4

Getting Uncle Sam to Play Fair with Medicare

Health care is the prime concern for most Americans in their prime of life. An illness or injury requiring medical attention can easily wipe out a life’s savings. Health insurance is an absolute must. But the cost of basic private coverage is out of reach for most older Americans. The Government’s answer is Medicare—federal health insurance available at age 65, which offers truly invaluable Golden Opportunities.

Unfortunately, your “friends” in Washington don’t play fair; they have transformed your Medicare program into a complex game and have stacked the deck against you. The rules are so confusing that even Uncle Sam doesn’t always understand them. And if that weren’t bad enough, the politicians keep reshuffling the playing cards to create “new and improved” versions of the game. Then they bury the rules you need to successfully compete.

Enough is enough. In the pages that follow we explain why the Medicare Monopoly Game was created; what the real Golden Rules are; and how you can WIN! The secrecy and mystery surrounding Medicare is about to come to an end!

THE TRUTH (ALMOST) BEHIND WHY MEDICARE DOESN’T CARE ABOUT YOU

One of the best-kept secrets of all time is the “real” reason why our Government created Medicare. In 1965, when President Lyndon B. Johnson signed the legislation for this program, Americans were told that the purpose of Medicare was to provide basic national health insurance for seniors. Phooey. That story was simply a cover-up. What you are about to read has never before been revealed to the public: the secret goal of the Medicare program. Be forewarned, the truth might shock you.

In the late 1950s, census studies showed that the American population was rapidly graying. The implications were grave. Too many seniors with too much leisure time spelled trouble. What if all these competent retirees decided to become political activists? Congress panicked. The prospect of being monitored by thousands of seniors was frightening.

A solution was needed that would keep America’s seniors so busy they wouldn’t have any energy left to pester Congress. In a flash of skin-saving genius, our legislators found the perfect answer: Congress gave America Medicare. We were told the program was designed with our best interests at heart. But Congress never intended to create a workable health-care safety net. What our legislators wanted was a time-consuming national “hobby” for seniors. Now you know the “truth.”

When President Johnson signed on the dotted line, what our citizens actually received was the rule book for the largest group activity ever created—the great Medicare Monopoly Game. (If you doubt the credibility of this theory, consider the following: Had Medicare truly been intended to provide you with health-care protection, don’t you think it would work just a little better?)

The concept behind Medicare Monopoly is brilliant. Here are some of the game’s key features:

1. Portable components—No matter where you travel in the United States, you will always be able to find playing pieces (stop in at any friendly Social Security office).

2. Socialization benefits—Swap Medicare war stories with others in any doctor’s waiting room. A common rapport is immediate.

3. All-season use—So, outside it’s too cold? Too hot? No sweat. You will never be at a loss for something to do. Interpreting and sorting denied claims is good for hours of activity.

4. Promotes family ties—If you are at a loss for ideas that will bring your relatives together, you can always invite them to Medicare Monopoly parties to develop new strategies for getting claims paid.

And you thought Medicare was a health insurance program!

WHEEL OF MISFORTUNE: LEARNING HOW TO PLAY MEDICARE MONOPOLY

Now that you know the “why” behind Medicare, you need to develop a fresh strategy for dealing with the system. You must learn how to play the game.

To win any game of chance, a player needs a combination of luck, nerve, and timing. Playing Medicare Monopoly is no different in this regard. Some aspects of the game you will have control over, like making sure information on a claim is accurate; some you won’t, like choosing the date and severity of an illness. But the key is knowledge. You would never think of going to Las Vegas, plunking down hundreds of dollars at the blackjack table, and playing, without ever bothering to learn the rules of the game. Yet when it comes to Medicare, that’s exactly what most people do. They toss the dice, shut their eyes, and hope the right numbers come up so the medical bills can get paid. People keep playing until their pockets are empty and there is nothing left to lose.

This is a tragedy, but it doesn’t have to happen to you. When you play Medicare Monopoly, don’t just keep picking the “Take a Chance” cards. There are rules of the game; if you know them, and turn them to your favor, you can improve your odds of opening the Community Chest of valuable benefits.

As you prepare to play, keep two important principles in mind:

• Medicare is not charity. You have earned your right to Medicare through the Social Security taxes that were deducted from your or your spouse’s salary. Remember when you looked at your paycheck and saw that big gap between gross and net income? Well, some of that hard-earned money should finally reappear in the form of Medicare benefits. When you play Medicare Monopoly, you’re playing to win your own funds.

• Medicare is confusing. No, you are not senile or stupid because you can’t understand all the ins and outs of the program. Medicare is a red-tape nightmare. (What did you expect when politicians, government bureaucrats, hospitals, doctors, and insurance companies all have a say in spending over $100 billion in taxpayer money!) Take heart—there is nothing wrong with your mind. To ask for help in battling the bureaucracy is not an admission of stupidity. Whether you have a high school diploma or three Ph.D.s, you will find dealing with Medicare exasperating because it often defies logic. Perseverance (not brains) is key for a successful game of Medicare Monopoly.

Preparing to Play

The official rules for playing Medicare Monopoly can be found in The Medicare Handbook, published annually by the U.S. Department of Health and Human Services. But as anyone who has used this guide knows, the instructions for playing are unclear at best. (Let’s face it, Uncle Sam wants to win the game, so he’s not anxious to reveal where the aces are hidden.) Don’t despair, this chapter will help even the odds.

The Medicare Handbook, despite its flaws, is still an essential game piece. Since the Handbook is updated every year to reflect changes in the program, make sure you have the latest edition. Medicare automatically provides the first copy when you enroll, but after that, staying current is up to you. If you have misplaced your Handbook, or if it’s outdated, get another. Call or visit your Social Security Office or local Office on Aging.

The Medicare Handbook should always be your starting point for explanations about Medicare coverage. Before wasting any time on the phone with Medicare personnel, refer to this guide. Uncle Sam just might have something to say on the subject. Scan the Table of Contents and the Medicare Ready Reference Chart at the very beginning of the guide. If you have a simple question, such as “What is the phone number to call when reporting Medicare fraud?” chances are you will find the answer.

It’s dealing with any issue beyond the realm of the most simple that can cause problems. The fine print of Medicare coverage, supposedly provided in the Handbook, can be so fine that it’s nonexistent. If you want to find out the Government’s “secret rules,” this chapter is just what the doctor ordered.

Armed with the newest Medicare Handbook in one hand and this book in the other, you will be ready to play Medicare Monopoly, set to pass go, and collect the treasure you are entitled to receive under Medicare law.

Begin at the Beginning

“Begin at the beginning … and go on till you come to the end” is the wise advice the King of Hearts offers Alice during her journey through Wonderland. Since we are not ones to tamper with sound suggestions, that’s exactly where we will begin our discussion of the Medicare Monopoly Game: at the beginning.

When we talk about Medicare, we’re referring to the federal health insurance program for people 65 or older and certain disabled people. It is run by the Health Care Financing Administration of the U.S. Department of Health and Human Services. Your local Social Security Administration office has the job of taking applications and answering questions about eligibility and basic benefits of the program. (Medicare carriers and intermediaries are responsible for handling your specific questions about claims.)

Health Insurance Card

Uncle Sam will give you a card identifying you as an official Medicare Monopoly player. Everyone calls this card the “Medicare Card.” It makes sense. The name is clear and simple. Even The Medicare Handbook refers to this document as the “Medicare Card.” Nevertheless, Uncle Sam actually has chosen another name as the official title: the “Health Insurance Card.” So don’t be surprised when the card you receive has “Health Insurance,” not “Medicare,” written in bold letters.

Your Medicare card is as unique as your fingerprint. You are assigned a health insurance claim number (Medicare number) that has nine digits (your Social Security number) and one letter (sometimes two letters), and it belongs to you alone. The only way the bureaucracy recognizes your existence as legitimate is by the identification information on the card. For this reason, always:

• Carry your Medicare card with you.

• Write your health insurance claim number on any documents or forms you send to Medicare.

• Replace a lost card immediately (call Social Security).

• Use your own card. Never use anyone else’s claim number, even your spouse’s. You are asking for a paperwork nightmare if you do.

