15 STORMS, CRISIS, AND NEAR DEATH, 1985–1993

The expansion of IBM’s worldwide business took many forms in 1980. Among the most visible were the 8 million square feet of plant and laboratory space under construction in eight countries at the end of the year.

—IBM ANNUAL REPORT, 19801

BEHIND IBM’S DOMINANCE of the mainframe business, its annual rankings by business magazines as the most admired corporation, and the whimsical ads of the “Little Tramp” and IBM’s PCs hid a story of corporate failure of gigantic proportions. Beginning in the late 1980s and extending over two decades, IBM dismissed or retired some 200,000 employees, more than half of whom were located in the United States. A generation of executives and middle managers left, too, including John Akers, the first chairman to be terminated in IBM’s history. The tsunami of layoffs and retirements proved so massive that an employee walking through almost any IBM office in North America saw entire floors of empty cubicles and offices, an old IBM telephone directory tossed on the floor, an IBM coffee mug perched on a window sill, or perhaps a half dozen IBMers working in a space that used to hold over 100 colleagues. At least there was more than enough parking. It did not matter whether the location was a sales office, factory, divisional headquarters, or laboratory. IBMers gauged the extent of the layoffs by the number of cars parked out front. Ironically, most of these empty buildings were relatively new. A construction boom at IBM during the 1970s and 1980s added skyscrapers in such cities as Paris, Chicago, New York, Minneapolis, and Detroit, and new factories on both sides of the Atlantic and in Asia. It seemed executives needed their own tower, especially sales executives.

Inside IBM, rumors and grumbling increased sharply in the early 1990s, while it was not uncommon for employees to devote an hour or more each day to spreading those rumors, gossiping and grousing about potential layoffs. They asked when the board of directors was going to act, what group would be laid off next, whose “dumb” idea it was to break up the company, and whatever happened to the Basic Beliefs. Wall Street analysts were fuming: “What was happening to IBM’s profits and revenues?” “Why aren’t more employees being laid off?” “Why is the stock dropping in value?”2 Customers were complaining of too many IBM proposals conflicting with each other, deteriorating service, inability to get things done with IBM, and prices that were too high. Nobody was happy; something had to be done.

Increasingly, everyone wanted to blame one person: John Akers. In the New York area, rumors had it that Frank Cary and John R. Opel, both still on IBM’s board, were not pleased with his performance; Tom Watson Jr. reportedly wished he were still running the company. Even Akers barked at staff. Exactly one year before his departure, he yelled frustratingly at a room full of managers in a training class, asking them, “What [have you] done for the company recently?” One of those managers took notes and spread the news of Akers’s outburst around the company through e-mail. Never had an e-mail traveled so far so fast or been read by so many so quickly.

Yet the board kept issuing public assurances that things were under control and that it had full confidence in Akers’s leadership, until IBM announced on January 26, 1993, that he would “retire” on April 1, a full year early. Akers appeared on the internal IBM TV station and in press photos standing next to board member James E. Burke (1925–2012), who led the cabal pushing him out, as he announced the change of command. Burke said the board would now start a 90-day hunt for a new CEO, including looking outside of IBM. Watching the proceedings of Akers’s retirement and later the introduction of his replacement, Louis V. Gerstner Jr., on IBM’s internal TV network was surreal. Most of the North American IBM population clustered around these TVs. The majority believed Akers had been fired for good cause.

Figure 15.1

John F. Akers was the first CEO at IBM to be dismissed by the company for poor performance. He was IBM’s chairman of the board from 1986 to 1993 and CEO from 1985 to 1993. Photo courtesy of IBM Corporate Archives.

Akers, too, was upset long before he was forced out. In that April 1992 managers’ class, he burst out that he was “goddam mad” with how IBM was losing market share for various products. He criticized the assembled managers for not trying harder, saying, “The tension level is not high enough” and that IBMers “can’t change fast enough.”3 Periodically, internal e-mails with similar messages attributed to him leaked out, irritating and frustrating employees, but by then it seemed “everyone” knew the company was failing. Akers complained about the decline in IBM stock’s value. Observant employees, customers, and industry watchers were in denial or remained confident that Akers would fix the problems. He said he would do so in every annual report during his last five years at IBM.

