2.2 Your Decisions and Your Demand Curve

So far, we’ve focused on the actual buying decisions that people make. Let’s turn to the harder question: What are the best buying choices you can make? The core principles of economics can provide useful guidance. As we go through each principle, you’ll get a deeper sense of the various factors that shape individual demand curves.

Choosing the Best Quantity to Buy

Let’s start by exploring what’s behind Darren’s individual demand curve. In a follow-up interview, he provided some insight into his preferences. Darren starts by thinking about all of the possible uses he has for a gallon of gas and prioritizes them. He does this by thinking about the benefits he gets from each alternative use. Because dollars is the measuring stick by which we assess benefits, he puts a dollar value on these benefits that summarizes how much he’s willing to pay for each possible use of a gallon of gas. Figure 4 gives his explanations for how he’ll use each gallon of gas and the benefit each use has for him.

Figure 4 | Darren’s Uses for Gas

Focus on your marginal benefits.

Each row shows one of Darren’s uses for each additional gallon of gas. He’s listed them in order of his priority—from the uses that deliver the largest benefit to him to those that deliver the least benefit. When he thinks about these benefits, he’s not just thinking about the dollars involved. He’s thinking about his benefits broadly, such as the benefits of saving time, of seeing his parents, or of taking a relaxing drive to unwind. And in each case, he’s comparing them to his next best alternative.

Darren is thinking about the additional benefit of one more gallon of gas—that is, the marginal benefit. When Darren thinks about the different ways he can use an extra gallon of gas, he’s really thinking about the marginal benefit he gets from each gallon of gas, and this is shown in the final column of Figure 4, “Marginal benefit.”

Do the Economics

Let’s return to Darren as he was driving toward the gas station. He noticed that gas is selling for $3 per gallon (well, actually for

Should he buy a first gallon of gas?

Yes. According to Figure 4, Darren will use this gallon to shop at Walmart, which yields him a marginal benefit of $5, which is greater than the $3 it will cost him.

OK, so continue: Should he buy a second gallon of gas at $3? (Hint: You should ask: What are the benefits? What will this cost?)

OK, so gas is never exactly $3 per gallon.

The second gallon of gas yields a $4 marginal benefit, which is greater than the marginal cost of $3. Sounds like a good deal.

And should he buy a third gallon?

The third gallon is a close call. It yields $3 of marginal benefits, which is slightly more than the marginal cost (which is actually

What about a fourth gallon?

The fourth gallons yields a $2.50 marginal benefit, and it’s not worth spending $3 to get a $2.50 marginal benefit.

And a fifth? A sixth?

Similar logic suggests that Darren shouldn’t buy a fifth or sixth gallon either: In each case they yield a marginal benefit less than the $3 marginal cost of a gallon of gas.

Bottom line: What quantity of gas should he buy at

Darren should buy three gallons of gas.

Notice that your advice is based solely on comparing the price of a gallon of gas with the marginal benefit that Darren gets from it. In fact, whenever you need to figure out your demand for any good, you should follow the same logic, comparing the price with your marginal benefit. This is why economists say that understanding demand is all about understanding marginal benefits.

Apply the core principles to make good buying decisions.

Darren’s approach to buying gas seems pretty sensible. In fact, he’s implicitly relying on the core principles of economics. You’ll want to apply the same logic when you’re making your own demand decisions, whether you’re deciding how many pairs of jeans to purchase, how many shares of Google to invest in, or how many workers to hire. Let’s see how.

The marginal principle says that you should break “how many” questions into a series of smaller marginal choices. Darren’s clearly thinking this way, considering each additional, or marginal, gallon of gas separately, and how he would use it. It means that he’s ready to analyze the simpler question of whether to buy just one more gallon of gas. And indeed, we just evaluated whether to buy a first, then a second, then a third and a fourth gallon of gas when the price was $3.

For each of these marginal decisions, Darren’s best choice depends on the cost-benefit principle, which says: Yes, he should buy that additional gallon of gas if its benefit exceeds the cost. The cost of an additional gallon of gas is simply its price. The benefit of an additional gallon is called its marginal benefit.

