Make the most of global bargains.

“It is optimism that is the enemy of the rational buyer.”

—WARREN BUFFETT

THE ANNALS OF GLOBAL ACQUISITIONS ARE FILLED WITH failure: megadeals that ended up costing shareholders dearly because of the premium paid, the difficulties at realizing expected synergies, and other postmerger integration issues. While merging balance sheets is straightforward, making two corporate cultures work together is a different story. Many companies have treated acquisitions as ends in themselves, rather than as a means to an end. As Warren Buffett observed, optimism is rampant when a company announces the acquisition of another. The euphoria, however, often ends in disappointment not only because of unwarranted expectations as to the potential benefits but also because of the lack of attention to postacquisition restructuring and integration. Sara Lee famously bought and sold companies without going through the more time-consuming process of improving the management of the acquired assets. Meanwhile, Bimbo, as we have seen, overtook Sara Lee by fixating on operational performance.

The history of acquisitions is not entirely bleak. Established multinationals such as Nestlé, Unilever, and Procter & Gamble have effectively used acquisitions to become not just bigger but more efficient and better serving of their customers. By and large, though, old-line corporate behemoths from developed countries tend to assume a know-it-all attitude toward the companies they acquire and to impose their own hierarchy and culture. They fail to understand that the goal is to learn, not dominate. That was the utterly counterproductive attitude that Ford adopted after acquiring Volvo’s car division in 1999 for $6.45 billion. Detroit’s number two failed to make the most out of the acquisition, selling it to China’s Geely Group for a mere $1.8 billion in 2010.

Geely chairman Li Shufu is determined not to make the same mistake: “After the takeover, Geely remains Geely, and Volvo is still Volvo. The relationship between the two companies is brotherhood and not a parent-and-child relationship.”1

Ford made similar mistakes after acquiring Jaguar for $2.5 billion in 1989 and Land Rover for $2.7 billion in 2000. After years of mismanagement, Ford sold the companies in 2007 to Tata Motors of India for just $2.3 billion. In both cases, emerging market multinationals were waiting in the wings to take advantage of Ford’s failures.

American firms are not alone in thinking they can manage anything they acquire. Ford did not buy Land Rover from its original owner but from Germany’s BMW, which had also failed to make good of its own acquisition of the entire Rover group over a period of six years. German automakers are indisputably among the best in the world when it comes to engineering and performance, but acquiring other companies is definitely not their forte. In yet another epic example, Daimler merged in 1998 with Chrysler to form DaimlerChrysler. The deal was valued at a whopping $37 billion. The German side was meant to predominate from the start—and so it did, to the point of stifling Chrysler’s ability to compete. After nearly a decade of disappointing results, Daimler sold Chrysler to Cerberus, the private equity group, for $7.4 billion, which in turn passed Chrysler on to Italy’s Fiat in 2009. The deal involved a $12 billion government bailout and a 20 percent equity stake for Fiat in exchange for no cash at all. The Italian firm later raised its stake to almost 54 percent, a serious blow to shareholder value since Fiat did not contribute any new funds. Only time will tell whether the Italians are better than the Germans at managing an acquired company.

So are global acquisitions a bad idea, something to be avoided? Obviously not. While the traditional corporate landscape is littered with failed deals, many of the most high-profile emerging market multinationals have grown more sophisticated and prospered precisely through their acquisitions. Here’s the difference: the new multinationals acquire smart—precisely in the two meanings implied. First, they engage in acquisitions to make up for shortcomings in their resources and capabilities, frequently acquiring brands, technologies, or other types of proprietary skills. Second, they choose their targets intelligently, with the intention of advancing their international presence as opposed to making headlines or breaking the record established in a previous megamerger.

Below, case studies of how Tenaris, Cemex, and Tata Communications used smart acquisitions to become leading companies in their respective industries.

