Defining What Platform Users

and Partners Can and Cannot Do

Wikipedia is a marvel of the world of platforms—an open-sourced encyclopedia that, within a few years, eclipsed traditional purveyors of information to become the most popular reference site in the world. Millions of people have come to rely upon Wikipedia as a useful, universally accessible, virtually unlimited source of data that is generally highly reliable.

Except when it isn’t. And when it isn’t, the results can be horrific.

Many users of Wikipedia will be able to point to their own favorite tale of bizarre misinformation popping up on the site. Perhaps the most famous is the entry titled “Murder of Meredith Kercher”—better known by the names of the two people widely suspected of the crime, the American student Amanda Knox and her Italian boyfriend Raffaele Sollecito. Under Wikipedia’s policy of largely open editing by any interested party, this entry has now been edited over 8,000 times by over 1,000 people—almost entirely by people who have been convinced of the guilt of Knox and Sollecito ever since the crime was committed back in 2007. Throughout their complicated legal ordeal, including one conviction, its overturning by a second court, and another conviction, these self-appointed editors continually revised the page to eliminate any potentially exculpating evidence and to emphasize the likelihood of guilt.

The controversy over the entry grew so intense that Wikipedia founder Jimmy Wales got involved. Wales studied the matter and issued a statement: “I just read the entire article from top to bottom, and I have concerns that most serious criticism of the trial from reliable sources has been excluded or presented in a negative fashion.” Shortly thereafter, he wrote, “I am concerned that, since I raised the issue, even I have been attacked as being something like a ‘conspiracy theorist.’” Perhaps most disturbing, some of the editors involved in slanting the Kercher page were found to be contributors to other websites dedicated to “hating” Amanda Knox, thereby shattering any illusion of objectivity.1

The problems Wikipedia faces in maintaining high quality while maximizing its accessibility to all the users who want to contribute to its content illustrate the challenges inherent in managing an open platform model. Yet the obvious solution—to close down the model and institute strict controls over participation—has a huge downside. Increasing the friction involved in actively using any platform inevitably reduces participation and can even destroy the value-creation potential of the platform altogether.

HOW OPEN? HOW CLOSED?:

WALKING THE TIGHTROPE

In one of the first discussions of platform openness back in 2009, two of the authors of this book (Geoffrey Parker and Marshall Van Alstyne, in collaboration with Thomas Eisenmann) provided a basic definition of openness:

A platform is “open” to the extent that (1) no restrictions are placed on participation in its development, commercialization, or use; or (2) any restrictions—for example, requirements to conform with technical standards or pay licensing fees—are reasonable and non-discriminatory, that is, they are applied uniformly to all potential platform participants.2

Being closed isn’t simply a matter of absolutely forbidding outside participants on the platform. It may also involve creating such onerous participation rules that would-be users are discouraged, or charging such excessive fees (or “rents”) that the profit margins of potential participants are reduced below sustainable levels.3 The choice between open and closed isn’t a choice between black and white; there is a spectrum between the two extremes.

Calibrating the right level of openness is undoubtedly one of the most complex as well as one of the most critical decisions that a platform business must make.4 The decision affects usage, developer participation, monetization, and regulation. It’s a challenge that Steve Jobs struggled with throughout his career. In the 1980s, he got it wrong by choosing to keep the Apple Macintosh a closed system. Competitor Microsoft opened its less elegant operating system to outside developers and licensed it to a host of computer manufacturers. The resulting flood of innovation enabled Windows to claim a share of the personal computer market that dwarfed Apple’s. In the 2000s, Jobs got the balance right: he opened the iPhone’s operating system, made iTunes available on Windows, and captured the lion’s share of the smartphone market from rivals like Nokia and Blackberry.5

Jobs liked to recast the open/closed dilemma as a choice between “fragmented” and “integrated,” terms that subtly skewed the debate in favor of a closed, controlled system. He wasn’t completely wrong: it’s true that, the more open a system becomes, the more fragmented it becomes. An open system is also more difficult for its creator to monetize, and the intellectual property that defines it is more difficult to control. Yet openness also encourages innovation.

It’s a difficult tradeoff to master. And the consequences of choosing the wrong level of openness in either direction can be severe, as the rise and fall of the social network Myspace suggests.

Although the history is now sometimes forgotten, Myspace was the dominant social network before Facebook was launched in 2004, and remained so until 2008. Even in its early days, it had much of the functionality that would be familiar to users of today’s social networks. Its internal staff created a wide variety of features, such as instant messaging, classified ads, video playback, karaoke, “self-serve advertising” easily purchased through the use of simple online menus, and more.

However, because of limited engineering resources, these features were often buggy, leading to a poor user experience.6 And an ill-considered decision to keep the site closed to outside developers made solving the problem practically impossible. Chris DeWolfe, cofounder of Myspace, recalled the company’s flawed thinking in a 2011 interview: “We tried to create every feature in the world and said, ‘O.K., we can do it, why should we [open up to] let a third party do it?’ We should have picked 5 to 10 key features that we totally focused on and let other people innovate on everything else.”

