short selling or the other customers’ long stock that is coming on the market.”

I understood at once. He wanted to cover up his brother-in-law’s operations with my reputation as a plunger! It so happened that I had made my biggest killing on the bear side a year and a half before, and, of course, the Street gossips and the stupid rumor mongers had acquired the habit of blaming me for every decline in prices. To this day when the market is very weak they say I am raiding it. 13.6

I didn’t have to reflect. I saw at a glance that Dan Williamson was offering me a chance to come back and come back quickly. I took the check, banked it, opened an account with his firm and began trading. It was a good active market, broad enough for a man not to have to stick to one or two specialties. I had begun to fear, as I told you, that I had lost the knack of hitting it right. But it seems I hadn’t. In three weeks’ time I had made a profit of one hundred and twelve thousand dollars out of the twenty-five thousand that Dan Williamson lent me.

I went to him and said, “I’ve come to pay you back that twenty-five thousand dollars.”

“No, no!” he said and waved me away exactly as if I had offered him a castor-oil cocktail. “No, no, my boy. Wait until your account amounts to something. Don’t think about it yet. You’ve only got chicken feed there.”

There is where I made the mistake that I have regretted more than any other I ever made in my Wall Street career. It was responsible for long and dreary years of suffering. I should have insisted on his taking the money. I was on my way to a bigger fortune than I had lost and walking pretty fast. For three weeks my average profit was 150 per cent per week. From then on my trading would be on a steadily increasing scale. But instead of freeing my self from all obligation I let him have his way and did not compel him to accept the twenty-five thousand dollars. Of course, since he didn’t draw out the twenty-five thousand dollars he had advanced me I felt I could not very well draw out my profit. I was very grateful to him, but I am so constituted that I don’t like to owe money or favours. I can pay the money back with money, but the favours and kindnesses I must pay back in kind—and you are apt to find these moral obligations mighty high priced at times. Moreover there is no statute of limitations.

3.6 The problem of Livermore being identified with every market swoon became so extreme that in 1929 he was forced to hire a bodyguard. A former policeman, Frank Gorman, stayed in Livermore’s mansion after several anony mous death threats were made against the speculator.

22

There was a lot of property to protect in years when he wasn’t flat broke. Patricia Livermore, the trader’s daughter-in-law, gave a rundown of the family’s lifestyle in a 1990 documentary about the 1929 crash. She said in part:

23”[The Livermores] lived in utter splendor, typical of the ‘20s when society was showy and wealth was displayed. They had a beautiful place on 76th Street in Manhattan on the West Side, off Central Park.… They had a house in Great Neck. They had a summer house in Lake Placid. They had a house in Palm Beach. They had a private railroad car, two yachts.

The only yacht that was bigger was J. P. Morgan’s. And they used one of them, the big one, very frequently when they went to Europe. They lived very comfortably….

“Jesse Livermore had a ticker tape in every home that he owned, on his railway cars, on his yachts....They had several Rolls Royces, lots of chauffeurs. They had a staff of about 20 or 25 and in each place, in each house, see, and with the exception of [his wife‘s] personal maid, they did not take their staffs with them. They simply kept them year-round in all their establishments.…Oh, they lived. They really lived. Mrs. Livermore was a spender. And, of course, she loved to buy. She spent her days buying and buying and buying.”

3.7Known formally as the Baltimore, Chesapeake and Atlantic Railroad, the company was the result of an 1868 merger between the Virginia Central and the Covington & Ohio systems. In 1899, the Pennsylvania Railroad purchased a majority interest in the company.

24 The railroad operated from the Atlantic shores of Virginia and over the Appalachian Mountains into Illinois, Michigan, and Canada. Eventually, the line joined with a number of smaller railroads to form today’s CSX Transportation.

25 I left the money undisturbed and resumed my trading. I was getting on very nicely. I was recovering my poise and I was sure it would not be very long before I should get back into my 1907 stride. Once I did that, all I’d ask for would be for the market to hold out a little while and I’d more than make up my losses. But making or not making the money was not bothering me much. What made me happy was that I was losing the habit of being wrong, of not being myself. It had played havoc with me for months but I had learned my lesson.