When IBM’s profits started falling by billions of dollars beginning in 1990 and then it started posting losses in 1991, everyone seemed shocked, stunned that the great IBM was really in trouble. This company was the great American multinational. Writers at The Economist reported that “IBM was always more the model of an all-conquering American multinational than such other heavyweights as General Motors or Proctor & Gamble. It pervaded every market it was allowed to enter; it was more widely visible, more scrutinized, more admired.… IBM was the best.”4 Another observer pointed out that “IBM unquestionably created a strikingly vigorous and usually profitable industry.”5

What happened at IBM cannot be fully understood as being just about declining costs of mainframe technologies, new entrants into the PC market, or the tiring effects of a decade of litigation, although all were factors. We have to understand the problems in a broader context, addressed in this chapter. Then, chapter 16 looks at how IBM responded and the results, even at the risk of repeating points made earlier. There is much to learn, beginning with a review of the financial performance of the company to demonstrate the magnitude of the crisis it faced. Then, we move to an explanation of how IBM’s growth strategy failed, which will be useful to those who consider corporate strategy crucial in understanding business history. It is the cautionary tale that strategy created by smart, well-intentioned, successful executives is no guarantee of success. IBM’s experience reinforces the importance of strategy linked to execution, the limits of strategy, and the uncertainties of directing even a well-run company in uncertain times. IBM’s story reminds us that strategy is about making choices, mitigating risks, and giving employees a direction, a purpose. Realities and choices shaped subsequent events here. Historians observe that incremental decisions often are the determinants of a company’s strategy and performance. Control—a central intent of strategy—is an aspiration, not a guarantee of success. As William Lazonick argues, understanding decision making in creating strategy is essential. It is the lens through which this chapter examines IBM, because its experience reinforces his argument.6

WHAT THE FINANCIAL RECORD SHOWS

By beginning with the financial record, we can see the stark shift from the well-run company to one in deep trouble, and the swiftness of that transition. The combination of extent and speed of change that so shocked people highlighted the feeling of betrayal on the part of customers, stockholders, and especially employees. The numbers illustrate that a large corporation can change quickly, so much so that normal causes of largeness and old attitudes can only partially explain what happened at IBM. American automotive companies were also under enormous pressure beginning in the late 1960s; high-profile tire manufacturers failed. Many firms in various industries were also in trouble in the 1970s and 1980s, so while IBM managed to delay its difficult time, it ultimately was not alone.

Just as Louis V. Gerstner Jr. and a small group of executives were able to formulate a rescue of IBM in the 1990s, a handful of earlier senior managers, perhaps as few as two dozen, had led IBM into the abyss in the 1980s. The only way IBM could move swiftly enough in one direction or another was through the personal actions of these executives, and none more than those of its CEOs. They were never pleased with the speed at which their vast organizations transformed, but IBM evolved. With the benefit of hindsight and the historical record, it is clear that both Opel and Akers can be held responsible for much of what happened, not the employees who Akers blamed but who were powerless individually to turn the ship around. They could only do their jobs and watch the disaster unfold.

Nevertheless, there was plenty of blame to go around. Wall Street gave terrible advice to IBM and its board, then pressured the board to fire Akers.7 Board members ignored their responsibilities and listened too much to Akers and to stock analysts. None of these groups—IBM executives, board members, or Wall Street analysts and large institutional stockholders—paid enough attention to the company’s customers or to its competitors. Their behavior ran contrary to the Watsonian practices of being attentive to their customers and ruthless in neutralizing competitors, behaviors that won IBM customer loyalty, if also continuing to attract the attention of antitrust lawyers.

Regarding Akers’s complaint that IBM was losing market share all over the world, what did the facts show? Recall that, on the surface, the first half of the 1980s was great, even though the economics of mainframes, minicomputers, and PCs were changing and IBM was struggling to keep up. Table 15.1 shows the revenues and profits (earnings) IBM reported for 1980 through 1985. IBM still dominated the mainframe and PC markets. Table 15.2 paints a different picture. While revenue continued to pour into the company, total earnings became uneven for the first time since the 1930s. To an informed observer, this data indicated growing volatility in the company’s operations and its deteriorating performance in the marketplace but not necessarily in the quality of the company’s strategy. The decline in the number of employees, however, sent up red flags among employees, while Wall Street and the IBM board saw this as evidence of management taking steps to control expenses. Meanwhile, IBM’s management kept sending the world soothing messages of confidence. Even the terrible performance of 1989, which could not be hidden from the public, did not stop Akers from declaring that “demand for IBM’s products and services remains good … we look forward to a more competitive IBM” and that “IBM is planning for growth in all major geographies in 1990,” built on the opportunity to acquire “new” (additional) customers and take advantage of new uses of computers.8