The Medicare program has two parts: Hospital Insurance (Part A) and Medical Insurance (Part B). The highlights of both are summarized in Table 4.1. Table 4.2 shows the costs of health care services that will be shared between you and Medicare.

Medicare hospital (Part A) and medical (Part B) insurance are wonderful benefits—the rich rewards for winning Medicare Monopoly. But as we’ve said, Uncle Sam doesn’t want to make it too easy for you. So he’s written the rule book in Medicarese.

Medicarese

Medicarese is the mode of communication used by the folks at Medicare. It looks like English, but it’s not. The unique feature of this language is that it was created for the sole purpose of promoting secrecy and misunderstanding. (You’ve heard of legalese—well this is worse!)

Obviously, you can’t play a winning game of anything when the rules are not written in plain English. You’ve got to learn at least the basics of Medicarese vocabulary. The Government’s Medicare Handbook provides a Glossary of Medicare Related Terms (written, of course, in Medicarese). You will find it buried at the back of the Handbook. We have taken the liberty of translating the key Medicarese terms from this list into people-friendly language. Mr. Webster might not approve of our style, but he probably never had to read a Medicare document, either!

Defined here are certain words and phrases central to understanding both Parts A and B of the Medicare program. These VIPs (Very Important Phrases) deserve VIP attention because you can’t play Medicare Monopoly without them.

Medicare VIP Glossary

Approved Charge. This is the dollar amount that Medicare has decided is an appropriate fee for a provider’s service. Medicare uses a complex formula to arrive at this figure. The approved charge is like a price ceiling. Medicare generally won’t pay more than 80 percent of its approved charge for a service, no matter what the provider bills you. Don’t be confused—just because Medicare “approves a charge” does not mean Uncle Sam will pay 100 percent of the bill.

TABLE 4.1

Basics of the Medicare Program

Hospital Insurance—Part A

What Is Covered?

As you will see, Medicare’s use of the term “covered” is a gross overstatement. There are lots of limitations, but here is the basic list:

1. Inpatient hospital care

2. Inpatient Skilled Nursing Facility (SNF) Care

3. Home health care

4. Hospice care

Who Is Eligible?

At 65, you are entitled to receive Part A benefits based on your (or your spouse’s) employment record. Most people are covered.

What Are the Costs?

Part A is “free” (no premiums are required), but you must pay all deductibles ($652 in 1992) and co-insurance (a percentage of the bill for the care or service received—no small potatoes).

Medical Insurance—Part B

What Is Covered?

The following kinds of care and services fall under the Medicare Part B umbrella of coverage:

1. Doctor care

2. Outpatient hospital care

3. Diagnostic testing

4. Durable Medical Equipment (DME)

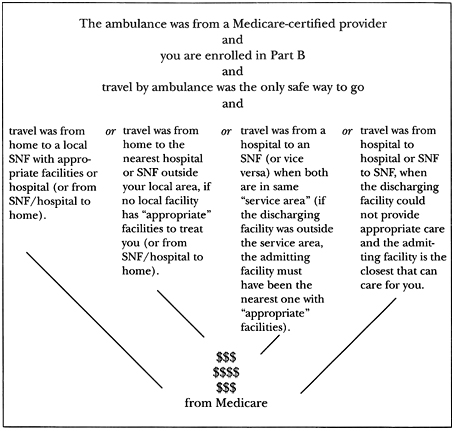

5. Ambulance travel

6. Various other services and supplies not included under Part A

See the Medicare Handbook under Medicare Medical Insurance (Part B) for an official summary.

At first glance, the range of care and services covered looks impressive. Don’t be fooled. When your first rainy day arrives, you will discover many leaks in your Part B umbrella of coverage.

Who Is Eligible?

Basically, anyone (65 or older) who wants to pay.

What Are the Costs?

You pay a monthly premium, plus deductibles and co-insurance. In 1992, the Part B premium is $31.80 a month and the annual deductible is $100.

TABLE 4.2

Health Care Payments Under Medicare

Assignment. This is perhaps the most misunderstood term in the Medicare VIP Glossary; it applies to Part B medical insurance. Understanding assignment is essential for playing the Medicare Monopoly game.

Assignment is a three-way agreement among you, Medicare, and a service provider (e.g., a doctor) to share the costs of your medical treatment. Here’s how the deal works:

• The provider agrees to accept the Medicare approved charge as total payment for a service.

• Medicare then pays its share (usually 80%) of that approved amount (less any unmet deductible) directly to the provider.

• To complete the triangle, you must pay your share (20% co-insurance for most services) of the approved charge to the provider (plus any unmet deductible).

A provider who accepts assignment accepts as payment in full the amount Medicare has approved as a reasonable charge for this service, even if his normal fee would be higher. The provider is not agreeing to accept Medicare’s check for 80 percent of the bill as payment in full. When a doctor accepts assignment you still must pay your 20 percent co-insurance; you don’t get off the hook. Unfortunately, a sign in a doctor’s office that reads “I accept assignment” is not a ticket to free medical care!

Benefit Period. This is Medicare’s way of measuring your use of Part A covered services. It is the period of time during a spell of illness when the care you receive is eligible for Medicare reimbursement. Maximum benefit periods are listed in Table 4.2; a spell of illness is defined below.

Co-insurance (or Co-payment). This is the amount you must pay after Medicare pays its share of the bill for Medicare approved services and supplies. Both Parts A and B can require you to pay co-insurance.

Under Part A, you get 60 days in a hospital or 20 days in a skilled nursing home absolutely free (after paying your deductible). Once you have exceeded the free day limit, you and Medicare will share the costs. Your portion is called co-insurance.

Under Part B, if the provider accepts assignment, Medicare pays 80 percent of the cost and you (or your private supplemental insurance) pay 20 percent (your co-insurance). Remember, assignment means you will not have to pay more than the Medicare approved charge for a service; it does not mean Medicare picks up the entire bill.

When a provider does not accept assignment, expect to pay more. Since the provider is not agreeing to use Medicare’s price lid on his fee, you will owe the 20 percent co-insurance (based on Medicare’s approved charge) plus all of the “unreasonable” charges for a service (any amount the doctor bills above Medicare’s approved charge) up to 120 percent of the Medicare approved amount. (Some states limit fees charged by providers even more.)

Deductible. This is a fee you must pay before Medicare will begin to pay for any of your hospital or medical expenses. In 1992, the Part A deductible (for each benefit period) is $652 and the Part B annual deductible is the first $100 in approved charges (see Table 4.2) and can be met by any Medicare-covered expenses over the course of a year. You must meet your Part A deductible each time you are admitted to the hospital or skilled nursing facility (SNF) if more than 60 days has passed since your last hospital or SNF stay. Medicare will keep a running tally and will deny payment until you hit the mark. It’s a good idea for you to keep track of your expenses too, so you can make sure you aren’t wrongfully denied benefits once the deductible is satisfied.

Reasonable and medically necessary. Medicare pays for “covered” services, but only if the services are also “reasonable and medically necessary.” Unfortunately, this vague language allows the Government to unfairly deny all sorts of claims.

It’s probably safe to say that no one really knows for sure what this term means, and Medicare likes it that way. What appears perfectly “reasonable” to you or us may not look that way to the Medicare claim processor who just happened to wake up on the wrong side of the bed the day your claim passed through. However, here’s a “reasonable” way of applying this slippery standard: Had a panel of doctors been convened to review your case, would the majority agree that your doctor’s plan for care:

• Was based on sound medical practice?

• Was a safe and effective choice of treatment?

• Gave consideration to your entire physical and mental condition?

If so, the service in question should be considered “reasonable and medically necessary.”

GEM: When You Choose, You Lose

In the vague world of “reasonable and necessary,” there is a very important, clear-cut no-no. When you exercise your freedom of choice and opt for nonessential care, Uncle Sam will exercise his veto power.