Just about that time I turned bear and I began to sell short several railroad stocks. Among them was Chesapeake & Atlantic. 3.7 I think I put out a short line in it; about eight thousand shares.

One morning when I got downtown Dan Williamson called me into his private office before the market opened and said to me: “Larry, don’t do anything in Chesapeake & Atlantic just now. That was a bad play of yours, selling eight thousand short. I covered it for you this morning in London and went long.”

I was sure Chesapeake & Atlantic was going down. The tape told it to me quite plainly; and besides I was bearish on the whole market, not violently or insanely bearish, but enough to feel comfortable with a moderate short line out. I said to Williamson, “What did you do that for? I am bearish on the whole market and they are all going lower.”

But he just shook his head and said, “I did it because I happen to know something about Chesapeake & Atlantic that you couldn’t know. My advice to you is not to sell that stock short until I tell you it is safe to do so.”

What could I do? That wasn’t an asinine tip. It was advice that came from the brother-in-law of the chairman of the board of directors. Dan was not only Alvin Marquand’s closest friend but he had been kind and generous to me. He had shown his faith in me and confidence in my word. I couldn’t do less than to thank him. And so my feelings again won over my judgment and I gave in. To subordinate my judgment to his desires was the undoing of me. Gratitude is something a decent man can’t help feeling, but it is for a fellow to keep it from completely tying him up. The first thing I knew I not only had lost all my profit but I owed the firm one hundred and fifty thousand dollars besides. I felt pretty badly about it, but Dan told me not to worry.

“I’ll get you out of this hole,” he promised. “I know I will. But I can only do it if you let me. You will have to stop doing business on your own hook. I can’t be working for you and then have you completely undo all my work in your behalf. Just you lay off the market and give me a chance to make some money for you. Won’t you, Larry?”

Again I ask you: What could I do? I thought of his kindliness and I could not do anything that might be construed as lacking in appreciation. I had grown to like him. He was very pleasant and friendly. I remember that all I got from him was encouragement. He kept on assuring me that everything would come out O.K. One day, perhaps six months later, he came to me with a pleased smile and gave me some credit slips.

“I told you I would pull you out of that hole,” he said, “and I have.” And then I discovered that not only had he wiped out the debt entirely but I had a small credit balance besides.

3.8Livermore is likely referring to the Atlantic Coast Line Railroad that operated from New York City down along the Atlantic seaboard to Tampa, Florida. It was formed through combination of smaller lines in 1869 by William Walters, a produce merchant from Baltimore. In addition to transporting vacationers to the tropical waters of the Gulf of Mexico, the Southern Atlantic moved fresh fruit and vegetables in refrigerator cars to northern cities. In the late 1950s, the railroad merged with its old rival, the Seaboard Coast Line, before becoming part of CSX.

26 I think I could have run that up without much trouble, for the market was right, but he said to me, “I have bought you ten thousand shares of Southern Atlantic.” 3.8 That was another road controlled by his brother-in-law, Alvin Marquand, who also ruled the market destinies of the stock.

When a man does for you what Dan Williamson did for me you can’t say anything but “Thank you”—no matter what your market views may be. You may be sure you’re right, but as Pat Hearne used to say: “You can’t tell till you bet!” and Dan Williamson had bet for me—with his money.

Well, Southern Atlantic went down and stayed down and I lost, I forget how much, on my ten thousand shares before Dan sold me out. I owed him more than ever. But you never saw a nicer or less importunate creditor in your life. Never a whimper from him. Instead, encouraging words and admonitions not to worry about it. In the end the loss was made up for me in the same generous but mysterious way.

He gave no details whatever. They were all numbered accounts. Dan Williamson would just say to me, “We made up your Southern Atlantic loss with profits on this other deal,” and he’d tell me how he had sold seventy-five hundred shares of some other stock and made a nice thing out of it. I can truthfully say that I never knew a blessed thing about those trades of mine until I was told that the indebtedness was wiped out.

After that happened several times I began to think, and I got to look at my case from a different angle. Finally I tumbled. It was plain that I had been used by Dan Williamson. It made me angry to think it, but still angrier that I had not tumbled to it quicker. As soon as I had gone over the whole thing in my mind I went to Dan Williamson, told him I was through with the firm, and I quit the office of Williamson & Brown. I had no words with him or any of his partners. What good would that have done me? But I will admit that I was sore—at myself quite as much as at Williamson & Brown.

