page 420

©Joana Lopes/123RF

page 421

If you ever thought about buying stocks or bonds but decided not to, your reasons were probably like most other people’s: You didn’t know enough to make a good decision, and you lacked enough money to diversify your investments among several choices. These same two reasons explain why people invest in mutual funds. A mutual fund pools the money of many investors—its shareholders—to invest in a variety of securities.1 For a fee, a professional fund manager or team of managers invest money from investors in stocks, bonds, and other securities that are appropriate to a fund’s investment objective.

Mutual funds are an excellent choice for many individuals. In many cases, they can also be used for retirement accounts, including traditional individual retirement accounts, Roth IRAs, and 401(k) and 403(b) retirement accounts.

An investment in mutual funds is based on the concept of opportunity costs, which we have discussed throughout this text. Simply put, you have to be willing to take some risks if you want to get larger returns on your investments. The fact that fund investments can decrease in value does underscore the need to understand the risk associated with all investments, including mutual funds.

LO13.1

Explain the characteristics of mutual fund investments.

Why Investors Purchase Mutual Funds

For many investors, the notion of investing their money in a mutual fund may be a new idea, but mutual funds have been around for a long time. Fund investing began in Europe in the late 1700s and became popular in the United States before the Great Depression in 1929. After the Depression, government regulation increased, the number of funds grew, and the amount invested in funds continued to increase. New types of funds, including index funds, aggressive growth funds, life-cycle funds, and social responsibility (or green) funds, were created to meet the needs of a larger and more demanding group of page 422investors. During this same time period, the cost of investing in funds decreased while the popularity of fund investing increased. Experts often say that one man, John Bogle, was the driving force behind attempts to make fund investing affordable for the average American. When he introduced the Vanguard 500 Index Fund in 1976, he gave investors a low-cost way to invest in funds while providing investment diversification. Today, the Vanguard Group is one of the largest fund companies that competes with other companies in the fund industry.

Despite the accusations of fraud and mutual fund scandals in the first part of the 21st century and poor fund performance and investor losses during the last economic crisis, mutual funds are still the investment of choice for many investors. The following statistics illustrate how important mutual fund investments are to both individuals and the nation’s economy:

Almost 96 million individuals own mutual funds in the United States.2

The number of funds grew from 361 in 1970 to over 19,000 by the end of 2016.3

The combined value of assets owned by investment companies in the United States totals more than $19 trillion.4

No doubt about it, the mutual fund industry is big business. And yet you may be wondering why so many people invest in mutual funds.

The Psychology of Investing in Funds

The major reasons investors purchase mutual funds are professional management and diversification. Most investment companies do everything possible to convince you that they can do a better job of picking securities than you can. Sometimes these claims are true, and sometimes they are just so much hot air. Still, investment companies do have professional fund managers who try to pick just the “right” securities for their funds’ portfolios. Be warned: Even the best portfolio managers make mistakes. So you must be careful and evaluate a fund before investing your money.

The diversification mutual funds offer spells safety, because a loss incurred with one investment contained in a fund may be offset by gains from other investments in the fund. For example, consider the diversification provided in the portfolio of the Invesco Dividend Income Fund, shown in Exhibit 13–1. An investment in the $2.5 billion Invesco Dividend Income Fund represents ownership in 60 different companies. For beginning investors or investors without a great deal of money to invest, the diversification offered by funds is especially important because there is no other practical way to purchase the individual stocks issued by a large number of corporations. A fund such as the Invesco Dividend Income Fund, on the other hand, can provide a practical way for investors to obtain diversification because the fund can use the pooled money of a large number of investors to purchase shares of many different companies.

page 423

Exhibit 13–1 Types of Securities Included in the Portfolio of the Invesco Dividend Income Fund

Top Industries |

% of Total Assets |

|---|---|

Multiutilities |

8.72 |

Integrated telecommunication services |

7.58 |

Pharmaceuticals |

7.08 |

Electric utilities |

6.75 |

Integrated oil and gas |

6.57 |

Gas utilities |

5.40 |

Regional banks |

5.19 |

Packaged food and meats |

5.19 |

Household products |

4.17 |

Tobacco |

2.86 |

Top 5 Equity Holdings |

% of Total Assets |

WGL Holdings |

3.19 |

M&T Bank Corporation |

3.15 |

Procter & Gamble |

2.91 |

Public Service Enterprise Group |

2.79 |

Coca-Cola |

2.73 |

Source: Invesco (https://www.invesco.com/pdf/I-DIVI-PC-1.pdf), accessed March 31, 2017.

Characteristics of Funds

Today funds may be classified as closed-end funds, exchange-traded funds, or open-end funds.

CLOSED-END, EXCHANGE-TRADED, OR OPEN-END MUTUAL FUNDS Approximately 260, or less than 2 percent, of all mutual funds are closed-end funds offered by investment companies.5 A closed-end fund is a mutual fund whose shares are issued by an investment company only when the fund is organized. As a result, only a certain number of shares are available to investors. After all the shares originally issued have been sold, an investor can purchase shares only from another investor who is willing to sell. Typically, closed-end funds are actively managed by professional fund managers and shares are traded on the floors of stock exchanges or in the over-the-counter market. Like the prices of stocks, the prices of shares for closed-end funds are determined by the factors of supply and demand, by the value of stocks and other securities contained in the fund’s portfolio, and investor expectations.

page 424Most exchange-traded funds (ETF) are funds that invest in the stocks or other securities contained in a specific stock or securities index. While most investors think of an ETF as investing in the stocks contained in the Standard & Poor’s 500 stock index, many different types of ETFs available today attempt to track all kinds of indexes, including:

Midcap stocks.

Small-cap stocks.

Fixed-income securities.

Stocks issued by companies in specific industries.

Stocks issued by corporations in different countries.

As in a closed-end fund, shares of an exchange-traded fund are traded on a securities exchange or in the over-the-counter market. With both types of funds, an investor can purchase as little as one share of a fund. Also as in a closed-end fund, prices for shares in an ETF are determined by supply and demand, the value of stocks and other investments contained in the fund’s portfolio, and investor expectations.

Although exchange-traded funds are similar to closed-end funds, there is an important difference. Most closed-end funds are actively managed, with portfolio managers making the selection of stocks and other securities contained in a closed-end fund. An exchange-traded fund, on the other hand, invests in the securities included in a specific index. Exchange-traded funds tend to mirror the performance of the index, moving up or down as the individual securities contained in the index move up or down. Therefore, there is less need for a portfolio manager to make investment decisions. Because of passive management, fees associated with owning shares are generally lower than those of both closed-end and open-end funds. In addition to lower fees, other advantages to investing in ETFs include:

There is no minimum investment amount, because shares are traded on an exchange and not purchased from an investment company.

Shares can be bought or sold through a brokerage firm any time during regular market hours at the current price.

You can use limit orders and the more speculative techniques of selling short and buying on margin—all discussed in Chapter 12—to buy and sell ETF shares.

Although increasing in popularity, approximately 2,500, or about 13 percent of all funds, are exchange-traded funds.6

Just over 16,000, or about 85 percent of all mutual funds, are open-end funds.7 An open-end fund is a mutual fund whose shares are issued and redeemed by the investment company at the request of investors. Investors are free to buy and sell shares at the net asset value. The net asset value (NAV) per share is equal to the market value of securities contained in the fund’s portfolio minus the fund’s liabilities divided by the number of shares outstanding.

For open-end funds, the net asset value is calculated at the close of trading each day.

page 425In addition to buying and selling shares on request, most open-end funds provide their investors with a wide variety of services, including payroll deduction programs, automatic reinvestment programs, automatic withdrawal programs, and the option to change shares in one fund to another fund within the same fund family—all topics discussed later in this chapter.