GEM: Be an Exception to the Rule

Your claim may be unfairly denied because the treatment you received is usually considered unreasonable and unnecessary. But the circumstances of your case might make you “exceptional” and, by law, Medicare must evaluate your claim based on the unique aspects of your total condition. If your claim is denied and you believe it’s unfair because Medicare didn’t notice that you were special, ask for a review. Have your doctor write and explain why the service was reasonable and necessary, and refile the claim. There’s a good chance Medicare will see it your way this time. (For details on how to file an appeal, see Chapter 5.)

EXAMPLE 1

Your doctor tells you that a cyst must be removed. He says he can fix you up in the office. But you’d feel better if the treatment is done in a hospital, so you ask to have it done there.

Get out your checkbook. If necessary treatment can be done on an outpatient basis but you opt to check into the hospital, you’ll have to pay yourself.

EXAMPLE 2

You might think a face-lift is essential to your well-being, but don’t expect Uncle Sam to agree. You will pay the price for beauty, as well as for any other procedure that is not essential for preserving your health.

* * *

Spell of Illness. You may receive Medicare benefits only during a spell of illness. A spell of illness begins when a patient is admitted to a hospital or skilled nursing facility and ends when the patient has not received hospital or skilled care for 60 consecutive days.

The Medicare Timer

When you play Medicare Monopoly, you’ll play Part A against a Medicare timer. Uncle Sam sets the timer when you go into the hospital or skilled nursing facility, and when your timer runs out—buzzzz, you lose. You can start the timer again for each new spell of illness.

The Medicare timer starts running when you start a benefit period, which is the time during which you can get Medicare Part A coverage. For example, for each Medicare hospital insurance benefit period, after meeting your deductible, you are eligible for 60 “free days” of coverage (you actually pay the deductible on the first day and then you pay no co-insurance for the next 59 days) plus 30 “shared” cost days (you must pay co-insurance—see Table 4.2 for amounts). These 90 days (free and shared) are “renewable”; when you begin a new spell of illness, the timer is reset for 90 days. You also have 60 “reserve days” you can draw on over your life, but these are not renewable. You still must pay co-insurance for each day, and once lifetime reserve days are used up, they are gone forever. Example 3 shows how this works:

EXAMPLE 3

Your husband first enters a hospital on April 15. He is there three days, and pays his deductible. When he reenters on May 1, all costs are paid by Medicare right from the start. The Medicare timer began running from the day he paid his deductible.

After 60 days in the hospital (combining both visits), you start sharing the costs. The sharing continues for 30 days. Then the timer runs out. Now you have a choice: you start using your 60 reserve days or you pay out of your own pocket.

EXAMPLE 4

Same facts as Example 3, except your husband’s prior hospitalization was February 15 to 18. When he reenters on May 1, he must pay his deductible ($652) again, even though he paid the deductible once already this year, because he is in a new spell of illness—he has been out of the hospital for more than 60 consecutive days. But the good news is he gets a new benefit period—60 new free days and 30 new shared-cost days.

How Does Medicare Calculate a Benefit Period?

The Medicare payment timer starts ticking on the first day you enter a hospital. Each free day is like one second on a stopwatch, and when the hands on the Medicare stopwatch reach 60, your full coverage days are over. You must begin paying co-insurance for the next 30 days of care.

How Do You Get a New Benefit Period?

Again, the stopwatch analogy applies. You can begin a new benefit period with each new spell of illness, after you have been out of the hospital (or SNF) for 60 days in a row. The day of discharge will count as your first day out.

There is no limit to the total number of benefit periods you can have, either in a year or in your life. If you are out of the hospital for 60 consecutive days, the timer goes back to zero and you are given a new benefit period (60 free days followed by 30 shared cost days). At the start of each new benefit period, you pay a deductible.

GEM: Play the Numbers

As you can see, you are playing a “60s” number game: You want to stay out of a hospital for 60 consecutive days, and because Medicare limits the number of free hospital days to 60 for each benefit period, your other goal is to avoid exceeding that magic number. Obviously, you don’t always have a choice, but sometimes you do. See Examples 5 and 6.

EXAMPLE 5

You require two complex nonemergency surgical procedures and extended hospitalization will be needed. Speak to your doctor about separating the treatments. By reentering the hospital after 60 days back home, you will be entitled to reset the Medicare timer for 60 more free days. Although you must pay a deductible again, it will still cost you less than the daily co-payments that you would have paid beginning on Day 61 of your long hospitalization. You and your doctor will need to consider all the medical and financial circumstances.

EXAMPLE 6

You are being treated for a chronic illness. You are hospitalized for 10 days, home for 20, then rehospitalized for 3 days and home for 15. If you keep this up, you will soon deplete your free days. So do whatever you can, without jeopardizing your health, to stay home for 60 days (e.g., arrange for home health care services). Then you can enter a new benefit period and gain new free days.

* * *

How Does Medicare Calculate a Day?

Sounds like a dumb question. A day is a day, right? Wrong. Medicare views a day in a different way from how you or we would. Since your coverage is based on calculating inpatient service days, it’s essential that you know how Uncle Sam defines a day. A Medicare day begins at midnight. (Not surprisingly, those bureaucrats chose the darkest hour as the starting point for a Medicare day!)

Any part of a day you are in a hospital or skilled nursing facility (including the day of admission) counts as one inpatient day. Your day of discharge does not count as an inpatient service day and will not be counted against you. To remember which days count, a quote from Shakespeare comes in handy (is it possible he had trouble with Medicare too?), “Life’s but a walking shadow, a poor [emphasis added] player that struts and frets his hour upon the stage, and then is heard no more; it is a tale told by an idiot, full of sound and fury, signifying nothing.” (Macbeth, Act V).

The day you depart does not count—it “signifies nothing.”

GEM: Avoid Late Charges

If you choose to stay in your room after normal checkout time for reasons of comfort or convenience, you will be responsible for any late charges, and the day will count even if you depart later that day. But if the delay is due to circumstances beyond your control (e.g., a morning treatment you were scheduled for was delayed, or the ambulance service does not to pick you up on time), then Medicare should cover any late charges, and your late departure should not be counted against you as another inpatient day.

GEM: Count Medicare Days

Double-check the dates of your admission and release on the hospital bill to make sure they are correct. When you are mistakenly billed for extra days, not only does it cost big bucks but it will also cause your Medicare game timer to run out early!

Also, keep watch on your Medicare timer to avoid unpleasant billing surprises later. You can’t count on Medicare or the hospital to watch out for you.

GEM: Watch Out for Unpaid Deductibles

Uncle Sam doesn’t play fair in starting the Medicare timer. Let’s say you are admitted to the hospital and this is your first illness. You have not yet met your Part A deductible. Even though you will be footing the bill until you have paid off your deductible, the Medicare timer does not go on hold. It will still begin ticking on the day you entered and will count toward your 60 free days.

* * *

When Should You Use Reserve Days?

You, or someone acting for you, can decide at any time during a hospital stay whether or not to dip into your 60 nonrenewable reserve days. You can use these only once, and when they’re gone—that’s it! So use them wisely.

A hospital should notify you, at least five days before you have used up your 90 days of coverage, that you have the option to begin drawing on reserve days for the remainder of your stay. You will receive a form to sign to start taking reserve days. The reserve-day withdrawals will begin the day after your signed notice is filed and will remain in effect unless it is revoked.

GEM: Recapture Lost Reserve Days

Your decision to use reserve days is not cut in stone—at least not immediately. If you change your mind after leaving the hospital, you can recapture reserve days if both:

• You notify the hospital within 90 days of discharge that you will pay back all costs for services not covered by insurance.

• The hospital agrees.

You can even recapture lost reserve days after 90 days if your expenses will be paid by a third party (insurance company) and the hospital agrees. See Example 7.

EXAMPLE 7

More than three months after leaving the hospital, you decide that you’ve made a mistake by using reserve days. You’ve discovered that your supplemental insurance will cover your hospital care after the first 90 days. Now you would like to recapture your reserve days.

Even though it’s been longer than 90 days since your discharge, don’t give up. Contact the hospital’s billing department and ask if you can file a retroactive request not to use reserve days. If the hospital agrees, Medicare will be reimbursed and your private health insurance company will be billed for the additional care.

