2 Public/private research partnerships

This chapter begins with a discussion of the economic concept of market failure as the theoretical mandate for public sector intervention into private sector activities. The concept of market failure is the justification offered for public sector support of science and technology, or R&D, such as, in the present study, for battery technologies for electric drive vehicles. Then, having offered an economic argument for DOE’s investments in battery storage technologies to be utilized in the private sector, the relationship between DOE and the private sector is described in terms of a public/private partnership.

Market failure and private investments in R&D

Market failure describes a situation where market forces lead to an inefficient allocation of resources from a social perspective. Public investments in science and technology (or R&D) are justified in principle by their potential to correct market failures involving underinvestment by the private sector in basic and applied research and the development and commercialization of new technology. Martin and Scott (2000, p. 438) observe about market failure:

Limited appropriability, financial market failure, external benefits to the production of knowledge, and other factors suggest that strict reliance on a market system will result in underinvestment in innovation, relative to the socially desirable level. This creates a prima facie case in favor of public intervention to promote innovative activity.

These and other factors contributing to private-sector underinvestment in R&D (termed barriers to technology and innovation) have been elaborated on by Link and Scott (2010); thus, only a brief overview follows.1

First, the social rate of return to R&D investment is likely to exceed the private rate of return for several reasons. The scope of potential markets for new technology is often broader than the market strategy of any one firm, making it unlikely that one firm could appropriate (even if it could envision) all of the social returns to its R&D, particularly for activities that tend toward the more basic end of the research spectrum. Knowledge and ideas generated by one firm’s R&D investments will often spill over to other firms, both rivals competing in the same markets and (because of the breadth of application for new technology) firms in unrelated markets. Such spillovers are socially valuable but not privately rewarding to the firm making the R&D investment. A firm may also anticipate some amount of opportunism by potential buyers of the new technology it develops; a potential buyer may learn enough about the new technology, in the process of making its decision whether to buy, that it can invent around any intellectual property protections and acquire the value of the new technology without paying for it.2

Second, the private hurdle rate (the expected rate of private return that an R&D investment must meet to be deemed worthwhile to the firm) is likely to be higher than the social hurdle rate (the opportunity costs of the public’s investment funds). Given the technical and commercial risks associated with R&D investments (will the R&D achieve certain technical criteria and will the market embrace the resulting innovation?), owners and lenders who provide the investment capital for R&D will generally require a higher risk premium than will society, if for no other reason than that society can spread its R&D investments over a larger portfolio. Even small differences between the private and social costs of investment capital (in terms of a required annual expected rate of return) can lead to substantial differences between the private and social net present values of R&D projects when there is a long lag between the time that investments are made and the time that returns are realized. For example, assuming a 10 percent private and 5 percent social cost of capital, the ratio of private to social present value of a future return is 0.79 five years into the future, 0.63 ten years out, and 0.39 twenty years out.3

Figure 2.1 illustrates the implications of these two observations – that social returns to R&D investments typically exceed private returns and that private hurdle rates typically exceed social hurdle rates – for public policy decisions involving R&D investment.4 R&D projects for which the social rate of return exceeds the private rate of return lie above the 45-degree line in Regions I, II, and III. Projects in Region I are neither privately nor socially valuable: their rate of return is less than the hurdle rate from both the private and social perspective. Projects in Region II (like Project A) are good candidates for public investment: the social rate of return for these projects exceeds the social hurdle rate, and their private rate of return falls short of the private hurdle rate – meaning that these projects are socially valuable but unlikely to be undertaken by the private sector. Projects in Region III (like Project B) are socially valuable but poor candidates for public investment: since the private rate of return to these projects exceeds the private hurdle rate, we would expect them to be undertaken by the private sector; public investment in such projects would only crowd out the private investment.

Conflated in the private and social rates of return are the returns themselves – the streams of private and social gains ensuing from an investment in R&D – and the costs – the streams of R&D expenditure. The reasons given above for why the social rate of return may exceed the private rate of return focused on the arguably more straightforward reasons why the streams of social returns may be greater than the streams of private returns. In fact there are also compelling arguments for why public investments in R&D, especially in collaboration with private-sector partners, may lower the expected cost of achieving a given R&D outcome. A successful R&D effort may, for example, require (Link and Scott, 2010, p. 9):

Decision-making model for public R&D investments |

multidisciplinary and multiskilled research teams; unique research facilities not generally available within individual firms; or fusing technologies (i.e., technologies used together or sequentially) from heretofore separate, noninteracting parties [or] investments in combinations of technologies that, if they existed, would reside in different industries that are not integrated.