What’s the home base of the largest and most sophisticated firm in the cryptic but enormously important industry called “oil country tubular goods”? Germany? Japan or the United States? No. The answer, improbably enough, is Argentina. With a 30 percent share of the global OCTG market and 20 percent of the highly sophisticated market for seamless steel pipes, Tenaris has become one of the world’s most admired companies, ahead of competitors such as IPSCO, JFE Holdings, Lone Star Technologies, and Sumitomo Metal Industries. In 2011, Paolo Rocca, grandson of the founder, received the 2011 Steelmaker of the Year award at the annual Association for Iron & Steel Technology conference held in Indianapolis for “his dynamic and diverse leadership in the manufacturing of steel, most notably for the production of quality pipe and tube to support the world’s energy infrastructure.”2

The origins of Tenaris go back to 1909, when a company then named Dalmine began making steel pipes in Italy. In 1935, Agostino Rocca became managing director. A decade later, Rocca used the experience he had accumulated at Dalmine to launch, along with his son Roberto, a similar enterprise he called Techint. Soon thereafter, father and son moved to Argentina, a chronically unstable country where half of the population came from Italy’s poorest regions and the other from Spain’s—the only country in the world with such a demographic composition.

In 1954, Agostino founded Siderca, his first company solely devoted to seamless steel tubes, and added that to the Techint portfolio. During the 1960s, 1970s, and 1980s the company suffered through Argentina’s endless boom-and-bust cycles, choosing to diversify into related and unrelated industries as a way to cope with uncertainty and chaos. The firm grew into fields such as machinery, engineering, construction, turnkey plant design and construction, oil and gas exploration and production, flat and pressed glass, paper, cement and ceramic tiles, and a bewildering assortment of privatized firms, including sanitary services, railways, toll highways, telecommunications, gas transportation and distribution, power generation, and even correctional facilities. Techint became a true conglomerate.

In the mid-1990s, thanks to the brief period of monetary stability afforded by peso-dollar convertibility, Techint decided to refocus on steel and build a global presence. In 1993 it acquired Mexico’s Tamsa, and in 1998 Italy’s Dalmine, thus circling back to Techint’s own roots. Rechristened DST—from Dalmine, Siderca, and Tamsa—the new company was now the largest OCTG producer in the world. In the following two years it consolidated its leadership position by buying Tavsa in Venezuela and Confab in Brazil. Later, it acquired Maverick Tube Corp. in the United States and Jaya in Indonesia, and in 2011 Brazil’s Usiminas. These acquisitions together with joint ventures in Canada, Japan, and China enabled Tenaris to make coiled tubing, drill pipe, pipe casings, and oil pipes in Argentina, Brazil, Canada, Mexico, the United States, Italy, Saudi Arabia, China, Japan, and Indonesia, with service centers in an additional 20 countries. In 2001, DST changed its name to Tenaris, a variation on the Latin word tenax, the root of (appropriately enough) tenacious. The company is listed on the NYSE as well as in Milan, Buenos Aires, and Mexico City. While incorporated in Luxembourg, its top management and most of its R&D sit in Argentina.

Unlike many companies, Tenaris does not see acquisitions as a raid but as a stepping-stone into profitability. “If we see a target that could enhance our ability to corner a market segment, we will pursue that acquisition,” present CEO Paolo Rocca said. “We keep profitability in mind over expansion.”3 Expansion, in fact, proved the way to profitability in the seamless tubing industry in which customers (i.e., oil companies) are increasingly global in their operations and consolidation of producers is rampant because of overcapacity. While Tenaris thought of acquisitions as the way to succeed under such circumstances, its main competitors stayed still. Several of them (IPSCO and Lone Star Technologies, for example) became prey to larger steel companies.

Tenaris’s strategy is built on the premise that the company with the most extensive and integrated global network wins.4 Oil companies are large and global in reach, and they naturally prefer suppliers that have a similar footprint. Historically, they extracted oil directly underneath the ground. With the expansion of global demand and the sharp rise in prices, deeper deposits both onshore and offshore have become the target of exploration and exploitation. That’s where Tenaris’s seamless steel tubes are crucial. They range from 10 to 14 inches in diameter and can sustain temperatures up to 700 degrees Fahrenheit and pressures up to 12,000 pounds per square inch. “We target customers who are developing and exploring fields that require complex piping,” said Rocca. “We can establish clear differentiation and command a large position in these markets—such as nonstandard products developed for deep-water operations off the coast of West Africa, highly corrosive environments in the Caspian Sea, and other high-pressure or high-temperature environments—because there are few competitors.”5

The secret of Tenaris is its organization and management, especially of acquired companies. “State giveaways are no longer the norm,” one executive told us. “Access to cheap credit isn’t either. Production technology is not proprietary. Our competitive advantage lies in managing people and processes.”