COSTS: LOAD FUNDS COMPARED TO NO-LOAD FUNDS With regard to cost, mutual funds are classified as load funds or no-load funds. A load fund (sometimes referred to as an A fund) is a mutual fund in which investors pay a commission every time they purchase shares. The commission, often referred to as the sales charge, may be as high as 8.5 percent of the purchase price for investments. Many exceptions exist, but the average load charge for mutual funds is between 3 and 5 percent. Notice in the example below, the Davis Opportunity mutual fund has a load charge of 4.75 percent. As illustrated below, this represents a sales charge of $475 on a $10,000 investment. After the $475 is paid, the remaining $9.525 can be used to purchase shares in the fund.

There are two specific exceptions that should be noted. First, investment companies offering front-end load funds often waive or lower fees for shares purchased for retirement accounts. Second, load fund fees are often lower for investors who make large purchases.8

The “stated” advantage of a load fund is that the fund’s sales force (account executives, financial planners, or employees of brokerage divisions of banks and other financial institutions) will explain the mutual fund, help you determine which fund will help you achieve your financial objectives, and offer advice as to when shares of the fund should be bought or sold.

A no-load fund is a mutual fund in which the individual investor pays no sales charge. No-load funds don’t charge commissions when you buy shares because they have no salespeople. If you want to buy shares of a no-load fund, you must make your own decisions and deal directly with the investment company. The usual means of contact is by internet, telephone, or mail. You can also purchase shares in a no-load fund from many brokers, including Charles Schwab, TD Ameritrade, Fidelity, and E*Trade.

As an investor, you must decide whether to invest in a load fund or a no-load fund. Some investment salespeople have claimed that load funds outperform no-load funds. But many financial analysts suggest there is generally no significant difference between mutual funds that charge commissions and those that do not.9 Since no-load funds offer the same investment opportunities load funds offer, you should investigate them further before deciding which type of mutual fund is best for you.

Instead of charging investors a fee when they purchase shares in a mutual fund, some mutual funds charge a contingent deferred sales load (sometimes referred to as a back-end page 426load or a B fund), a fee that shareholders pay when they sell shares in a mutual fund. Typically, these fees range from 1 to 5 percent, depending on how long you own the mutual fund before making a withdrawal. For example, you may pay a 5 percent contingent deferred sales load if you withdraw money the first year after your initial investment. In most cases, this fee declines every year until it disappears if you own shares in the fund for more than five years.

COSTS: MANAGEMENT FEES AND OTHER CHARGES Companies that sponsor funds charge management fees. This fee, which is disclosed in the fund’s prospectus, is a fixed percentage of the fund’s net asset value on a predetermined date. Today annual management fees range between 0.25 and 1.5 percent of the fund’s net asset value. While fees vary considerably, the average is 0.5 to 1 percent of the fund’s net asset value.

The investment company may also levy a 12b-1 fee (sometimes referred to as a distribution fee) to defray the costs of marketing a mutual fund, commissions paid to a broker who sold you shares in the fund, and shareholder service fees. Approved by the Securities and Exchange Commission, annual 12b-1 fees are calculated on the value of a fund’s net assets and cannot exceed 1 percent of a fund’s assets per year. Note: For a fund to be called a “no-load” fund, its 12b-1 fee and shareholder service fees must not exceed 0.25 percent of its assets.

Unlike the one-time sales load fees that mutual funds charge to purchase or sell shares, the 12b-1 fee is often an ongoing fee that is charged on an annual basis. Note that 12b-1 fees can cost you a lot of money over a period of years. Assuming there is no difference in performance offered by two different mutual funds, one of which charges a 12b-1 fee while the other doesn’t, choose the latter fund. The 12b-1 fee is so lucrative for investment companies that a number of them sell Class C shares that often charge a higher 12b-1 fee and no sales load or contingent deferred sales load to attract new investors. (Note: Some investment companies may charge a small contingent deferred sales load for Class C shares if withdrawals are made within a short time—usually one year.) When compared to Class A shares (commissions charged when shares are purchased) and Class B shares (commissions charged when withdrawals are made over the first five years), Class C shares, with their ongoing, higher 12b-1 fees, may be more expensive over a long period of time.

To help you sort out all the research, statistics, and information about mutual funds and give you some direction as to what to do first, read the suggestions in the nearby Financial Literacy in Practice feature.

HOW IMPORTANT ARE FEES? Together, all the different management fees and fund operating costs are often referred to as an expense ratio. Since it is important to keep fees and costs as low as possible, you should examine a fund’s expense ratio as one more fact to consider when evaluating a mutual fund.

Mutual fund fees are important because they reduce your investment return and are a major factor to consider when page 427choosing a fund. Although fees and expenses vary from fund to fund, a fund with high costs must perform better than a low-cost fund to generate the same returns to you, the investor.

Make no mistake, fees can make a big difference. For example, assume you invested $10,000 in a fund that earned a 10 percent annual return and had an annual expense ratio of 1.5 percent. Also, assume you chose a second fund that earns 10 percent annual return but had an expense ratio of 0.5 percent. The value of both investments at the end of 20 years is illustrated below.

Although the two funds in the above example earned the same 10 percent return, the fund with the lower expense ratio earned over $11,000 more than the fund with the higher expense ratio. That’s a lot of money that could be yours, instead of going to the investment company that sponsors the fund. The bottom line: Assuming the quality of two different page 428funds is equal and each fund offers the same investment potential, choose the fund with the lower expense ratio.

To calculate how much it will cost to invest in different mutual funds and the effect that fees have on your investment returns, you can use a mutual fund cost calculator. For example, the mutual fund analyzer provided by the Financial Industry Regulatory Authority is easy to use and provides very useful information about the effect of fees on your investment returns. To try it out, go to http://apps.finra.org/fundanalyzer/1/fa.aspx.

The investment company’s prospectus must provide all details relating to management fees, sales fees, 12b-1 fees, and other expenses. Exhibit 13–2 reproduces the summary of expenses (sometimes called a fee table) taken from the Davis Opportunity Fund. Notice that this fee table has two separate parts. The first part describes shareholder transaction fees. For this fund, the maximum sales charge is 4.75 percent. The second part describes the fund’s annual operating expenses. For this fund, the expense ratio is 0.96 percent for Class A shares.

Exhibit 13–2 Summary of Expenses Paid to Invest in the Davis Opportunity Fund

|

Class A Shares |

Class B Shares |

Class C Shares |

|---|---|---|---|

SHAREHOLDER FEES (fees paid directly from your investment) |

|

|

|

Maximum sales charge (load) imposed on purchases (as a percentage of offering price) |

4.75% |

None |

None |

Maximum deferred sales charge (load) imposed on redemptions (as a percentage of the lesser of the net asset value of the shares redeemed or the total cost of such shares. *Only applies to Class A shares if you buy shares valued at $1 million or more without a sales charge and sell the shares within one year of purchase.) |

0.50%* |

4.00% |

1.00% |

Redemption fee (as a percentage of total redemption proceeds) |

None |

None |

None |

ANNUAL FUND OPERATING EXPENSES (expenses that you pay each year as a percentage of the value of your investment) |

|

|

|

Management fees |

0.55% |

0.55% |

0.55% |

Distribution and/or service (12b-1) fees |

0.21% |

1.00% |

1.00% |

Other expenses |

0.20% |

0.43% |

0.20% |

Total annual fund operating expenses |

0.96% |

1.98% |

1.75% |

Source: Davis Opportunity Fund Prospectus (www.davisfunds.com), accessed April 30, 2017, Davis Funds, P.O. Box 8406, Boston, MA 02266.