And notice that when Darren evaluates his marginal benefits, he applies the opportunity cost principle, asking: “Or what?” He doesn’t just ask about the benefits of driving to Walmart; he compares it to the next best alternative, which is doing his shopping nearby. It’s only by comparing driving to Walmart with the next best alternative that he figured out that the marginal benefit of the first gallon of gas is $5. He does something similar in each row of Figure 4. Here’s a chance to test yourself: Go back and underline the “or what?”—the next best alternative that he identifies on each row. (Answer: It’s the second sentence of each row.)

The Rational Rule for Buyers

Working systematically through the core principles—as shown in Figure 5—leads to the conclusion that Darren should keep buying additional gallons of gas as long as the marginal benefit is greater than (or equal to) the price.

Figure 5 | Rational Rule for Buyers

We’ve uncovered a pretty powerful rule, which you can apply to any buying decision:

The Rational Rule for Buyers: Buy more of an item if the marginal benefit of one more is greater than (or equal to) the price.

The Rational Rule for Buyers puts together the advice from three of the four core principles in one sentence. You should think at the margin, comparing the marginal benefit of one more item with the marginal cost (in this case, the price), and evaluate these costs and benefits relative to your next best alternative. You can apply this rule to your real-world buying decisions. For instance, it says to Darren: You should buy another gallon of gas if it yields a marginal benefit greater than or equal to its price.

You might be wondering what role the interdependence principle plays in all this. It’s already there in Darren’s reasoning: His decisions depend on the availability of the bus, his desire to go to the gym, and even his love for his parents! For now, we’re focusing only on the effects of different prices, holding these other things constant. But when we return to the interdependence principle later in this chapter, we’ll see that if these other things were to change, so would his plans.

Follow the Rational Rule for Buyers to maximize your economic surplus.

The Rational Rule for Buyers is good advice. Why? If buying one more gallon of gas yields marginal benefits for Darren that exceed the price he pays, then he is better off. That is, he’ll enjoy greater economic surplus—which is the difference between his total benefits and total costs—because this purchase will boost his total benefits by more than it boosts his total costs. And that’s the reason why you’ll want to follow this rule in your own life.

In fact, you want to take every opportunity to make those purchases that will make you better off, and take a pass on any purchases that will make you worse off. If you relentlessly follow the Rational Rule for Buyers and buy more gas (and more food and more clothes and so on) for as long as the marginal benefits are at least as large as the price, then by taking every opportunity to boost your economic surplus, you’ll succeed at maximizing your economic surplus.

(You might wonder why this rule says its marginal benefit is exactly equal to the price. Truth is, this decision doesn’t make a difference, because buying that last item will make you neither better off nor worse off. Still, I say you should continue to buy up to, and including, the point when marginal benefit equals price, because it’ll make the rest of your analysis a bit simpler.)

Keep buying until price equals marginal benefit.

If you follow the Rational Rule for Buyers, you’ll keep buying more gas until the marginal benefit of the last gallon you buy is equal to the price. Why? The rule suggests you keep buying gallons of gas as long as the marginal benefit of each gallon is at least as high as the price. Consequently, you will stop buying more gas just before the marginal benefit of the next gallon falls below the price—which occurs when the marginal benefit equals price.

You might recognize this insight. Recall the Rational Rule from Chapter 1, which said: “If something is worth doing, keep doing it until your marginal benefits equal your marginal costs.” We’re simply adapting this rule to when you’re buying stuff, and so the marginal cost of an extra gallon of gas or pair of jeans is simply the price. As such, adapting the Rational Rule to your role as a buyer says you should keep buying until:

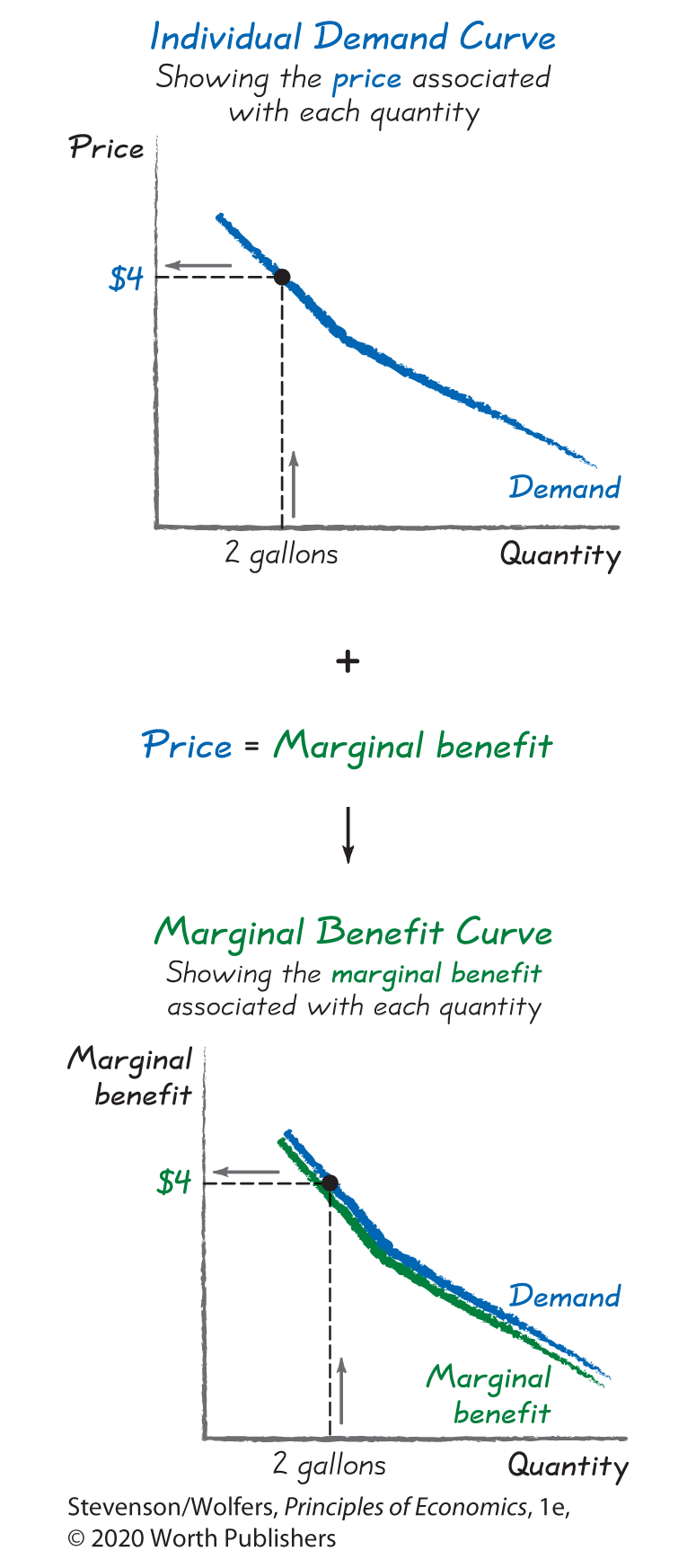

Your demand curve is also your marginal benefit curve.

Hopefully you can now see why economists say that understanding demand requires remembering just one phrase: Price equals marginal benefit.

This reveals a new perspective for thinking about demand: Your demand curve is also your marginal benefit curve. Think about it: Your demand curve illustrates the price at which you will buy each quantity of gas. If you keep buying until price equals marginal benefit, then the same curve illustrates the marginal benefit of each gallon of gas.

Your demand curve reveals your marginal benefits.

This yields an important insight for managers. It’s likely that you’ll want to know how much your customers benefit from your products. You could commission an expensive survey to find out. But there’s a cheaper way to do this: Your customers’ demand curves are also their marginal benefit curves, and so you can also learn about their marginal benefits by just observing their buying patterns. For instance, if Darren buys two gallons of gas when the price is $4 per gallon, then you can infer that the marginal benefit to Darren of that second gallon is $4.

Let’s summarize. Demand is all about marginal benefits. Indeed, your demand curve is your marginal benefit curve. Consequently, understanding demand is really about understanding marginal benefits.

Diminishing marginal benefit explains why your demand curve is downward-sloping.