Rocca emphasizes how important it is to integrate acquisitions. “A challenging point for us is being able to manage very different cultures and to adapt and incorporate them into our company. We need to capture brilliant people from diverse cultures. We are establishing an evaluation, training, and promotion system that rewards employee commitment and capability on a worldwide scale. Our people preserve our competitive advantage in the long run,” he said, adding, “After our strong expansion in the past few years, this is an opportunity to regroup and strengthen our focus on improving the service we provide our customers worldwide.”6

The recipe, in truth, is deceptively simple. Strategically, you need acquisitions to create a global presence and serve your customers everywhere they operate. Organizationally, you need to create systems that enable the pieces you acquire to work as one company. But the parent firm must have the capabilities to make the whole system operate as a unit.

Effective targeting and integration of other companies also enabled Cemex of Mexico to become a leader—one of the world’s top five cement firms and number one in certain product categories. The company was founded over a century ago, but most of its international growth has taken place since the mid-1980s through a series of acquisitions, the largest of which was the purchase of Australia’s Rinker for $14.2 billion in 2007. Although the global downturn in construction has hit the cement industry hard, Cemex has been able to remain profitable and to service debt through efficiency gains and the disposal of noncore assets.

At first sight, there’s nothing particularly special about cement. It’s simply a building material that sets and hardens when mixed with water and, when combined with other materials, generically labeled as aggregates, forms a rocklike mass called concrete. Concrete can be mixed on site or sold as a ready-mix by cement manufacturers through mixer trucks. Although its origins can be traced back to the ancient Macedonians almost three millennia ago, modern cement with high standards in terms of setting time and early strength is a product of the Industrial Revolution. That’s when one of the most popular variants of the product, Portland cement, was developed using four groups of raw materials: lime, silica, alumina, and iron. Cement is a capital- and energy-intensive industry in which the raw materials are treated in subsequent phases of raw milling, pyro processing, clinker cooling, clinker storage, finish milling, and packing, a series of steps not that different from cooking the raw materials. The cost of a new plant typically equals three years of turnover.

Cement is so heavy relative to its value that it does not pay to transport it by road beyond 200 miles from where it is produced. Not surprisingly, then, the industry was historically very fragmented, with established local or regional companies enjoying hefty profits at the expense of efficiency and innovation. Since the 1980s, however, the increasing availability of low-cost bulk shipping in special cement carriers and the availability of floating cement terminals in ports have transformed the industry as firms with excess capacity gained access to distant markets for the first time. It was an opportunity for firms to build large plants that not only serve the local market but also international markets through sea bulk transportation.

The world’s cement leader is Lafarge. Founded in 1833, this French company started its international expansion through foreign direct investment in the 1950s by setting up plants in Canada, Brazil, and North Africa. Beginning in the 1980s, the company grew via acquisition. Nowadays, Lafarge is present in 78 countries. Its main competitors are Holcim of Switzerland, HeidelbergCement of Germany, and Cemex, the first emerging market cement firm to break out of its home territory and today the global leader in ready-mix concrete.

How did Cemex do it? How did it become one of the most widely recognized and respected emerging market multinationals, famous for its ability to grow through acquisitions and widely considered by industry consultants to be Lafarge’s superior when it comes to integrating acquisitions? Maybe the roots lie in the fact that Cemex itself was the result of a sometimes rocky 1931 merger between two Mexican cement manufacturers, Cementos Hidalgo (founded in 1906) and Cementos Portland Monterrey, founded in 1920 by Lorenzo H. Zambrano, grandfather of Lorenzo Zambrano, the current CEO of Cemex.

Despite his pedigree, Zambrano’s path to the CEO position was far from smooth. A generation earlier, other shareholding families had pushed for a professional manager, Jesús Barrera. Over time Barrera also became an important shareholder and was succeeded by his own son, Rodolfo. The Barreras grew the company in Mexico by building new plants and acquiring other companies, like Cementos Maya, Cementos Portland del Bajío, and Cementos Guadalajara. With the acquisition of the latter in 1976, Cemex became the Mexican market leader. Then, in 1985, the time came to replace Barrera, and the board turned to Zambrano as its new CEO.

