New technologies in the form of flexible production systems enable companies to produce smaller batches and be profitable. Toyota has made an art of it.

New technologies in the form of flexible production systems enable companies to produce smaller batches and be profitable. Toyota has made an art of it.Follow the path of least resistance.

Any customer can have a car painted any color that he wants so long as it is black.

—HENRY FORD

IN 1909, HENRY FORD PROPOSED A RADICAL IDEA, THE world embraced it, and thus was launched the age of Mass Production and Mass Consumption—mass with a capital M. Ford made one car—the Model T—in one color, basic black. If you wanted a Ford, that was the choice. And it worked. By paying attention to the mainstream of the market and neglecting the niches, Henry Ford became history’s first billionaire.

Unfortunately, many executives today are stuck in a Henry Ford time warp. They continue to believe that only the mainstream mass market is attractive from the point of view of growth potential and profitability. Large, established multinational firms tend not to bother with marginal customers. “Small niches are just not worth the effort,” they claim.

But consider how much the world has changed over the past 100 years:

New technologies in the form of flexible production systems enable companies to produce smaller batches and be profitable. Toyota has made an art of it.

Selling to a small market segment in just one country may be a losing proposition, but doing so across a large number of national markets can be enormously profitable.

Most important, niches can be thought of as stepping-stones into the mainstream mass market, especially when entering a foreign country with large, entrenched local competitors.

Companies from emerging markets have perfected the use of market niches, homogeneous groups of customers with unattended needs by the market leaders, as launching pads to global domination. We saw in the last chapter how Embraer used operational excellence to outpace the competition, but the Brazilians also aggressively moved into the overlooked need for regional jets, a niche that industry giants Airbus and Boeing dismissed as a residual market. Now, Embraer is applying the same principles in other well-defined niches, including executive, VIP-transport, and light-training jets; intelligence-surveillance-reconnaissance aircraft; and cargo aircraft.

This is also how Haier of China became the world’s largest household appliances brand. Haier’s global success started with a timid product launch in a tiny niche segment of the U.S. market, one that established firms didn’t even know existed. Modelo, the Mexican brewer, went global similarly, within the niche of light, exotic import beer with its famous Corona Extra label. Natura of Brazil is not yet the largest cosmetics company in the world, but it is growing rapidly by focusing on market niches neglected by huge companies such as L’Oréal and Procter & Gamble.

Incumbent firms tend to look down on an emerging market firm entering a small, underserved niche in their own backyard. They see an annoying gnat, not a Trojan horse using the path of least resistance to take over the stronghold of an established brand. Indeed, often they don’t catch on until it’s too late. “When I look across the major appliance categories, I’ve not yet seen [Haier] have any perceivable position,” Whirlpool’s David L. Swift, the head of the North American Region, told a reporter back in 2006.1 Within four years, Haier had become the leading brand in the industry. Embraer faced a similar skepticism from the industry’s aristocratic establishment. “Years ago our competitors said: ‘How dare those ugly ducklings from South America try to sell a jet in the Northern Hemisphere,’” remembered Satoshi Yokota, Embraer’s head of engineering and development. “Fortunately, they underestimated us.”2

Often, too, established companies find niches—and the effort required to reach them—beneath their dignity. L’Oréal, one of the world leaders in personal-care products, always thought that direct sales represented a second-tier market that could tarnish the image of the company and its brands. Delivering catalogs through independent salespeople or organizing sales events in someone’s living room simply wasn’t what the French company did to sell its products. That is, until Natura showed that approaching the client directly with a quality, even high-end product was a great way to gain market share. Nowadays, given the importance of direct sales in emerging markets, L’Oréal is considering an acquisition specialized in direct selling—tacitly admitting failure.

In many ways, established firms miss the relevance of niches because of deeply ingrained beliefs about the nature of the world. They think globalization equals standardization of tastes, preferences, and needs. They believe that globalization is a tsunami, when it really behaves more like a tornado, bringing about big effects in some specific areas while leaving others unscathed. Customer preferences remain fragmented across countries and among customer groups looking for product differentiation and multiple brand offerings. The fact is, globalization has made niches more, not less, relevant.

Let’s examine how Haier, Modelo, and Natura stunned established firms by growing global out of a niche market.

The global market for household appliances is big and difficult to crack. We’re just too idiosyncratic about what we do within our homes. In some countries, people prefer front-load washing machines, while in others they like to throw their clothes through an opening on the top. Those preferences are further shaped by the intended location for the appliance—under a countertop or in a dedicated laundry room or closet. The size of the freezer in refrigerators needs to be large in countries like the United States, where people shop once a week, as opposed to Europeans, who go to the grocery store around the corner every day. Preferences also differ within national markets: older consumers expect reliability from their household appliances, while younger ones look for special features. The needs of people with no kids differ massively from those with offspring. For a long time, European and American companies dominated this market with extensive portfolios of brands positioned to serve each of these different needs. But the likes of Electrolux, Whirlpool, Frigidaire, and GE bothered to serve only relatively large segments of the market.

