It’s time to turn our attention from consumption to saving. Of course, this isn’t a change of focus at all—how much you save depends on how much you consume, and vice versa. Don’t think of this as a separate analysis of saving, but rather as a continuation of our analysis that will lead to a more complete understanding of both consumption and saving.

There are four key motives that drive saving, and it’s time to explore their implications for saving, consumption, and macroeconomic outcomes.

Saving Motive One: Changing Income over the Life Cycle

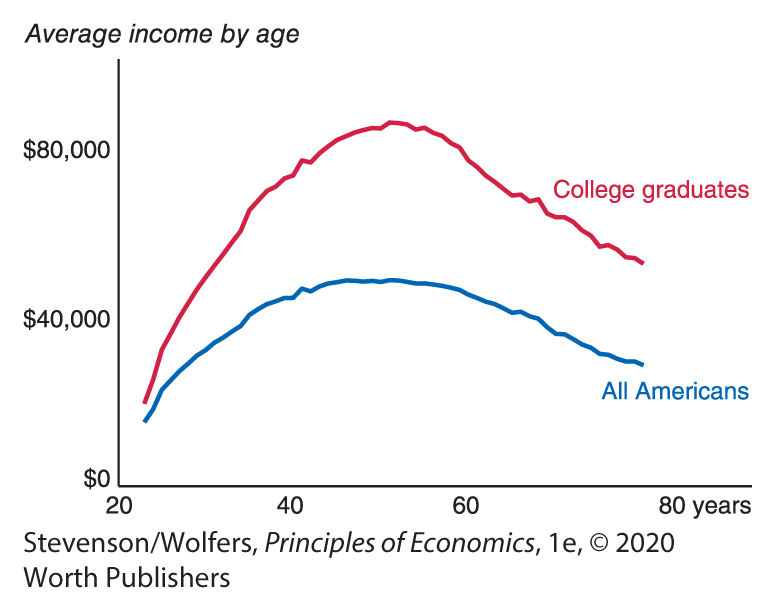

You’ve already seen that most people borrow when young, save in midlife, and spend down their savings in retirement. This pattern is driven by how income typically changes over the life course. Your income will probably start low and then rise over your 20s and 30s; you’ll enjoy your peak earning years in your 40s, 50s, and maybe 60s; and then your income will drop off sharply when you retire. That is, your income will probably follow a hump-shaped pattern. As Figure 13 shows, it looks like this . But your consumption shouldn’t follow the same pattern. The logic of consumption smoothing is that you should save money in those phases of your life when your income will be predictably higher, so that you can spend more than your income when it’s lower.

Figure 13 | Income over the Life Cycle

2017 Data from: American Community Survey.

As a result, people tend to spend more than their meager incomes in their 20s and thus accumulate debt. Then as their earnings grow, they pay down their debt and accumulate savings in their 30s, 40s, and 50s. People tend to spend down their accumulated assets starting around the mid-60s, as they head into retirement.

These patterns mean that demographics have macroeconomic implications for national savings. If a large share of the population is very young or very old, then national savings will be lower than it would be if more people were middle-aged. The share of the U.S. population over age 65—the age at which many people retire and move from saving to dissaving—has more than doubled over the past several decades. This demographic shift has helped push the national savings rate down from over 10% in the 1950s to 6% at the end of 2018.

Saving Motive Two: Changing Needs over the Life Cycle

So far, we’ve analyzed how your income varies over your life. Your needs also vary over your life course. You should save more (and spend less) in periods when you have fewer needs, so that you’ll have more to spend when there’s a greater need.

They’re little, but they’re expensive. Believe me.

So look ahead now and forecast how your needs will vary over your life course. For most college students, their most important needs are tuition, accommodations, and living expenses. When you graduate you won’t be paying tuition any more, although you might have to start paying down your student loans. Different people follow different life paths, but for many, the next big expense comes when they get married, which might involve a costly wedding, a honeymoon, and setting up a new household. But a wedding is cheap, relative to the cost of feeding, clothing, and raising kids. If you’re planning a family, be aware that those first few years with young kids involve some big expenses. It’s not just diapers and toys; you’ll need to budget for child care if you plan to keep working, and that often costs more than in-state tuition at a public college. All of this means that for many people it’s a good idea to spend modestly in your early 20s—even though your permanent income might allow higher consumption—because your needs are likely to rise as you enter your 30s.