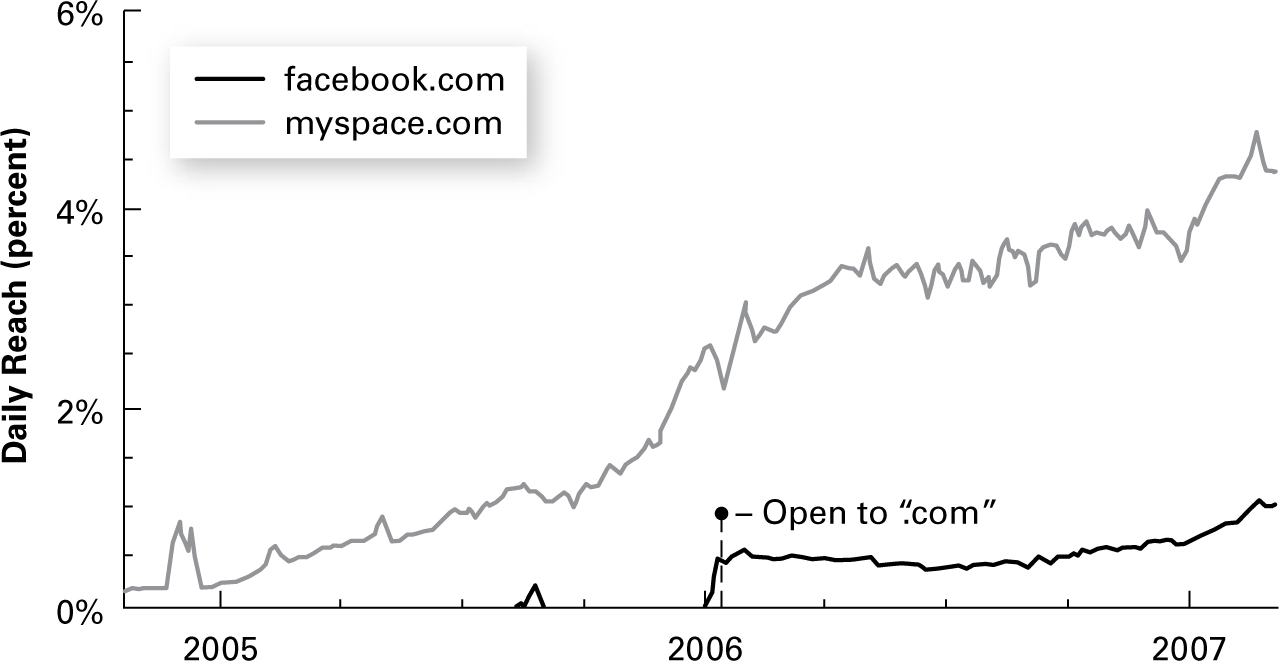

Facebook didn’t make the same mistake. Like Myspace, it was initially closed to outside innovators. It opened to dot-com users in 2006. This helped Facebook begin a slow climb toward competitiveness with Myspace. The trend is reflected in Figure 7.1, which shows the average daily reach of the two platforms in terms of percentage of Internet users during 2006 and early 2007, when Myspace was still king.

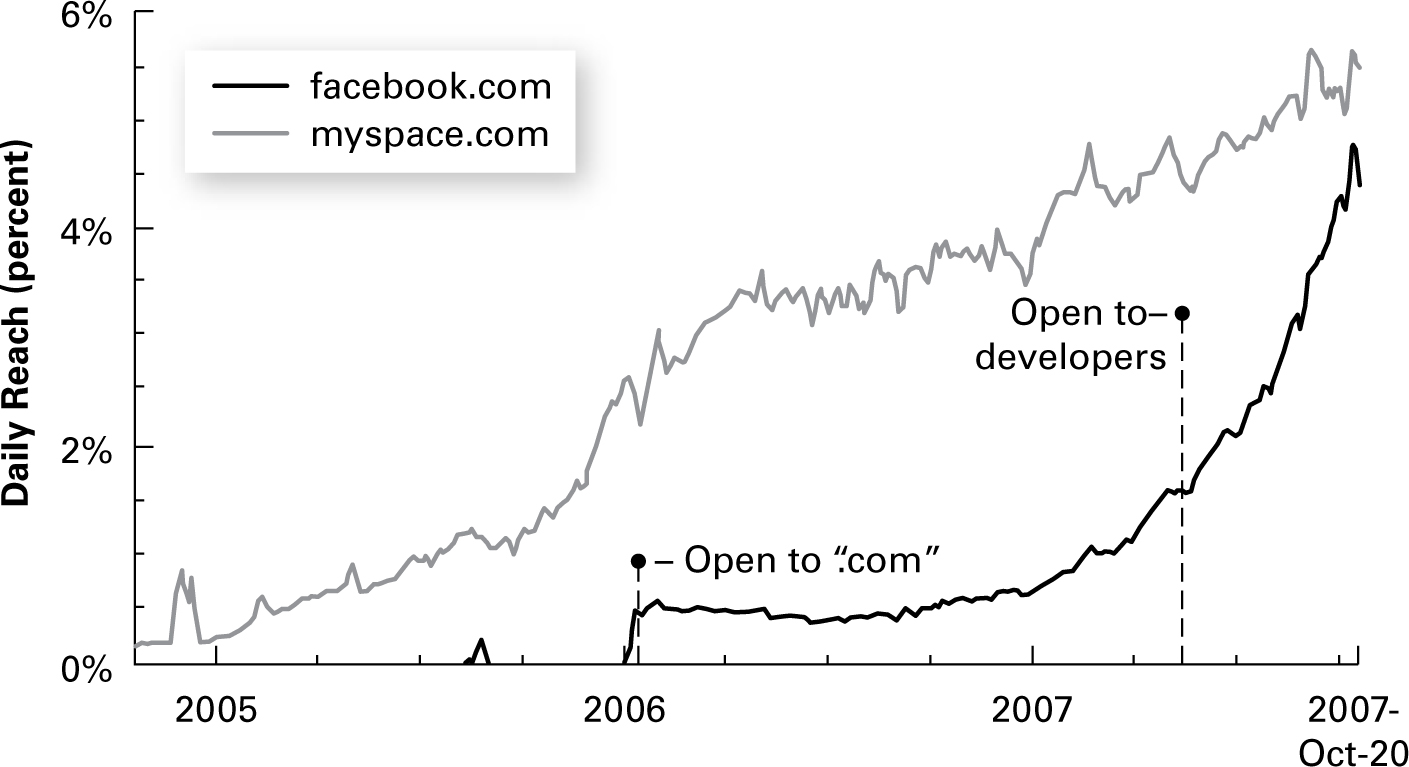

When Facebook launched Facebook Platform to help developers create apps in May 2007, the big shift began. An ecosystem of partners willing to extend the capabilities of Facebook quickly took root.7 By November 2007, there were 7,000 outside applications on the site.8 Recognizing how this flood of new apps was enhancing its rival’s appeal, Myspace responded by opening to developers in February 2008. But the tide had already turned, as shown in Figure 7.2. Facebook overtook Myspace in April 2008, and today it enjoys unquestioned supremacy in the social networking space.

FIGURE 7.1. The market dominance of Myspace over Facebook during 2006 and early 2007. © 2015, Alexa Internet (www.alexa.com).

FIGURE 7.2. Facebook rapidly overtakes Myspace after opening its platform to developers in May 2007. © 2015, Alexa Internet (www.alexa.com).

Had Myspace opened itself earlier to contributions from a wider community of outside developers—especially those who had world-class technology for specific functions that Myspace wanted to build out, such as classified advertising, an effective spam filter, and user-friendly communication tools—they might have had a more robust product offering. Perhaps today Myspace and Facebook would still be competing on an almost equal footing.

At first glance, then, it would appear that Myspace’s problems arose from precisely the opposite direction as Wikipedia’s: the collaborative encyclopedia is struggling with the consequences of too much openness, while Myspace foundered as a result of too little. That’s true to some extent—but the story is more complicated than that. Along some other important dimensions, Myspace was actually too open.