By now, you are probably asking yourself, “Should I purchase Class A shares, Class B shares, or Class C shares?” There are no easy answers, but your professional financial advisor or broker or your own research can help you determine which class of shares of a particular fund best suits your financial needs. Factors to consider include whether you want to invest in a load fund or no-load fund, management fees, 12b-1 fees, expense ratios, and your own situation. As you will see in the “How to Make a Decision to Buy or Sell Mutual Funds” section in this chapter, a number of sources of information can help you evaluate investment decisions.

To reinforce the material on the costs of investing in funds, Exhibit 13–3 summarizes information for load charges, no-load charges, and contingent deferred sales loads, and reports typical management fees, 12b-1 charges, and expense ratios. It also summarizes the difference between Class A, Class B, and Class C shares.

Exhibit 13–3 Typical Fees Associated with Mutual Fund Investments

page 429

Type of Fee or Charge |

Customary Amount |

|---|---|

Load fund |

Up to 8.5 percent of the purchase. |

No-load fund |

No sales charge. |

Contingent deferred sales load |

1 to 5 percent of withdrawals, depending on how long you own shares in the fund before making a withdrawal. |

Management fee |

0.25 to 1.5 percent per year of the fund’s assets. |

12b-1 fee |

Cannot exceed 1 percent of the fund’s assets per year. |

Expense ratio |

The amount investors pay for all fees and operating costs. Financial experts recommend funds with an expense ratio of 1 percent or less. |

Class A shares |

Commission charge when shares are purchased. |

Class B shares |

Commission charge when money is withdrawn during the first five years. |

Class C shares |

No commission to buy or sell shares of a fund but may have higher, ongoing 12b-1 fees. |

LO13.2

Classify mutual funds by investment objective.

Classifications of Mutual Funds

The managers of mutual funds tailor their investment portfolios to the investment objectives of their customers. Usually, a fund’s objectives are plainly disclosed in its prospectus. For example, the objective of the Vanguard Mid-Cap Growth Fund is described as follows:

This actively managed mid-capitalization option invests primarily in the stocks of mid-size domestic companies that the fund’s investment managers believe have stronger earnings and revenue growth prospects than the average midcap company. Investors who are seeking exposure to the midcap arena of the U.S. stock market and who are willing to endure the volatility that can come from an investment in stocks may wish to consider this fund as an option for their portfolio.10

page 430Although categorizing over 19,000 funds may be helpful, note that different sources of investment information may use different categories for the same fund. In most cases, the name of the category gives a pretty good clue to the types of investments included within the category. The major fund categories are stock funds, bond funds, and other funds.

Stock Funds

Aggressive growth funds seek rapid growth by purchasing stocks whose prices are expected to increase dramatically in a short period of time. Turnover within an aggressive growth fund is high because managers are buying and selling stocks of small growth companies. Investors in these funds experience wide price swings because of the underlying speculative nature of the stocks in the fund’s portfolio.

Equity income funds invest in stocks issued by companies with a long history of paying dividends. The major objective of these funds is to provide income to shareholders. These funds are attractive investment choices for conservative or retired investors.

Global stock funds invest in stocks of companies throughout the world, including the United States.

Growth funds invest in companies expecting higher-than-average revenue and earnings growth. While similar to aggressive growth funds, growth funds tend to invest in larger, well-established companies. As a result, the prices for shares in a growth fund are less volatile compared to those of aggressive growth funds.

Index funds invest in the same companies included in an index such as the Standard & Poor’s 500 stock index. Since fund managers pick the stocks issued by the companies included in the index, an index fund should provide approximately the same performance as the index. Also, since index funds are cheaper to manage, they often have lower management fees and expense ratios.

International funds invest in foreign stocks sold throughout the world; thus, if the economy in one region or nation is in a slump, profits can still be earned in others. Unlike global funds, which invest in stocks issued by companies in both foreign nations and the United States, a true international fund invests outside the United States.

Large-cap funds invest in companies with total capitalization of $10 billion or more. Large-capitalization stocks are generally stable, well-established companies and are likely to have minimal fluctuation in their value.

Midcap funds invest in companies with total capitalization of $2 billion to $10 billion whose stocks offer more security than small-cap funds and more growth potential than funds that invest in large corporations.

Regional funds seek to invest in stock traded within one specific region of the world, such as the European region, the Latin American region, and the Pacific region.

Sector funds invest in companies within the same industry. Examples of sectors include health and biotechnology, science and technology, and natural resources.

Small-cap funds invest in smaller, lesser-known companies with a total capitalization of between $300 million and page 431$2 billion. Because these companies are small and innovative, these funds offer higher growth potential. They are more speculative than funds that invest in larger, more established companies.

Socially responsible funds avoid investing in companies that may cause harm to people, animals, and the environment. Typically, these funds do not invest in companies that produce tobacco, nuclear energy, or weapons or in companies that have a history of discrimination. These funds invest in companies that have a history of making ethical decisions, establishing efforts to reduce pollution, and other socially responsible activities.

Bond Funds

High-yield (junk) bond funds invest in high-yield, high-risk corporate bonds.

Intermediate corporate bond funds invest in investment-grade corporate debt with maturities between three and 10 years.

Intermediate U.S. government bond funds invest in U.S. Treasury securities with maturities between three and 10 years.

Long-term corporate bond funds invest in investment-grade corporate bond issues with maturities in excess of 10 years.

Long-term (U.S.) government bond funds invest in U.S. Treasury securities with maturities in excess of 10 years.

Municipal bond funds invest in municipal bonds that provide investors with tax-free interest income.

Short-term corporate bond funds invest in investment-grade corporate bond issues with maturities of less than three years.

Short-term (U.S.) government bond funds invest in U.S. Treasury issues with maturities of less than three years.

World bond funds invest in bonds and other debt securities offered by foreign companies and governments.

Other Funds

Asset allocation funds invest in different types of investments, including stocks, bonds, fixed-income securities, and money market instruments. These funds seek high total return by maintaining precise amounts within each type of asset.

Balanced funds invest in both stocks and bonds with the primary objectives of conserving principal, providing income, and providing long-term growth. Often the percentage of stocks, bonds, and other securities is stated in the fund’s prospectus.

Fund of funds invest in shares of other mutual funds. The main advantage of a fund of funds is increased diversification and asset allocation because this type of fund purchases shares in many different funds. Higher expenses and extra fees are common with this type of fund.

Lifecycle funds (sometimes referred to as lifestyle funds or target-date funds) are popular with investors planning for retirement by a specific date. Typically, these funds initially invest in risk-oriented securities and become increasingly conservative and income oriented as the specified date gets closer.

Money market funds invest in certificates of deposit, government securities, and other safe and highly liquid investments.

A family of funds exists when one investment company manages a group of mutual funds. Each fund within the family has page 432a different financial objective. For instance, one fund may be a long-term government bond fund and another a growth stock fund. Most investment companies offer exchange privileges that enable shareholders to switch among the mutual funds in a fund family. For example, if you own shares in the Franklin Biotechnology Discovery Fund, you may, at your discretion, switch to the Franklin Balance Sheet Investment Fund. Generally, investors may give instructions to switch from one fund to another within the same family via the internet, over the phone, or in writing. The family-of-funds concept allows shareholders to conveniently switch their investments among funds as different funds offer more potential, financial reward, or security. Charges for exchanges, if any, generally are small for each transaction. For funds that do charge, the fee may be as low as $1 to $5 per transaction.

