5.3.4 Further Properties of Poisson Processes

Consider a Poisson process  having rate

having rate  , and suppose that each time an event occurs it is classified as either a type I or a type II event. Suppose further that each event is classified as a type I event with probability

, and suppose that each time an event occurs it is classified as either a type I or a type II event. Suppose further that each event is classified as a type I event with probability  or a type II event with probability

or a type II event with probability  , independently of all other events. For example, suppose that customers arrive at a store in accordance with a Poisson process having rate

, independently of all other events. For example, suppose that customers arrive at a store in accordance with a Poisson process having rate  ; and suppose that each arrival is male with probability

; and suppose that each arrival is male with probability  and female with probability

and female with probability  . Then a type I event would correspond to a male arrival and a type II event to a female arrival.

. Then a type I event would correspond to a male arrival and a type II event to a female arrival.

Let  and

and  denote respectively the number of type I and type II events occurring in

denote respectively the number of type I and type II events occurring in  . Note that

. Note that  .

.

Proposition 5.2

and

and  are both Poisson processes having respective rates

are both Poisson processes having respective rates  and

and  . Furthermore, the two processes are independent.

. Furthermore, the two processes are independent.

Proof

It is easy to verify that  is a Poisson process with rate

is a Poisson process with rate  by verifying that it satisfies Definition 5.3.

by verifying that it satisfies Definition 5.3.

•  follows from the fact that

follows from the fact that  .

.

• It is easy to see that  inherits the stationary and independent increment properties of the process

inherits the stationary and independent increment properties of the process  . This is true because the distribution of the number of type I events in an interval can be obtained by conditioning on the number of events in that interval, and the distribution of this latter quantity depends only on the length of the interval and is independent of what has occurred in any nonoverlapping interval.

. This is true because the distribution of the number of type I events in an interval can be obtained by conditioning on the number of events in that interval, and the distribution of this latter quantity depends only on the length of the interval and is independent of what has occurred in any nonoverlapping interval.

•

Thus we see that  is a Poisson process with rate

is a Poisson process with rate  and, by a similar argument, that

and, by a similar argument, that  is a Poisson process with rate

is a Poisson process with rate  . Because the probability of a type I event in the interval from

. Because the probability of a type I event in the interval from  to

to  is independent of all that occurs in intervals that do not overlap

is independent of all that occurs in intervals that do not overlap  , it is independent of knowledge of when type II events occur, showing that the two Poisson processes are independent. (For another way of proving independence, see Example 3.23.)

, it is independent of knowledge of when type II events occur, showing that the two Poisson processes are independent. (For another way of proving independence, see Example 3.23.)

Example 5.14

If immigrants to area  arrive at a Poisson rate of ten per week, and if each immigrant is of English descent with probability

arrive at a Poisson rate of ten per week, and if each immigrant is of English descent with probability  , then what is the probability that no people of English descent will emigrate to area

, then what is the probability that no people of English descent will emigrate to area  during the month of February?

during the month of February?

Example 5.15

Suppose nonnegative offers to buy an item that you want to sell arrive according to a Poisson process with rate  . Assume that each offer is the value of a continuous random variable having density function

. Assume that each offer is the value of a continuous random variable having density function  . Once the offer is presented to you, you must either accept it or reject it and wait for the next offer. We suppose that you incur costs at a rate

. Once the offer is presented to you, you must either accept it or reject it and wait for the next offer. We suppose that you incur costs at a rate  per unit time until the item is sold, and that your objective is to maximize your expected total return, where the total return is equal to the amount received minus the total cost incurred. Suppose you employ the policy of accepting the first offer that is greater than some specified value

per unit time until the item is sold, and that your objective is to maximize your expected total return, where the total return is equal to the amount received minus the total cost incurred. Suppose you employ the policy of accepting the first offer that is greater than some specified value  . (Such a type of policy, which we call a

. (Such a type of policy, which we call a  -policy, can be shown to be optimal.) What is the best value of

-policy, can be shown to be optimal.) What is the best value of  ? What is the maximal expected net return?

? What is the maximal expected net return?

