Executive Summary

4

Summary Appraisal Report

The sales comparison approach is the only method that can be used for land appraisals unless the land is leased or in some other way produces income. Land is sometimes leased for grazing, parking, or other uses. However, when it is leased for structures, the lease is generally long term—often for 20 years or more—and leases of this type are more common in other countries than in the United States.

With long-term leases, the lessee may build a structure, and generally the ownership of the structure goes to the lessor at the end of the lease. A typical lease for land in the United States would be for a cell tower. Depending on the agreement, the lease may require the lessee to remove the tower at the end of the lease or the tower may become the lessor’s property when the lease terminates.

The income approach for appraising leased land will not be covered here because Chapter 5, the commercial appraisal chapter, will go over it, and the same principles are applicable. The example in that chapter applies to any income stream, whether it comes from a lease or another source.

Land valuations can be relatively simple if the valuation is for a lot in a subdivision where others that are similar have sold. However, for many land appraisals, there are myriad aspects that must be considered that are specific and often unique for each parcel under valuation. And, like the proverbial snowflake, the more closely comparable land sales are examined, the more apparent their differences become. Moreover, the complexity of land sales seems to rise relative to the land regulations of the state in which they occur. The more environmentally active states tend to have more rules limiting development, and they allow more avenues of recourse for those organizations and state agencies that challenge development.

Some of the issues the appraiser has to consider are wetlands, protected species, environmental contamination, noise and pollution, drainage, traffic restrictions (also known as concurrency), building moratoriums, and citizen pressure. All of these issues are set against a backdrop of dealing with various echelons of government—federal, state, and local—some of which are redundant in the areas they regulate and may use different yardsticks in their determinations.

For this reason, the fact that land is zoned for a particular use does not mean that its development is realistic or cost effective. For instance, a small parcel of land that is two acres in size may be zoned for 6,000-square-foot lots. However, once the easements for access are considered, and the engineering and other development fees are calculated, in addition to the time that the property must be held to get the permits approved, there may be no profit in the venture.

For this reason, developers pay a premium for prime land, which normally means land that has been approved for construction and has already been through the permitting process.

Land values can also change quickly and significantly depending on hearings that may be held regarding potential usage in various tribunals, or by local politicians. (For more information, also see the segment on land valuation in Chapter 7 on industrial building appraisal.)

When development is at low ebb due to economic conditions or other circumstances that have lessened demand, there may be very few buyers for land, and prices may fall precipitously. However, the appraisal may not reveal this clearly because sales may be used that are older, and adjustments for those sales may not have kept up with the diminished demand. Listings also may not reveal the extent of the drop in value because they often stay higher than market value as compared to other real estate. The reason for this is that landowners often own their property free and clear and are under less pressure to sell than the owners of other types of real estate.

However, in an appraisal in a declining market, the appraiser may not be attempting to inflate the value. The appraiser works only from the data that is available. If there are few sales and they are older, the indicated value of the subject property may be inaccurate only because there have been no recent sales that reflect the change in values, and the appraiser has no other valuation evidence to use.

Conversely, when values are climbing because demand has increased, even sales that are six-months or a year old may not reflect the current value. Appraisers may know that values are increasing in such a market, but they must work from actual sales as evidence of the value, and higher listings do not provide evidence that can be used in the appraisal to prove a value. Essentially the appraiser’s hands are tied in such a market, and the value may come in lower than the sale price due to the rapidly increasing market.