The Benefits of Portfolio Construction

While reading this section, keep in mind one important fact. As mentioned in the first part of this chapter, there are more than 19,000 funds to choose from. That’s a lot of funds, and by now you realize that some funds will help you achieve your investment goals better than others. To decide which funds are right for you, first, you must decide what type of fund(s) you want. Choices include stock funds, bond funds, or the other funds that were described earlier. You can choose more than one type of fund and even other investment alternatives, including individual stocks, real estate, or more speculative investments, to construct a portfolio of investments that will help you obtain your investment goals. Portfolio construction is the process of choosing different types of stocks, bonds, funds, and other investment alternatives to obtain larger returns while reducing risk. Using the portfolio construction concept is a very personalized process, and the choice of investments is often determined by your goals, tolerance for risk, your age, how much money you have to invest, how long before you retire, and other factors. In addition to personal factors, the nation’s economy, world economy, unemployment rate, inflation rates, interest rates, and a host of other factors that could affect your investment portfolio must be considered. People who use portfolio construction are much more involved in their investment program and are willing to invest the time and effort to build a portfolio that is more suited to their particular needs—especially when they are planning for retirement.

Choosing the Right Fund for a Retirement Account

Assume you have just secured a new job and your employer offers you the opportunity to participate in the company’s 401(k) or 403(b) retirement plan. In this situation, you must weigh at least three considerations that can affect your financial future.

Do you want to participate in the retirement account? The answer to this question is a definite yes for two reasons. The reasons are simple: Employer-sponsored retirement accounts—as explained in Chapter 14—provide a way to reduce the amount of current income tax that is withheld from your paycheck. So there are immediate tax savings. A second reason for participating in a retirement plan is because many employers will match your contributions. A common match would page 433work like this: For every $1.00 the employee contributes, the employer contributes an additional $0.50. All monies—both the employer’s and your contributions—are then invested in mutual funds that are selected by you. Note: Many employers that match place a limit on how much of the employee’s salary can be matched each year.

Which mutual funds do you want to invest in? Most retirement plans allow you to choose the mutual funds for your plan from a number of different fund options. When making your choices, keep in mind your long-term goals and the time value of money concept that was discussed in Chapter 1. The time value of money concept is especially important because the investments in your plan will grow because you (and your employer) continue to contribute money to your retirement account and quality investments should increase in value over a long period of time.

What is your stage in life? The actual choice of investments for your retirement account should be determined by your age, how long before you retire, and your tolerance for risk. Typically, younger workers choose more risk-oriented funds that have greater potential for growth over a long period of time. Older workers closer to retirement tend to choose more conservative funds with less risk.

Regardless of the type of funds you choose for your retirement plan, it is important to evaluate each fund before making your choices. The information in the “How to Make a Decision to Buy or Sell Mutual Funds” section will help you choose the right funds. Once your investment choices are made, it is important to continue to monitor each of your funds to determine if you are on the right track to achieve your financial objectives.

LO13.3

Evaluate mutual funds.

How to Make a Decision to Buy or Sell Mutual Funds

Often the decision to buy or sell shares in mutual funds is “too easy” because investors assume they do not need to evaluate these investments. Why question what the professional portfolio managers decide to do? Yet professionals do make mistakes. And sometimes, economic and financial conditions beyond the control of a fund manager cause a fund’s value to decrease. And yet, you should realize that the responsibility for choosing the right mutual fund rests with you.

page 434Fortunately, a lot of information is available to help you evaluate a specific mutual fund. To begin the search for the fund that can help you achieve your financial goals, answer one basic question: Do you want a managed fund or an index fund?

Managed Funds versus Index Funds

Most mutual funds are managed funds. In other words, there is a professional fund manager (or team of managers) who chooses the securities that are contained in the fund. The fund manager also decides when to buy and sell securities in the fund. To help evaluate a fund, you may want to determine how well a fund manager manages during both good and bad economic times. The benchmark for a good fund manager is the ability to increase share value when the economy is good and retain that value when the economy is bad. For example, most funds increased in value in the years after the recent economic crisis. Although there are exceptions, many funds provided investors with a 10, 20, or 30 percent or higher annual return. And yet the question remains whether these same funds can retain their value when there is another economic crisis. One important consideration is how long the present fund manager has been managing the fund. If a fund has performed well under its present manager over a five-year, 10-year, or longer period, there is a strong likelihood that it will continue to perform well under that manager in the future. On the other hand, if the fund has a new manager, his or her decisions may affect the performance of the fund. Managed funds may be open-end funds or closed-end funds.

Instead of investing in a managed fund, some investors choose to invest in an index fund. Why? The answer to that question is simple: Over many years, the majority of managed mutual funds fail to outperform the Standard & Poor’s 500 stock index—a common benchmark of stock market performance often reported on financial news programs. The exact statistics vary, depending on the year, but a statistic often found in mutual fund research is that the Standard & Poor’s 500 stock index outperforms 50 to 80 percent of all mutual funds.11

Because an index mutual fund is a mirror image of a specific index such as the S&P 500, the dollar value of a share in an index fund also increases when the index increases. Unfortunately, the reverse is also true. If the index goes down, the value of a share in an index fund goes down. Index funds, sometimes called “passive” funds, have managers, but they simply buy the stocks or bonds or securities contained in the index.

A second and very important reason why investors choose index funds is the lower expense ratio charged by these passively managed funds. As mentioned earlier in this chapter, the total fees charged by a mutual fund are called the expense ratio. If a fund’s expense ratio is 1.25 percent, then the fund has to earn at least that amount on its investment holdings just to break even each year. With very few exceptions, typical expense ratios for an index fund are 0.50 percent or less. And while lower fees may not sound significant, don’t be fooled. Over a long period of time, even a small difference can become huge. Although expense ratios and the effect they have on investment returns was discussed earlier in this chapter, a second example is presented in this section to reinforce this concept. Assume two different investors each invest $10,000. One investor chooses an index fund that has annual expenses of 0.20 percent; the other chooses a managed fund that has annual expenses of 1.22 percent. Both funds earn 10 percent a year. After 35 years, the index fund is worth $263,683, while the managed fund is worth $190,203. That’s a difference of $73,480. Thus, even though the two funds earned the same 10 percent a year, the difference in annual expenses made a substantial difference in the amount of money each investor had at the end of 35 years.12 Index funds may be open-end, closed-end, or exchange-traded funds.

page 435

Adapted from Huang, Nellie S., “Why Good Funds Turn Bad,” Kiplinger’s Personal Finance. Copyright © 2017 The Kiplinger Washington Editors, Inc.

What are the primary reasons why managed funds that have outperformed the market fail to maintain the same rate of return over a period of time?

This article suggests that when evaluating a fund, you should examine how a fund (and its manager[s]) performed when the market was declining or even when there is an economic crisis such as the 2008 recession. How can this suggestion help you pick a fund that will provide above average investment returns in both up and down markets?

In this chapter, we have discussed the importance of picking funds that have low fees. In your own words, describe how fees can reduce an investor’s returns.

page 436Should you choose a managed fund or an index fund? Good question. The answer depends on which managed fund you choose. If you pick a managed fund that has better performance than an index, then you made the right choice. If, on the other hand, the index (and the index fund) outperforms the managed fund—which happens as often as 50 to 80 percent of the time—an index fund is a better choice. With both investments, the key is how well you can research a specific investment alternative using the sources of information described in the remainder of this section. Read the nearby From the Pages of . . . Kiplinger’s Personal Finance feature to learn more about potential pitfalls in choosing an investment fund.