This may sound like the opposite of consumption smoothing, since it says that you should spend more when your needs are greater, but it’s not. The Rational Rule for Consumers says that if your needs are similar over time, then you should smooth your consumption. But if your needs are changing, then your consumption should also change over time. The Rational Rule for Consumers tells you to spend more when the marginal benefit of spending today is more than the marginal benefit of spending a dollar-plus-interest in the future. At certain times in your life the marginal benefit of each dollar of consumption will be higher, so you’ll want to consume more. In turn, that means that you’ll need to save more in those phases of your life when your needs aren’t so great. The main idea here remains the same—you want to shift your spending to the times in your life when it’ll yield the largest marginal benefit.

Saving Motive Three: Bequests

The third motive for saving is that you might want to build up a stock of wealth that you’ll pass on when you die. For some people, that means leaving an inheritance for their children. For others, it’s about leaving money to a cause they care about. It’s important to draw up a detailed will in order to ensure your bequest goes to help the folks you care most about.

The bequest motive helps explain why many elderly people don’t spend down all their wealth—they’re hoping their money will outlive them, and that it’ll make a difference even if they aren’t around to see it.

Saving Motive Four: Precautionary Saving

The final motive for saving comes from the old saying that you should hope for the best, but prepare for the worst. This suggests that you should build up a buffer stock of saving to protect you in case financial misfortune strikes. That misfortune could be a layoff that leaves you unemployed, a medical emergency, or any other unexpected cost. Saving to be prepared for a financial emergency is called precautionary saving because you’re building up that buffer as a precaution. It’s the idea that you should save for a rainy day.

Save enough to weather the financial risks you face.

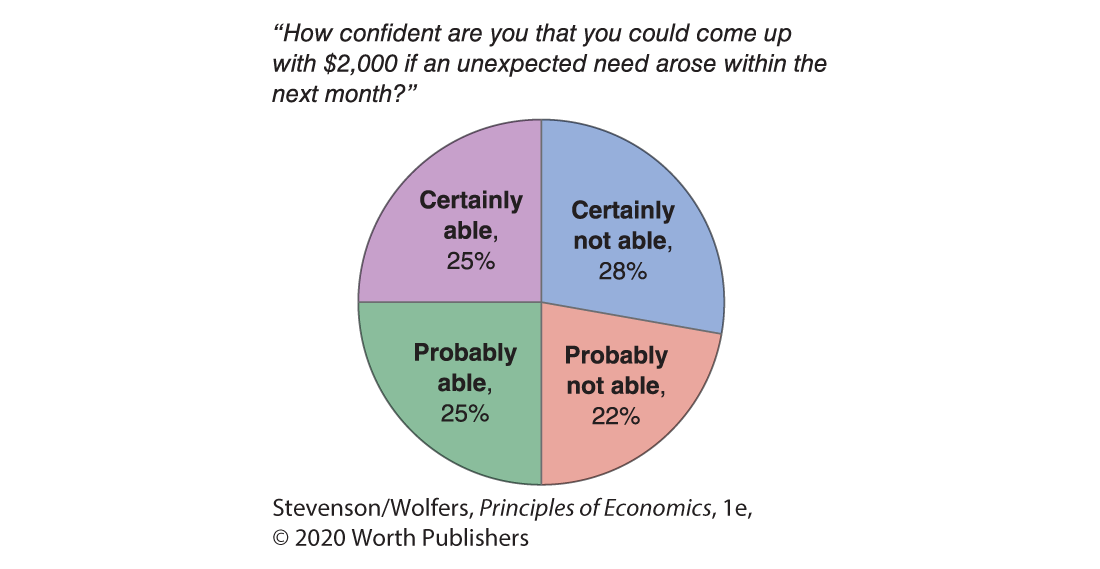

Figure 14 | Many Americans Are Financially Unprepared

Data from: Annamaria Lusardi, Daniel Schnieder, and Peter Tufano, “Financially Fragile Households: Evidence and Implications,” Brookings Papers on Economic Activity, 2011.