In such cases (Link and Scott, 2010, p. 10):

[u]nderinvestment will occur not only because of the lack of recognition of possible benefit areas or the perceived inability to appropriate whatever results but also because coordinating multiple players in a timely and efficient manner is cumbersome and costly.… [S]ociety may be able to use a technology-based public institution to act as an honest broker and reduce costs below those that the market would face.

The argument for public investment in R&D to bring forth new technologies that improve environmental outcomes is especially strong because of the negative externalities associated with pollution (Jaffe et al., 2005). In the case of battery technology for electric drive vehicles, drivers underappreciate the social value of the more fuel-efficient technology because the price they pay at the pump does not fully reflect the social opportunity cost of gasoline; namely, the price of gasoline does not reflect the cost of the associated pollution. Therefore, the gap between the private and social returns to R&D investments in technologies that improve vehicle fuel efficiency, including the battery technologies considered in this book, is likely to be especially large.

A public/private partnership model

Consider the following definition of aspects of a public/private partnership model. Link (1999) first proposed this definition and then Link and Link (2009, p. 32) elaborated on it:

The term public refers to any aspect of the innovation [and technology development] process that involves the use of governmental [i.e., public-sector] resources, be they federal, state, or local in origin. Private refers to any aspect of the innovation [or technology development] process that involves the use of private-sector resources, mostly firm-specific resources. And, resources are broadly defined to include all resources – financial resources, infrastructural resources, research resources, and the like – that affect the general environment in which innovation [or technology development] occurs. Finally, the term partnership refers to any and all innovation-related [and technology-development-related] relationships, including but not limited to formal and informal collaborations or partnerships in R&D.

The framework that defines our view of a public/private partnership is described in Table 2.1. The first column of the table describes the nature and scope of the public sector’s involvement in the partnership. The public sector’s involvement can be indirect or direct, and if direct there could be an explicit allocation of public resources including financial, infrastructural, and/or research resources. The second and third columns in the table relate to the economic objectives of the public/private partnership. Broadly, the objectives are either to leverage public-sector R&D activity or to leverage private-sector R&D activity. Although the objectives of innovative activity are often multifactorial, for illustrative purposes, one single overriding economic objective is assumed here.

Taxonomy of public/private partnership mechanisms and structures |

Economic objective |

||

Public sector involvement |

Leverage public-sector R&D |

Leverage private-sector R&D |

Indirect |

… |

… |

Direct |

||

Financial resources |

… |

… |

Infrastructural resources |

… |

… |

Research resources |

… |

… |

Public resources involved in battery technology R&D, or more precisely energy storage R&D, came from the VTO. These resources are direct. VTO’s financial contributions are shown in Figure 1.1 to have begun in 1976. But also, significant research on battery technology occurs at DOE’s national laboratories so there is an infrastructural resource and research resource contribution as well.

Regarding private resources, an important part of VTO’s support for NiMH and Li-ion battery technologies was the funding of U.S. Advanced Battery Consortium (USABC). USABC shared the cost of contracts to private-sector companies to conduct in-house research on battery technology.5

DOE’s Office of Transportation Technologies (OTT) managed USABC’s contracts to private companies; these contracts were awarded through a competitive process. The OTT also managed Cooperative Research and Development Agreements (CRADAs) with DOE’s national laboratories.6 These CRADAs often focused on developing test procedures and evaluating batteries developed in the USABC program.

A research director with a company that now manufacturers Li-ion batteries for EDVs described the company’s present chemistry as being a direct result of interaction with DOE, through USABC, and emphasized the importance of this interaction in leveraging for vehicle applications the company’s prior work on smaller platforms: cell phones and laptops, where (to paraphrase) “the protocols and formalisms used to test the batteries are entirely different.” As an example, “the development of vehicle batteries requires you to think of a 10–15 year lifespan compared to 1–3 years for cell phones and laptops.” To paraphrase another respondent, “uniform technical targets for vehicle-batteries were set by the USABC program and these formed the basis for several of the manufacturers and original equipment manufacturers (OEMs) to develop battery chemistries that are durable through the life of the vehicle.” In the words of another, “without the VTP push for cycle and calendar life, there was very little incentive for the battery to reach 3000 cycles and a 10-year life; consumer electronics require only 500 cycles and a 2-year life, and can tolerate high price.”