The Internet

Many investors have found a wealth of information about mutual fund investments on the internet. Basically, you can access information three ways. First, you can obtain current market values for mutual funds by using a website such as Marketwatch (www.marketwatch.com) or Yahoo! For example, the Yahoo! Finance page (finance.yahoo.com) has a box in which you can enter the symbol of the mutual fund you want to research. If you don’t know the symbol, you can enter in the name of the mutual fund in the “Quote Lookup” box. The Yahoo! Finance website will respond with the correct symbol. In addition to current market values, you can obtain a price history for a mutual fund, a profile including information about current holdings, performance data, risk, and purchase information.

Second, most investment companies that sponsor mutual funds have a web page. To obtain information, all you have to do is access an internet search engine and type in the name of the fund or enter the investment company’s internet address (URL) in your browser. Generally, statistical information about performance of individual funds, procedures for opening an account, promotional literature, and different investor services are provided. Be warned: Investment companies want you to become a shareholder. As a result, the websites for some investment companies read like a sales pitch. Read between the glowing descriptions and look at the facts before investing your money.

Finally, professional advisory services, covered in the next section, offer online research reports for mutual funds. A sample of the information available from the Morningstar website for the T. Rowe Price Value Fund is illustrated in Exhibit 13–4. Note that information about the fund symbol, net asset value (NAV), past growth information, Morningstar risk measures, and style map is provided. You can obtain even more detailed information, including fund performance, ratings, and expenses, by clicking on the links located above the net asset value.

Exhibit 13–4 Information about the T. Rowe Price Value Fund Available from the Morningstar Website

Source: Morningstar, Inc. (http://beta.morningstar.com/funds/xnas/trvlx/quote.html), accessed May 7, 2017.

In many cases, more detailed information is provided by professional advisory services such as Morningstar, Inc. (www.morningstar.com) and Value Line (www.valueline.com). While the information available on the internet is basically the same as that in the printed reports described later in this section, the ability to obtain up-to-date information quickly without having to wait for research materials to be mailed or to make a trip to the library is a real selling point.

page 437

Professional Advisory Services

As pointed out in the previous section, a number of subscription services provide detailed information on mutual funds. Morningstar, Inc. and Value Line are two widely used sources of such information. Exhibit 13–5 illustrates the type of information page 438provided by Value Line for the Oppenheimer Main Street Midcap Fund. Although the Value Line report is just one page long, it provides a wealth of information designed to help you decide if this is the right fund for you. Notice that the information is divided into various sections. At the top, overall rankings and a graph for total return contain basic information about the fund and its performance. Notice that this Oppenheimer fund is rated above average and has a five-year annualized return of 16.8 percent. The report also provides information about the fund’s holdings and historical financial information toward the middle of page. Toward the bottom, the “Management Style” section describes how the fund’s managers choose different stocks and securities to achieve the fund’s objectives.

Exhibit 13–5 Mutual Fund Research Information for the Oppenheimer Main Street Midcap Fund A Provided by Value Line.

“The Value Line Fund Advisor,” Value Line, Inc. website (http://www.valueline.com/uploadedFiles/Valueline/Tools/Special_Situations/Fund%20Advisor-July%202015.pdf) accessed May 2, 2017.

page 439

As you can see, the research information for this fund is pretty upbeat. However, Morningstar and Value Line will also tell you if a fund is a poor performer that offers poor investment potential.

In addition, various mutual fund newsletters provide financial information to subscribers for a fee. All of the professional advisory services are rather expensive, but their reports may be available from brokerage firms or libraries.

The Mutual Fund Prospectus and Annual Report

An investment company sponsoring a mutual fund must give potential investors a prospectus. You can also obtain a prospectus by accessing the investment company website, by calling a toll-free phone number, or by mail.

According to financial experts, the prospectus is usually the first piece of information investors receive, and they should read it completely before investing. Although it may look foreboding, a commonsense approach to reading a fund’s prospectus can provide valuable insights. In addition to information about the fund’s investment objective(s) and fees, the prospectus should provide the following:

A statement describing the risk factor associated with the fund.

A description of the fund’s past performance.

A statement describing the type of investments contained in the fund’s portfolio.

Information about dividends, distributions, and taxes.

Information about the fund’s management.

Information on limitations or requirements, if any, the fund must honor when choosing investments.

The process investors can use to open an account and to buy or sell shares in the fund.

A description of services provided to investors and fees for services, if any.

Information about how often the fund’s investment portfolio changes (sometimes referred to as its turnover ratio).

If you are a prospective investor, you can read a fund’s annual report by using the internet to access an investment company’s website. You can also request an annual report by calling a toll-free phone number or by mail. Once you are a shareholder, the investment company will send you an annual report. A fund’s annual report contains a letter from the president of the investment company, from the fund manager, or both. The annual report page 440also contains detailed financial information about the fund’s assets and liabilities, performance, statement of operations, and statement of changes in net assets. Next, the annual report includes a schedule of investments. Finally, the fund’s annual report should include a letter from the fund’s independent auditors that provides an opinion as to the accuracy of the fund’s financial statements.

Financial Publications and Newspapers

Investment-oriented magazines such as Bloomberg Businessweek, Forbes, Fortune, Kiplinger’s Personal Finance, and Money are excellent sources of information about mutual funds. Depending on the publication, coverage ranges from detailed articles that provide in-depth information to simple listings of which funds to buy or sell. And many investment-oriented magazines now provide information on the internet about mutual funds. The material in Exhibit 13–6 was obtained from the Kiplinger website and is a partial listing of 25 different funds that were recommended in the feature “Kiplinger’s 25 Favorite No-Load Mutual Funds.” Specific information is broken down by the type of stocks and securities in each category and includes:

Exhibit 13–6 Information about No-Load Funds Recommended by Kiplinger

“Kiplinger’s 25 Favorite No-Load Mutual Funds,” the Kiplinger website (http://www.kiplinger.com/tool/investing/T041-S000-kiplingers-25-favorite-fund/index.php), accessed March 31, 2017.

The fund name and symbol.

The fund’s one-year return.

The fund’s three-year return.

The fund’s five-year return.

The fund’s 10-year return.

The fund’s 20-year return.

The fund’s expense ratio.

In addition to mutual fund information in financial publications, a number of mutual fund guidebooks are available at your local bookstore or public library.

Although many newspapers have reduced or eliminated mutual fund coverage, many large metropolitan newspapers and The Wall Street Journal often provide news and information about funds. In addition to feature articles about selected funds, typical information about prices and financial performance includes the name of the fund family and fund name, the current net asset value for a fund, net change, and year-to-date percentage of return. Much of this same information (along with more detailed information) is also available on the internet.

page 441

LO13.4

Describe how and why mutual funds are bought and sold.

The Mechanics of a Mutual Fund Transaction

For many investors, mutual funds have become the investment of choice. In fact, you probably either own shares or know someone who owns shares in a mutual fund—they’re that popular! They may be part of a 401(k) or 403(b) retirement account, a SEP IRA, a Roth IRA, or a traditional IRA retirement account, all topics discussed in Chapter 14. They can also be owned outright in a taxable account by purchasing shares through a registered sales representative who works for a bank or brokerage firm or an investment company that sponsors a mutual fund. Although there are exceptions, most individuals invest in mutual funds to achieve long-term financial objectives. When you invest your money, you are counting on the time value of money concept to help build your nest egg. Remember that in Chapter 1 time value of money was defined as the increases in an amount of money as a result of interest earned. For example, saving or investing $2,000 instead of spending it today results in a future amount greater than $2,000. If the $2,000 is used to purchase shares in a fund, your shares can increase in value, and you can receive income from your investment that can be reinvested to purchase more shares. As you will see later in this section, it’s easy to purchase shares in a mutual fund. For $250 to $2,000 or more, you can open an account and begin investing. And there are other advantages that encourage investors to purchase shares in funds. Unfortunately, there are also disadvantages. Exhibit 13–7 summarizes the advantages and disadvantages of fund investments.