IBM’s good years: Financials and number of employees, 1980–1985, select years (revenues and earnings in billions of dollars) |

||||||

Year |

Gross income |

Net earnings |

Year-end global workforce |

|||

1980 |

26.2 |

3.4 |

341,279 |

|||

1982 |

34.4 |

4.41 |

364,796 |

|||

1984 |

46.3 |

6.58 |

394,930 |

|||

1985 |

50.7 |

6.55 |

404,535 |

|||

Source: Emerson W. Pugh, Building IBM: Shaping an Industry and Its Technology (Cambridge, MA: MIT Press, 1995), 324. |

||||||

IBM’s transition years: Financials and number of employees, 1986–1990 (revenue and earnings in billions of dollars) |

||||||

Year |

Revenue |

Net earnings |

Year-end global workforce |

|||

1986 |

52.16 |

4.79 |

403,508 |

|||

1987 |

55.26 |

5.26 |

389,348 |

|||

1988 |

59.6 |

5.74 |

387,112 |

|||

1989 |

62.65 |

3.72 |

383,220 |

|||

1990 |

68.93 |

5.97 |

373,289 |

|||

Source: Emerson W. Pugh, Building IBM: Shaping an Industry and Its Technology (Cambridge, MA: MIT Press, 1995), 324. |

||||||

Now look at table 15.3, where in a three-year period revenue, earnings, and number of employees all shrank. Note the extent of the change from 1990 through 1991: a $4 billion drop in revenue, $8 billion freefall in earnings, and a substantial decline in the number of employees, although Wall Street observers thought that the employee population should have shrunk further. Performance in 1992 and 1993 reflected that continuing trend in deteriorating effectiveness that had started when the number of employees began to shrink in 1987.

IBM’s disaster years: Financials and number of employees, 1991–1993 (revenue and earnings in billions of dollars) |

||||||

Year |

Revenue |

Net earnings |

Year-end global workforce |

|||

1991 |

64.77 |

−2.86 |

344,396 |

|||

1992 |

64.52 |

−4.97 |

301,542 |

|||

1993 |

62.72 |

−8.1 |

256,207 |

|||

Source: Emerson W. Pugh, Building IBM: Shaping an Industry and Its Technology (Cambridge, MA: MIT Press, 1995), 324. |

||||||

However, the deterioration proved more subtle than the public evidence suggested. A closer look at IBM’s annual reports in 1991 through 1993 reveals that it actually had operating earnings of $3 billion in 1991 and 1992, although they dropped sharply to $300 million in 1993. The reports of IBM losing money resulted from the huge write-offs it took to cover the cost of severance for the tens of thousands of employees pushed out of the company. If it had not let so many employees go, earnings in 1991 and 1992 would have been lower than in the past, but not so bad. The problem in 1993 was the precipitous decline in earnings and what it foretold about 1994, which is what set off alarms. From 1991 through 1993, IBM claimed $24 billion in restructuring costs. Those were massive write-offs by any measure, made more frightening because they came quickly, in the short span of three years.