An engineer educated in the prestigious Mexican University ITESM (popularly known as Tecnológico de Monterrey), Zambrano had joined the company in 1968, after getting an MBA from Stanford. His relation was never good with Barrera, who intended for his own son to succeed him, but Zambrano was determined to reach the top position. In fact, he became so devoted to Cemex that he never married. Working in the operations department, he spent a lot of time studying how to integrate IT into the management of the company, especially to monitor plant performance. When he finally was appointed CEO, IT was one of the cornerstones of his efforts to turn around the company. His two other key ideas were to make all decisions on the basis of the value created for the customer and to grow aggressively via acquisitions. Zambrano also opted for focusing on cement as the core business, divesting noncore assets.

One of the first future-shaping decisions Zambrano made was to create an IT department and to introduce the position of CIO. “At that point, there was no IT department. Basically, there were a couple of computers that ran accounting programs. We realized that IT needed to be a key part of our new business strategy,”7 said José Luis Luna, Cemex’s current CIO. The company invested heavily in IT infrastructure, creating CemexNET, a satellite communications system that interconnected all of their plants, and set up GPS tracking on all of its trucks. The more established European and American competitors never thought about that. Later Cemex created an Internet platform to build B2B portals to connect suppliers, distributors, and customers. This infrastructure led the company to redefine working processes with the help of IT. This was a huge internal revolution that boosted efficiency inside the company in more ways than one, perhaps most dramatically in terms of customer service.

In a typical show of managerial prowess, the company, now in full control of production and delivery systems and in direct contact with customers, started to guarantee delivery of its products in just 20 minutes. That was the central reason why Cemex became number one in the world in ready-mix concrete. Cemex also improved the value proposition for its customers by discovering new market opportunities. Mexico is among the 15 largest countries both in terms of cement production and consumption, and one peculiarity of the market is that a large segment is comprised of individual customers who buy the cement in bags. In order to serve them better, Cemex set up a chain of building-materials distributors named Construrama. This network was a long-term cooperation project with existing Mexican distributors that, in exchange for exclusivity in selling only Cemex cement, received technical, management, and marketing support, and the right to use the label Construrama. Nowadays more than 2,000 stores are associated with the chain.

Cemex also innovated by launching Patrimonio Hoy, a savings-and-loan program that helps low-income citizens build and expand their homes by making access to cement blocks and other building materials affordable. Again, none of the European or American competitors made similar moves.

These initiatives embedded Cemex’s leadership in the Mexican market, which it came to fully dominate after acquiring Cementos Tolteca in 1989, the second-largest cement producer in the country. Creating value with acquisitions is all about buying a company at a discount price and/or raising its capacity to increase profits. Cemex put the emphasis on the latter. Given the myriad inefficient cement producers around the world, the industry was full of consolidation opportunities. Armed with its superior IT system and excellent skills at customer relationships, Cemex went on a shopping spree, buying competitors in Spain, Venezuela, Panama, Dominican Republic, Colombia, Costa Rica, the Philippines, Egypt, and the United States.

To avoid indigestion, Cemex moved quickly to integrate the acquired firms. It created a team of managers that would descend upon each acquired company to transfer all of Cemex’s expertise, technology, and systems, and then move onto the next acquisition. Over time the company learned to shorten the process of turning around and transferring its management routines and systems. Whereas the integration of the Spanish plants took two years, 10 years later the same process took only two months. “It’s like a SWAT team. For the first two months, we look for quick hits that will bring immediate savings,”8 said one experienced leader of these teams. But this process was not a mere unilateral transfer of systems and routines. On the contrary, Cemex also looked for sound managerial practices in the acquired companies to adopt. “We introduce our system, but we also pick up good practices that we haven’t seen anywhere else,” this same leader pointed out.9

In 2000, already a big global player, Cemex launched an ambitious program that took stock of what was learned during the growth process and used this as the basis for establishing a set of principles and values for managing the company. This program, dubbed the Cemex Way, aims to disseminate and identify best practices across the whole corporation, standardizing business processes with the help of Cemex’s IT infrastructure. “Essentially, it is internal benchmarking,”10 explained Zambrano. The program also fostered innovation by encouraging employees to propose innovations.

The Cemex Way was introduced just as Cemex started a second wave of acquisitions that included bigger targets. Its first prey was Southdown, the second-largest cement company in the United States. Southdown was a tough test for company principles and practices. Not only was it by far the largest target Cemex had sought to acquire and integrate, Southdown also operated in a market in which bulk sales to firms were much more important than sales to individuals. Rather than make the acquisition fit the Cemex Way, however, Cemex altered the “way” after the U.S. experience.