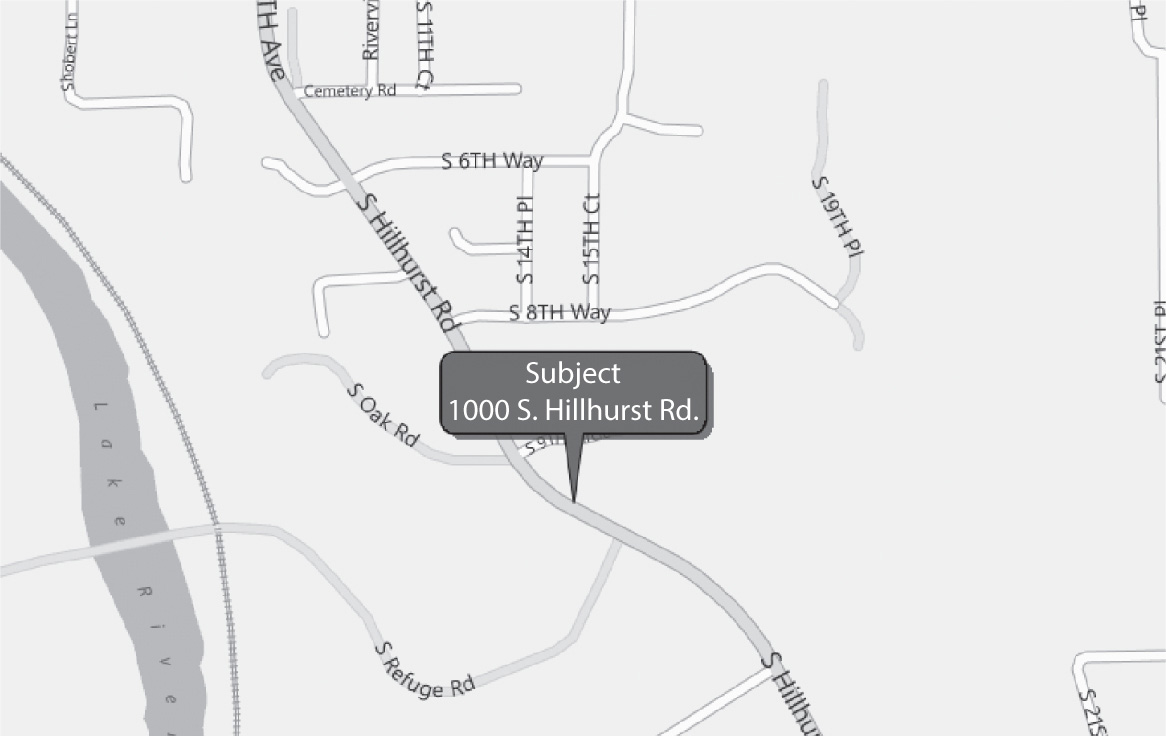

Map of Subject Property—Approximate, Not Actual, Address

Map of the Subject Property, Parcel Number 216888-000, on Record with the County Assessor

Summary Appraisal Report

5

Aerial Map of the Subject Property, Parcel Number 216-888-000, on Record with the County Assessor

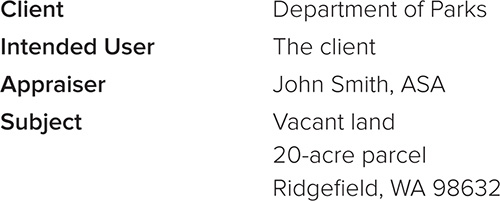

This is a summary appraisal report, which is intended to comply with the reporting requirements set forth under Standards Rule 2-2(b) of the Uniform Standards of Professional Appraisal Practice for a Complete Appraisal presented in Summary Form. As such, it presents summary discussions of the data, reasoning, and analyses that were used in the appraisal process to develop the appraiser’s opinion of value. The depth of discussion contained in this report is specific to the needs of the client and for the intended use stated below.

I have appraised this property previously, and that appraisal is in the possession of my client. The appraiser is not responsible for unauthorized use of this report. This report is the result of a full appraisal process. The sales comparison approach is the only applicable valuation approach for this assignment. The value opinion is based on current understanding of the market and market trends.