GEM: Deal Yourself into the Game

Uncle Sam stacks the cards against you. Thanks to a “Joker” in the deck, the Medicare Monopoly Game may prevent you from getting necessary treatment. Why? Providers can only find out whether a service is covered by Medicare after they’ve given you the care. So if it’s not a sure bet that Medicare will foot the bill, then chances are they won’t take a gamble on treating you.

The trick is to convince the hospital, skilled nursing facility, or home health agency to provide service. How? If you can afford to pay in case Medicare denies the claim, say so. If you can’t afford the cost, become a squeaky wheel: badger the provider to take a chance. A provider who hasn’t filed many wrong claims may still get paid by Medicare even if it turns out that the service isn’t really eligible for coverage.

MEDICARE HOSPITAL INSURANCE (PART A)

Now that you know the general rules of Medicare Monopoly, you’re almost ready to play. We first look at Hospital Coverage (Part A), and then discuss Medical Coverage (Part B). By the time you’re through, you should be able to give Uncle Sam a good run for your money.

Medicare Part A is the hospital, skilled nursing facility, and home health insurance that Uncle Sam provides when you turn 65. You can get Medicare Part A premium-free if you are eligible to receive Social Security retirement or survivor benefits (Chapters 1 and 2) or Railroad Retirement benefits (Chapter 13).

GEM: Take Medicare Even If You Delay Other Benefits

If you are eligible but choose not to file for retirement or survivor benefits yet, you are still entitled to receive Medicare at age 65. Don’t pass up this freebie—delaying Medicare serves no purpose.

GEM: Get Medicare Even If You Are Not Eligible for Free Coverage

At age 65, if you are a U.S. citizen or have been a permanent resident for five years, you can still enroll in Part A, even if you are not eligible for Medicare based on Social Security or Railroad eligibility. You will pay a monthly premium ($192 a month in 1992), but it is often worth the price. Contact your local Social Security office for enrollment information and an application.

GEM: Get Medicare Before Age 65!

You can start taking Part A Medicare if you have received Social Security or Railroad disability benefits for at least 24 months (see here, here). Don’t miss out on this valuable gem!

GEM: Government Employees Can Now Cash In

Until recently, federal, state, and local government employees were not eligible to receive Medicare benefits. State and local government employees hired before April 1, 1986, are probably still not Medicare qualified. But the rules have been broadened, and if you are now paying for Medicare hospital insurance (Part A) as part of your FICA tax, you should be considered Medicare qualified at age 65.

The rules covering government employees are very confusing. Have the folks at Social Security check your and your spouse’s employment record to determine if you are eligible. If you are told you are not qualified, request a specific explanation so you can double-check with a Medicare lawyer or someone familiar with the employee benefits where you work. Don’t take one person’s word as gospel. Mistakes are made.

* * *

Enrollment

Application for Medicare Part A can be a hassle. Thankfully, most people don’t have to apply. If you are 65 and will be receiving Social Security or Railroad Retirement benefits, you can escape the filing process. You are automatically enrolled as soon as you start taking these other government benefits.

EXAMPLE 8

You are turning 65 and starting to collect Social Security. Don’t worry about Medicare application forms—you are automatically enrolled in Part A (you will also get Part B unless you choose to decline the opportunity and opt out).

EXAMPLE 9

At age 65, you were still working and didn’t apply for Social Security at that time. Now, at age 67, you are retiring. Your Social Security application automatically triggers your Medicare enrollment.

Individuals who take early Social Security retirement benefits will be enrolled automatically at age 65. If you opt to continue working after age 65, and delay receiving Social Security benefits, you can still start Medicare at 65, but you’ll have to apply—it won’t come automatically. You’ll also have to apply (at any age) to get Medicare benefits after receiving Social Security disability benefits for 24 months. Table 4.3 shows how this works.

If you qualify for automatic enrollment, your Medicare card should arrive in the mail. (If a card doesn’t appear in your mailbox by two weeks before your birthday, contact Social Security.) When you are Medicare eligible because of disability, your card will also come automatically. If you qualify at age 65, your card will be good for both Parts A and B. If you don’t want Part B, you will need to follow the instructions and notify Uncle Sam.

TABLE 4.3

Work Status and Enrollment

If you do not meet the automatic enrollment requirements, paperwork unfortunately will be necessary. Call or visit your local Social Security office to obtain an application. Be prepared to provide the following information:

1. Age. Don’t try fooling Uncle Sam; you need to submit proof—a birth certificate, hospital records, or some other documentation.

2. Social Security Number. If it’s lost, Uncle Sam has ways to track it down.

3. Income for the Previous Year. A W-2 form or copy of income tax return. Don’t worry, you won’t be audited.

4. Government Benefits. A list of any benefits you are entitled to receive (e.g., Federal Civil Service, Railroad Retirement).

GEM: Timing Is Everything

If you don’t qualify for automatic enrollment, sign up for Medicare Part A three months before your 65th birthday. Don’t procrastinate; delays could cost you. If you become ill and incur expenses before obtaining coverage, you may get stuck for all the medical bills. In addition, if you don’t apply promptly for Part B, you will pay a higher premium as a penalty for late enrollment, and your Part B coverage may be delayed a year or longer. Table 4.4 shows when to apply for Medicare.

TABLE 4.4

When to Apply for Medicare

If Your Birthday Is |

|

Apply for Medicare in |

|

||

January 2*–February 1 |

|

October |

February 2–March 1 |

|

November |

March 2–April 1 |

|

December |

April 2–May 1 |

|

January |

May 2–June 1 |

|

February |

June 2–July 1 |

|

March |

July 2–August 1 |

|

April |

August 2–September 1 |

|

May |

September 2–October 1 |

|

June |

October 2–November 1 |

|

July |

November 2–December 1 |

|

August |

December 2–January 1 |

|

September |

|

||

*Note: We will explain why we start with the second day of each month on here.

EXAMPLE 10

You have just turned 65. Although you are eligible to retire and to receive Social Security retirement payments, you have decided to continue working. You will wait to start Social Security, but you still expect to pick up Medicare now.

Your birthday came and went. You received cards from all your friends, but not the health insurance card from Uncle Sam. Should you be irate at the government bureaucracy for messing up again?

No. Here is one case where you can’t blame Uncle Sam. You don’t have to retire to receive Medicare Part A, but if you choose not to receive Social Security benefits at 65, your enrollment in Medicare Part A will not be automatic at that age. You must apply (contact your local Social Security office for an application).

EXAMPLE 11

You are retired and will begin receiving your Social Security benefits when you turn age 65 next month. You assume you don’t have to do anything to get Medicare.

Right! You are automatically enrolled in Medicare Part A when you receive Social Security benefits.

GEM: Get Medicare Part A Retroactively

You can change your mind and get Part A benefits retroactively! This is an extremely important tip to know when fate deals you an unlucky blow.

Let’s say you were eligible for Social Security but chose to postpone receiving those benefits. You forgot to apply for Medicare. Unfortunately, two months after your 65th birthday, you have a bad fall and fracture your hip. You are hospitalized and upon your release will require skilled physical therapy. If you sign up to receive Social Security (as soon as you can get back on your feet, so to speak), the Medicare Part A benefits you will receive can pay for any covered hospital and health care expenses even though they occurred before you applied.

However, there are time limits to Medicare’s patience. Here are the Golden Rules: You can pick up coverage dating back to the first day of your 65th birthday month, but not more than six months before the month you filed your application. (The deadline is 12 months if you are receiving Social Security survivor benefits.) You’ll be stuck paying any expenses incurred more than six months before you applied.

* * *

The date of your birthday can put money in your pocket. Our next three gems are Happy Birthday presents from your Uncle Sam.

GEM: Get Coverage for Your Full Birthday Month

You turn 65 on September 27. Surprise! Uncle Sam will give you Medicare coverage starting on September 1—the first day of your birthday month. Those extra days of coverage can mean a lot of dough to you.

GEM: Get an Extra Month Free If Your Birthday Falls on the First of the Month

Growing old is no laughing matter. Or is it? Consider this riddle: When is your birthday not your birthday? Answer: When you are dealing with Medicare!