The loss of the money didn’t bother me. Whenever I have lost money in the stock market I have always considered that I have learned something; that if I have lost money I have gained experience, so that the money really went for a tuition fee. A man has to have experience and he has to pay for it. But there was something that hurt a whole lot in that experience of mine in Dan Williamson’s office, and that was the loss of a great opportunity. The money a man loses is nothing; he can make it up. But opportunities such as I had then do not come every day.

The market, you see, had been a fine trading market. I was right; I mean, I was reading it accurately. The opportunity to make millions was there. But I allowed my gratitude to interfere with my play. I tied my own hands. I had to do what Dan Williamson in his kindness wished done. Altogether it was more unsatisfactory than doing business with a relative. Bad business!

And that wasn’t the worst thing about it. It was that after that there was practically no opportunity for me to make big money. The market flattened out. Things drifted from bad to worse. I not only lost all I had but got into debt again—more heavily than ever. Those were long lean years, 1911, 1912, 1913 and 1914. 3.6 There was no money to be made. The opportunity simply wasn’t there and so I was worse off than ever.

It isn’t uncomfortable to lose when the loss is not accompanied by a poignant vision of what might have been. That was precisely what I could not keep my mind from dwelling on, and of course it unsettled me further. I learned that the weaknesses to which a speculator is prone are almost numberless. It was proper for me as a man to act the way I did in Dan Williamson’s office, but it was improper and unwise for me as a speculator to allow myself to be influenced by any consideration to act against my own judgment. Noblesse oblige—but not in the stock market, because the tape is not chivalrous and moreover does not reward loyalty. I realise that I couldn’t have acted differently. I couldn’t make myself over just because I wished to trade in the stock market. But business is business always, and my business as a speculator is to back my own judgment always.

13.9 After the excitement of the preceding decade, the years running up to the beginning of World War I were rather dull. It was a period marked by investigations and regulations in the aftermath of the Panic of 1907 and the populism of the administration of Theodore Roosevelt. In 1911, the Supreme Court ordered both Standard Oil and American Tobacco dissolved. The Dow Jones Industrials added less than 1% for the year to close at 81.68. The Dow Jones Transportation Average added 2.4% to close at 116.83.

The year 1912 brought the sinking of the Titanic, a panic on the Paris Bourse, the country’s first minimum wage statute, and the Pujo Anti-Trust Committee. The Dow Industrials gained 7.6% while the Dow Transports were essentially unchanged. In 1913, the New York Stock Exchange waged war against stock manipulation and excessive margins, federal income taxes began, and the Federal Reserve System was established. The Dow Industrials lost 10.3% while the Dow Transports fell 11.2%.

Unfortunately, 1914 continued the downward trend. World War I broke out after Archduke Franz Ferdinand was assassinated in Austria. On July 31, the war in Europe prompted the NYSE to close for four months: the first time it had closed at all since 1873. The Curb Market also closed. Wall Street feared that a liquidation of European accounts, which were valued at $2.4 billion, would cause a panic. Over the summer, the situation in Europe deteriorated as Germany declared war on France and Russia before attacking Belgium. England reciprocated by declaring war on Germany.

On December 1, the San Francisco Stock and Bond Exchange became the first exchange to reopen. On December 12, trading resumed with restrictions on the NYSE. The Dow Industrials fell 30.7% to a level not seen since just after the Panic of 1907—erasing seven years of growth. The Dow Transports fell 17.2%.

27It was a very curious experience. I’ll tell you what I think happened. Dan Williamson was perfectly sincere in what he told me when he first saw me. Every time his firm did a few thousand shares in any one stock the Street jumped at the conclusion that Alvin Marquand was buying or selling. He was the big trader of the office, to be sure, and he gave this firm all his business; and he was one of the best and biggest traders they have ever had in Wall Street. Well, I was to be used as a smoke screen, particularly for Marquand’s selling.

Alvin Marquand fell sick shortly after I went in. His ailment was early diagnosed as incurable, and Dan Williamson of course knew it long before Marquand himself did. That is why Dan covered my Chesapeake & Atlantic stock. He had begun to liquidate some of his brother-in-law’s speculative holdings of that and other stocks.