6

Summary Appraisal Report

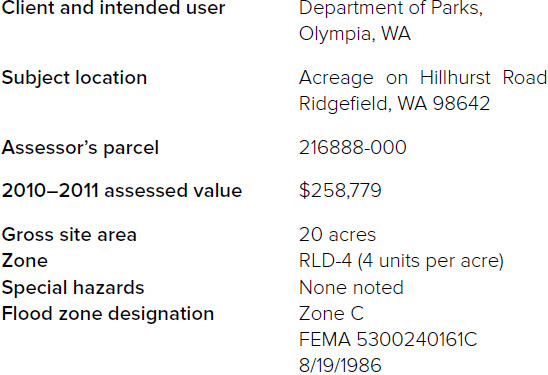

The purpose of this appraisal is to provide the appraiser’s best estimate of the subject’s as-is fee simple market value. The use of this appraisal is to aid the Department of Parks to determine the price the Department may want to pay for the land.

Market value is defined by the federal financial institutions regulatory agencies as follows:

Market value means the most probable price which a property should bring in a competitive and open market under all conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a sale as of a specified date and the passing of title from seller to buyer under conditions whereby:

1. buyer and seller are typically motivated;

2. both parties are well informed or well advised, and acting in what they consider their own best interests;

3. a reasonable time is allowed for exposure in the open market;