Hard as it is to believe, Uncle Sam even had to stick his nose into this basic fact of life. For 65 years, you might have thought you knew your date of birth, but guess what? You were wrong. According to the folks at Social Security (who know better), you officially turn one year older on the day before your actual date of birth. Why do they do this? Who knows. Why does it matter? Because you can get an extra month of benefits, as Example 12 shows.

EXAMPLE 12

You turned 65 on February 1. Medicare says your birthday is really January 31. That means you can get Medicare benefits for the whole month of January!

Don’t forget that this crazy birthday rule will also affect the month in which you should enroll for Medicare. We’ve taken this into account when setting up Table 4.4.

MEDICARE PART A: INPATIENT HOSPITAL CARE

As we mentioned earlier, Medicare Hospital Insurance Part A is not exactly the most fitting title Uncle Sam could have picked to describe this entire program, because Part A actually covers more than just hospital-based services. Also included are inpatient skilled nursing facility care, home health care, and hospice care.1

We’ll first tell you about inpatient hospital care, giving you a treasure chest of gems to help you extend your coverage. Then we’ll uncover the secrets of the other Part A benefits.

How Do You Get in the Hospital Door?

Before the gates of Medicare Part A coverage are even opened to you, you need to meet Medicare’s four Hospital Entry Conditions, as stated in The Medicare Handbook (page 12).

• Has a doctor (not you) decided that your medical condition requires inpatient care?

• Is the type of care you need only available in a hospital?

• Is the hospital participating in Medicare?

• Has the hospital’s Utilization Review Committee (URC) or Uncle Sam’s Peer Review Organization (PRO) not disapproved your stay?

If you answered yes to all four questions, then go knock on the hospital’s doors. You should be allowed in, as Medicare’s guest.

What Medical Services Does Part A Inpatient Hospital Care Actually Include?

A good understanding of the inpatient hospital services you are entitled to under Medicare Part A should help assure you get what you deserve and avoid wrongful charges (which often occur). We have listed the most important covered services in Table 4.5.

TABLE 4.5

Covered Hospital Services

• Use of hospital facilities ordinarily provided to treat inpatients (isn’t that generous; there’s no extra charge for walls and floors).

• Semiprivate hospital room (2–4 beds).

• All your meals, special diets too (of course, we know they should be paying you to eat the food).

• Special care units, such as coronary care and intensive care, are thrown in at no extra charge.

• Medical social services, which can include:

1. Assessments of your social and emotional status to determine their impact on treatment and recovery

2. Evaluations of your medical and nursing needs to determine what community and personal resources will be needed upon discharge

3. Any social services ordinarily provided by the hospital that can contribute to the treatment of your illness

• Drugs ordinarily provided to hospital patients. Drug must be FDA approved as safe and effective for treating your illness. Experimental drugs or drugs that have not received final FDA marketing approval are not covered, unless specific permission has been given by Medicare.

• Blood transfusions. Although blood processing fees, starting with the first pint of blood, are covered, you are expected to either pay for, or find donors willing to replace, the first three pints you used. Don’t worry—Medicare does not intend to “bleed you dry.” During a calendar year, if you satisfy the blood deductible under Part B, you won’t be required to give another three pints for your Part A deductible. Isn’t that comforting?

• X-rays and other radiology services, including radiation therapy. These services must be billed by the hospital. Medicare bureaucrats with “x-rated” vision can see through any claims submitted from unapproved facilities and will deny coverage.

• Operating and recovery room costs, including hospital fees for anesthesia services. You can put your mind at rest. You won’t “go under” paying the hospital’s fees for surgery. The surgeon’s and anesthesiologist’s fees, though not covered by Part A, should be covered by Part B (here).

• Lab tests and diagnostic services performed by the hospital.

• Medical supplies and equipment. Medicare will pay for items a hospital ordinarily provides for the care and treatment of its inpatients—casts, splints, wheelchairs. However, you generally can’t take these items with you and expect Medicare Part A to pay (although Part B can cover these items; see here).

• Routine nursing care. You’re in luck: the nurse who wakes you at 6:00 A.M. to take your temperature is included at no extra charge!

• Specialists (e.g., nurses, anesthetists, psychologists). When the specialist works for the hospital, Medicare will pay.

• Rehabilitation services, such as speech therapy, occupational therapy, and speech pathology.

• Hospitalization due to dental-related disorders. Getting Medicare to pay for dental costs is, pardon the expression, like pulling teeth. But under certain circumstances, you will be covered for the hospital’s charges. For example, Medicare should pay hospital expenses for a noncovered dental service if your stay is required because of either the severity of the procedure or your physical condition (e.g., you have a history of heart trouble, and the dental surgery you’re having requires anesthesia). Your dental surgeon or physician must certify that hospitalization is necessary.

• Alcoholism treatment. Inpatient hospital care for alcoholism and detoxification should be covered (usually two to three days), if medical complications are likely to occur. A stay for rehabilitation will not be covered unless specific reasons can be given for a hospital setting rather than using a less costly outpatient treatment program.

• Inpatient psychiatric hospital care. You generally are entitled to a lifetime total of 190 days of coverage at a Medicare-approved psychiatric hospital.

Source: The Medicare Handbook, page 13.

The following gems can help you cash in on the covered services listed in Table 4.5.

GEM: Get Special Drug Coverage

If you can get the hospital to agree to specially order a drug for you because it is not routinely stocked, Medicare should cover the cost, even though it is not ordinarily provided to hospital patients. In addition, for a limited period of time, Medicare will pay the costs of drugs after you leave a hospital, if using that medication on an outpatient basis will speed your departure. Why? By treating you at home, Medicare saves money.

GEM: Get Special Coverage for Off-site Lab or Diagnostic Tests

If an off-site location must be used to perform diagnostic procedures because the hospital is unable to provide this care, Medicare should cover the cost.

EXAMPLE 13

In order to diagnose your hearing disorder, complex testing is necessary. The hospital does not have an audiologist on staff so you are sent to a hearing and speech center. This off-site service should be covered.

Part A should pay for any off-site lab and diagnostic service if the hospital has an agreement with a Medicare-approved provider and the services will be billed directly to the hospital. Ask your doctor or the hospital to make sure Medicare is covering. If you receive a bill for the service, DO NOT PAY! Call the service provider and explain why.

GEM: You Can Take It with You: Keep Your Pacemaker!

As Table 4.5 shows, Medicare generally won’t pay for supplies and equipment you take with you. But when it would be medically unreasonable to demand their return, you should be allowed to “carry out” items you are “wearing,” such as cardiac valves, pacemakers, drainage tubes, replaced body organs, and so on—at Medicare’s cost! Although equipment provided to use outside the hospital will not be paid under Inpatient Hospital coverage, you might be eligible for additional benefits under Medicare’s Part A Home Health Care Insurance (here) or under Medicare Part B (here).

GEM: Get Special Coverage for Nonstaff Members

While Medicare says it only pays for services by persons on the hospital staff, you should also be covered if hospital service is provided by a nonstaff member (such as a psychologist or therapist) under a contract with the hospital. (Any private agreements you work out don’t count!)

GEM: Pass the Rehabilitation Services Coverage Test

Although The Medicare Handbook states that rehabilitation services are covered, getting coverage is not as easy as it sounds. Medicare will pay only when you can prove the rehabilitation is “reasonable and necessary” for treating your illness. To meet these requirements, make sure the therapy is:

• Prescribed in writing by your doctor or physical therapist.

• Performed by a qualified therapist or done under his supervision. (Even health maintenance and routine services performed by nurses’ aides or other support staff to promote fitness or flexibility can sometimes be covered; check with your doctor or hospital’s representative who handles Medicare services.)

• Restorative. No matter who provides the service, Medicare won’t pay a penny for therapy if you are not going to improve “significantly” after a “reasonable” period of time. When you and the Government don’t see eye-to-eye on your progress, have your doctor or therapist write a letter explaining why the therapy is still justifiable to maintain or restore your health.

GEM: A Hospital Can’t Stick You Twice

If a service you receive at a hospital is eligible for Medicare coverage, the hospital is not allowed to charge you at all for that service, even if its actual cost for providing you with the care is more than the Medicare reimbursement. The hospital must pay any additional cost—so don’t let them “needle” you for the money.