Instead of capitalizing such expenses over several years, as is normal for U.S. corporations, IBM claimed (“recognized”) them in the years in which they occurred. The company wanted to lower its overhead costs quickly and put these expenses behind it as part of the process of “turning the ship” in a new direction. Akers and his colleagues did not believe there would be further write-downs year after year. Their accounting tactic created more chaos sooner and of a greater intensity than might otherwise have been the case, fueling concerns that IBM was headed for disaster. That fear surfaced even with the first charge to earnings but grew as others followed. In defense of Akers, who made this decision one year at a time, he did not think this would happen more than once. As business management experts D. Quinn Mills and G. Bruce Friesen summarized it, “What began as a prudent fiscal practice became a burden under which IBM’s finances and Akers’s own career collapsed.”9 Another expert on the company, Wall Street Journal reporter Paul Carroll, summed up IBM’s situation: “By fall 1992, things were out of control.” In the third quarter, “business died in the last couple of weeks of the quarter,” despite Akers’s prediction that it would be a good quarter. The last quarter of the year “turned into IBM’s biggest disaster ever.”10 That was the bad news. The good news was that Akers’s successor thus came into IBM with a great deal of the restructuring costs behind him that otherwise he would have taken. Recall that all this activity occurred while the company had experienced a decline in operating margins dating to the 1970s. In the 1950s, a dollar’s worth of revenue spun off 55 cents in earnings. That rate of return kept dropping steadily to below 40 cents by 1993, with mainframes by then a diminishing contributor to IBM’s finances. IBM prudently sought to reduce operating expenses and moved heaven and earth to do so, cautiously in the beginning but with a brisk sweep through the business by the time Gerstner joined IBM.

How did it go? By 1990, IBM’s selling, general, and administrative (SG&A) expenses consumed 30 percent of the company’s revenue. That was a bit high, but very high if you take into account the long-term decline in the profits of the mainframe business when customers were also acquiring other forms of computing. By 1993, IBM had only reduced its operating expenses by 1 percent. Restructuring had amounted to shrinking an existing organization, not a fundamental redesign of the company. Akers had thought of a fundamental reboot of the company. In the early 1990s, margins still remained high and expenses lower. Margins remained in the 16 percent range, not bad, though dropping, while expenses were not falling fast enough. When IBM hit its financial wall in 1993, its margins came in at 39 percent and its operating expenses at 29 percent, leaving 1 percent profit after accounting for all other costs. If we layer on the charges for shutting factories and discarding employees, we arrive at the numbers in table 15.3. The company was unable to cut expenses as quickly as it needed to, because it had too many factories and employees and too much bureaucracy. The top 200 executives had not been sufficiently aggressive in redesigning their operations and slashing expenses.

IBM’s stock value reflected the company’s changing circumstances, shocking investors who saw it as the safe stock for “orphans and widows.” From 1943 to 1974, its value had risen continuously and the company had paid out a dividend. The years 1975 through 1981 were turbulent as IBM’s stock price declined, as did the value of the entire market. From 1982 through 1987, IBM’s stock value rose, at which point it began to decline into the 1990s, dropping to levels not seen in a decade. A deeper dive into the numbers shows that, adjusted for inflation, the stock had stagnated in the 1970s and 1980s, and of course in the early 1990s. The market had kept the stock’s value artificially high because its quarter-to-quarter forecasting made it look like the company’s business was improving. It was the point Akers made each quarter and in each annual letter to stockholders.11

A more fundamental influence on the value of IBM and hence on its performance was the changes in information technology, with cycles different from the financial flows that were of greater interest to Wall Street. This forced companies like IBM to better manage balances between mature technologies and their revenue and profit streams as the former technologies became obsolete and new ones surfaced with different costs and profits. That balancing act was at best difficult to achieve for any firm. IBM struggled with that balance all through the 1970s and 1980s. Mills and Friesen explained the connection with stock values: “In periods when IBM is pioneering new technology projected earnings will be good and real growth positive; the markets therefore overvalue potential and elevate the stock above long-run equilibrium.”12 The bottom line was that the stock was overvalued for too long. When problems with IBM’s performance became obvious, its value quickly declined by double digits.

What about Akers’s complaint regarding market share—what happened? Between the mid-1980s and the end of 1991, IBM lost market share in slow-growing markets, specifically in mainframes and minicomputers. The more serious problem concerned mainframes. In 1986, IBM generated $17 billion in sales from mainframes, but by 1991 that business had declined to $15 billion. IBM’s market share shrank by nearly a third. IBM’s revenue shrank by 2.4 percent, while all its rivals’ revenues grew on average by 3.3 percent. That was alarming, but in an industry where changing technologies required vendors to ride new waves of technology, the bigger problem for IBM occurred with those new forms of computing, the most rapidly expanding markets at the time. Numbers proved deceiving. In 1986, for example, IBM sold $6 billion in PCs and workstations, and in 1991 sales of these products were $10 billion. While impressive, in those intervening years IBM grew sales by 11 percent while all other vendors combined expanded theirs by 21 percent.13

IBM’s relatively weaker growth was not for lack of trying. The $6 billion per year IBM spent on R&D was more than almost all its rivals combined, but its shrinking percentage of market share continued across the product line. All of this was made worse by new customer managers coming to power who were increasingly comfortable buying from multiple vendors, suppliers who offered newer technologies at lower cost that performed well and conformed to industry standards.