For example, Myspace’s self-serve advertising feature created an all-too-accessible pathway for a significant amount of inappropriate content, including pornography available to platform users of any age. The lack of control over such material made Myspace less attractive to many users and even triggered investigations by a number of state attorneys general. In combination with Myspace’s slowness to accommodate outside app developers, this failure to adequately curate its content helped accelerate the platform’s competitive collapse.

It might seem impossible for a platform to be both too closed and too open simultaneously, but Myspace managed the feat.

THE PLATFORM ECOSYSTEM AND THE VARIETIES OF OPENNESS

How can we make sense of the openness decisions that platform managers must make? It’s helpful to start by recalling the key elements of a platform as discussed in chapter 3. As we explained there, a platform is fundamentally an infrastructure designed to facilitate interactions among producers and consumers of value. These two basic types of participants use the platform to connect with each other and to engage in exchanges—first, an exchange of information; then, if desired, an exchange of goods or services in return for some form of currency. These participants come together on the platform to engage in a core interaction that is at the heart of the platform’s value-creating mission. In time, other kinds of interactions may be layered onto the platform, increasing its usefulness and attracting other participants.

Given this basic design, it’s axiomatic that a vibrant and healthy platform is dependent on the value created by partners who are outside of the platform itself. If a platform is too closed, then partners cannot or will not contribute the value required to make mutually rewarding exchanges possible.9

Consider Google’s YouTube. Because the system is highly open, it has become a viable outlet for commercial as well as amateur videos, delivering a wide array of content, ranging from the silly to the practical to the political and the inspirational. Without its vast array of user-supplied content, YouTube would be dependent on one or a few corporate sources of video material. Over time, it would likely evolve into more of a distribution system—similar to Hulu, for instance—than a true platform.

However, as we’ve noted, and as the examples of Wikipedia and Myspace illustrate, openness is not a black-or-white area. Decisions about degrees and kinds of openness are critical and often challenging.

There are three kinds of openness decisions that platform designers and managers need to grapple with. These are:

• Decisions regarding manager and sponsor participation

• Decisions regarding developer participation

• Decisions regarding user participation

Each type of decision has unique ramifications and implications. Let’s consider them in turn.

MANAGER AND SPONSOR PARTICIPATION

Behind any platform, with responsibility for its structure and operation, are two entities: the firm that manages the platform and directly touches users, and the firm that sponsors the platform and retains legal control over the technology. In many cases, these two entities are one and the same. Companies like Facebook, Uber, eBay, Airbnb, Alibaba, and many others are both platform managers and platform sponsors. In this situation, control of the platform, including decisions about openness, rests completely with the manager/sponsor firm.

In other cases, however, the platform manager and the platform sponsor are not identical. In general terms, the platform manager organizes and controls producer/consumer interactions, while the platform sponsor controls the overall architecture of the platform, the intellectual property that underlies the platform (such as the software code that controls its operations), and the allocation of other rights. When the manager and the sponsor are separate, the manager is closest to the customer/producer relationship as well as to outside developers who may contribute to the platform. This gives the manager considerable influence over the daily operations of the platform. But, in general, the sponsor has greater legal and economic control over the platform and therefore a larger measure of power over its long-term strategy.

In some cases, both the platform manager and the platform sponsor can be either a single company or a group of companies—with further implications for issues of control and openness.10

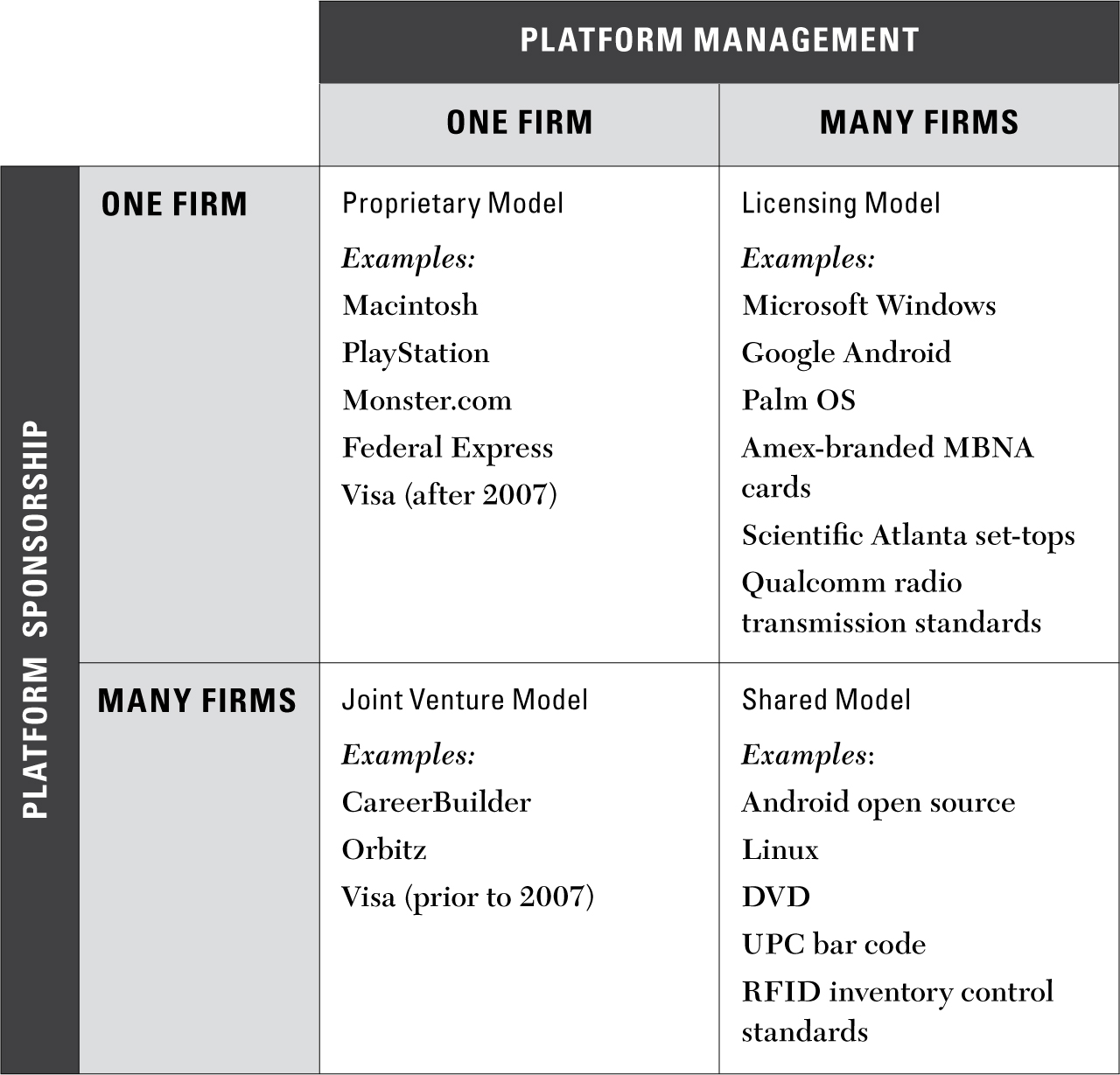

Figure 7.3 illustrates four models for managing and sponsoring platforms. In some cases, a single firm both manages and sponsors the platform. We call this the proprietary model. For example, the hardware, software, and underlying technical standards for the Macintosh operating system and mobile iOS are all controlled by Apple.