* * *

What Hospital Services Will You Pay for?

Medicare will not pay for your “comfort and convenience” in the hospital. It is best to operate on the assumption that any care or service used to make your hospital visit more pleasant will not be paid for by Medicare. Therefore, according to The Medicare Handbook (page 13), you will be billed for:

1. Telephone, television (and any other personal conveniences).

2. Private-duty nurses. Even if this care was ordered by your doctor because the hospital was unable to provide the needed service, you must still pay.

3. Any extra charges for a private room, unless your condition required isolation or no semiprivate rooms were available.

What If You Go to a Non-Medicare Hospital?

Although most do, not every hospital participates in the Medicare program. If the hospital you go to has not signed a participation agreement with Medicare, Medicare will not pay even for covered services. Medicare does not pay for services performed at a nonparticipating hospital.

There’s an important exception to this rule: Medical services provided by a nonparticipating hospital in life threatening situations can be covered.

EXAMPLE 14

You are involved in a car accident and are very seriously injured. The emergency medical squad takes you to the closest hospital that is qualified to handle such emergencies. The bad news is that you were unconscious and couldn’t ask if it was a Medicare participating facility, and it isn’t. The good news is that Medicare may still pay.

To qualify for emergency Medicare coverage, you must meet all of the following requirements.

1. Your medical condition, if not treated immediately, would have resulted in death or serious impairment.

2. The hospital chosen was significantly easier to reach or closer than the nearest participating facility. (Caution: Medicare has denied claims when a participating hospital was available 15 miles away.)

3. The hospital meets Medicare’s standards for providing the needed emergency services.

The regional Health Care Financing Administration (HCFA) office is responsible for deciding if all criteria for coverage have been met. A physician’s statement supporting the claim of a medical emergency will also be required.

GEM: Get Out When the Emergency Is Over

Medicare will pay for your care at a non-Medicare facility for only as long as the emergency condition exists. When Medicare decides you are well enough to be transferred or released, coverage will stop.

* * *

Will you be covered if a medical emergency arises while you are vacationing in a foreign country? Non, Nein, Lo—the answer in any language is no, with one exception: If you were in Canada or Mexico and you can prove that the foreign (non-Medicare) hospital was closer than the nearest participating U.S. hospital, Medicare might pay.

MEDICARE PART A: SKILLED NURSING FACILITY (SNF) CARE

Nursing-home costs can be catastrophic. In limited cases, your Part A insurance can continue to pay for care at an SNF after you leave the hospital. But, as you probably have guessed, Medicare does not make it easy to qualify; very specific conditions must be met. You are eligible for this type of extended care coverage if you can check yes to all of these statements, according to The Medicare Handbook (page 15).

Medicare does not like paying for skilled nursing care. Nationally, only about 2 percent of all nursing-home costs are paid by Medicare. That is far too little. By understanding Medicarese and vigorously pursuing your rights, however, you should be able to get better results from Medicare. (If you can’t cash in on Medicare, Medicaid may provide a Golden Opportunity for funding; see Chapter 11).

What Is a Skilled Nursing Facility?

According to The Medicare Handbook, an SNF is “a specially qualified facility with the staff and equipment to provide skilled nursing care or rehabilitation services and other related services.” Some nursing homes provide only skilled care and participate entirely in Medicare. In others, only certain portions of the facility might participate in Medicare as an SNF, and some SNFs don’t participate in Medicare at all. Make sure you are in a Medicare-qualified bed in a Medicare-qualified facility.

The key question is, Is this facility a Medicare-qualified SNF for the services I need? Have your doctor give you a complete list of the services you need. That way you will have an accurate record to work with when you are playing caregiver matchmaker.

How do you find out if the facility qualifies for Medicare coverage for your service? Here is a list of likely sources for help:

• Hospital Discharge Planners. These folks are familiar with the services available at local SNFs and can usually provide an answer, or they can call and inquire for you.

• Nursing Home Admissions Offices and their Utilization Review Committee (URC). Every facility that participates in Medicare has a URC, and it is their job to decide whether the services you need will be covered by Medicare.

• The Medicare Intermediary for Your Area. Each state chooses which insurance company will act as an intermediary and process its Medicare Part A claims. The toll-free numbers of the Medicare Intermediaries for every state can be found in Appendix 17.

• Social Security. If you are lucky enough to get through on the toll-free number, tell the representative that it is printed in The Medicare Handbook that Social Security can “check with the HCFA” to determine whether your specific needs will be covered. (See the Handbook section titled Skilled Nursing Facility Care.) Then read the list of services you require.

GEM: Get Help to Help You Get Help

When we say “you,” you don’t need to take us literally. If you are not feeling up to taking action (and obviously if you were feeling terrific, you wouldn’t be needing SNF care services), don’t make yourself sicker trying to do all this alone. Get some help.

Whom should you ask? Consider all sources for assistance:

• Family

• Friends

• Hospital social worker or discharge planner

• Office on Aging (check the blue pages of your phone book under County Government)

• Senior citizen centers in your community

• State or county nursing home ombudsman (these individuals are paid by the state or county to act as advocates for nursing home residents)

GEM: Don’t Let the SNF’s Goof Cost You

You shouldn’t have to pay for someone else’s mistake. If you are incorrectly placed in the nonparticipating section of an SNF, Medicare will deny coverage. But since it is the facility’s fault, not yours, you shouldn’t be liable. Hold on to your wallet; let the facility fight it out with Uncle Sam.

* * *

What Is the Difference Between Routine (Custodial) and Skilled Care?

When it comes to extended care coverage, Medicare makes it perfectly clear that there is a major distinction between routine (custodial) and skilled care. You’d better know the difference too, because how your care is defined will determine who is paying—Uncle Sam or you. Medicare pays for skilled nursing-home care provided on a daily basis; you pay for routine or custodial care (unless you have purchased private nursing-home insurance or can qualify for Medicaid—see Chapter 11).

Custodial Care. Could any Tom, Dick or Harry perform the job safely? A service that does not require the medical expertise of a skilled professional is considered routine or custodial (e.g., help with bathing, feeding, dressing, eating, or walking). In practical terms, if Medicare defines your care as custodial care, you will pay the bill.

Table 4.6 provides a sampling of services which are “routinely” considered routine and custodial.

TABLE 4.6

Sampling of Custodial and Personal Care Services

• Assistance with routine application of eye drops, ointments, and other medications

• Maintenance of colostomy, ileostomy, bladder catheters

• Changes of dressings for noninfected postoperative or chronic conditions

• Baths or care for minor skin problems

• Routine care of incontinence (e.g., diaper and linen changes)

• Routine help with braces, casts

• Heat treatments for comfort (e.g., whirlpool)

• Assistance with medical gases, once a regimen has been established

• Help with dressing, eating, personal hygiene

• Supervision and assistance with exercise programs that have already been taught (e.g., repetitive exercises to maintain or improve strength and endurance) and do not require skilled supervision

Source: 42 C.F.R. §409.33(d).

Skilled Care. As you probably can guess, skilled care is just the opposite of routine care. A service is skilled when only someone with special training can perform safely and effectively the tasks of care, observation, or assessment. At least on paper, the difference between routine and skilled care seems clear. But as you will see, determining what care requires skilled services is not at all clear. Shades of gray appear because each person’s psychological, physical, and environmental circumstances are unique, and by law, Medicare is supposed to base its care decisions on your total situation [42 C.F.R. §409.33 (a) (1)].

Medicare can barely handle black and white, so do you actually believe some bureaucrat buried in paperwork has the time to examine the “gray”? You can expect “differences of opinion” (read that denial of claims). In fact, the Government unfairly avoids paying claims by strictly interpreting “skilled” care. We have had clients who were connected to so many tubes they looked like something out of a science fiction movie, and yet Uncle Sam refused to pay, claiming their care was not skilled! The Government will trample your rights unless you (or a loved one) insist on coverage.

Here is an example that illustrates the gray variations that can arise over routine and skilled care.