Akers was right to be frustrated. IBM faced declining demand for what it was selling. Its executives were staring at a death spiral that if not corrected meant the end of IBM. Similar problems had destroyed many of IBM’s rivals. Was IBM next? More to the point, how did IBM get into this mess in the first place? It is the central question to ask because its senior executives understood the economic dynamics underpinning IBM’s mainframe and PC businesses. Despite this, the majority demonstrated a reluctance to reduce the power and cultural influence of their portions of the firm as technological changes suggested new directions, new opportunities not seized on as quickly as they might have been, the story introduced in chapter 14.

A GROWTH STRATEGY GONE WRONG

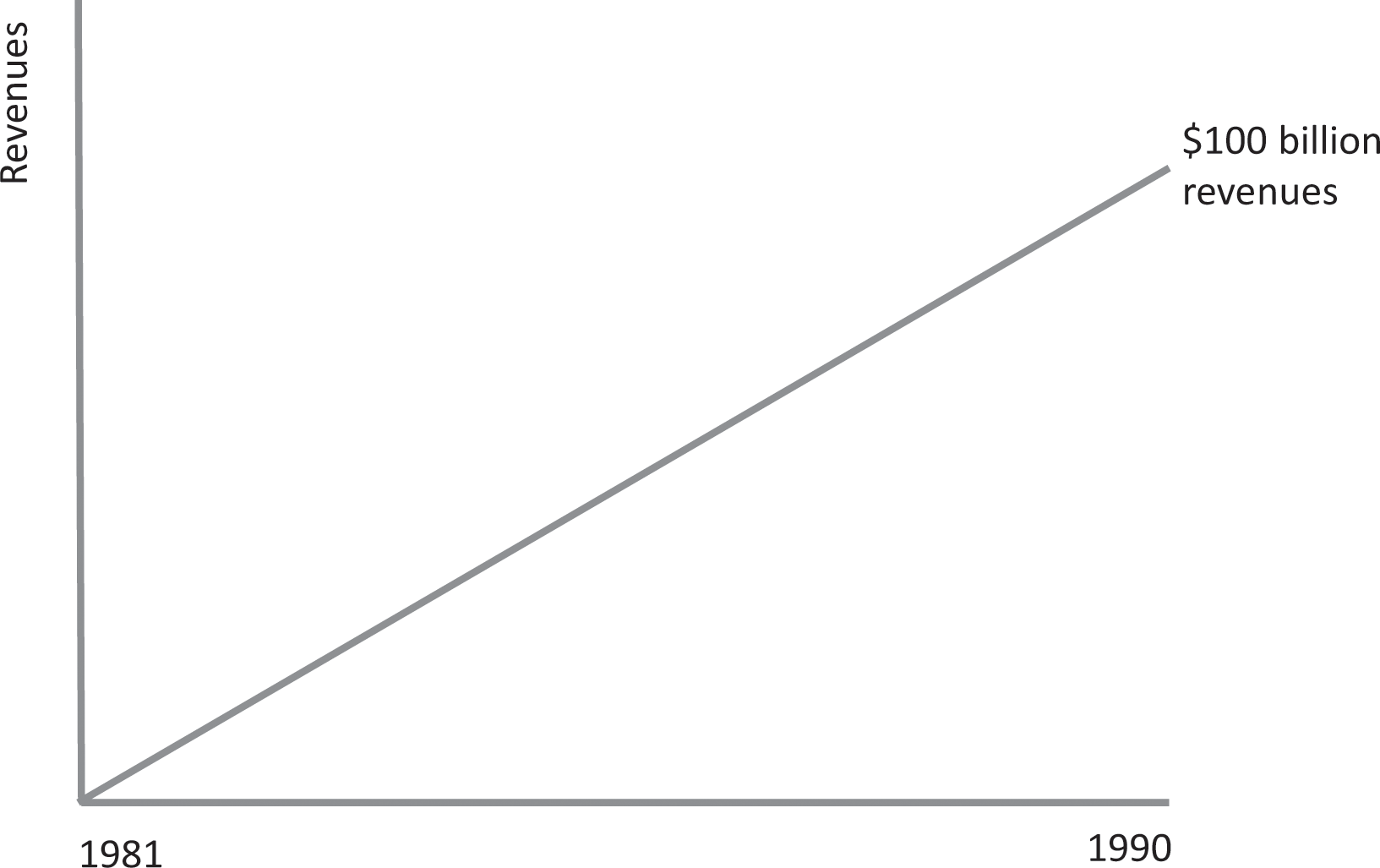

IBM had a business strategy that failed because of suppositions underpinning it. A junior executive in the strategy department at Corporate walked into a Sales School classroom in Poughkeepsie, New York, in 1982 to introduce sales trainees to IBM’s business plan. He had his collection of slides (“foils” in IBM’s language), which he assured his audiences were the same ones he used with the CEO and his most senior managers. They were so secret, he said, that the students would not be given a copy of them. After discussing market trends, IBM’s plans for new products, and so forth, he put up a slide showing what all this meant for IBM’s financial future. It showed that IBM’s revenue would grow from $29 billion in 1981 to $100 billion in 1990. Figure 15.2 is a representation of that chart. Half a dozen Sales School instructors were sitting in the back of the class. All had been successful salesmen. One dropped his coffee, while several others looked surprised. Following normal practice with guest speakers, none asked questions; none of the students who should have did. After the strategist left, the instructors asked each other if they had ever seen such a chart that unwaveringly pointed straight up. The slide did not show wavering lines to account for years of more or less revenue growth. It was a mathematically compounded, even growth line to $100 billion.

A representation of the chart used in the 1982 sales meeting that forecast revenue growth to $100 billion by 1990.

In other words, it was IBM’s old view of controlled growth, much as it enjoyed in the 1950s through the 1970s, imposed on the 1980s, when the instructors sitting in the back row knew that emerging technologies guaranteed a different growth pattern. What that would be remained foggy. That same chart appeared all over the company and soon was even used by industry pundits. By late 1983, anyone who cared to know had probably seen or heard