Besides other acquisitions of regional players since 2000, two deals have been critical in the recent development of Cemex. The first was the 2005 $5.8 billion acquisition of Britain’s RMC, a company with a presence in 20 additional countries and equal in size to Cemex. That integration process involved 400 managers from Cemex being sent to the different RMC plants to implement the benchmarking philosophy of the Cemex Way. The success of this integration led Zambrano to make an even bolder move: the acquisition of Australia’s Rinker, a company with a strong presence in the United States, for a whopping $14.2 billion.

The latter deal was met by board resistance, so Cemex had to offer an important premium for the acquisition, adding much debt to the company’s balance sheet. Worse, this acquisition was made just one year before the 2008 financial crisis, which slowed down the demand for cement in the developed world. Cemex’s finances deteriorated steeply enough that in 2009 it was forced to sell the Australian operations of Rinker to Holcim, its Swiss competitor.

Reflecting on those tough years, Zambrano said that “The mistake was not to finance the Rinker acquisition more conservatively,” but, he added, “If every time we make a decision to grow, we think of the absolute worst that can happen, then you don’t do anything.”11 Besides, his company was far from the only one in the industry doing financial restructuring in the wake of the Great Recession. World leader Lafarge has also been forced to refinance its debt.

The bottom line is that, even in perilous times, Cemex is still on a growth path. In 2010, the company launched Blue Rock Cement Holdings with the aim of investing in the cement industry in growing markets. Cemex holds a minority equity position (with the option to acquire Blue Rock’s assets) and provides management expertise. So far, Blue Rock has invested in Peru. Cemex is also looking for targets in India and China, where its competitors Lafarge and Holcim are already present, but is obviously reluctant to pay big premiums for local firms. In fact, the company recently declined the acquisition of a company in India because of its high valuation.

Cemex offers a key lesson to would-be acquirers, especially when having a global consolidation purpose in mind. Don’t buy anything unless you have the skills to turn the target around. You can’t win the acquisition game without developing a set of routines for making the target more efficient and integrating it with the rest of your operations. Obviously, not all of Cemex’s acquisitions were equally successful. But even in the case of Rinker, the only mistake was not to anticipate the magnitude of the current financial crisis, something that hardly anyone in the world did. The ability of Cemex to turn around cement companies remains intact, and Zambrano is still thinking of further acquisitions. In his own words: It is “within our DNA.”12

Acquisitions turned Tata Communications into not only the world’s largest international wholesale voice carrier—over 40 billion minutes annually, or about 10 percent of the world total—but also the most efficient. Tata owns a submarine and terrestrial cable network of more than 146,000 miles, nearly six times the length of the equator; a tier-1 IP network with connectivity to more than 200 countries and territories; and a huge data center in Pune, India, offering co-location, hosting, and storage services for customers.

Tata Communications, of course, is part of the Tata conglomerate, founded by Jamsetji Nusserwanji in 1868. Comprising over 100 companies and employing some 330,000 people, its revenues top $84 billion across such a diverse assortment of industries as consumer goods, chemicals, cement, steel, automobiles, engineering, energy, information systems, telecommunications, financial services, hospitality, and many, many others. It is now under the leadership of the family’s fifth generation. The Economist estimated Tata’s return on equity as of the year ending in March 2011 at an astounding 25 percent, the highest of any Indian conglomerate. Scale, scope, political connections, and true managerial capabilities all play a role in this company’s competitive position.13

The Tata Group made several acquisitions in telecommunications within the compressed time period of one decade: VSNL and Dishnet DSL in India, Teleglobe in Canada, Tyco Global Network in the United States, Neotel in South Africa, and Cipris in France, among others. In 2008, Tata grouped its telecommunications companies under Tata Communications. In addition to the physical infrastructure, Tata gained access to other valuable assets with these acquisitions. For instance, Teleglobe came with a software system that facilitates the location of roaming mobile phones used by 95 percent of telecom operators in the world.

A key moment in Tata’s foray into telecommunications came with the 2002 acquisition of 45 percent of VSNL, the state-owned monopoly on international long-distance voice. Once in the Tata fold, the company became the target of an extensive acculturation program.