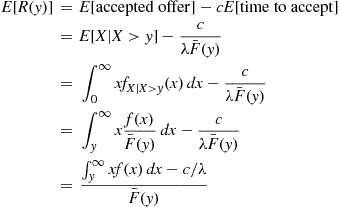

Solution: Let us compute the expected total return when you use the  -policy, and then choose the value of

-policy, and then choose the value of  that maximizes this quantity. Let

that maximizes this quantity. Let  denote the value of a random offer, and let

denote the value of a random offer, and let  be its tail distribution function. Because each offer will be greater than

be its tail distribution function. Because each offer will be greater than  with probability

with probability  , it follows that such offers occur according to a Poisson process with rate

, it follows that such offers occur according to a Poisson process with rate  . Hence, the time until an offer is accepted is an exponential random variable with rate

. Hence, the time until an offer is accepted is an exponential random variable with rate  . Letting

. Letting  denote the total return from the policy that accepts the first offer that is greater than

denote the total return from the policy that accepts the first offer that is greater than  , we have

, we have

(5.14)

(5.14)

Differentiation yields

Therefore, the optimal value of  satisfies

satisfies

or

or

It is not difficult to show that there is a unique value of  that satisfies the preceding. Hence, the optimal policy is the one that accepts the first offer that is greater than

that satisfies the preceding. Hence, the optimal policy is the one that accepts the first offer that is greater than  , where

, where  is such that

is such that

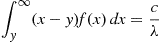

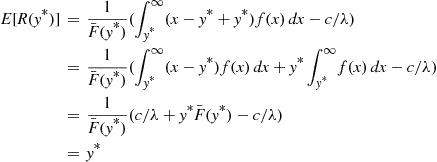

Putting  in Equation (5.14) shows that the maximal expected net return is

in Equation (5.14) shows that the maximal expected net return is

Thus, the optimal critical value is also the maximal expected net return. To understand why this is so, let  be the maximal expected net return, and note that when an offer is rejected the problem basically starts anew and so the maximal expected additional net return from then on is

be the maximal expected net return, and note that when an offer is rejected the problem basically starts anew and so the maximal expected additional net return from then on is  . But this implies that it is optimal to accept an offer if and only if it is at least as large as

. But this implies that it is optimal to accept an offer if and only if it is at least as large as  , showing that

, showing that  is the optimal critical value.

is the optimal critical value.

It follows from Proposition 5.2 that if each of a Poisson number of individuals is independently classified into one of two possible groups with respective probabilities  and

and  , then the number of individuals in each of the two groups will be independent Poisson random variables. Because this result easily generalizes to the case where the classification is into any one of

, then the number of individuals in each of the two groups will be independent Poisson random variables. Because this result easily generalizes to the case where the classification is into any one of  possible groups, we have the following application to a model of employees moving about in an organization.

possible groups, we have the following application to a model of employees moving about in an organization.

Example 5.16

Consider a system in which individuals at any time are classified as being in one of  possible states, and assume that an individual changes states in accordance with a Markov chain having transition probabilities

possible states, and assume that an individual changes states in accordance with a Markov chain having transition probabilities  . That is, if an individual is in state

. That is, if an individual is in state  during a time period then, independently of its previous states, it will be in state

during a time period then, independently of its previous states, it will be in state  during the next time period with probability

during the next time period with probability  . The individuals are assumed to move through the system independently of each other. Suppose that the numbers of people initially in states

. The individuals are assumed to move through the system independently of each other. Suppose that the numbers of people initially in states  are independent Poisson random variables with respective means

are independent Poisson random variables with respective means  . We are interested in determining the joint distribution of the numbers of individuals in states

. We are interested in determining the joint distribution of the numbers of individuals in states  at some time

at some time  .

.

Solution: For fixed  , let

, let  denote the number of those individuals, initially in state

denote the number of those individuals, initially in state  , that are in state

, that are in state  at time

at time  . Now each of the (Poisson distributed) number of people initially in state

. Now each of the (Poisson distributed) number of people initially in state  will, independently of each other, be in state

will, independently of each other, be in state  at time

at time  with probability

with probability  , where

, where  is the

is the  -stage transition probability for the Markov chain having transition probabilities

-stage transition probability for the Markov chain having transition probabilities  . Hence, the

. Hence, the  will be independent Poisson random variables with respective means

will be independent Poisson random variables with respective means  ,

,  . Because the sum of independent Poisson random variables is itself a Poisson random variable, it follows that the number of individuals in state

. Because the sum of independent Poisson random variables is itself a Poisson random variable, it follows that the number of individuals in state  at time

at time  —namely

—namely  —will be independent Poisson random variables with respective means

—will be independent Poisson random variables with respective means  , for

, for  .