about it. In annual reports, John Opel and John Akers spoke about an industry whose growth would reach over a trillion dollars worldwide, so on the surface IBM’s projection seemed reasonable and conservative. Opel was excited and had explained to his board how the oil and global economic crises of the 1970s were behind them and that IBM would increase revenue each year by an amount equal to DEC’s revenues. Only Japanese mainframe vendors, whom he worried most about, stood in his way, constantly drawing him back to the locus of his career, mainframes.

Akers’s strategy for riding the anticipated wave of new demand and for addressing the Japanese threat revolved around becoming the low-cost provider of machines and key components. That meant building factories that could produce in quantity. That additional construction called for more factory employees, salesmen, and other support personnel. Because of the large barriers to entry for manufacturing semiconductors, Akers saw that building such capacity in support of mainframes would play to IBM’s technological strengths and economies of scale. IBM’s financial power would allow it to capitalize its investments over the long haul. Akers’s strategy meant all these new employees represented an unavoidable expense, and their subsequent dismissal created enormous churn in the company for the next quarter century.

The thinking that went into his call for massive growth had been worked out in the late 1970s. In 1980, for the first time, IBM published a public corporate strategy. Opel told stockholders that, “We see many indications that the growth of IBM’s business will remain strong” and that “the majority of IBM’s growth will continue to come in data processing and office products.” He added that, first, to execute the strategy, IBM was “investing heavily in the several dozen key technologies that drive the information processing industry ahead,” including “placing a high priority on designing and building quality into every product.” He intended to be the “low-cost” provider, to invest in “sales and service innovation,” and to add facilities.14 The following year, using almost the same language, he repeated the mantra for IBM “to be the product leader,” relying on such descriptors as “foremost in quality,” products that were “defect-free,” and of best “value.” Second, he stated that it is IBM’s “goal to be the most efficient company in our industry,” and third, “to compete in, and grow with, the information industry in all its aspects.”15 He then devoted the next two pages of his letter to stockholders to a description of plans for new products, higher-volume marketing, expansion of the company’s global footprint, and optimizing the number of employees.