Sometimes a group of firms manages the platform while one firm sponsors it. This is the licensing model. Google, for example, sponsors the “stock” Android operating system, but it encourages a number of hardware firms to supply devices that connect consumers to the platform. These device makers, including Samsung, Sony, LG, Motorola, Huawei, and Amazon, are licensed by Google to manage the interface between producers and consumers.

FIGURE 7.3. Four models for managing and sponsoring platforms. Adapted from “Opening Platforms: How, When and Why,” by Thomas Eisenmann, Geoffrey Parker, and Marshall Van Alstyne.11

In still other cases, a single firm manages the platform while a group of firms sponsors it—the joint venture model. The Orbitz travel reservations platform was launched in 2001 as a joint venture sponsored by a collection of major airlines in order to compete with upstart Travelocity. Similarly, the job search platform CareerBuilder was created jointly in 1995 (under the original name of NetStart) by three newspaper groups as a platform for help-wanted advertising.

Finally, in some cases, a group of firms manages the platform while another group sponsors it—the shared model. For example, there are both many sponsors and many managers of the open source Linux operating system, which, like the Mac and iOS systems, serves as a platform connecting app developers and other producers to millions of consumers. Corporate sponsors of Linux include IBM, Intel, HP, Fujitsu, NEC, Oracle, Samsung, and many other companies, while the manager companies include dozens of device makers—TiVo, Roomba, Ubuntu, Qualcomm, and many others.

Sometimes, a particular platform may migrate from one model to another as business demands and the structure of the marketplace evolve. Consider, for example, the Visa credit card operation, which is a platform that permits merchants and consumers to engage in payment transactions with one another. It originated in 1958 as a proprietary platform under the name of BankAmericard, sponsored and managed by the Bank of America. In the 1970s, it took on the Visa brand name and morphed into a joint venture, independently managed while being sponsored by a number of banks. In 2007, Visa became a freestanding corporate entity and reverted to the proprietary model. It is now self-sponsoring rather than being supported by an outside institution.

As you can see, these four models of manager and sponsor participation are, in effect, variant patterns of openness. The proprietary model provides the greatest control and facilitates the most closed system of operation, as exemplified by Apple’s management of the Mac operating system. The licensing and joint venture models are, in effect, open at one end and closed on the other, while the shared model, exemplified by Linux, leads to a platform that is open to both a wide array of sponsors and a wide array of managers.

Who wins? Who loses? Which of these four models is most advantageous to platform sponsors? Which works best for platform managers? Which model generates the greatest flow of predictable, controllable profits? It would be nice to offer definitive, one-size-fits-all answers to these questions—but, as is usually the case in business, the answer is, “It depends.”

The proprietary model, used with enormous success by Apple, might seem to be every platform company’s dream. After all, it allows you to capture an entire market and to realize all the profits it generates. The logical way to accomplish this is by developing a new technology standard and maintaining sole control of it. And this is not impossible—but in the real world, it doesn’t always produce lasting economic returns.

A classic illustration is the so-called VCR war of the 1970s and 1980s, which pitted two technology platforms against each other: the Betamax videotape standard sponsored by Sony, and the VHS standard sponsored by JVC. Unlike most platforms of today, these standards from the pre-Internet era did not create an online venue in which producers and consumers could meet to conduct interactions together. However, they qualified as platforms because they established technology systems that would allow multiple producers (chiefly movie and TV studios) to sell products to consumers. Thus, they faced many of the same kinds of strategic challenges that today’s Internet-based platforms must confront.

From a technical quality standpoint, the Betamax platform was slightly better, providing sharper images and longer recording times. But the outcome of the war was decided by the varying sponsorship/management strategies chosen by the rivals.

Sony chose the proprietary platform model, retaining control of the Betamax standard on the theory that, in the long run, its better quality would win out in the marketplace. But that never happened. JVC followed the licensing model, enlisting many manufacturers to produce VHS recorders and players. As manufacturing volume increased, prices fell, making VHS devices more attractive to consumers. With more device makers supporting the VHS standard and with more consumers owning VHS players, movie studios and other content providers issued more products in VHS format than in Betamax. A feedback loop set in that gave VHS a large, steadily growing advantage over Betamax. By the mid-1980s, manufacturers that embraced the VHS standard came to dominate the VCR arena. Ironically, however, JVC itself enjoyed only modest profits from this victory; its development of the original VHS standard didn’t lead to a large or lasting stream of income.

Years later, Sony became embroiled in a new format war with a different outcome—though one that proved to be no more satisfactory in the long run to the Japanese giant. In the mid-2000s, when videotape gave way to digital video discs (DVDs), Sony’s Blu-ray high-definition video standard competed against the HD-DVD standard pioneered by Toshiba. Sony decided to pursue the same sole proprietorship model it had chosen for Betamax. In this case, Sony won the battle, thanks largely to its successful introduction of the PlayStation 3 gaming device, which included Blu-ray video and made it instantly available to millions of consumers.

Unfortunately for Sony, this victory proved short-lived. Today, a few years after the triumph of Blu-ray, the migration of consumers away from DVD to streaming video is well under way, making Bluray’s dominance increasingly irrelevant. The lesson? If, like Sony, you choose to fight a standards battle in quest of proprietary control of a market, you’d better win it—and win it fast, before the next big thing supersedes the very technology you seek to dominate.

The story of Visa—another platform that originated in the pre-digital era—illustrates some of the other challenges faced by different management and sponsorship models. During its years of sponsorship by a consortium of big banks, Visa achieved significant success as a leading credit card company. But over time, this management model proved cumbersome. When a platform is sponsored—and therefore owned—by a number of companies, key decisions must be approved by a committee of owners with varying goals and preferences, which is an inherently inefficient management system. This is why Visa’s owners ultimately agreed to spin off the business as a self-contained entity, granting it the capability to make competitive moves more nimbly.