.

Example 5.17

The Coupon Collecting Problem

There are  different types of coupons. Each time a person collects a coupon it is, independently of ones previously obtained, a type

different types of coupons. Each time a person collects a coupon it is, independently of ones previously obtained, a type  coupon with probability

coupon with probability  . Let

. Let  denote the number of coupons one needs to collect in order to have a complete collection of at least one of each type. Find

denote the number of coupons one needs to collect in order to have a complete collection of at least one of each type. Find  .

.

Solution: If we let  denote the number one must collect to obtain a type

denote the number one must collect to obtain a type  coupon, then we can express

coupon, then we can express  as

as

However, even though each  is geometric with parameter

is geometric with parameter  , the foregoing representation of

, the foregoing representation of  is not that useful, because the random variables

is not that useful, because the random variables  are not independent.

are not independent.

We can, however, transform the problem into one of determining the expected value of the maximum of independent random variables. To do so, suppose that coupons are collected at times chosen according to a Poisson process with rate  . Say that an event of this Poisson process is of type

. Say that an event of this Poisson process is of type  , if the coupon obtained at that time is a type

, if the coupon obtained at that time is a type  coupon. If we now let

coupon. If we now let  denote the number of type

denote the number of type  coupons collected by time

coupons collected by time  , then it follows from Proposition 5.2 that

, then it follows from Proposition 5.2 that  are independent Poisson processes with respective rates

are independent Poisson processes with respective rates  . Let

. Let  denote the time of the first event of the

denote the time of the first event of the  th process, and let

th process, and let

denote the time at which a complete collection is amassed. Since the  are independent exponential random variables with respective rates

are independent exponential random variables with respective rates  , it follows that

, it follows that

Therefore,

(5.15)

(5.15)

It remains to relate  , the expected time until one has a complete set, to

, the expected time until one has a complete set, to  , the expected number of coupons it takes. This can be done by letting

, the expected number of coupons it takes. This can be done by letting  denote the

denote the  th interarrival time of the Poisson process that counts the number of coupons obtained. Then it is easy to see that

th interarrival time of the Poisson process that counts the number of coupons obtained. Then it is easy to see that

Since the  are independent exponentials with rate 1, and

are independent exponentials with rate 1, and  is independent of the

is independent of the  , we see that

, we see that

Therefore,

and so  is as given in Equation (5.15).

is as given in Equation (5.15).

Let us now compute the expected number of types that appear only once in the complete collection. Letting  equal

equal  if there is only a single type

if there is only a single type  coupon in the final set, and letting it equal

coupon in the final set, and letting it equal  otherwise, we thus want

otherwise, we thus want

Now there will be a single type  coupon in the final set if a coupon of each type has appeared before the second coupon of type

coupon in the final set if a coupon of each type has appeared before the second coupon of type  is obtained. Thus, letting

is obtained. Thus, letting  denote the time at which the second type

denote the time at which the second type  coupon is obtained, we have

coupon is obtained, we have

Using that  has a gamma distribution with parameters

has a gamma distribution with parameters  , this yields

, this yields

Therefore, we have the result

The next probability calculation related to Poisson processes that we shall determine is the probability that  events occur in one Poisson process before

events occur in one Poisson process before  events have occurred in a second and independent Poisson process. More formally let

events have occurred in a second and independent Poisson process. More formally let  and

and  be two independent Poisson processes having respective rates

be two independent Poisson processes having respective rates  and

and  . Also, let

. Also, let  denote the time of the

denote the time of the  th event of the first process, and

th event of the first process, and  the time of the

the time of the  th event of the second process. We seek

th event of the second process. We seek

Before attempting to calculate this for general  and

and  , let us consider the special case

, let us consider the special case  . Since

. Since  , the time of the first event of the

, the time of the first event of the  process, and

process, and  , the time of the first event of the

, the time of the first event of the  process, are both exponentially distributed random variables (by Proposition 5.1) with respective means

process, are both exponentially distributed random variables (by Proposition 5.1) with respective means  and

and  , it follows from Section 5.2.3 that

, it follows from Section 5.2.3 that

(5.16)