Akers kept tuning the message. In 1983, he described four objectives. IBM was now going to grow with the industry, meaning at the same speed. IBM would demonstrate leadership across the entire product line, with technology, quality, and value. IBM would be the most efficient by being the low-cost producer and low-cost seller, and have the lowest cost of administration. IBM would maintain high levels of profit. How did Akers do with his four-part plan? During his watch, IBM lost market share in all its markets. Better, more innovative, less-expensive technologies appeared first outside of IBM. Akers’s cost of doing business remained one of the highest in the industry. Profitability evaporated, but it could almost be excused in the euphoria that enveloped the company. IBM had been accused of hubris and “arrogance” throughout the 1970s and 1980s. Both Watsons would have found this most curious, but in part the conceit had been fueled by more than IBM’s success with the S/360 and S/370, or even later in the early years of the PC. As Robert Heller explained,

The IBM of the early Eighties was a place of inexhaustible pride. Like the Roman Empire at its zenith, IBM was rich with the fruit of past conquests and supremely confident of new victories. To admirers, inside and outside the empire, its actions and ideas seemed to fit together with an innate perfection, like some vast Swiss watch.16

In their best-selling business book of the decade, In Search of Excellence, McKinsey and Co. consultants Thomas J. Peters and Robert Waterman Jr. cited IBM as one of the greatest companies on earth.17 They celebrated IBM’s bias toward action, continuous ties to customers, productivity, innovative actions, and emphasis on business values, ethics, and a combination of loose and tight controls. That in hindsight they were more wrong than right did not become obvious for half a decade, but for the moment, IBM was fabulous, ranked the best-run company by Fortune magazine year after year. It seemed IBM could do no wrong.

Buck Rodgers’s mantra, “The IBM Way,” seemed absolute in its confidence and relevance, and it was widely emulated even late in the 1980s. Liberated from the constraints of the antitrust suit of the 1970s, IBM was now free to expand, to manifest its excellence in all that it touched. IBM’s public relations machine seemed to work overtime to promote this image of excellence. Read Think magazine, annual reports, and transcripts of interviews with executives, and the same messages continued. Every success called for its own press release, every failure well couched in language dismissing its relevance. College graduates wanted to work for IBM, just as in the 2010s they saw Google, Amazon, and Apple as the “go-to” destinations for the smart and ambitious. That was the environment in which John Opel stepped in as IBM’s leader.

FLAWED EXECUTION

Curiously, in none of Opel’s public statements about IBM’s new strategy did he mention what customers wanted, only what IBM desired. It is against this background of growth that we can come back to the fateful decision to shift IBM’s long-standing practice of renting equipment to outright sale of its products.18 Recall that Opel wanted the faster influx of revenue from outright sales to fund his expansion. IBM began reporting leases as increased sales, an accounting gimmick, which nonetheless made it possible for the company to generate additional funding for the growth strategy. All over IBM, management obtained permission to hire thousands of employees, while billions of dollars went into new factories, sales headquarters, and training facilities. Employees and construction companies described IBM’s expenditures in the 1980s as “lavish.” Mills and Friesen correctly called it “wildly optimistic; even negligently so.”19 While overconfidence and arrogance prevailed, customers began complaining about the changing terms of acquiring equipment, concerned that the ties with IBM that so bound them together through leasing would deteriorate. They were right.

Figure 15.3

John Opel was the CEO who expanded IBM’s factories and number of employees in the belief that the company would grow massively in the 1980s. Photo courtesy of IBM Corporate Archives.

To pull off the financial strategy, revenue from renting and leasing had to drop from 85 percent of IBM’s sales to 12 percent. The surge in income that would come from selling equipment outright instead of accumulating revenue over the life of a lease was a bubble. By the early 1990s, only 4 percent of IBM’s revenue came from the steady flow of rentals. The rest had to be earned every year against rivals and in the face of fluctuating economic conditions. It had to take into account the seemingly ever-changing technologies underpinning everyone’s products. IBM became increasingly marginalized as customer loyalty declined as a result of Opel’s fateful decision to transform IBM’s offerings from a relationship-based business grounded in leasing to a transaction-based one relying on purchases. IBM no longer served as the center of the data processing ecosystem. Industry observers opined that the shift away from leasing did not need to occur, because the 4300 computers were generating a good deal of new revenue.20 IBM sped up the move to the purchase strategy for new and already installed equipment. If properly managed, PC sales would have provided additional manna from Heaven.21 Instead, purchase revenue cannibalized the installed leased equipment, sacrificing predictable cash flows for uncertainty and short-term gains.