The inherent awkwardness of multi-sponsor decision-making can affect the elegance, simplicity, and ease of use of technology. The long history of the personal computer wars between Apple’s proprietary model and Microsoft’s so-called Wintel standard clearly illustrates the fact that a standard controlled by a single company with a unified esthetic and technical vision can produce more attractive, intuitive tools and services than a collection of competing companies, each with its own design approach. Apple has also become far more profitable and valuable than any single company in the Wintel universe—despite the fact that its market share of computer sales has never approached that of the PC.

Similarly, Apple’s iPhone is generally considered more elegant and user-friendly than any smartphone created using Google’s less tightly controlled Android standard. This is particularly so today, with the Android Open Source Platform (AOSP) permitting experimentation and change by any interested company. AOSP is the platform used by Amazon in its Kindle Fire and by China’s Xiaomi in its mobile phones.

This doesn’t mean that Apple’s proprietary iPhone strategy is necessarily “better” than Google’s more open strategy. In fact, the story is a complicated one. Even though Apple’s iPhone continues to be a more elegant device than competing Android phones, by 2014, open innovation by multiple phone manufacturers had earned Android about 80 percent of the smartphone market, as compared with just 15 percent for Apple.12

A big win for Google? Not really. The AOSP operating system doesn’t automatically channel user traffic to Google’s online services—which means that Google, despite being the progenitor of Android, receives no revenue or data flow from AOSP devices. In response, Google has reversed course and closed Android in an effort to reassert its control over the system.13 (We’ll return to this story later in the chapter.)

In the end, of course, the choice of a sponsorship/management model comes down to the purposes for which the platform is being developed and the goals of those designing it. The wireless radio frequency identification (RFID) technology is used to create smart tags that can be attached by the millions to products for inventory control. In effect, the RFID system is an inventory management platform that retailers can access to interact with the goods they distribute.

The RFID platform was sponsored by a huge consortium of retailers, and the tags themselves are now manufactured by many companies which compete on the basis of price as well as design. The shared model of sponsorship and management means that the RFID technology itself doesn’t generate enormous profits for anyone—the tags sell for just a few cents apiece. But this suits the sponsors perfectly, since their goal all along was to make the technology as simple, accessible, and affordable as possible.

DEVELOPER PARTICIPATION

As you’ve seen, designing and building a platform generally starts with a core interaction. But over time, many platforms expand to include other kinds of interactions that create additional value for users and attract new kinds of participants. These new interactions are created by developers who may be afforded more or less open access to the platform and its infrastructure. We refer to the three kinds of developers as core developers, extension developers, and data aggregators.

Core developers create the core platform functions that provide value to platform participants. These developers are generally employed by the platform management company itself. Their main job is to get the platform into the hands of users and to deliver value through tools and rules that make the core interaction easy and mutually satisfying.

Core developers are responsible for basic platform capabilities. Airbnb provides an infrastructure that allows guests and hosts to interact with each other using system resources, including the search capabilities and data services that allow guests to find attractive properties as well as the payment mechanisms necessary to conclude a transaction. In addition, Airbnb manages behind-the-scenes functions that reduce transaction costs for guests and hosts. For example, the platform provides default insurance contracts for both parties, protecting guests in the event of accident or crime and protecting hosts from negligent guest behavior (though, as we’ll discuss in chapter 11, this insurance coverage is not without its shortcomings). It also verifies the identity of participants in order to make its reputation system a meaningful measure of user behavior. Designing, fine-tuning, maintaining, and continually improving systems like these are all elements of the work of Airbnb’s core developers.

Extension developers add features and value to the platform and enhance its functionality. They are normally outside parties, not employed by the platform management firm, who find ways to extract a portion of the value they create and thereby profit from the benefits they offer. A familiar group of extension developers is the individuals and companies that produce apps sold via the iTunes store—games, information and productivity tools, activity enhancers, and so on. One of the crucial decisions a platform manager must make—and often reconsider as the market evolves—is the extent to which the platform will be open to extension developers.

A number of extension developers have enhanced the value of the Airbnb platform. For example, Airbnb’s own research reveals that properties listed with professional-quality photographs are viewed by prospective renters twice as often as those with lower-quality images. In response, an extension developer now offers professional support under the rubric of “Airbnb photography service” to create compelling images that should make an Airbnb host more successful.

Extension developer Pillow (formerly known as Airenvy) supports hosts on the platform by providing tools to simplify property listing, guest checkin, and cleaning and linen delivery. Other developers, including Urban Bellhop and Guesthop, make travel arrangements for guests, such as dining reservations and babysitting services. With the assistance of outside firms, an Airbnb host can offer a suite of services that compares to those provided by a full-service hotel.

In order to facilitate this extension of its platform’s functionality, Airbnb must open its business to participation by these extension developers. But calibrating its degree of openness is a challenge for Airbnb. If the platform is too closed—if it is too onerous for extension developers to hawk their wares on the site—it will lose the opportunity to provide valuable extra services to platform users, perhaps alienating participants in the process. But if the platform is too open—if it is too easy for extension developers to appear on the site—then it’s likely that poor-quality service providers will join the platform, tarnishing the reputation of the other developers as well as that of Airbnb itself. Furthermore, excessive openness may lead to too many providers of the same type of service, which will reduce the profit earned by any one provider and reduce the incentive to extension developers to customize services for Airbnb users.

Platforms that choose to encourage extension developers by granting a high degree of openness will usually create an application programming interface. This is one of the control points that a platform manager can use to manage open access to its system. An application programming interface (API) is a standardized set of routines, protocols, and tools for building software applications that makes it easy for an outside programmer to write code that will connect seamlessly with the platform infrastructure.

Currently, although Airbnb has developed an API, it is not generally available to all developers that wish to connect to the platform—an indication of the middle way the platform managers want to tread when it comes to developer participation.

Some companies erect steep barriers against extension developers not just to protect the quality of platform content but also in an effort to retain control of the revenue streams their platforms generate. We’ve already seen how this strategy backfired on Myspace. Today, a similar fate may be hitting Keurig, the popular maker of coffee machines—which, for this purpose, may be viewed as a platform dedicated to brewing hot beverages. We’ll consider Keurig’s story in chapter 8.

The Guardian, a British daily newspaper, has gone in the opposite direction. The paper’s website enjoys significant international readership and has always been open to users, who are free to read its content, as written and edited by the newspaper’s staff. However, the site was formerly closed to extension developers. Recognizing the value of the Guardian’s vast trove of information and ideas, and the potential benefit to be derived from transforming the paper’s website into an open platform, the company’s management went through a months-long strategic exercise in which they discussed and analyzed the implications of such a shift. Having studied both the possible risks and the likely rewards, the Guardian’s managers decided both to “open in” the website, by bringing in more data and applications from the outside, and to “open out” the site, by enabling partners to create products using Guardian content and services on other digital platforms.