Exhibit 13–7 Advantages and Disadvantages of Investing in Mutual Funds

Advantages |

|---|

|

|

|

|

|

|

|

Disadvantages |

|

|

|

|

|

|

One advantage of any investment is the opportunity to make money on the investment. In this section, we examine how you can make money by investing in funds. We consider how taxes affect your fund investments. Then we look at the options used to purchase shares in a fund. Finally, we examine the options used to withdraw money from a fund.

Return on Investment

As with other investments, the purpose of investing in a closed-end fund, exchange-traded fund, or open-end fund is to earn a financial return. Shareholders in such funds can receive a return in one of three ways. First, all three types of funds pay income dividends. page 442Income dividends are the earnings a fund pays to shareholders from its dividend and interest income. Note: Many exchange-traded funds often pay dividends on a monthly or quarterly basis. Second, investors may receive capital gain distributions. Capital gain distributions are the payments made to a fund’s shareholders that result from the sale of securities in the fund’s portfolio. Both amounts generally are paid once a year. Note: Many exchange-traded funds may pay monthly or quarterly income dividends, but exchange-traded funds don’t usually pay end-of-the-year capital gain distributions. Third, as with stock and bond investments, you can buy shares in funds at a low price and then sell them after the price has increased. For example, assume you purchased shares in the Fidelity Stock Selector All Cap Fund at $35 per share and sold your shares two years later at $40 per share. In this case, you made $5 ($40 selling price minus $35 purchase price = $5) per share. When shares in a fund are sold, the profit that results from an increase in value is referred to as a capital gain.

Note the difference between a capital gain distribution and a capital gain. A capital gain distribution occurs when the fund distributes profits that result from the fund selling securities in the portfolio at a profit. On the other hand, a capital gain is the profit that results when you sell your shares in your mutual fund for more than you paid for them. Of course, if the price of a fund’s shares goes down between the time of your purchase and the time of sale, you incur a capital loss.

For any fund, it is possible to calculate total return and percentage of total return. To see how to calculate these amounts, read the information in the nearby Figure It Out! feature.

Taxes and Mutual Funds

Taxes on reinvested income dividends, capital gain distributions, and profits from the sale of shares can be deferred if fund investments are held in your retirement account. Assuming all qualifications are met, you can even eliminate taxes on reinvested income, capital gain distributions, and profits from the sale of shares for funds held in a Roth individual retirement account. For mutual funds held in taxable accounts, income dividends, capital gain page 443distributions, and financial gains and losses from the sale of funds are subject to taxation. At the end of each year, investment companies are required to send each shareholder a statement specifying how much he or she received in income dividends and capital gain distributions. Investment companies report amounts for dividend income and capital gain distributions on IRS Form 1099 DIV. The same information may also be reported as part of their year-end statement. The following information provides general guidelines on how mutual fund transactions are taxed when held in a taxable account:

Income dividends are reported on your federal tax return and are taxed as income.

Capital gain distributions that result from the fund selling securities in the fund’s portfolio at a profit are reported on your federal tax return. Capital gain page 444distributions are taxed as long-term capital gains, regardless of how long you own shares in the fund.13

Capital gains or losses that result from your selling shares in a mutual fund are reported on your federal tax return. How long you hold the shares determines if your gains or losses are taxed as a short-term or long-term capital gain. (See Chapter 3 for more information on capital gains and capital losses, or visit the IRS website at www.irs.gov.)

Two specific problems develop with taxation of mutual funds. First, almost all investment companies allow you to reinvest income dividends and capital gain distributions from the fund to purchase additional shares instead of receiving cash. Even though you didn’t receive cash because you chose to reinvest such distributions, they are still taxed in a taxable account and must be reported on your federal tax return as current income.

Second, when you purchase shares of stock, corporate bonds, or other securities, you decide when you sell. Thus, you can pick the tax year when you pay tax on capital gains or deduct capital losses. Mutual funds, on the other hand, buy and sell securities within the fund’s portfolio on a regular basis during any 12-month period. At the end of the year, profits that result from the mutual fund’s buying and selling activities are paid to shareholders in the form of capital gain distributions. Unlike the investments you manage, you have no control over when the mutual fund sells securities and when you will be taxed on capital gain distributions. Because capital gain distributions are taxable, one factor to consider when choosing a mutual fund is its turnover. For a mutual fund, the turnover ratio measures the percentage of a fund’s holdings that have changed or “been replaced” during a 12-month period of time. Simply put, it is a measure of a fund’s trading activity. Caution: A mutual fund with a high turnover ratio can result in higher income tax bills for the investor. A higher turnover ratio can also result in higher transaction costs and fund expenses.

To ensure having all of the documentation you need for tax reporting purposes, it is essential that you keep accurate records. The same records will help you monitor the value of your fund investments and make more intelligent decisions with regard to buying, holding, or selling these investments.

Purchase Options

You can buy shares of a closed-end fund or exchange-traded fund through a stock exchange or in the over-the-counter market. You can purchase shares of an open-end, no-load fund by contacting the investment company that manages the fund. You can purchase shares of an open-end load fund through a salesperson who is authorized to sell them, through an account executive of a brokerage firm, or directly from the investment company that sponsors the fund.

You can also purchase both no-load and load funds from mutual fund supermarkets available through most brokerage firms. A mutual fund supermarket such as Fidelity, Charles Schwab, or TD Ameritrade offers at least two advantages. First, instead of dealing with numerous investment companies that sponsor funds, you can visit one website or make one toll-free phone call to obtain information, purchase shares, and sell shares in a large number of mutual funds. Second, you receive one statement from one brokerage firm instead of receiving a statement from each investment company or brokerage firm you deal page 445with. One statement can be a real plus because it provides the information you need to monitor the value of your investments in one place and in the same format.

Because of the unique nature of open-end fund transactions, we will examine how investors buy and sell shares in this type of mutual fund. To purchase shares in an open-end mutual fund, you may use four options:

Regular account transactions.

Voluntary savings plans.

Contractual savings plans.

Reinvestment plans.

The most popular and least complicated method of purchasing shares in an open-end fund is through a regular account transaction. When you use a regular account transaction, you decide how much money you want to invest and when you want to invest, and then you simply buy as many shares as possible.

The chief advantage of the voluntary savings plans is that they often allow you to make smaller purchases than the minimum purchases required by the regular account method described above. At the time of the initial purchase, you declare an intent to make regular minimum purchases of the fund’s shares. Although there is no penalty for not making purchases, most investors feel an “obligation” to make purchases on a periodic basis, and, as pointed out throughout this text, small monthly investments are a great way to save for long-term objectives. For most voluntary savings plans, the minimum purchase ranges from $25 to $100 for each purchase after the initial investment. Funds try to make investing as easy as possible. Most offer payroll deduction plans, and many will deduct, upon proper shareholder authorization, a specified amount from a shareholder’s bank account. Also, many investors can choose voluntary savings plans as a vehicle to invest money contributed to a 401(k), 403(b), or individual retirement account. When part of a retirement plan at work, the amount used to purchase shares is often a percentage of the employee’s pay that is deducted each pay period.