Let’s take a measure of your financial health: How would you cope if you needed to replace your car’s transmission? Such a shock might set you back around $2,000. Could you come up with the money? Figure 14 shows that a survey asking Americans this question found that half were either “probably not able” or “certainly not able” to come up with the funds. Among young adults, the numbers were even worse.

If you’re in a similar situation, my advice is to start saving to build up your rainy-day fund. It’s an urgent task because once you get into financial trouble, your problems can quickly cascade. If you can’t fix your car, then you can’t get to work, and if you can’t get to work, you’ll lose your job, and then you’ll never be able to afford to fix your car.

While many people can’t come up with $2,000 to fix their car, people often face even more critical risks. To evaluate how much you’ll need to save, think through the sorts of financial risks you face and how much money you’ll need to have on hand to weather them. One of the biggest risks you’ll face is unemployment. The good news is that most people who lose their jobs find a new job within a few months; the bad news is that this still means going a few months without a paycheck. That’s why financial planners typically advise that you build up a buffer stock that’s equivalent to three-to-six months of your typical consumption.

Precautionary saving is why national savings goes up when economic uncertainty rises.

Figure 15 | Saving Stayed High After the Recession

The more uncertain your economic future looks, the larger your rainy-day fund should be. So when economic uncertainty rises, millions of people increase their precautionary saving. But remember that savings and consumption are two-sides of the same coin—to save more, they have to consume less. As a result, growing uncertainty can lead to a decline in total consumption.

Precautionary saving also shapes how the economy recovers following a recession, as shown in Figure 15. A recession puts millions of people out of work, leading them to deplete their rainy-day funds or go into debt. And so even after the economy has returned to normal, people will save more (and thus consume less) in order to rebuild their financial buffers. The result is that saving rates remained high after the 2007–2009 Great Recession. This in turn partly explains why weak consumption spending held back the economic recovery.

EVERYDAY Economics

Preparing for the unexpected

Be prepared.

If a financial emergency strikes before you’ve built up your rainy-day fund, you’ll quickly discover there are no great options for borrowing money—but some options are less bad than others. The first thing to consider is whether you have a friend or family member who can loan you the money. This is often the cheapest option in dollar terms, but in personal terms it can be pretty costly, so be careful.

The rest of your options involve borrowing money through the financial sector, and it’s worth evaluating the costs and benefits of each of your alternatives.

Credit cards: One quick option is to use your credit card to cover expenses. But note that credit cards typically charge high interest rates. It’s better to use your card to make purchases than to get a cash advance because you get a a 30-day grace period to repay purchases before interest starts accruing. Borrowing cash on your credit card is worse because it typically involves fees in addition to the interest charges.

Pay off your balance as quickly as you can (and always make minimum payments on time). If you must carry a balance, it’s worth calling your credit card company to ask for a lower rate—you’ll be surprised how often it works. Try asking if they have any balance transfer offers. Be careful: Sometimes they’ll offer low introductory rate for a few months, so they can jack up their rates later. But if you read the terms carefully and plan accordingly, you can work a balance transfer offer to your advantage.

Loans: Some banks offer personal loans, precisely to help their customers handle a financial emergency or to pay off a high-interest credit card. You can call a few banks and ask what you need to qualify for one and what interest rate they’ll charge. If you own your car or your house, you can take out a car loan or a home equity loan. These loans tend to charge lower interest rates since they have the car or house to back them—but if you don’t pay them back, you risk losing your car or house.

Notice that they’re not advertising their interest rate.

Retirement accounts: If you have a retirement plan, you might have the option of borrowing from it, and paying yourself back with interest. But ask a lot of questions first, because if you don’t follow the rules precisely this can lead to a significant increase in your tax obligations.

Payday loans: Be very wary about payday loans. These lenders lend you small amounts of money at very high interest rates if you agree to pay the money back when you get your next paycheck. Unless you’re absolutely sure you can repay the loan with your next paycheck, you should avoid these loans because they quickly get out of hand once they start to compound: The annual interest rate is often over 100%, and sometimes over 1,000%!