To work toward the “open out” goal, the Guardian created a set of APIs that made its content easily available to external parties. These interfaces include three different levels of access. The lowest access tier, which the paper calls Keyless, allows anyone to use Guardian headlines, metadata, and information architecture (that is, the software and design elements that structure Guardian data and make it easier to access, analyze, and use) without requesting permission and without any requirement to share revenues that might be generated. The second access tier, Approved, allows registered developers to reprint entire Guardian articles, with certain time and usage restrictions. Advertising revenues are shared between the newspaper and the developers. The third and highest access tier, Bespoke, is a customized support package that provides unlimited use of Guardian content—for a fee.

Some of the first products released under the Guardian’s new open platform model include a Content API, which provides access to over a million articles; a Politics API, which provides election results and candidate information; a Data Store, which provides access to data sets and visualizations, ranging from a table of country-by-country laws and practices regarding the death penalty to a colorful graph depicting all of the time-travel journeys of TV sci-fi hero Doctor Who; and an App Framework, which facilitates app development, aimed at making the system easy to experiment with and build applications for. In response, over 2,000 extension developers signed up in the first twelve months.

The power of APIs to attract extension developers and the value they can create is enormous. Compare the financial results experienced by two major retailers: traditional giant Walmart and online platform Amazon. Amazon has some thirty-three open APIs as well as over 300 API “mashups” (i.e., combination tools that span two or more APIs), enabling e-commerce, cloud computing, messaging, search engine optimization, and payments. By contrast, Walmart has just one API, an e-commerce tool.14 Partly as a result of this difference, Amazon’s stock market capitalization exceeded that of Walmart for the first time in June 2015, reflecting Wall Street’s bullish view of Amazon’s future growth prospects.15

Other platform businesses have reaped similar benefits from their APIs. Cloud computing and computer services platform Salesforce generates 50 percent of its revenues through APIs, while for travel platform Expedia, the figure is 90 percent.16

The third category of developers who add value to the interactions on a platform are data aggregators. Data aggregators enhance the matching function of the platform by adding data from multiple sources. Under license from the platform manager, they “vacuum up” data about platform users and the interactions they engage in, which they generally resell to other companies for purposes such as advertising placement. The platform that is the source of the data shares a portion of the profits generated.

When the services provided by data aggregators are well designed, they can match platform users with producers whose goods and services are interesting and potentially valuable to them. For example, if a Facebook user has been posting information about plans for a vacation in France, a data aggregator might sell that data to an advertising agency that, in turn, would generate messages about Paris hotels, tour guides, discount airfares, and other topics likely to be of interest.

Data aggregation is now practiced by many kinds of businesses, both on and off digital platforms. When it works well, it produces results that consumers experience as seamless and even delightful: “How did they know I’ve been looking for kitchen tiles in exactly that shade of blue!” But when it is ham-fisted—as is too often the case—the results feel intrusive and sometimes creepy.

A story—possibly apocryphal—recounted by Charles Duhigg in the New York Times describes the angry father of a teenage girl marching into a Target store to ask why his daughter had been receiving coupons for baby products. “Are you trying to encourage her to get pregnant?” he demanded. The store manager apologized, but when he called the family to discuss the matter a few days later, the father was embarrassed and apologetic. “I had a talk with my daughter,” he said. “She’s due in August.”

How did Target “know” about the girl’s pregnancy before her family did? Duhigg describes Target’s system for analyzing customer behaviors in an effort to anticipate future needs and purchasing activities. Thus, when a (hypothetical) female consumer visits her local Target store and buys cocoa butter lotion, a diaper bag–sized purse, zinc and magnesium supplements, and a bright blue rug, Target’s algorithm calculates an 83 percent chance that she is pregnant. Cue the coupons for baby clothes.17

Perhaps for obvious reasons, data aggregation systems such as these are little discussed by the platform businesses that provide them access. Knowing the degree to which their personal behavior is being monitored makes many consumers queasy. Because data aggregation is a large and growing source of revenue for platform companies, managing it appropriately poses an enormous ethical, legal, and business challenge. We’ll delve into this topic in more detail in chapters 8 and 11, which deal with platform governance and regulation.

WHAT TO OPEN AND WHAT TO OWN

As we’ve seen, innovations that are valuable to platform users can come from many sources. Some are created by core developers and therefore are owned and controlled by the platform company itself. Others are created by extension developers and therefore are owned and controlled by outside businesses. This raises the question: when does the power of an outside developer threaten that of the platform itself? And when this happens, how should the platform manager respond?

The answer to these questions depends on the amount of value created by a particular extension app. If you are a platform manager, you don’t want to let an outside firm control a primary source of user value on your platform. When this happens, you need to move to take control of the value-creating app—most often by buying the app or the company that created it. On the other hand, when an extension app adds a modest amount of additional value, then it’s perfectly safe and generally very efficient to allow the outside developer to retain control of it.

Consider, for example, the ownership and control decisions Apple has made in regard to its mobile phone operating system. Apple has been careful to own most of the applications that come preloaded with the iPhone, such as music playing, photography, and voice recording. It bought SRI International, the company that developed the technology behind the iPhone’s “virtual personal assistant,” Siri.18 All of these are all-high-value-adding features with significant impact on the market for the iPhone, which is why Apple is eager to own and control them.

By contrast, YouTube is content to own its video distribution and playing technology while leaving control of the millions of video clips available on the platform in the hands of the people and organizations that uploaded them. One might assume that globally popular videos like the Korean pop hit “Gangnam Style” generate significant value for YouTube consumers. But that value is ephemeral (this year’s favorite video is quickly displaced by next year’s) and represents just a tiny fraction of the total value of YouTube’s video content. In a case like this, the platform owner has no need to own or control the individual element of value.

There are two other principles that platform managers should consider when weighing whether an extension app represents a threat to their economic power.

First, if a particular app has the potential to become a powerful platform in its own right, the manager of the platform that hosts the app should seek to own it—or to replace it with an app controlled by the platform itself.

In 2012, Google Maps had become the premier provider of mapping services and location data for mobile phone users. It was a popular feature on Apple’s iPhone. However, with more consumer activity moving to mobile devices and becoming increasingly integrated with location data, Apple realized that Google Maps was becoming a significant threat to the long-term profitability of its mobile platform. There was a real possibility that Google could make its mapping technology into a separate platform, offering valuable customer connections and geographic data to merchants, and siphoning this potential revenue source away from Apple.