Not as popular as they once were, contractual savings plans (sometimes referred to as periodic payment plans) require you to make regular purchases over a specified period of time, usually 10 to 15 years. These plans are sometimes referred to as front-end load plans because almost all of the commissions are paid in the first few years of the contract period. Also, you may incur penalties if you do not fulfill the purchase requirements. For example, if you drop out of a contractual savings plan before completing the purchase requirements, you may sacrifice the prepaid commissions. In some cases, contractual savings plans combine mutual fund shares and life insurance to make these plans more attractive. Many financial experts and government regulatory agencies are critical of contractual savings plans. As a result, the Securities and Exchange Commission and many states have imposed new rules on investment companies offering contractual savings plans.

You may also purchase shares in an open-end fund by using the fund’s reinvestment plan. A reinvestment plan is a service provided by an investment company in which income dividends and capital gain distributions are automatically reinvested to purchase additional shares of the fund. Many reinvestment plans allow shareholders to use reinvested money to purchase shares without having to pay additional sales charges or commissions. Reminder: When your dividends or capital gain distributions are reinvested in a taxable account, you must still report these transactions as taxable income.

All four purchase options allow you to buy shares over a long period of time. As a result, you can use the principle of dollar cost averaging, which was explained in Chapter 12. Dollar cost averaging allows you to average many individual purchase prices over a long period of time. This method helps you avoid the problem of buying high and selling low. With dollar cost averaging, you can make money if you sell your fund shares at a price higher than their average purchase price.

page 446

Withdrawal Options

Because closed-end funds and exchange-traded funds are listed on stock exchanges or traded in the over-the-counter market, an investor may sell shares in such a fund to another investor. Shares in an open-end fund can be sold on any business day to the investment company that sponsors the fund. In this case, the shares are redeemed at their net asset value. All you have to do is give proper notification, and the fund will send you a check. With some funds, you can even write checks to withdraw money from the fund.

In addition, most funds have provisions that allow investors with shares that have a minimum asset value (usually at least $5,000) to use four options to systematically withdraw money. First, you may withdraw a specified, fixed dollar amount each investment period until your fund has been exhausted. Normally, an investment period is three months.

A second option allows you to liquidate or “sell off” a certain number of shares each investment period. Since the net asset value of shares in a fund varies from one investment period to the next, the amount of money you receive will also vary.

A third option allows you to withdraw a fixed percentage of asset growth. If no asset growth occurs, no payment is made to you. Assuming you withdraw less than 100 percent of asset growth, your principal continues to grow.

A final option allows you to withdraw all asset growth that results from income dividends and capital gain distributions earned by the fund during an investment period. Under this option, your principal remains untouched.

page 447

page 448

Chapter Summary

LO13.1 The major reasons investors choose mutual funds are professional management and diversification. Mutual funds are also a convenient way to invest money—especially for retirement accounts. There are three types of funds: closed-end funds, exchange-traded funds, and open-end funds. A closed-end fund is a fund whose shares are issued only when the fund is organized. An exchange-traded fund (ETF) is a fund that invests in the stocks contained in a specific stock index or securities index. Both closed-end and exchange-traded funds are traded on a stock exchange or in the over-the-counter market. An open-end fund is a mutual fund whose shares are sold and redeemed by the investment company at the net asset value (NAV) at the request of investors.

Mutual funds can also be classified as A shares (commissions charged when shares are purchased), B shares (commissions charged when money is withdrawn during the first five years), and C shares (no commission to buy or sell shares but often higher, ongoing fees). Other possible fees include management fees and 12b-1 fees. Together, all the different management fees and operating costs are referred to as an expense ratio. Since it is important to keep fees and costs as low as possible, you should examine a fund’s expense ratio as one more consideration when evaluating a mutual fund.

LO13.2 The managers of funds tailor their investment portfolios to the investment objectives of their customers. The major fund categories are stock funds and bond funds. There are also funds that invest in a mix of different stocks, bonds, and other securities that include asset allocation funds, balanced funds, fund of funds, lifecycle funds, and money market funds. Today many investment companies use a family-of-funds concept, which allows shareholders to switch among funds as different funds offer more potential, financial reward, or security. It is also possible to participate in a retirement plan and choose different funds to obtain your financial objectives.

LO13.3 The responsibility for choosing the “right” mutual fund rests with you, the investor. Often, the first question investors must answer is whether they want a managed fund or an index fund. With a managed fund, a professional fund manager (or team of managers) chooses the securities that are contained in the fund. Some investors choose to invest in an index fund, because over many years, index funds have outperformed the majority of managed funds. To help evaluate different mutual funds, investors can use the information on the internet, from professional advisory services, from the fund’s prospectus and annual report, in financial publications, and in newspapers.

LO13.4 The advantages and disadvantages of mutual funds have made mutual funds the investment of choice for many investors. For $250 to $2,000 or more, you can open an account and begin investing. The shares of a closed-end fund or exchange-traded fund are bought and sold on organized stock exchanges or the over-the-counter market. The shares of an open-end fund may be purchased through a salesperson who is authorized to sell them, through an account executive of a brokerage firm, from a mutual fund supermarket, or from the investment company that sponsors the fund. The shares in an open-end fund can be sold to the investment company that sponsors the fund. Shareholders in mutual funds can receive a return in one of three ways: income dividends, capital gain distributions when the fund buys and sells securities in the fund’s portfolio at a profit, and capital gains when the shareholder sells shares in the mutual fund at a higher price than the price paid. To ensure you have all of the documentation you need for tax reporting purposes, it is essential that you keep accurate records. A number of purchase and withdrawal options are available for mutual fund investors.

page 449

Key Terms

capital gain distributions 442

contingent deferred sales load 425

exchange-traded funds (ETF) 424

Key Formulas

Page |

Topic |

Formula |

Net asset value |

|

|

Load charge |

|

|

Contingent deferred sales load |

|

|

Total return |

|

|

Percent of total return |

|

|

Withdrawal calculation |

|

Self-Test Problems

Three years ago, Mary Applegate’s mutual fund portfolio was worth $410,000. Now, the total value of her investment portfolio has decreased to $296,000. Even though she has lost a significant amount of money, she has not changed her investment holdings, which consist of either aggressive growth funds or growth funds.

How much money has Ms. Applegate lost in the last three years?

Given the above information, calculate the percentage of lost value.

What actions would you take to get your investment back in shape if you were Mary Applegate?

Twelve months ago, Gene Peterson purchased 200 shares in the no-load Fidelity Growth Company Fund—a Morningstar five-star fund that seeks capital appreciation. His rationale for choosing this fund was that he wanted a fund that was highly rated. Each share in the fund cost $128. At the end of the year, he received dividends of $0.09 and a capital gain distribution of $8.16 a share. At the end of 12 months, the shares in the fund were selling for $154.

How much did Mr. Peterson invest in this fund?

At the end of 12 months, what is the total return for this fund?

What is the percentage of total return?

page 450

Solutions

While Ms. Applegate has several options, any decision should be based on careful research and evaluation. First, she could do nothing. While she has lost a substantial portion of her investment portfolio ($114,000, or 27.8 percent), it may be time to hold on to her investments if she believes the value of her shares will increase. Second, she could sell (or exchange) some or all of her shares in the aggressive growth or growth funds and move her money into more conservative money market or government bond funds or even certificates of deposit if she thinks the economy is headed for a recession. Finally, she could buy more shares of the funds she owns or different quality funds if she believes the economy will improve in the future. Deciding which option for Ms. Applegate to take may depend on the economic conditions at the time you answer this question.