Other respondents emphasized the importance of USABC in developing human capital in the United States. One industry respondent said, “DOE funding has led not only to technical breakthroughs but has also led to an accumulation of human capital and expertise in the U.S., which would not exist at all without DOE funding; without the DOE, the advancements that have been made in U.S. industry and government and university labs over the past 20 years would have taken 30 years longer – what has taken 20 years would have taken 50 without DOE.”7 Said another respondent, “without VTP, a whole generation of battery scientists would have been lost, given the state of funding for battery research in the 1990s; although the funding level was still low, at least it was maintained, and when interest in batteries exploded in the mid-2000s, those students, who had by then taken jobs at universities and companies, were there to re-ignite the research in the U.S.”

As shown in Figure 2.2, DOE invested $315 million in 2012 dollars in energy storage technologies through its funding of USABC contracts from 1992 through 2010 (2010 is the last year of available information on USABC contracts). Private-sector R&D investment amounted to an additional $358 million in 2012 dollars over the same period.

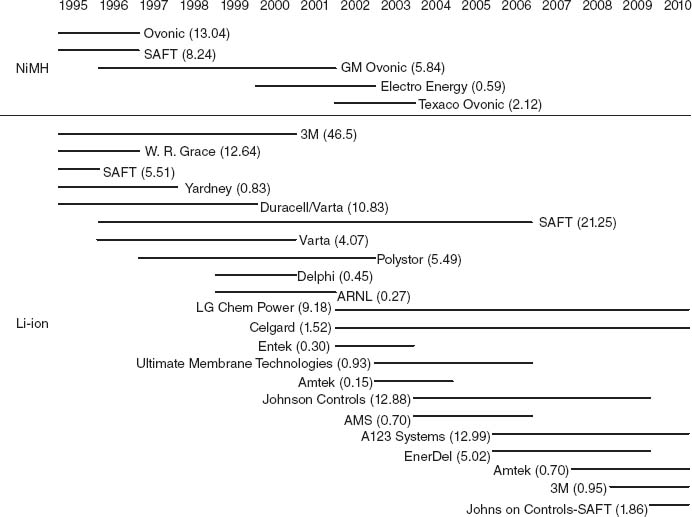

Approximately 9 percent of VTO’s total USABC R&D investments supported NiMH battery research. U.S. companies receiving support for NiMH R&D included: Energy Conversion Devices, Inc. (ECD), also known as ECD Ovonic; Ovonic Battery Company, Inc., a subsidiary of ECD Ovonic; GM Ovonic, a joint venture between GM and Ovonic Battery Company; Texaco Ovonic Battery Systems, a joint venture between Texaco and Ovonic Battery Company (Texaco acquired GM’s interest); and Cobasys LLC, a joint venture between Chevron and Ovonic Battery Company (Chevron acquired Texaco’s interest). To paraphrase one industry respondent, “NiMH technology was around in the 1980s, but not until the 1990s did Ovonic start scaling up for large capacity suitable for vehicle applications; Ovonic was a small company and could not have done what it did without DOE and USABC.”

Cumulative USABC R&D investments in energy storage technologies, 1992 through 2010 |

Approximately 50 percent of VTO’s total USABC investments supported Li-ion battery research. U.S. companies receiving support for NiMH battery research included: 3M; Johnson Controls; Saft; Johnson Controls/Saft (JCS), a joint venture between Johnson Controls and Saft; A123Systems; and LG Chem Power Inc., a North American subsidiary of LG Chem Ltd. See Figure 2.3 for a visual description of the timeline for VTO’s support of these companies. To paraphrase one respondent, whose work in industry had leveraged research performed in government laboratories,

the impact of VTO funding has been significant in that it allowed the emergence of new types of materials that would enhance the energy density of Li-ion batteries; without VTO funding, the work that Argonne National Labs and Lawrence Berkeley Labs have done on new materials would not have been possible; VTP funding has firmly established the battery industry in the U.S. right now, so that battery manufacturing can happen in the U.S. – plants are being built, machinery has been installed, and the U.S. can be a credible supplier of batteries for vehicle applications.