Apple’s decision to create its own mapping app to compete with Google Maps made sound strategic sense—despite the fact that the initial service was so poorly designed that it caused Apple significant public embarrassment. The new app misclassified nurseries as airports and cities as hospitals, suggested driving routes that passed over open water (your car had better float!), and even stranded unwary travelers in an Australian desert a full seventy kilometers from the town they expected to find there. iPhone users erupted in howls of protest, the media had a field day lampooning Apple’s misstep, and CEO Tim Cook had to issue a public apology.19 Apple accepted the bad publicity, likely reasoning that it could quickly improve its mapping service to an acceptable quality level—and this is essentially what has happened. The iPhone platform is no longer dependent on Google for mapping technology, and Apple has control over the mapping application as a source of significant value.

Second, if particular functionality is reinvented by a number of extension developers and gains widespread acceptance by platform users, the manager of the platform should acquire the functionality and make it available through an open API. Widely useful functions such as video and audio playback, photo editing, text cutting-and-pasting, and voice commands have often been invented by extension developers. Recognizing their broad applicability, platform managers have moved to standardize these functions and incorporate them into APIs that all developers can use. This accelerates innovation and enables improvements in service for everyone who uses the platform.

USER PARTICIPATION

The third kind of openness that platform managers need to control is user participation—in particular, producer openness, which is the right to freely add content to the platform. Remember, many platforms are designed to facilitate side switching, which enables consumers to become producers, and vice versa; so the same individual users who consume value units on the platform can also create value units for others to consume. YouTube users can both view others’ videos and upload videos of their own; Airbnb guests can become hosts; Etsy customers can sell their own craft products on the site.

The platform’s objective in opening to these users is to facilitate the creation and provision of as much high-quality content as possible. Of course, this stipulation—that the objective is the development of high-quality content—is the reason most platforms reject absolute openness as a strategy for managing user participation.

When it was launched, Wikipedia aspired to a condition of complete openness. Maintenance of quality would be entrusted solely to the users of the platform, who would take it upon themselves to monitor the content of the site, fix errors, and challenge biases.

This was a utopian vision that assumed good intentions on the part of all Wikipedia users; or, a trifle less idealistically, it assumed that the varying, sometimes conflicting motivations and attitudes of users would eventually balance one another, producing content that represented the combined wisdom of the entire community, much as, in capitalist theory, the “invisible hand” of the market is supposed to maximize the benefits for all through the interaction of countless self-interested participants.

However, reality teaches us that democracy—like free markets—can be messy, especially when intense passions and partisanship are involved. Hence the episode we recounted at the start of this chapter, in which the Wikipedia article about the death of Meredith Kercher was hijacked by “haters” of Amanda Knox who were determined to make sure the page should assert her guilt and were prepared to eradicate any signs of dissension.

The Kercher killing is not the only instance in which Wikipedia is embroiled in controversy—far from it. An article on the platform headed “Wikipedia: List of controversial issues” lists over 800 topics that “are constantly being re-edited in a circular manner, or are otherwise the focus of edit warring or article sanctions.” Organized under headings that include “Politics and economics,” “History,” “Science, biology, and health,” “Philosophy,” and “Media and culture,” they include everything from “Anarchism,” “Genocide denial,” “Occupy Wall Street,” and “Apollo moon landing hoax accusations” to “Hare Krishna,” “Chiropractic,” “SeaWorld,” and “Disco music.”

Limiting openness through artful curation. How can Wikipedia establish high standards for the quality of the platform’s content when some of its users are determined to manipulate it for their own purposes? That is not easy. Those who manage the platform try hard to rely primarily on community standards and social pressure. Guidelines are promulgated through articles like “Wikipedia: five pillars,” which explains one of the platform’s “fundamental principles” this way:

Wikipedia is written from a neutral point of view: We strive for articles that document and explain the major points of view, giving due weight with respect to their prominence in an impartial tone. We avoid advocacy and we characterize information and issues rather than debate them. In some areas there may be just one well-recognized point of view; in others, we describe multiple points of view, presenting each accurately and in context rather than as “the truth” or “the best view”. All articles must strive for verifiable accuracy, citing reliable, authoritative sources, especially when the topic is controversial or is on living persons. Editors’ personal experiences, interpretations, or opinions do not belong.

Yet there are times when community pressure is not enough. When the quality of particular articles is repeatedly degraded by biased or dishonest content, other methods and tools for protecting Wikipedia’s integrity kick in. These include VandalProof, a software program written especially for Wikipedia that highlights articles edited by users with a track record of unreliable work; tagging tools that draw attention to potentially problematic articles so that other editors can review and, if necessary, improve them; and a range of blocking and protection systems that can only be employed by users who have earned special privileges through the general consensus of the Wikipedia community.

This complex, largely self-organized set of interlocking systems for ensuring the quality of Wikipedia content is a form of curation—the crucial content protection process that must be fine-tuned to ensure the right degree and kind of producer openness.

Curation usually takes the form of screening and feedback at critical points of access to the platform. Screening decides who to let in, while feedback encourages desirable behavior on the part of those who have been granted entry. A user’s reputation, as shaped by past behavior both on and off the platform, is usually a key factor in curation: users rated positively by the rest of the community are more likely to pass through the screening process and to receive favorable feedback than those with poor reputations.

Curation can be managed through human gatekeepers—moderators who personally screen users, edit content, and provide feedback designed to promote quality. Media platforms such as blogs and online magazines often use this kind of system. But employing moderators who are trained and paid by the platform company is time-consuming and costly. A better system—though one that can be challenging to design and implement—relies on users themselves to curate the platform, generally through software tools that quickly gather and aggregate feedback and apply it to curation decisions.

As we’ve seen, user-driven curation facilitated by software tools is the method Wikipedia employs. Similarly, Facebook relies on users to flag objectionable content such as hate speech, harassment, offensively graphic images, and threats of violence. Service platforms like Uber and Airbnb incorporate user ratings into their software tools so consumers and producers can make informed choices about whom they choose to interact with.

No system of curation is foolproof. When curation tools err on the side of openness, potentially offensive or even dangerous content can slip through. When the tools are overly restrictive, valuable users and appropriate content may be screened out or discouraged—as when social networking algorithms intended to eliminate pornography end up blocking educational materials on topics like breast cancer awareness. Platform managers need to devote significant time and resources—including human eyeballs and informed judgment—to continually monitoring their platforms’ boundaries between openness and closedness and ensuring they are set appropriately.