Economists have studied the marginal benefits of many different items, and discovered a general tendency toward diminishing marginal benefit. That is, the marginal benefit of each additional item is smaller than the marginal benefit of the previous item.

Let’s get delicious about this, and focus on ice cream. (Yum!) One or two scoops are scrumptious. A third scoop still tastes pretty good. By the fourth, you’re getting tired of all that sugar. And a fifth scoop will make you feel sick. (Believe me.) As you eat more ice cream, the marginal benefit of another scoop keeps getting smaller.

And a similar pattern follows for other goods. Take Darren’s demand for gas. He planned to use his first gallon of gas for his high marginal benefit activities (shopping), his second gallon would go to a slightly lower benefit activity (driving to work), and each successive gallon is used for a lower priority trip. As a result, each extra gallon yields a successively lower marginal benefit.

If you think about most of the things you buy in a year, I bet you’ll agree that you get diminishing marginal benefits from not just extra scoops of ice cream, or gallons of gas, but also pairs of jeans, concert tickets, pairs of headphones, and just about everything you buy. (If you want to point out that there are exceptions to this rule—for instance, your second shoe yields a larger marginal benefit than your first shoe—I’ll agree, as long as you agree that these exceptions are rare.)

Diminishing marginal benefits is an important phenomenon because it means that each extra purchase yields a lower marginal benefit, and hence your marginal benefit curve is downward-sloping. And since your marginal benefit curve is also your demand curve, this means that your demand curve is downward-sloping. That is, if extra scoops of ice cream, gallons of gas, or pairs of jeans yield a lower marginal benefit, you’ll only buy them if the price is lower. And that’s why your individual demand curve is downward-sloping.

Recap: Individual demand reflects marginal benefits.

We’ve covered a lot of ground, so let’s take a breather and recap. So far, we’ve been focused on individual demand—the buying decisions that you as an individual will make. We began with the individual demand curve, which summarizes the quantity you demand at each price.

We then turned to the more difficult question: What are the best buying choices you can make? This led us to the Rational Rule for Buyers, which says to keep buying more of an item as long as the marginal benefit of one more is greater than (or equal to) its price. This process helps us see why people, like Darren, are willing to pay less for each additional item, like each additional gallon of gas, since the marginal benefit from each additional item is declining. As a result, we saw that individual demand curves are downward-sloping.

How Realistic Is This Theory of Demand?

By this point you might be thinking: Is this realistic? Does anyone really act this way? And maybe it is a bit unrealistic to say that when you’re shopping, you’re actually thinking deeply about your marginal benefits. Good point. But these are still important ideas, for two reasons.

Thinking through the core principles provides useful advice and helpful forecasts.

First, the Rational Rule for Buyers provides useful advice to you. As you learn to apply this rule to your everyday buying decisions, you’ll find yourself making better decisions.

Second, these rules will often provide a useful way for you to understand, and even predict, how other people will act. This is the “someone else’s shoes” technique discussed in Chapter 1. If you want to know how someone else will act, put yourself in their shoes and ask: What would you do if you were in their shoes? Presumably, you would try to make the best decisions possible, so you would try to follow the Rational Rule for Buyers. In fact, store owners have long known that diminishing marginal benefits is an important factor in determining sales—that is one reason you often see specials like: “Buy one, get the second half-off.”

As buyers experiment, they may come to act as if they follow the core principles.

Still, it’s likely that people don’t act exactly as this theory suggests. But people generally do (and should!) buy more of those goods with higher marginal benefits and lower prices. And even though most people aren’t thinking through the exact calculations that we’ve outlined, they may follow a different process to the same outcome.

People move closer and closer to making their very best decisions as they gain more experience. Perhaps you got overexcited when you visited Sam’s Club for the first time and bought a 64-ounce jar of mayonnaise, only to see it spoil. But next time you hit the store you’ll make savvier choices. Through the process of experimenting—buying different goods and different amounts of goods—people find out what works best for them. As a result, people will often end up making choices as if they made the calculations that our theories predict they should make. This is going to be a really useful insight, as we now turn to analyzing how buyers—as a group—combine to make up market demand.