EXAMPLE 15

After a complex surgery, you were admitted to an SNF for care. Why was an SNF appropriate? In addition to needing physical therapy three times a week, a nurse had to take your temperature hourly each day. When the claim for your care is submitted, the Medicare bureaucrat who reviews it says, “Aha—do they take us for fools? Obviously, SNF level care isn’t needed for this person because reading a thermometer is an unskilled duty. The claim must be denied,” she says with glee.

Now here comes the gray. What she failed to notice (or could not know because the claim form was not specific enough in its explanation) was this key fact: You had recently been placed on a potent, potentially lethal medication, and the first sign of toxicity is a slight fever. The services of a skilled nurse to read a thermometer were truly medically justified to evaluate and manage your condition. In this situation, although the care itself is unskilled, only an LPN had the level of expertise to interpret symptoms and make recommendations for adjusting the treatment. Your care should be considered skilled—and covered!

The best way to get an idea of which type of care is skilled is to look at actual situations. In Table 4.7, we list some real-life circumstances that should qualify for skilled nursing service coverage.

TABLE 4.7

Sampling of Skilled Nursing Services

• Tube feedings and other related services. Gastrostomy feedings, and nasopharyngeal and tracheostomy maintenance and replacement, are complex activities requiring skilled nursing and should be covered when needed to treat your illness.

• Catheters. Insertion, cleaning, and replacement of catheters should be covered skilled services.

• Wound care. Don’t expect Medicare to pay for a skilled nurse to bandage your little nicks and scratches. But when the size and nature of a wound, burn, tube site, sore or tumor require application of medicated dressings or other special care and monitoring, the care should be considered skilled. Your doctor will need to document the reasons and provide specific instructions in your plan for care (your doctor’s written prescription for the services and treatment you will need to stabilize or cure your condition); otherwise, you might be denied coverage.

• Ostomy care. Immediately following surgery, or where complications occur, care for an ostomy can be covered.

• Heat treatments (e.g., hot packs, whirlpool baths, infrared treatments). You’ll take the heat for this care unless the treatments have been ordered by a physician and require observation by nurses to evaluate your progress.

• Intravenous, intramuscular, or subcutaneous injections. Diabetics take note: insulin injections fall into this category and so can be covered as a skilled service. This has often been a bone of contention for SNF eligibility.

• Medical gases. Administration of medical gases can be covered in an SNF. Teaching you or your caregivers how to administer treatment and also monitoring your response to the gases until your condition stabilizes also can be qualified as skilled service.

• Treatment of serious skin disorders. Serious skin problems, such as decubitus ulcers, often require skilled care.

• Bowel and bladder training. Helping a patient regain bowel and bladder control can qualify for coverage as skilled care.

Source: 42 C.F.R. §409.33(b).

What Are Skilled Rehabilitation Services?

You are entitled to coverage under Part A for skilled rehabilitation services—such as physical, speech, and occupational therapy—at an SNF. Speech therapy includes procedures necessary to diagnose and treat speech and language disorders. Occupational therapy includes treatment to improve or restore a patient’s ability to handle daily activities.

EXAMPLE 16

You had a hip replacement, and after the operation you have difficulty regaining your balance. Your doctor prescribes physical therapy. Working with a qualified therapist at an SNF, you learn standing and walking techniques to improve your balance. The cost for these services should be covered by Uncle Sam.

EXAMPLE 17

You suffer a stroke and lose partial use of your right arm. An occupational therapist teaches you new ways to hold eating utensils so that you can feed yourself and regain independence. The SNF costs should be covered.

Table 4.8 lists some examples of rehabilitation services that should qualify as skilled care in an SNF.

TABLE 4.8

Sampling of Skilled Rehabilitation Services

• Assessment of rehabilitation needs. These include tests and measurements of range of motion, strength, balance, coordination, endurance and functional abilities.

• Therapeutic exercises or activities. If the type of exercises or your condition requires supervision to ensure your safety or the effectiveness of the treatment, it should be covered.

• Walking evaluation and training. If your ability to walk has been impaired, evaluation and training should be covered.

• Exercises in response to loss or restriction of range of motion.

• Maintenance therapy. Let’s say you have Parkinson’s disease. Exercises to maintain your present level of functioning, under the supervision of a qualified therapist, should be covered.

• Ultrasound, short-wave, and microwave therapy.

• Hot pack, hydrocollator, infrared treatments, paraffin baths, and whirlpool. These should be covered if warranted to treat your specific condition and the skills, knowledge and judgement of a qualified therapist are required.

• Services of a speech pathologist or audiologist.

Source: 42 C.F.R. §409.33 (c).

The Government often catches you in one of two traps: your claim for SNF coverage will be denied if you can’t show that the treatment or therapy is essential to improve or maintain your physical condition; and coverage will be denied if skilled care is not required on a daily basis.

Uncle Sam generally expects improvement over a “reasonable” and “predictable” time period.

EXAMPLE 18

As a result of a stroke, your speech is impaired. A skilled speech pathologist assesses your rehabilitation potential and determines that, with therapy, a measurable improvement in your communicative skills can be achieved. A plan of care is devised with specific goals for speech production. Medicare will pay for the skilled speech therapy because you have “rehabilitation potential” and it is hoped significant improvement can be achieved in a predictable time. Keep in mind that coverage will last only as long as you can continue to “pass” the tests. Once the benefit of therapy stops, Medicare coverage will, too.

GEM: Maintenance Is Enough to Get Coverage

The Government has a tendency to overlook the fact that rehabilitation service should be covered as long as the treatment is necessary to maintain your condition. Don’t let them!

EXAMPLE 19

Your father suffered a stroke and is having trouble walking. A therapist in the SNF has been helping him learn to walk with a walker, but now the Government says he’s not making further progress.

Although he may not be making further progress, he is likely to regress if therapy is stopped. Without continued therapy, he will go back to the wheelchair. In this case, you can fight the Government’s decision to cut off benefits.

To qualify for coverage in an SNF, the skilled care must be provided on a daily basis. This means that the skilled nursing or rehabilitation service you receive must be needed seven days a week. Uncle Sam does allow one important exception: if skilled rehabilitation services are not available every day, you can still qualify for coverage if you receive the service at least five days a week.

* * *

GEM: A Short Break in Rehabilitation Should Not End Coverage

Let’s say your doctor suspends your rehabilitation program for a couple of days because you are exhausted and need a rest. Or maybe you get sick and miss three days. The short break should not cause you to lose Medicare coverage, but a break in skilled nursing care can terminate your benefits.

GEM: Try Part B Coverage

Therapy at an SNF can also be covered under Medicare Part B insurance. If you have used up, or aren’t eligible for, Part A coverage, check out this option with the SNF. Note: under Part B, the services of an independent therapist are limited to $750 a year and you must pay co-insurance, too.

GEM: Make Sure the Provider Uses the Right Claim Form

We have seen rehabilitation claims unfairly denied simply because the wrong claim form was used. You can’t use a Part B claim form to get Part A services, and vice versa. If you are denied, check to see if the right form was used and ask the provider to refile. Your denial may have just been from incorrect paper work.

GEM: Make Sure Doctor Certifies Need for Skilled Care

Your doctor must certify in writing that skilled-level care is required as an inpatient or on a daily basis (at least five days a week). If your doctor doesn’t routinely attend to Medicare patients, make sure he works with the hospital’s discharge planner to assure all the certification paperwork is done.

* * *

What Are the Time Requirements?

To get Medicare to cover SNF services, you must have been hospitalized at least three consecutive days before entering an SNF. That three-day requirement is a hidden trap that can cost you plenty.

EXAMPLE 20

Dan entered the hospital on January 1 and was transferred to a Medicare-approved SNF on January 3. Will Medicare pay? No. Even though Dan went to an approved facility and was receiving skilled nursing care, he did not meet the three-consecutive-day hospitalization requirement. Medicare counts the day of admission as one day, but does not count the day of discharge. If Dan had stayed in the hospital one more day and transferred on January 4, he would have been eligible for Medicare coverage. Instead, he will be paying thousands of dollars to the nursing home out of his own pocket.