Another industry respondent said of VTO’s impact, “without DOE, there would be essentially no U.S. industry; technology would still have been developed abroad in Japan and Korea, for example, and EDVs would still have made their way into the U.S. market, but it would have taken longer – perhaps 10 years longer – to get to where we are today, and there would presently be no Li-ion batteries on the road.”

In addition to funding the private sector for research on battery technologies, USABC’s support of private-sector research established what have become the standardized performance metrics for batteries. See Table 2.2 for definitions of these performance metrics.

Thus, the public/private partnership framework in Table 2.1 can be filled in to reflect the resource contribution of the public sector (i.e., VTO) and the private sector (i.e., recipient companies through USABC); see Table 2.3.

Table 2.3 shows that DOE’s role in the public/private partnership to support the development of new battery technology, NiMH and Li-ion battery technologies in particular, was direct. DOE, and VTO in particular, contributed financial, infrastructural, and research resources to leverage private-sector R&D. In addition, DOE provided direct financial support to leverage ongoing battery technology research at the national laboratories.

This framework for the mechanisms and structure of a public/private partnership complements an earlier conceptualization by the Office of Technology Policy (OTP, 1996). The OTP’s taxonomy classified public/private partnerships in the United States at two undefined points of transition to emphasize the evolution of the government’s role – from that of a customer of private-sector research to that of a partner in that research. Specifically:

VTO’s R&D investments for NiMH and Li-ion battery technologies, by company, 1995 through 2010 (millions $) |

Metric |

Definition |

Specific energy (Wh/kg) |

A measure of the total energy density of the battery pack per unit weight. It provides an indication of the vehicle range. Total energy is analogous to the size of the gas tank on a conventional, combustion-engine-powered automobile. This metric is important for EV batteries because added mass requires more energy to move. |

Energy density (Wh/L) |

A measure of the total energy stored in the battery pack per unit volume. This metric is important in portable electronics where size is often limited. |

Specific power (W/kg) |

A measure of the total power that can be delivered per unit weight. Power, which is energy divided by the time it is delivered, translates to the acceleration ability of the source. In EVs, power is limited by how fast the energy in a battery pack can be delivered to motors or electrical circuitry. |

Power density (W/L) |

A measure of the total power per unit volume of the battery pack that can be delivered in a short burst of time such as during acceleration. |

Life (years) |

An engineering estimate of the expected time that an EV battery pack can be fully charged and discharged and maintain a specified capacity threshold. Some degradation in the pack’s specific energy occurs over time, and the battery needs to be replaced when its capacity falls below a specified percentage of the original value. |

Cycle life (cycles) |

The number of times a battery pack can be charged and discharged. Each charge-discharge event constitutes one cycle. Typically cycle life is related to the depth of discharge (DOD) of the battery pack. Deep discharge and charge cycles will lower cycle life. |

Ultimate price ($/kWh) |

The cost of a battery pack in dollars divided by the total energy that is contained (in kWh) in a single charge of the battery. |

Operating environment |

The environmental conditions under which the battery pack is expected to operate. The operating environment usually consists of a lower temperature limit and an upper temperature limit. Batteries typically do not operate in extremely cold conditions and may exhibit reduced performance or become unsafe at high temperatures. |

Capacity |

The total energy stored in the battery, usually expressed in kWh. |

Recharge time (hours) |

The time that it takes to recharge the battery to a predetermined acceptable level. Recharge time is often expressed as C rate. A recharge rate of 1C implies that the full capacity of the battery can be restored after 1 hour of charging, whereas a recharge rate of 0.1C implies that it takes roughly 10 hours to fully charge the battery pack. |

Continuous discharge in 1 hour |

Energy delivered in a constant power discharge required by an EV for hill climbing and high-speed cruising, specified as the percentage of energy capacity delivered in a 1-hour constant power discharge. |

Power and capacity degradation |

Performance degradation defines the extent to which the battery system is unable to meet the original performance specification. |

Note: Wh = watt-hours, L = liter, kg = kilogram.