(5.16)

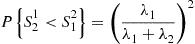

Let us now consider the probability that two events occur in the  process before a single event has occurred in the

process before a single event has occurred in the  process. That is,

process. That is,  . To calculate this we reason as follows: In order for the

. To calculate this we reason as follows: In order for the  process to have two events before a single event occurs in the

process to have two events before a single event occurs in the  process, it is first necessary for the initial event that occurs to be an event of the

process, it is first necessary for the initial event that occurs to be an event of the  process (and this occurs, by Equation (5.16), with probability

process (and this occurs, by Equation (5.16), with probability  ). Now, given that the initial event is from the

). Now, given that the initial event is from the  process, the next thing that must occur for

process, the next thing that must occur for  to be less than

to be less than  is for the second event also to be an event of the

is for the second event also to be an event of the  process. However, when the first event occurs both processes start all over again (by the memoryless property of Poisson processes) and hence this conditional probability is also

process. However, when the first event occurs both processes start all over again (by the memoryless property of Poisson processes) and hence this conditional probability is also  ; thus, the desired probability is given by

; thus, the desired probability is given by

In fact, this reasoning shows that each event that occurs is going to be an event of the  process with probability

process with probability  or an event of the

or an event of the  process with probability

process with probability  , independent of all that has previously occurred. In other words, the probability that the

, independent of all that has previously occurred. In other words, the probability that the  process reaches

process reaches  before the

before the  process reaches

process reaches  is just the probability that

is just the probability that  heads will appear before

heads will appear before  tails if one flips a coin having probability

tails if one flips a coin having probability  of a head appearing. But by noting that this event will occur if and only if the first

of a head appearing. But by noting that this event will occur if and only if the first  tosses result in

tosses result in  or more heads, we see that our desired probability is given by

or more heads, we see that our desired probability is given by

5.3.5 Conditional Distribution of the Arrival Times

Suppose we are told that exactly one event of a Poisson process has taken place by time  , and we are asked to determine the distribution of the time at which the event occurred. Now, since a Poisson process possesses stationary and independent increments it seems reasonable that each interval in

, and we are asked to determine the distribution of the time at which the event occurred. Now, since a Poisson process possesses stationary and independent increments it seems reasonable that each interval in  of equal length should have the same probability of containing the event. In other words, the time of the event should be uniformly distributed over

of equal length should have the same probability of containing the event. In other words, the time of the event should be uniformly distributed over  . This is easily checked since, for

. This is easily checked since, for  ,

,

This result may be generalized, but before doing so we need to introduce the concept of order statistics.

Let  be

be  random variables. We say that

random variables. We say that  are the order statistics corresponding to

are the order statistics corresponding to  if

if  is the

is the  th smallest value among

th smallest value among  ,

,  . For instance, if

. For instance, if  and

and  ,

,  ,

,  then

then  ,

,  . If the

. If the  , are independent identically distributed continuous random variables with probability density

, are independent identically distributed continuous random variables with probability density  , then the joint density of the order statistics

, then the joint density of the order statistics  is given by

is given by

(i) ( ) will equal (

) will equal ( ) if (

) if ( ) is equal to any of the

) is equal to any of the  ! permutations of (

! permutations of ( );

);

(ii) the probability density that ( ) is equal to

) is equal to  is

is  when

when  is a permutation of

is a permutation of  .

.

If the  , are uniformly distributed over

, are uniformly distributed over  , then we obtain from the preceding that the joint density function of the order statistics

, then we obtain from the preceding that the joint density function of the order statistics  is

is

We are now ready for the following useful theorem.

Theorem 5.2

Given that  , the

, the  arrival times

arrival times  have the same distribution as the order statistics corresponding to

have the same distribution as the order statistics corresponding to  independent random variables uniformly distributed on the interval

independent random variables uniformly distributed on the interval  .

.

Proof

To obtain the conditional density of  given that

given that  note that for

note that for  the event that

the event that  is equivalent to the event that the first

is equivalent to the event that the first  interarrival times satisfy

interarrival times satisfy  . Hence, using Proposition 5.1, we have that the conditional joint density of

. Hence, using Proposition 5.1, we have that the conditional joint density of  given that

given that  is as follows:

is as follows:

which proves the result.