EXAMPLE 21

Dan spent three days in a psychiatric hospital before being transferred to an SNF. Will he be covered? Yes. Treatment in a psychiatric hospital should be considered equivalent to a “general hospital,” so the three-day inpatient care requirement is met.

What if the three days prior to SNF admission were spent at a Christian Science Sanitorium? No. Medicare doesn’t consider these facilities hospitals, so time spent there is not counted.

Medicare applies the three-day requirement strictly. It won’t waive the three-day requirement even if you are forced out of a hospital because of a lack of beds.

EXAMPLE 22

You were treated in the hospital emergency room and required immediate hospitalization. Unfortunately no beds were available, so you were admitted to the SNF unit of the hospital. Medicare will not pay even though the unit was a participating SNF. Why? To receive benefits at an SNF, you must first be hospitalized for three days.

GEM: Beat the Three-Day Requirement!

Don’t let the hospital or doctor discharge you or a loved one to an SNF before you’ve spent three days in a hospital. Talk to your hospital discharge planner or doctor to see if an extra day can somehow be justified. That extra day can save you thousands of dollars in nursing costs.

If the hospital (through its Utilization Review Committee) or Peer Review Organization (PRO) tells you to leave, challenge their decision—don’t go! Insist on staying another day. If the PRO told you to leave, and you lose the appeal, you will have to pay the extra day of hospital care, but the cost will be worth it if the extra day helps you meet the three-day hospitalization requirement for SNF coverage! And if the notice to leave came from the hospital, you won’t have to pay while the PRO reviews your case (even if the PRO agrees with the hospital).

* * *

In addition to the three-day requirement, Medicare imposes another time requirement: You must enter the SNF within 30 days after leaving the hospital, and your care at the SNF must be necessitated by the same condition that first sent you to the hospital. Continuity of care is the key phrase here.

EXAMPLE 23

Dan was hospitalized for a severe foot infection; he stabilized and four days later was discharged. Twenty-two days later his doctor admitted him to a Medicare-approved nursing home, where he received skilled nursing care for a different condition. Will Medicare pay? No.

But Dan met the 30-day limit and 3-day hospitalization requirements, right? Yes and no. Remember, for the stay to be covered, the need for extended care services must either be due to the condition that necessitated hospitalization or be an ailment that arose during that stay.

GEM: Get Proof of Continuity of Care

Make sure your doctor’s statement certifying your need for care clearly establishes a link between your hospital stay and the skilled nursing care you will need.

* * *

Medicare expects you to enter an SNF within 30 days after the day you left the hospital. For example, if your date of discharge from the hospital is July 1, and you enter an SNF on July 31, you will be covered because the Medicare meter starts ticking on July 2, the day after discharge. But if you enter the SNF one day later on August 1, you will be out of luck. You will have exceeded the 30-day limit.

Will Medicare Pay?

Will Medicare pay if you:

• Enter an SNF for custodial care within 30 days after leaving the hospital but after 30 days you then need skilled care? NO. You must start skilled services within 30 days.

• Require skilled care for the first 10 days, only custodial care for the next twenty days, then on Day 31 skilled care again? NO. Medicare will pay for those first 10 days, but will not resume payment for the subsequent skilled care because 30 days have elapsed since your hospital discharge.

• Leave an SNF and are readmitted (to the same or a different SNF) within 30 days of your hospital discharge owing to the same illness? YES. You can go home again, so to speak, as long as it’s within Medicare’s time limits.

• Leave an SNF, then suffer a relapse within 30 days after discharge that requires a hospitalization? YES. If the hospitalization occurs within 30 days after your discharge from the SNF, Medicare will treat your hospital stay as if it’s a return to an SNF.

GEM: Extend the 30-Day Limit

Medicare—in its great wisdom—recognizes that, with certain health conditions, transfer to an SNF within 30 days to continue treatment is not always “medically appropriate.” In that case, you may be able to get an extension. To qualify, at the time you leave the hospital, your doctor must have a specific timetable for continuing skilled treatment at an SNF, and you must really follow through.

Medicare won’t accept any vague promises; Uncle Sam wants predictability. To illustrate this point, Examples 24 and 25 show two very different outcomes.

EXAMPLE 24

You fall and break a hip. After leaving the hospital you will still need physical therapy. Appropriate medical procedure requires a four- to six-week wait before treatment can begin. Your doctor prepares a written plan of care that states you will enter an SNF five weeks after hospitalization to begin rehabilitation therapy. Under Medicare rules, you shall be able to get an extension because the delay was “medically appropriate” and predictable.

EXAMPLE 25

You were hospitalized to treat a severe stomach disorder. It is very likely that you will require treatment again in the near future, but your doctor can’t give an exact time frame or estimate the level of care that will be needed. After 30 days, if you do need skilled care, tough luck! Although the delay in care might be medically appropriate, it is not predictable. That means no money.

GEM: If You Can’t Get in Within 30 Days, Try to Delay to 60

If you don’t need an SNF for 30 days, and you can’t get an extension, try to stay at home for 60 days, so that you can enter a new benefit period. If you then return as a hospital inpatient for three days, you will be entitled to a new chance to qualify for SNF benefits. Example 26 shows how this happens.

EXAMPLE 26

Let’s start with the same situation as Example 25. Just 59 days after your discharge from the hospital your stomach problems start to reappear. You immediately rush to the hospital, where you are treated for four days. You are then discharged to an SNF.

Unfortunately, since 60 days had not passed from the prior hospitalization, no new benefit period starts, so you don’t get coverage for the SNF. Had you been able to wait one more day at home before entering the hospital, your SNF bills would have been covered.

* * *

What Will Medicare Pay?

Once you qualify for SNF coverage, the questions are what Medicare will pay for, and what services are covered. Table 4.9 shows what Medicare pays.

TABLE 4.9

Who Pays for Skilled Nursing Facility Care Coverage?

As Table 4.9 shows, Medicare pays for all or part of your covered services for up to 100 days each benefit period. Keep in mind that once you are out of an SNF for 60 days in a row, the Medicare timer goes back to zero, and you are entitled to a new 100 days of SNF coverage. Of course, you must still meet all the same conditions (three-day hospital stay, etc.) before Medicare will pay.

What Services Do You Get?

Assuming you are in a participating SNF, you need skilled care, and you meet the time requirements, Medicare will pay for the services listed in Table 4.10. Table 4.11 lists services that Medicare will not pay for.

TABLE 4.10

SNF Services Paid by Medicare Part A

• Skilled nursing care.

• Semiprivate room (two to four beds in a room). If one isn’t available at time of admission, Medicare will pay for a private room, but when a semiprivate is ready, you must switch or pay.

• All meals and special diets (unfortunately, pizza doesn’t count as a special dietary need, so delivery charges for a pie aren’t covered!).

• Regular nursing services provided by SNF staff (e.g., taking your temperature or blood pressure).

• Rehabilitation services, including physical, speech, and occupational therapy.

• Drugs, medical supplies and therapeutic equipment (e.g., splints and wheelchairs).

• Blood transfusions (after meeting your three-pint deductible).

• Medical social services and diagnostic services, including a social worker’s assessment of your adjustment to treatment and help in responding to emotional issues resulting from the illness.

• Other services necessary to maintain your health that can only be provided by an SNF.

Source: The Medicare Handbook, pages 15–16.

TABLE 4.11

SNF Costs You Pay

• TVs, telephones, and any other personal luxuries

• Private-duty nurses

• Additional charges for a private room, unless medically necessary

• Custodial nursing home-care services (e.g., haircuts), other than daily personal care needs like bathing, feeding, and dressing

• Doctors’ bills (Medicare Part B insurance will help pay these fees—see here)

Source: The Medicare Handbook, page 16.

When Medicare is paying, don’t expect a room with a view and privacy, too. You are entitled to a semiprivate room (two to four beds in a room). That is it, period. This rule applies to both hospitals and SNFs.

GEM: Get a Private Room, at Uncle Sam’s Expense

Here are two ways you might get a private room.

First, if your condition requires isolation to protect your health or others, a private room should be considered “medically necessary.” Get Medicare to pay.