It did not help that the fundamental problem with IBM’s strategy was its overdependence on one assumption: that mainframes would dominate computing in the 1980s. Instead, a world of telecommunicating computers emerged using PCs, desktop processors, and minicomputers. In the 1980s, customers worldwide spent more on PCs (including software and maintenance) and telecommunications than on mainframes. So, instead of the $100 billion forecast for 1990, IBM brought in $69 billion, still a good performance but far from what Opel had planned on in 1980 and 1981. IBM acquired a great deal of modern manufacturing and sales capacity—for the wrong products. Its resource imbalances were real, and widening by huge amounts. As early as 1983, some of IBM’s senior executives saw that they had already missed the opportunity to control the software business for PCs. When Sales School instructors saw that fateful slide, one could understand their shock. As one industry observer insightfully noted, the shift “represented a mortgage on the future,” while revenue expanded fabulously and account control began a deep, rapid decline.22

In February 1985, Opel turned over control of IBM to John Akers, while remaining chairman. Other senior leaders included Paul Rizzo (b. 1936), now vice chairman, and Jack Kuehler (1932–2008), corporate vice president for products. All grew up in the mainframe era. Akers inherited a company that could not sustain Opel’s growth strategy. Several immediate events forced the switch away from his plan. IBM introduced the 3090 mainframe in February 1985, which contained few innovations but doubled performance versus price, the expected norm for new computers. The 3090s were uncompetitive when pitted against Amdahl’s and those of IBM’s other Japanese rivals. Revenue from mainframes remained soft. The 3090’s attractions were insufficient to convince customers to replace recently acquired equipment with this one. Second, IBM still did not have its act together with respect to minicomputers, so it was losing share to other vendors. Third, IBM went through the embarrassing PC Jr. episode. Akers’s first year resulted in weak profits. Famous for not liking bad news, he seemed in denial about softening mainframe sales in 1985 while declining PC profits put pressure on his margins. The square-jawed former Navy pilot seemed to lack the certitude called for under the circumstances, a bias for confident action.23

The year 1986 unfolded as another lackluster year. In January, an IBM executive told Fortune that IBM had “a revenue problem.”24 Costs, too, were disconcerting. Akers and his cohorts initially resisted laying off employees, respecting IBM’s historic full-employment practice. Akers and his generation of executives kept riding technologies and practices that needed changing. The same Fortune article observed that IBM “persisted in trying to sell them [customers] products when what they wanted was solutions, help in getting their thousands of computers to talk to each other, help in wringing both productivity gains and competitive advantage out of their investment in data-processing equipment.”25 That same month, Fortune announced its annual ranking of the most admired firms, and IBM was now number seven. While that was still a good ranking, as the magazine explained, “The world does not expect mere competence from IBM; it expects heroics. The company has been a near-icon. Millions of Americans rate it a national asset and prize it as a symbol of managerial and technological excellence.”26

In fairness to Akers, IBM responded to its failed strategy, the subject of chapter 16. Akers and his circle had responded to the error of their strategy in two phases, the first involving the management team that had implemented the failed strategy and then a second designed to correct this first attempt, the latter led by Louis V. Gerstner Jr. Accounts of IBM’s crises of the 1980s and 1990s describe IBM’s history as one combined phase of decline and Akers’s faulty response, Gerstner’s rescue of IBM as a separate event, and his postrecovery activities as an extension of his rescue. The evidence suggests a different chronology, as we will see in subsequent chapters. This chapter discussed the problems and crisis facing IBM. Chapter 16 recounts what Akers did in more detail than in this chapter, providing a different narrative than what has been available previously. Subsequent chapters will deal with the turnaround in IBM’s fortunes Gerstner initiated (the second response). I then demonstrate that the second half of Gerstner’s tenure was not about rescuing IBM but rather about developing and implementing a new strategy, so it deserves to be treated separately from the initial rescue. I present that in chapter 18, continuing the arc of his new IBM through the chairmanship of Sam Palmisano to 2012.