DOE’s role in the public/private partnership to support battery technology |

Economic objective |

||

Public sector involvement |

Leverage Public-sector R&D |

Leverage Private-sector R&D |

Indirect |

… |

… |

Direct |

||

Financial resources |

yes |

yes |

Infrastructural resources |

… |

yes |

Research resources |

… |

yes |

By the late 1980s, a new paradigm of technology policy had developed. In contrast to the enhanced spin-off programs – enhancements that made it easier for the private sector to commercialize the results of mission R&D – the government developed new public-private partnerships to develop and deploy advanced technologies.… [T]hese new programs … incorporate features that reflect increased influence from the private sector over project selection, management, and intellectual property ownership. Along with increased input, private sector partners also absorb a greater share of the costs, in some cases paying over half of the project cost.… The new paradigm has several advantages for both government and the private sector. By treating the private sector as a partner in federal programs, government agencies can better incorporate feedback and [thus] focus programs. Moreover, the private sector as partner [emphasis added] approach allows the government to measure whether the programs are ultimately meeting their goals: increasing research efficiencies and effectiveness and developing and deploying new technologies.

(OTP, 1996, pp. 33–34)

Innovative paradigm for a public/private technology partnership |

Source: Based on Office of Technology Policy (1996, p. 34).

Figure 2.4 illustrates this OTP view. There are several salient features in Figure 2.4. First, the federal government has changed from being a customer for the technology output of industry programs, which it often financed, to a partner, and often a research partner, in the programs. And second, not only does this role change increase the ability of industry to focus its efforts more efficiently on government needs, but also it speeds up the technology diffusion process.

In the following chapter we introduce advancements in NiMH and Li-ion battery technologies that resulted from VTO’s R&D support of those technologies. We argue that improvements in the performance characteristics of the state-of-the-art technology have translated over time into the commercial availability of EDVs and the subsequent market adoption of EDVs. Chapter 3 summarizes the market adoption of NiMH and Li-ion battery technologies through the purchase of EDVs in the United States beginning in 1999. This summary then becomes the benchmark for the evaluation analysis that follows in later chapters.

Notes

1 The discussion of specific barriers to innovation and technology by Link and Scott (2010, pp. 8–11) follows the foundational work of Kenneth Arrow (1962, p. 609), which pointed out that invention, or the production of knowledge, is characterized by “three of the classical reasons for the possible failure of perfect competition to achieve optimality in resource allocation: indivisibilities, inappropriability, and uncertainty.”

2 Potential buyers, for their part, may worry that the seller of a new technology may learn enough about the buyer’s operations that it could “back away from the transfer and instead enter the buyer’s industry as a technologically sophisticated competitor” (Link and Scott, 2010, p. 11).

3 Taking the cost of capital (as a required annual rate of return) to be r, the present value of a return, x, realized t years into the future, is x/(1+r)t. Thus the ratio of private to social present value in our example is (1.05/1.1)t.

4 Figure 2.1 is adapted from Link and Scott (2010, p. 6) and Jaffe (1998, p. 16).

5 USABC investments in NiMH and Li-ion technology began in earnest in 1995. However, USABC was established in 1991 and served as a model for other public/private partnerships that came after. Most notable among these in the U.S. automotive industry was the Partnership for a New Generation of Vehicles (PNGV), launched in 1993 by the Clinton Administration and the “Big Three” U.S. automakers: Ford, Chrysler, and General Motors. See Sperling (2001) and Trinkle (2009). Trinkle notes that “not only did USABC and other consortia precede PNGV, but their preexistence facilitated its conception and implementation” (p. 55).

6 The Stevenson-Wydler Technology Innovation Act of 1980, Public Law 96-480, called for federal laboratories to actively promote technology transfer to the private sector for commercial exploitation. In 1986, the Stevenson-Wydler Act was amended by the Federal Technology Transfer Act of 1986, Public Law 99-502, to, among other things, enable the laboratories to enter into CRADAs with outside organizations or parties:

Each Federal agency may permit the director of any of its Government-operated Federal laboratories – (1) to enter into cooperative research and development state and local agreements on behalf of such agency … with other Federal agencies; units of State or local government; industrial organizations (including corporations, schools and partnerships, and limited partnerships, and industrial development organizations); public and private foundations; nonprofit organizations (including universities); or other persons (including licensees of inventions owned by the Federal agency); and (2) to negotiate licensing agreements.…

In subsequent legislation, the activities that fall under a CRADA and related licensing arrangements were expanded. These legislations included the National Competitiveness Technology Transfer Act of 1989, Public Law 101-189; the National Technology Transfer and Advancement Act of 1995, Public Law 104-113; and the Technology Transfer Commercialization Act of 2000, Public Law 106-404.

7 In this, as in all instances where quotation marks are applied to the comments of interview respondents, only paraphrasing is implied.