SIMILAR PLATFORMS CAN COMPETE THROUGH DIFFERING LEVELS OF OPENNESS

Platforms that operate in similar arenas may choose to differentiate themselves by adapting different levels and kinds of openness. These variant openness regimes will attract different kinds and numbers of participants, generate distinct ecosystem cultures, and may ultimately produce divergent business models.

As we’ve previously observed, two platforms that made very different openness decisions are Apple’s Mac operating system/hardware combination and Microsoft’s Windows operating system in the 1980s and 1990s. Although some critics describe Windows as a closed system, by comparison to Apple it has been much more open. Apple made the decision to charge extension developers a relatively high $10,000 for system development kits (SDKs), thereby ensuring a small, select pool of outside software developers. Microsoft, by contrast, basically gave the developer SDKs away and consequently attracted a much larger developer pool.

Meanwhile, IBM lost control of the hardware standard, partly as the result of regulatory action, making it possible for any manufacturer to enter the PC market, which drove costs rapidly down. The combination of a large developer pool with inexpensive hardware was compelling to consumers, and the so-called Wintel platform dominated the market for nearly twenty years—while the share of the industry enjoyed by the closed Apple system steadily dwindled. In this case, it seems clear that the open path was far more successful than the closed path.

More recently, as we’ve seen, Google and Apple made differing openness decisions regarding their mobile platforms. Google allowed the development of an open-source version of Android, which is freely available to any manufacturer, while Apple sponsored the proprietary iOS operating system and tightly controlled the hardware so that it is the sole device provider and therefore the sole manager of the system.

At first, this might look like a repeat of the Microsoft/Apple PC operating system battle. However, although Apple is much more closed than Google—for example, retaining control of the vital device manufacturing function rather than opening it to other companies—it is more open than it was in the previous technological generation. Having opened its system just enough to encourage developers, Apple now assists them with strong developer toolkits and gives them access to its user base through the iTunes store. A multitude of apps has appeared as a result.

Google, meanwhile, needed to be more open because it entered the market after Apple. As a result, AOSP quickly grew beyond Google’s control, prompting Google to seek to restrict access to its platform through a variety of mechanisms. Because the underlying operating system is free to all, Google cannot easily close AOSP, but almost the same goal can be achieved by exerting control over critical functions. Journalist Ron Amadeo has described how Google closed the Android applications for functions such as search, music, calendar, keyboard, and camera, while also working hard to encourage handset manufacturers to join its so-called open handset alliance, dedicated to developing and maintaining open software and hardware standards for mobile devices. Amadeo explains the impact of Google’s move toward closing AOSP on extension developers:

If you use any Google APIs and try to run your app on a Kindle, or any other non-Google version of AOSP: surprise! Your app is broken. Google’s Android is a very high percentage of the Android market, and developers only really care about making their app easily, making it work well, and reaching a wide audience. Google APIs accomplish all that, with the side effect that your app is now dependent on the device having a Google Apps license.20

By requiring a license to access Google Play, the official app store for AOSP, the firm is able to control access to the platform even though the underlying technology is open source. In this way, Google can manage potential competition as well as ensure a more orderly technology environment for users and developers.

Stories like these illustrate the complicated competitive factors that impact openness decisions—as well as the never-ending balancing act that platform sponsors and managers need to practice to ensure that their platforms remain relevant, vibrant, and valuable to a growing base of users.

OPENING OVER TIME:

THE BENEFITS AND THE RISKS

As we’ve seen, platforms can expand and develop stronger network effects by opening out over time. More rarely, as in the case of Android, they can choose to become more closed over time.

The choice to become more open or more closed depends on whether a platform was originally structured as a proprietary or shared platform. Naturally, a proprietary platform, which is sponsored, managed, and completely controlled by a single company, can only become more open. By contrast, a fully open, shared platform (Linux, for example) can only become more closed.

As we noted in chapter 5, which deals with launching a platform, a new platform will often choose to execute virtually all of its processes internally simply because there are no partners willing to make the necessary investment. In these cases, employees must provide both content and curation. Over time, as the platform grows and outside developers are attracted, the openness pattern may change, which means that curation processes need to evolve as well.

A forward-looking platform management team must design ways to continually evaluate the platform’s openness level. Preferably, the platform will use a consistent strategic framework to make decisions for opening over time. Eventually, as the maturing platform moves processes outside the firm from employees to partners, it may need to develop algorithms to automate curation or to decentralize curation to the entire base of users. YouTube now depends upon its large user base to evaluate content, provide feedback, and flag content that should not be on the platform.

As the platform’s openness policies evolve, the challenge is always to find balance. If a platform is too closed—for example, if it extracts excessive rents in the form of unreasonable and arbitrary fees—its partners may refuse to make platform-specific investments. On the other hand, platforms face trouble when extension developers begin to insert themselves too aggressively between the platform and its users. If a particular developer successfully displaces other competitors, a platform manager should be careful to ensure that the developer does not seek to displace the platform itself.

There are a number of examples of such struggles for control of a particular platform’s user base. Consider SAP, the German-based multinational giant that produces software for large enterprises to use in managing their internal operations, customer relationships, and other processes. SAP, which operates a large business processes platform, has partnered with the U.S.-based firm ADP to provide payroll processing services to its users, partly in order to take advantage of ADP’s superior access to cloud computing capabilities. However, ADP has substantial customer relationships of its own and can serve as the platform host linking customers to a number of data/computing/storage partners. Thus, the partnership creates an opportunity for ADP to displace SAP as the primary manager of the customer relationship. This is an instance in which the platform manager (SAP) is in danger of losing control of the customer connection to an extension developer (ADP).

The unique power and value of the platform lies in its ability to facilitate connections among participants from outside the platform itself. But defining exactly who should have access to the platform and precisely how they can participate is an enormously complex issue with ever-changing strategic implications. That’s why the question of openness needs to be at the top of every platform manager’s agenda—not just during the initial design process, but throughout the life of the platform.

TAKEAWAYS FROM CHAPTER SEVEN

There are three kinds of openness decisions that managers face: those regarding manager/sponsor participation, developer participation, and user participation.

There are three kinds of openness decisions that managers face: those regarding manager/sponsor participation, developer participation, and user participation.

Management and sponsorship of a platform may be controlled by a single firm, by different firms, or by groups of firms. The four possible combinations lead to differing patterns of openness and control, with various advantages and disadvantages.

The open/closed dichotomy isn’t black or white. There are shades of gray, and benefits and drawbacks to every point on the spectrum. Sometimes, similar platforms choose to compete on the basis of differing openness policies.

Maturing platforms often evolve in the direction of greater openness. This demands continually reevaluating and adjusting curation processes to ensure consistently high quality of platform content and service value.