It’s easier to get a loan at a reasonable interest rate when you’ve established a reputation as a responsible borrower, so it’s a good idea to build up good credit before you need it. This means making all your payments on time, even when it’s somewhat difficult. Your student loans are a great place to start building a good credit history. Make your minimum payments on time, and if you find yourself unable to meet your payments, take action immediately: Call and negotiate a lower payment or even a break from payments (referred to as a deferral). Good credit you can help you out during times of financial stress—so don’t let bad decisions ruin your credit!

Smart Saving Strategies

As economists have studied people’s financial lives, they’ve come up with some smart strategies to help you manage your financial life successfully. Here are a few such strategies:

Plan ahead to avoid temptation.

Set a budget and stick to it.

The smart way to save is to make your spending and saving plans in advance by setting a budget. It’s valuable, because people find it easier to make good decisions in advance. In one famous experiment, when people were asked to choose a snack to eat in a week’s time, many chose a piece of fruit over a chocolate bar, but when offered a snack to eat right away, they chose the chocolate. The same problem makes it hard to save unless you’ve planned—that is, budgeted—your spending in advance. If you’re constantly deciding in the moment how much to spend, you’ll easily find yourself giving in to temptation. Instead, assess your financial situation and make a plan for how much to consume—and therefore how much to save or borrow—when you’re best able to be analytic and forward-looking. Once you’ve made that plan, stick to it. If your plan isn’t working, then go back and re-assess it.

Make sure you can handle an unexpected cost.

Once you graduate, you may find yourself in a predicament in which you think you should start saving, but you have a mountain of student debt to pay. What should you do? Remember that paying off debt is a form of saving, so choosing to pay off your debt is moving your net wealth in the right direction. But unless you can borrow money easily, you also want to accumulate a rainy-day fund to protect yourself in case you lose your job, your car breaks down, or you have an unexpected health cost. So build up your rainy-day fund before you start making extra payments on your student loans.

Sign up for your employer’s retirement plan.

Most employers will offer you some sort of retirement saving plan. Even if you have student loans or other debts, in most cases you should sign up for it. That’s because most employers match your contributions to their retirement plan, usually kicking in extra money—say, a percentage of what you contribute—up to some maximum. For example, your employer might kick in 50 cents for each dollar you put into your retirement plan up to 2% of your salary. This would mean that if you saved 2% of your $50,000 income, you’re putting $1,000 per year into your retirement plan, forcing your boss to kick in an extra $500. Never miss the opportunity to get free money from your boss. Don’t procrastinate; sign up for your employer’s retirement plan on your first day of work.

Plan to save more tomorrow.

One of the reasons people struggle to pay their student loans or to save adequately for retirement is that they get used to their current consumption spending and don’t want to give anything up. Financial advisers often tell people to give up some small habit like a daily coffee and to save that money instead. But giving up an already established habit is hard.

What’s easier is planning to save out of future income. One plan for building your retirement savings is to plan to keep making your student loan payments forever. Once you graduate, you’ll be making regular payments to your lender. Once you’ve paid off your loans, you can keep making those payments—but make them to your retirement account. You’ll never miss the money because you’ve never had a chance to spend it. You can do the same thing with every increase in your pay: If you get a raise of 10% with a promotion, put half of it straight into your retirement account—you’ll still feel the increase in your take home pay, while saving even more.

Keep as much of your money as you can.

This sounds obvious, right? But it turns out that there are some important things you need to do to follow this advice. The first is to avoid high fees. When you put your money in a retirement or investment account, you’ll be charged fees. You need to look for the smallest fees you can to keep as much of your money as possible. Minimizing fees also means trying to avoid carrying a balance on your credit card or holding on to other high-interest-rate debt for long.

You can also hang on to more of your money if you take advantage of government programs designed to increase saving. There are many different programs—mostly geared toward saving for retirement or education—but they all boil down to the same idea: If you save into these government programs, you’ll get a break on your taxes. And a break on your taxes means keeping more of your money.

. But your consumption shouldn’t follow the same pattern. The logic of consumption smoothing is that you should save money in those phases of your life when your income will be predictably higher, so that you can spend more than your income when it’s lower.

. But your consumption shouldn’t follow the same pattern. The logic of consumption smoothing is that you should save money in those phases of your life when your income will be predictably higher, so that you can spend more than your income when it’s lower.