Remark

The preceding result is usually paraphrased as stating that, under the condition that  events have occurred in

events have occurred in  , the times

, the times  at which events occur, considered as unordered random variables, are distributed independently and uniformly in the interval

at which events occur, considered as unordered random variables, are distributed independently and uniformly in the interval  .

.

Application of Theorem 5.2 (Sampling a Poisson Process)

In Proposition 5.2 we showed that if each event of a Poisson process is independently classified as a type I event with probability  and as a type II event with probability

and as a type II event with probability  then the counting processes of type I and type II events are independent Poisson processes with respective rates

then the counting processes of type I and type II events are independent Poisson processes with respective rates  and

and  . Suppose now, however, that there are

. Suppose now, however, that there are  possible types of events and that the probability that an event is classified as a type

possible types of events and that the probability that an event is classified as a type  event,

event,  , depends on the time the event occurs. Specifically, suppose that if an event occurs at time

, depends on the time the event occurs. Specifically, suppose that if an event occurs at time  then it will be classified as a type

then it will be classified as a type  event, independently of anything that has previously occurred, with probability

event, independently of anything that has previously occurred, with probability  where

where  . Upon using Theorem 5.2 we can prove the following useful proposition.

. Upon using Theorem 5.2 we can prove the following useful proposition.

Proposition 5.3

If  , represents the number of type

, represents the number of type  events occurring by time

events occurring by time  then

then  , are independent Poisson random variables having means

, are independent Poisson random variables having means

Before proving this proposition, let us first illustrate its use.

Example 5.18

An Infinite Server Queue

Suppose that customers arrive at a service station in accordance with a Poisson process with rate  . Upon arrival the customer is immediately served by one of an infinite number of possible servers, and the service times are assumed to be independent with a common distribution

. Upon arrival the customer is immediately served by one of an infinite number of possible servers, and the service times are assumed to be independent with a common distribution  . What is the distribution of

. What is the distribution of  , the number of customers that have completed service by time

, the number of customers that have completed service by time  ? What is the distribution of

? What is the distribution of  , the number of customers that are being served at time

, the number of customers that are being served at time  ?

?

To answer the preceding questions let us agree to call an entering customer a type I customer if he completes his service by time  and a type II customer if he does not complete his service by time

and a type II customer if he does not complete his service by time  . Now, if the customer enters at time

. Now, if the customer enters at time  , then he will be a type I customer if his service time is less than

, then he will be a type I customer if his service time is less than  . Since the service time distribution is

. Since the service time distribution is  , the probability of this will be

, the probability of this will be  . Similarly, a customer entering at time

. Similarly, a customer entering at time  , will be a type II customer with probability

, will be a type II customer with probability  . Hence, from Proposition 5.3 we obtain that the distribution of

. Hence, from Proposition 5.3 we obtain that the distribution of  , the number of customers that have completed service by time

, the number of customers that have completed service by time  , is Poisson distributed with mean

, is Poisson distributed with mean

(5.17)

(5.17)

Similarly, the distribution of  , the number of customers being served at time

, the number of customers being served at time  is Poisson with mean

is Poisson with mean

(5.18)

(5.18)

Furthermore,  and

and  are independent.

are independent.

Suppose now that we are interested in computing the joint distribution of  and

and  —that is, the joint distribution of the number in the system at time

—that is, the joint distribution of the number in the system at time  and at time

and at time  . To accomplish this, say that an arrival is

. To accomplish this, say that an arrival is

type 1: if he arrives before time  and completes service between

and completes service between  and

and  ,

,

type 2: if he arrives before  and completes service after

and completes service after  ,

,

type 3: if he arrives between  and

and  and completes service after

and completes service after  ,

,

Hence, an arrival at time  will be type

will be type  with probability

with probability  given by

given by

Thus, if  , denotes the number of type

, denotes the number of type  events that occur, then from Proposition 5.3,

events that occur, then from Proposition 5.3,  , are independent Poisson random variables with respective means

, are independent Poisson random variables with respective means

Because

it is now an easy matter to compute the joint distribution of  and

and  . For instance,

. For instance,

where the last equality follows since the variance of a Poisson random variable equals its mean, and from the substitution  . Also, the joint distribution of