Summary Appraisal Report

7

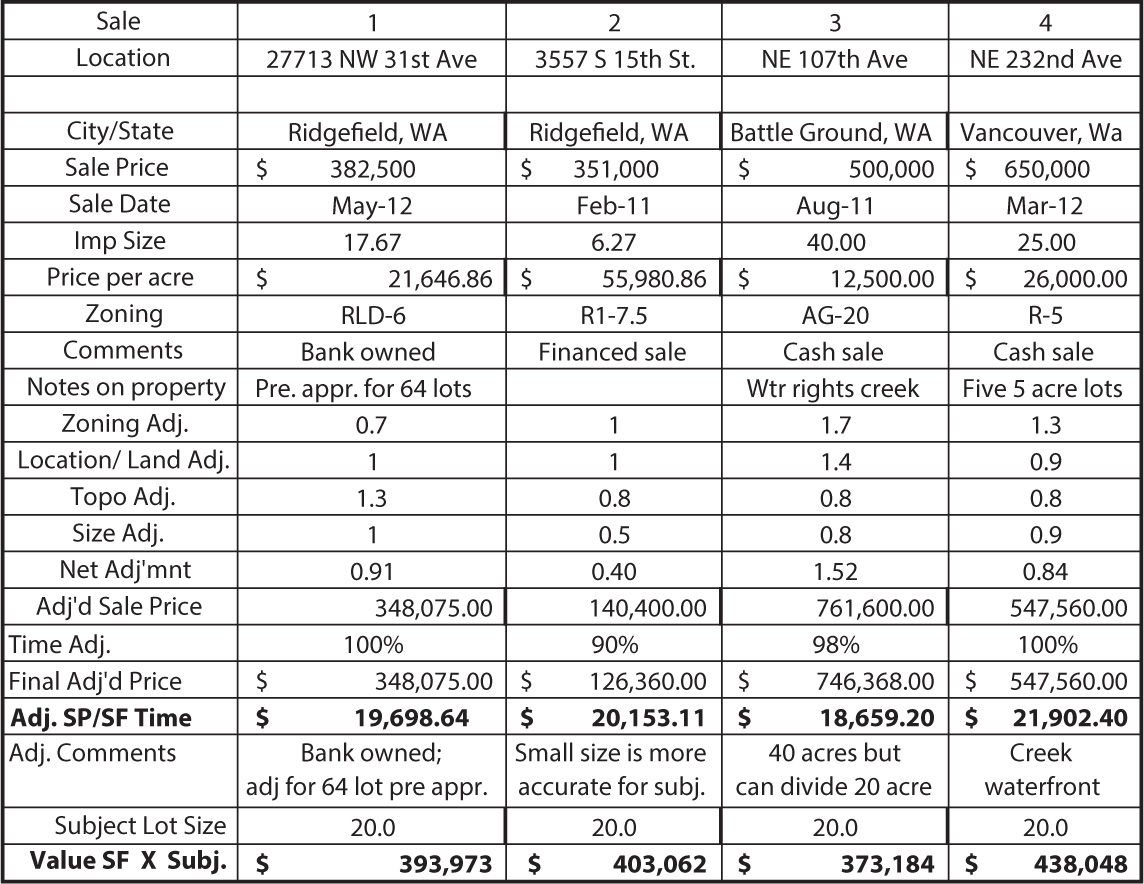

Because the market is very slow, there were few sales to use for this appraisal, and an expanded search included sales in Vancouver and nearby areas. The subject is zoned for development, but because of current economic conditions, land has been selling for less than its normal development value. Some sales are not developable, and others are dividable only into two parcels. Therefore, appropriate adjustments were made under the zoning adjustment on the grid.