Of course when Marquand died the estate had to liquidate his speculative and semispeculative lines, and by that time we had run into a bear market. By tying me up the way he did, Dan was helping the estate a whole lot. I do not speak boastfully when I say that I was a very heavy trader and that I was dead right in my views on the stock market. I know that Williamson remembered my successful operations in the bear market of 1907 and he couldn’t afford to run the risk of having me at large. Why, if I had kept on the way I was going I’d have made so much money that by the time he was trying to liquidate part of Alvin Marquand’s estate I would have been trading in hundreds of thousands of shares. As an active bear I would have done damage running into the millions of dollars to the Marquand heirs, for Alvin left only a little over a couple of hundred millions.

It was much cheaper for them to let me get into debt and then to pay off the debt than to have me in some other office operating actively on the bear side. That is precisely what I would have been doing but for my feeling that I must not be outdone in decency by Dan Williamson. 13.10

I have always considered this the most interesting and most unfortunate of all my experiences as a stock operator. As a lesson it cost me a disproportionately high price. It put off the time of my recovery several years. I was young enough to wait with patience for the strayed millions to come back. But five years is a long time for a man to be poor. Young or old, it is not to be relished. I could do without the yachts a great deal easier than I could without a market to come back on. The greatest opportunity of a lifetime was holding before my very nose the purse I had lost. I could not put out my hand and reach for it. A very shrewd boy, that Dan Williamson; as slick as they make them; farsighted, ingenious, daring. He is a thinker, has imagination, detects the vulnerable spot in any man and can plan cold-bloodedly to hit it. He did his own sizing up and soon doped out just what to do to me in order to reduce me to complete inoffensiveness in the market. He did not actually do me out of any money. On the contrary, he was to all appearances extremely nice about it. He loved his sister, Mrs. Marquand, and he did his duty toward her as he saw it.

13.10 There is no historical record of Williamson or his firm, so it is likely that this was another pseudonym to cover the identity of an individual who Livermore did not wish to openly name. Pugh retired in 1911, which coincides roughly with the timeline given here. It makes sense that Williamson, whoever he was, wanted to rein in Livermore’s bear operations to maximize the value of Pugh’s estate—especially in a trendless market.

28

ENDNOTES

1 “Obituary,”

Railway World (1913), 388.

2 John William Leonard,

Who’s Who in Finance, Banking, and Insurance (1911), 859.

3 “J.J. Hill Dead,”

New York Times, May 30, 1916, 1.

8 James Jerome Hill,

Highways of Progress (1910), 160.

9 Henry Morgenthau,

All in a Life-Time (1922), 77.

10 Maury Klein,

The Life & Legend of E.H. Harriman, 163

12 Mitchell Charles Harriman,

Prominent and Progressive Americans (1902), 321-323.

13 C. M. Keys, “The Money-Kings,”

The World’s Work: A History of Our Time (1907), 9520.

14 Maury Klein,

The Life & Legend of E.H. Harriman (2000), 163.

16 Bernard Baruch,

My Own Story (1957), 261.

17 Celia McGee, “A Wasp’s Buzz,”

New York, August 1, 1994, 38.

18 “James Stillman, Head of City Bank, Dies Suddenly,”

New York Times, March 16, 1918, 1.

19 Thomas William Lawson,

Frenzied Finance (1906), 52-53.

20 Klein,

The Life & Legend of E.H. Harriman, 165.

21 Robert F. Bruner and Sean D. Carr,

The Panic of 1907 (Hoboken, NJ: John Wiley & Sons, 2007), 186.

22 “Livermore Has Bodyguard.”

New York Times. December 21, 1929. 5.

23 “The American Experience: The Crash of 1929,” WGBH. 1990

24 “News of the Railroads,”

New York Times, September 5, 1899, 4.

25 John F. Stover and Mark Christopher Carnes,

The Routledge Historical Atlas of American Railroads (1999), 82-83.

27 Peter Wyckoff,

Wall Street and the Stock Markets (1972), 50-54.

28 “Pugh Leaves Pennsylvania,”

New York Times, February 25, 1911, 8.