. Also, the joint distribution of  and

and  is as follows:

is as follows:

Example 5.19

A One Lane Road with No Overtaking

Consider a one lane road with a single entrance and a single exit point which are of distance  from each other (See Figure 5.2). Suppose that cars enter this road according to a Poisson process with rate

from each other (See Figure 5.2). Suppose that cars enter this road according to a Poisson process with rate  , and that each entering car has an attached random value

, and that each entering car has an attached random value  which represents the velocity at which the car will travel, with the proviso that whenever the car encounters a slower moving car it must decrease its speed to that of the slower moving car. Let

which represents the velocity at which the car will travel, with the proviso that whenever the car encounters a slower moving car it must decrease its speed to that of the slower moving car. Let  denote the velocity value of the

denote the velocity value of the  th car to enter the road, and suppose that

th car to enter the road, and suppose that  are independent and identically distributed and, in addition, are independent of the counting process of cars entering the road. Assuming that the road is empty at time

are independent and identically distributed and, in addition, are independent of the counting process of cars entering the road. Assuming that the road is empty at time  , we are interested in determining

, we are interested in determining

(a) the probability mass function of  the number of cars on the road at time

the number of cars on the road at time  ; and

; and

(b) the distribution of the road traversal time of a car that enters the road at time  .

.

Solution: Let  denote the time it would take car

denote the time it would take car  to travel the road if it were empty when car

to travel the road if it were empty when car  arrived. Call

arrived. Call  the free travel time of car

the free travel time of car  , and note that

, and note that  are independent with distribution function

are independent with distribution function

Let us say that an event occurs each time that a car enters the road. Also, let  be a fixed value, and say that an event that occurs at time

be a fixed value, and say that an event that occurs at time  is a type

is a type  event if both

event if both  and the free travel time of the car entering the road at time

and the free travel time of the car entering the road at time  exceeds

exceeds  . In other words, a car entering the road is a type

. In other words, a car entering the road is a type  event if the car would be on the road at time

event if the car would be on the road at time  even if the road were empty when it entered. Note that, independent of all that occurred prior to time

even if the road were empty when it entered. Note that, independent of all that occurred prior to time  an event occurring at time

an event occurring at time  is a type

is a type  event with probability

event with probability

Letting  denote the number of type

denote the number of type  events that occur by time

events that occur by time  , it follows from Proposition 5.3 that

, it follows from Proposition 5.3 that  is, for

is, for  a Poisson random variable with mean

a Poisson random variable with mean

Because there will be no cars on the road at time  if and only if

if and only if  it follows that

it follows that

To determine  for

for  we will condition on when the first type

we will condition on when the first type  event occurs. With

event occurs. With  equal to the time of the first type

equal to the time of the first type  event (or to

event (or to  if there are no type

if there are no type  events), its distribution function is obtained by noting that

events), its distribution function is obtained by noting that

thus showing that

Differentiating gives the density function of  :

:

To use the identity

(5.19)

(5.19)

note that if  then the leading car that is on the road at time

then the leading car that is on the road at time  entered at time

entered at time  Because all other cars that arrive between

Because all other cars that arrive between  and

and  will also be on the road at time

will also be on the road at time  , it follows that, conditional on

, it follows that, conditional on  the number of cars on the road at time

the number of cars on the road at time  will be distributed as

will be distributed as  plus a Poisson random variable with mean

plus a Poisson random variable with mean  Therefore, for

Therefore, for

Substituting this into Equation (5.19) yields

(b) Let  be the free travel time of the car that enters the road at time

be the free travel time of the car that enters the road at time  and let

and let  be its actual travel time. To determine

be its actual travel time. To determine  let

let  and note that

and note that  will be less than

will be less than  if and only if both

if and only if both  and there have been no type

and there have been no type  events (using

events (using  ) before time

) before time  . That is,

. That is,

Because  is independent of what has occurred prior to time

is independent of what has occurred prior to time  , the preceding gives

, the preceding gives

Example 5.20

Tracking the Number of HIV Infections

There is a relatively long incubation period from the time when an individual becomes infected with the HIV virus, which causes AIDS, until the symptoms of the disease appear. As a result, it is difficult for public health officials to be certain of the number of members of the population that are infected at any given time. We will now present a first approximation model for this phenomenon, which can be used to obtain a rough estimate of the number of infected individuals.