“It wasn’t easy,” former CEO Srinath Narasimhan said about dealing with the bureaucracy at the formerly state-owned telecom monopoly. “There was simply no atmosphere of empowerment. Typically, what people would write on a file would be: ‘This is what I think we should do but my boss may please give his opinion.’ The file would go through 17 signatures on the way before it came to me. Then I’d have people who came saying, ‘I know I have the authority, but I just wanted your opinion.’ I’d simply say: ‘Not going to get it. Back to you.’”14

Acquiring the behemoth was the easy part. Making it work as a customer-oriented company was much harder. “We rewrote everything from scratch,” Narasimhan continued, “right from goal setting to assessment systems. And then a large chunk of people—almost a thousand—opted for voluntary retirement.” Maybe the greatest long-term value of acquiring VSNL lay in the very experience Narasimhan describes. By learning how to deal with a fossilized state-owned organization in its own backyard, Tata Communications was preparing itself for making similar acquisitions abroad since most state-owned companies share common features.

We’ve already seen in the cases of Tenaris and Cemex that the true value of an acquisition to the acquirer depends on what happens after the deal is done. An illuminating example of this dynamic is Tata’s acquisition of Tyco Global Network in the United States from the storied Switzerland-incorporated, New Jersey-based conglomerate Tyco International. The deal was managed by Kishor Chaukar, Tata Industries Managing Director. In 2005 he told a reporter that “the price that VSNL has paid is a fraction of Tyco’s total cable assets. It is a unique global network, with assets of almost $2.5 billion,” adding that “VSNL was short on bandwidth, information, and technology. With this deal no one will be able to beat us.”15

In telecommunications, customers expect seamless global services. The VSNL acquisition served that purpose as well. “This agreement will allow us to provide our enterprise and carrier clients with customized and robust connectivity solutions under one trusted global brand,” said Dave Ryan, chief operations officer at VSNL America.16 But seamless services don’t just happen: Any such strategy of growth through acquisition requires strong postmerger integration skills to succeed.

Indiscriminate integration simply won’t work. As experienced acquirers know, the trick consists in realizing what needs to be integrated and what does not. “We avoided the trap of ‘let’s integrate everything’ when it came to VSNL, VSNL International, and Teleglobe,”17 noted Srinivasa Addepalli, head of strategy at Tata Communications. Unifying the brand should and could wait, but the synergies from creating a single global operating unit to capitalize on scale, reduce costs, and manage traffic were absolutely essential for the acquisition to pay off.

In order to better appreciate Tata Communications’ success, compare its international acquisition strategy with those of BellSouth and AT&T. At the height of its Latin American influence during the 1990s, BellSouth overintegrated in some areas and underintegrated in others, forcing the company to eventually sell its assets to Telefónica of Spain. And that was only the beginning of its problems: BellSouth also expanded into one region only—a kind of antiglobalism when the world was headed in exactly the opposite direction—and it primarily simply wanted to milk the assets it had acquired. “We are not really committing new money to that region,” said CEO Duane Ackerman in 2003, “but we’re managing what we’ve got.”18

AT&T had its own disastrous bout with thinking too small. The company decided to focus on corporate customers, a segment that is increasingly global, without establishing a global presence of its own. AT&T’s CEO Bob Allen also caused the company to lose billions because of his strategic flip-flopping, which made it impossible to allocate enough resources to its telecommunications business. The 1991 purchase of NCR Corp. for $7.5 billion as a way to enter the computer business was especially disastrous because it distracted AT&T’s management from the new opportunities in global telecommunications being created by deregulation and technological innovation.

Whether you are selling steel tubes like Tenaris, cement like Cemex, or telecommunication services like Tata, if you want to be a global player, with global customers, you must blanket the world, and you must be willing to spend the resources, time, and effort to integrate your acquired assets so that you add value to your customers. Acquiring bits and pieces scattered throughout the world with no connectivity or integration among them will not be helpful to global customers.

BellSouth and AT&T also both paid far too much attention to their stock price. They did not pursue acquisitions hard enough because they feared investors. Yes, in the short run, an acquirer’s value in the stock market almost always suffers, but if the acquisition strategy is well executed, the market will reward the acquirer in the long term. Neither BellSouth nor AT&T’s managers and owners had the patience. Tata Communications, as a member of the Tata group of companies, was shielded from this type of investor pressure and managerial short-term orientation, an advantage that many emerging market multinationals possess thanks to their ownership structure. Few of them have widely dispersed share ownership. They are mostly owned by families or controlled by the state. While these types of owners have priorities (and challenges) of their own, they tend to focus on long-term profitability rather than short-term gains.