Income dividends = $0.09 Dividend per share × 200 shares = $18

Capital gain distribution = $8.16

Capital gain distribution = $8.16 × 200 shares = $1,632

Change in share value = $154 ending value − $128 beginning value = $26 a share gain

Total increase in value = $26 gain per share × 200 shares = $5,200 gain

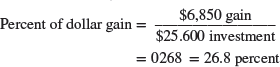

Total return = $18 Income dividends + $1,632 Capital gain distribution + $5,200 Change in share value = $6,850

Problems

The Western Capital Growth mutual fund has:

Total assets, $812,000,000

Total liabilities, $12,000,000

Total number of shares, 40,000,000

What is the fund’s net asset value (NAV)? (LO13.1)

Jan Throng invested $42,000 in the Invesco Charter mutual fund. The fund charges a commission of 5.50 percent when shares are purchased. Calculate the amount of commission Jan must pay. (LO13.1)

As Bart Brownlee approached retirement, he decided the time had come to invest some of his nest egg in a conservative fund. He chose the Franklin Utilities Fund. If he invests $30,000 and the fund charges a load of 4.25 percent when shares are purchased, what is the amount of commission Bart must pay? (LO13.1)

Mary Canfield purchased shares in the New Dimensions Global Growth Fund. This fund doesn’t charge a front-end load, but it does charge a contingent deferred sales load of 4 percent for any withdrawals during the first year. If Mary withdraws $8,000 during the first year, how much is the contingent deferred sales load? (LO13.1)

The value of Mike Jackson’s shares in the New Frontiers Technology Fund is $51,400. The management fee for this particular fund is 0.80 percent of the total asset value. Calculate the management fee Mike must pay this year. (LO13.1)

page 451Betty and James Holloway invested $71,000 in the Financial Vision Social Responsibility Fund. The management fee for this fund is 0.60 percent of the total asset value. Calculate the management fee the Holloways must pay. (LO13.1)

As part of his 401(k) retirement plan at work, Ken Lowery invests 5 percent of his salary each month in the Capital Investments Lifecycle Fund. At the end of this year, Ken’s 401(k) account has a dollar value of $210,400. If the fund charges a 12b-1 fee of 0.75 percent, what is the amount of the fee? (LO13.1)

When Jill Thompson received a large settlement from an automobile accident, she chose to invest $120,000 in the Vanguard 500 Index Fund. This fund has an expense ratio of 0.14 percent. What is the amount of the fees that Jill will pay this year? (LO13.1)

The Yamaha Aggressive Growth Fund has an expense ratio of 1.83 percent. (LO13.1)

If you invest $55,000 in this fund, what is the dollar amount of fees that you would pay this year?

Based on the information in this chapter and your own research, is this a low, average, or high expense ratio?

Jason Mathews purchased 300 shares of the Hodge & Mattox Energy Fund. Each share cost $15.15. Fifteen months later, he decided to sell his shares when the share value reached $18.10. (LO13.4)

What was the amount of his total investment?

What was the total amount Jason received when he sold his shares in the Hodge & Mattox fund?

How much profit did he make on his investment?

Three years ago, James Matheson bought 200 shares of a mutual fund for $23 a share. During the three-year period, he received total income dividends of $0.92 per share. He also received total capital gain distributions of $0.80 per share during the three-year period. At the end of three years, he sold his shares for $29 a share. What was his total return for this investment? (LO13.4)

Assume that one year ago, you bought 120 shares of a mutual fund for $33 a share, you received a capital gain distribution of $0.60 per share during the past 12 months, and the market value of the fund is now $38 a share. (LO13.4)

Calculate the total return for your $3,960 investment.

Calculate the percentage of total return for your $3,960 investment.

Over a four-year period, LaKeisha Thompson purchased shares in the Oakmark I Fund. Using the information below, answer the questions that follow. You may want to review the concept of dollar cost averaging in Chapter 12 before completing this problem. (LO13.4)

Year

Investment Amount

Price per Share

Number of Shares*

February 2014

$1,500

$45.00

February 2015

$1,500

$43.00

February 2016

$1,500

$57.00

February 2017

$1,500

$65.00

*Carry your answer to two decimal places.

At the end of four years, what is the total amount invested?

At the end of four years, what is the total number of shares purchased?

At the end of four years, what is the average cost for each share?

During one three-month period, Matt Roundtop’s mutual fund grew by $6,000. If he withdraws 40 percent of the growth, how much will he receive? (LO13.4)

|

To reinforce the content in this chapter, more problems are provided at connect.mheducation.com. |

page 452

Apply Yourself for Financial Literacy

For many investors, mutual funds have become the investment of choice. In your own words, describe why investors purchase mutual funds.

Using the internet, personal finance magazines, newspapers, or mutual fund reports, find examples of the following concepts.

The net asset value for a mutual fund.

A load fund.

A no-load fund.

The management fee for a specific fund.

A fund that charges a contingent deferred sales load.

A fund that charges a 12b-1 fee.

An expense ratio.

Using the information in this chapter, pick a type of mutual fund that you consider suitable for each of the following investors and justify your choice:

A 24-year-old single investor with a new job that pays $36,000 a year.

A single parent with two children who has just received a $400,000 inheritance, has no job, and has not worked outside the home for the past five years.

A husband and wife who are both in their mid-60s and retired.

Use the internet to obtain a prospectus for a specific mutual fund that you believe could be a quality long-term investment. As part of your evaluation of this fund, determine if there is a load charge and the procedures that can be used to buy or sell shares in the fund.

Choose the Alger International Growth Fund (symbol ALGAX), the Gabelli Asset Fund (symbol GATAX), or the Calvert Long-Term Income Fund (symbol CLDAX) and use the internet or library sources to report the type of fund, one-year return, net asset value, and Morningstar rating for the fund. Hint: You may want to use the Yahoo! Finance website at finance.yahoo.com or the MarketWatch website at marketwatch.com. Based on your research, would you invest in these funds? Explain your answer.

REAL LIFE PERSONAL FINANCE

RESEARCH INFORMATION AVAILABLE FROM VALUE LINE

This chapter stressed the importance of evaluating potential investments. Now it is your turn to try your skill at evaluating a potential investment in the Oppenheimer Main Street Midcap Fund A. Assume you could invest $10,000 in shares of this fund. To help you evaluate this potential investment, carefully examine Exhibit 13–5, which reproduces the Value Line research report for the Oppenheimer Main Street Midcap Fund A.

Questions

Based on the research provided by Value Line, would you buy shares in the Oppenheimer Main Street Midcap Fund A? Justify your answer.

What other investment information would you need to evaluate this fund? Where would you obtain this information?

On July 15, 2015, shares in the Oppenheimer Main Street Midcap Fund A were selling for $30.15 per share. Using the internet or a newspaper, determine the current price for a share of this fund. Based on this information, would your investment have been profitable? (Hint: The symbol for this fund is OPMSX.)

Assuming you purchased shares in the Oppenheimer Main Street Midcap Fund A on July 25, 2015, and based on your answer to question 3, how would you decide if you want to hold or sell your shares? Explain your answer.

page 453

Continuing Case

INVESTING IN MUTUAL FUNDS

Jamie Lee and Ross did several weeks’ worth of research trying to choose the right stock to invest in. After all, the $50,000 inheritance was a lot of money and they wanted to make the most informed investment choices they could. They discovered, by doing their homework, the various companies’ stocks that they were looking to invest in did not seem like they were going to have the promising future that Jamie Lee and Ross were hoping for. They were aware that they were taking a chance with any investment, but they were both nervous about “putting all of their eggs” in stocks and wanted to be more confident in making their investment choices. But how could they be more assured?

They decided to speak to their professional financial planner, who suggested that investing in mutual funds may be the way to lessen the risk by joining a pool of other investors in a variety, or bundle, of securities chosen by a professional mutual fund manager. This way, Jamie Lee and Ross could lessen the pressure of choosing the right company and minimize the chances of losing all of their investment money by diversifying their portfolio.