Let us suppose that individuals contract the HIV virus in accordance with a Poisson process whose rate  is unknown. Suppose that the time from when an individual becomes infected until symptoms of the disease appear is a random variable having a known distribution

is unknown. Suppose that the time from when an individual becomes infected until symptoms of the disease appear is a random variable having a known distribution  . Suppose also that the incubation times of different infected individuals are independent.

. Suppose also that the incubation times of different infected individuals are independent.

Let  denote the number of individuals who have shown symptoms of the disease by time

denote the number of individuals who have shown symptoms of the disease by time  . Also, let

. Also, let  denote the number who are HIV positive but have not yet shown any symptoms by time

denote the number who are HIV positive but have not yet shown any symptoms by time  . Now, since an individual who contracts the virus at time

. Now, since an individual who contracts the virus at time  will have symptoms by time

will have symptoms by time  with probability

with probability  and will not with probability

and will not with probability  , it follows from Proposition 5.3 that

, it follows from Proposition 5.3 that  and

and  are independent Poisson random variables with respective means

are independent Poisson random variables with respective means

and

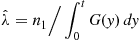

Now, if we knew  , then we could use it to estimate

, then we could use it to estimate  , the number of individuals infected but without any outward symptoms at time

, the number of individuals infected but without any outward symptoms at time  , by its mean value

, by its mean value  . However, since

. However, since  is unknown, we must first estimate it. Now, we will presumably know the value of

is unknown, we must first estimate it. Now, we will presumably know the value of  , and so we can use its known value as an estimate of its mean

, and so we can use its known value as an estimate of its mean  . That is, if the number of individuals who have exhibited symptoms by time

. That is, if the number of individuals who have exhibited symptoms by time  is

is  , then we can estimate that

, then we can estimate that

Therefore, we can estimate  by the quantity

by the quantity  given by

given by

Using this estimate of  , we can estimate the number of infected but symptomless individuals at time

, we can estimate the number of infected but symptomless individuals at time  by

by

For example, suppose that  is exponential with mean

is exponential with mean  . Then

. Then  , and a simple integration gives that

, and a simple integration gives that

If we suppose that  years,

years,  years, and

years, and  thousand, then the estimate of the number of infected but symptomless individuals at time 16 is

thousand, then the estimate of the number of infected but symptomless individuals at time 16 is

That is, if we suppose that the foregoing model is approximately correct (and we should be aware that the assumption of a constant infection rate  that is unchanging over time is almost certainly a weak point of the model), then if the incubation period is exponential with mean 10 years and if the total number of individuals who have exhibited AIDS symptoms during the first 16 years of the epidemic is 220 thousand, then we can expect that approximately 219 thousand individuals are HIV positive though symptomless at time 16.

that is unchanging over time is almost certainly a weak point of the model), then if the incubation period is exponential with mean 10 years and if the total number of individuals who have exhibited AIDS symptoms during the first 16 years of the epidemic is 220 thousand, then we can expect that approximately 219 thousand individuals are HIV positive though symptomless at time 16.

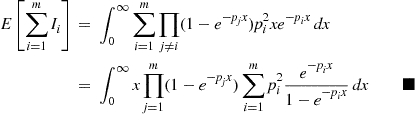

Proof of Proposition 5.3

Let us compute the joint probability  . To do so note first that in order for there to have been

. To do so note first that in order for there to have been  type

type  events for

events for  there must have been a total of

there must have been a total of  events. Hence, conditioning on

events. Hence, conditioning on  yields

yields

Now consider an arbitrary event that occurred in the interval  . If it had occurred at time

. If it had occurred at time  , then the probability that it would be a type

, then the probability that it would be a type  event would be

event would be  . Hence, since by Theorem 5.2 this event will have occurred at some time uniformly distributed on

. Hence, since by Theorem 5.2 this event will have occurred at some time uniformly distributed on  , it follows that the probability that this event will be a type

, it follows that the probability that this event will be a type  event is

event is

independently of the other events. Hence,

will just equal the multinomial probability of  type

type  outcomes for

outcomes for  when each of

when each of  independent trials results in outcome

independent trials results in outcome  with probability

with probability  . That is,

. That is,

Consequently,

and the proof is complete.