In making acquisitions, Tata Communications has gained yet another advantage relative to established multinationals. While offering global connectivity at a low cost, the company is stronger in emerging economies than in developed ones. That, too, could be a big plus. “The next trillion dollars to be made in global communications,” observed Camille Mendler, vice president of research at Yankee Group, “will depend heavily on emerging markets, where Tata Communications is already a leading player.”19

Cross-border acquisitions are the fastest way to gain global scale and expand quickly into foreign markets. Indeed, for latecomer firms, they are often the only way to get into the top positions in the global rankings. That said, many otherwise smart companies have dug their own grave because of failed acquisitions. Swept up by the chase and their own hubris, and perhaps impatient to make a bold move, they go to sometimes insane extremes to outbid competitors, convinced they can turn a profit no matter the price paid. Just as bad, that same arrogance tells them that the acquired company has everything to learn from the acquirer, and the acquirer nothing to learn from the acquired. Instead of asking how can we best work together and what can we learn from one another, the message delivered is “My way or the highway.”

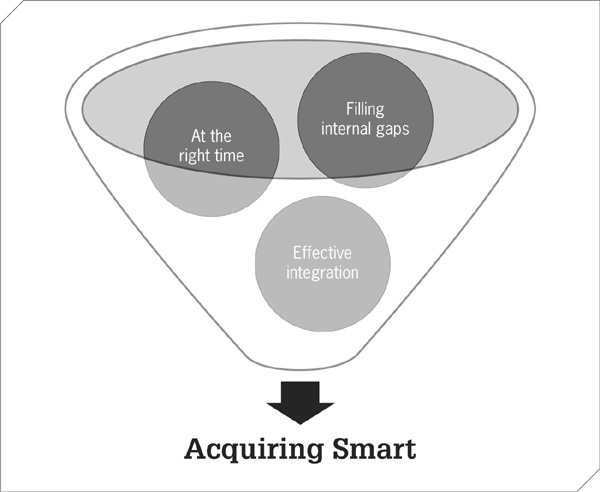

The recipe for successful acquisitions requires several ingredients. The first is to set a clear goal for the acquisition, namely, global consolidation and/or learning. Emerging market multinationals have excelled at both, as the cases discussed in this chapter illustrate. The other ingredients involve choosing the right target, at the right price, at the right time, and with the right integration approach. Failing to meet any of these requirements can seriously compromise the growth plan of the company. Figure 5 highlights these critical factors for making smart acquisitions:

FIGURE 5

Critical factors in aquiring smart.

First, acquire what you really need, and don’t be afraid of the size of the target, especially when the acquisition helps fill internal gaps. Think about the bold acquisitions made by Geely (Volvo) and the Indian steel giant Mittal, which purchased Europe’s Arcelor in 2006 for a whopping $33.1 billion. No matter whether you want to gain size or secure entry into a new market or field, always try to stand on the shoulder of giants.

First, acquire what you really need, and don’t be afraid of the size of the target, especially when the acquisition helps fill internal gaps. Think about the bold acquisitions made by Geely (Volvo) and the Indian steel giant Mittal, which purchased Europe’s Arcelor in 2006 for a whopping $33.1 billion. No matter whether you want to gain size or secure entry into a new market or field, always try to stand on the shoulder of giants.

Second, choose the right time. Making bold acquisitions does not necessarily entail paying big premiums. The volatility of global competition ensures that good targets will eventually become available, at bargain prices. But in order to take advantage of the opportunities, you must be prepared—financially and organizationally—to make your move.

Finally, choose the right integration mode. Depending on the aim of the acquisition—global consolidation or learning—the target must be either fully integrated or granted autonomy in decision making. Gains from experiential learning should never be neglected. The best example is the Cemex Way, which established a philosophy of benchmarking and innovation throughout the entire corporation. Also never forget that, especially when acquiring to consolidate, the bidder needs to be able to transfer some management capabilities to the target in order to create value. Acquisitions are not a miraculous solution for firms lacking capabilities. As Cemex’s CEO Lorenzo Zambrano once said, “If we cannot grow in markets where we already are, we cannot grow.”20