Sales Comparable to Subject Property

Summary Appraisal Report

23

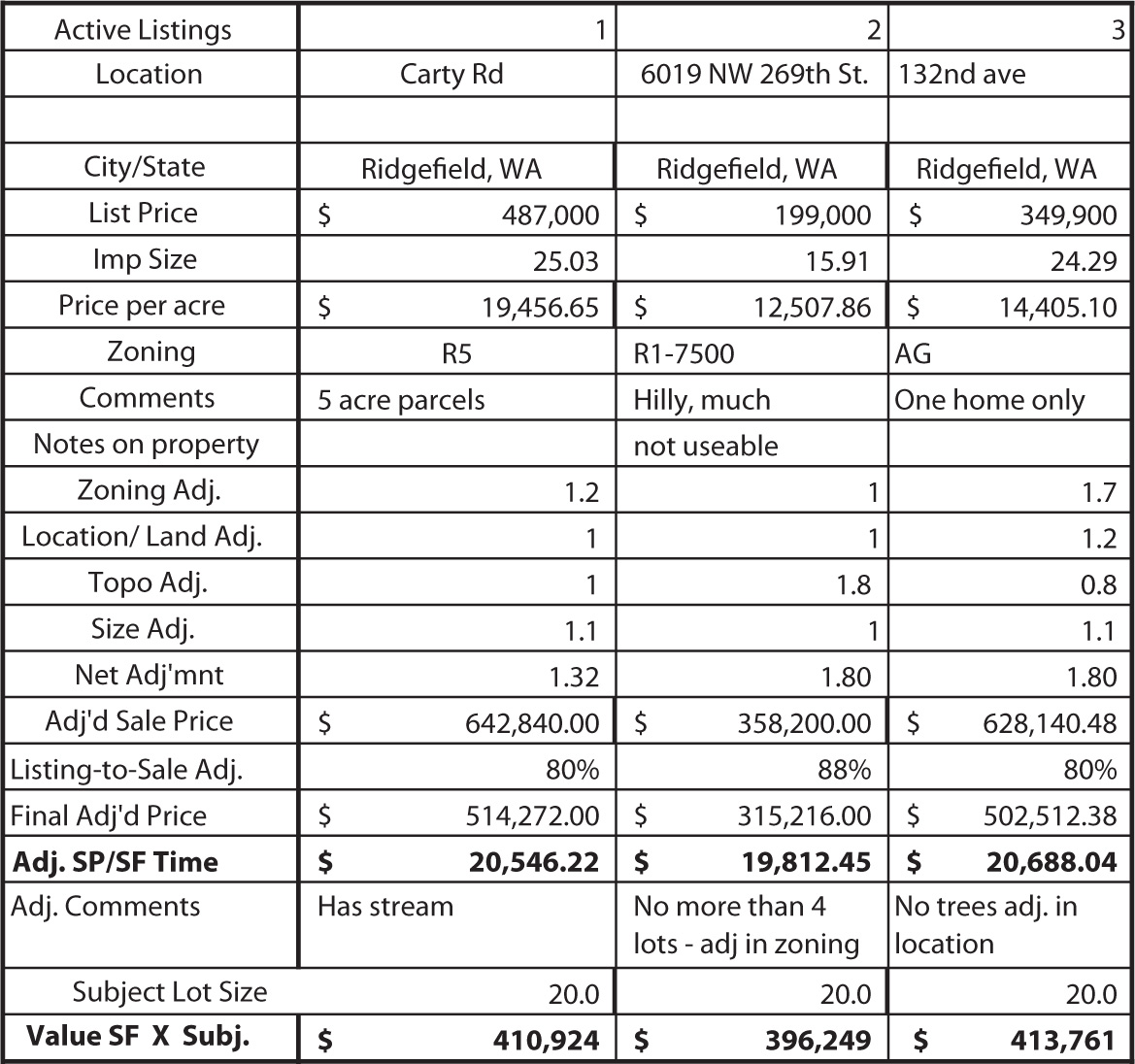

Listings Comparable to Subject Property

The land comparables vary in location, size, and timing, but all are generally helpful in estimating the subject value.

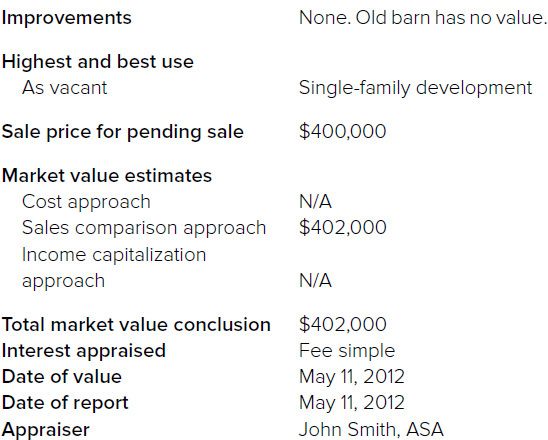

After a qualitative and quantitative analysis of these sales, I believe that a value of $20,100 per acre for the land as if vacant is supported and reasonable. The total land value would therefore be as follows:

20 acres × $20,100 = $402,000

24

Summary Appraisal Report

Note to Reader: It is common for the appraiser to discuss each of the comparable sales as part of the analysis, but that was not done in this appraisal. The lack of a discussion does not necessarily mean the appraisal is lacking, but it would have been preferable to get a little more information about each sale to understand the appraiser’s reasoning for the adjustments for the sales.

Based on the data and analysis presented, I therefore conclude the sales comparison approach yields a fee simple market value, as of May 11, 2012, of:

$402,000

The vacant lot is valued by the sales comparison approach only, and that is the only applicable approach for this lot.

The cost approach was inapplicable to this assignment.

The sales comparison approach is closely tied to the marketplace, and there was adequate data to support the land value and improved value conclusions by this approach.

The income capitalization approach was not performed in my valuation because the subject is not primarily an income producing property and because the client has requested a land-only appraisal. Therefore, I have placed all weight on the conclusion of the sales comparison approach.

Summary Appraisal Report

25

I therefore conclude the subject property has an as-is fee simple market value, as of May 11, 2012, of:

Four Hundred Two Thousand Dollars

The following are photographs of the subject property from different perspectives.

Property from Southeast Corner of Easement

26

Summary Appraisal Report

Looking West from South End of Property (South Great Blue Road)

Looking South, Land on Right

Summary Appraisal Report

27

Looking North from Great Blue Road (South End of Land)

Looking West, Middle of Parcel

30

Summary Appraisal Report

Looking North from the South End of Land

The undersigned does hereby certify that, except as otherwise noted in this appraisal report, to the best of my knowledge:

1. The statements of fact contained in this report are true and correct.

2. The reported analyses, opinions, and conclusions are limited only by the reported assumptions and limiting conditions, and they are my personal, unbiased professional analyses, opinions, and conclusions.

3. I have no present or future interest in the property that is the subject of this appraisal, and I have no personal interest or bias with respect to the parties involved.

Summary Appraisal Report

31