Enter Haier, the world’s new leading household appliances brand. Its beginnings were inauspicious at best. Imagine a gloomy and decrepit refrigerator factory not far from the workers’ living quarters in a dirty part of town. The wooden window frames had been taken down by employees to provide fuel for heating. The scene was chaotic, with tools and equipment scattered everywhere. This is not one of the Victorian-era factories described by Charles Dickens, or one of Karl Marx’s “satanic mills.” It’s the Qingdao General Refrigeration Factory, located in the namesake city on the East China Sea halfway between Beijing and Shanghai. The Qingdao factory was founded in 1955 by a group of workers as a collective enterprise just before the infallible Chairman Mao launched his ambitious, and ill-conceived, Great Leap Forward, intended to remake China as an industrial power.

The company languished for decades, one of hundreds of minor appliance makers in China. Then, in 1985, seventy-six refrigerators were found to be defective, and Zhang Ruimin, who had been appointed as CEO a few months earlier by the local government, asked the workers to smash them with a sledgehammer. Nobody followed his orders—they would rather repair the faulty appliances and take them home, given that each was worth two years of their wages. Zhang then took aim at the first refrigerator himself, and the astounded workers followed suit. Zhang was charismatic and authoritarian, and well-attuned to American management ideas. He admired Frederick Taylor, Abraham Maslow, and Peter Drucker, and was intent on improving operations, raising quality, acquiring other factories, and saturating the domestic market with over 100,000 points of sale. His ultimate goal was both simple and wildly audacious: to become the world’s leading appliance brand.

Technology was at the core of Zhang’s plan to turn the company into a producer of high-quality goods, but Haier lacked state-of-the-art capacity. So in 1985, the same year he led the fridge-smashing party, Zhang signed an agreement with Liebherr to license the low-temperature refrigerator technology commonly referred to as four star, which allows for the preservation of foodstuffs between 3 and 12 months. Haier thus became the only Chinese company offering this product in the local market—other Chinese manufacturers made two-star refrigerators that preserved food for up to one month. But Haier wasn’t a passive licensee. The company developed its own technological base and capabilities. “First we observe and digest [a new method],” Zhang said, “then we imitate it. In the end, we understand it well enough to design it independently.”3

Superior technology was not enough to conquer the Middle Kingdom, however, so Haier committed to delivery in no more than 24 hours within 150 kilometers of a point of sale, and that broke the logjam. As the 1990s wore on, customers in the high-growth Chinese economy could not get enough Haier appliances.

In 1991 the company changed its name and brand to Haier—the Chinese transliteration of the second part of the brand name Liebherr—and started to diversify by taking over 18 domestic companies, most of them in the Quindao area, producing an array of electric appliances such as air conditioners, freezers, microwave ovens, and washing machines. Zhang is fond of saying that these companies were “stunned fish,” meaning that they had good factories and distribution networks but poor management. Soon after acquiring them, Zhang turned them around in the same way he had reset the original refrigerator factory, by securing new technology through alliances and active learning. Haier then had an ample portfolio of appliances and design capabilities that enabled it to adapt to the specific needs of various customer groups.

The corporate culture nurtured by Zhang and the autonomy granted to each regional subsidiary within China made it possible to put into practice one of the Haier’s mottos: “Never say no to the market,”4 even in bad times. At the end of the 1990s, Chinese consumer spending was rocked by a combination of high unemployment and oversupply of durable goods, but that didn’t slow Zhang down. He pushed his managers to attain and maintain high satisfaction levels even among the least significant customers. “No matter how small they are,” said Zhang, “they are ours to keep.”5

A telling example of this philosophy is the case of the washing machine turned vegetable rinser. Haier’s technical after-sales service in one region discovered that some washing machines were breaking down because customers used them not only to wash clothes but also to rinse potatoes and vegetables. Instead of blaming customers for misusing its products, Haier designed a specific, dual-use model for that market niche.

Once Haier had become the dominant brand in China, with a commanding 30 percent market share, the company went global, first making appliances for American retailers to sell, then launching its own branded products. The timing was right. China became a member of the World Trade Organization in 2001, and this meant Haier would no longer have the domestic market for itself. The best defense, Zhang decided, was to mount an attack abroad.

Rather than reach for obscure, underserved markets, Haier followed a philosophy of “first the hard, then the easy.” Zhang’s number one target was the United States, the most competitive market of all. Why? As Zhang put it, “If we can effectively compete in the mature markets with such brand names as GE, Matsushita, and Philips, we can surely take the markets in the developing countries without much effort.”6 (Note how closely this approach echoes the lyrics of the famous song “New York, New York”: “If we can make it there, we can make it anywhere.”) The key issue, though, was not the market the company chose but rather how Haier attacked the American colossus—not frontally, but one product niche at a time.

Haier also benefited greatly during this critical period from the advice of Michael Jemal, who at the time was in charge of Welbilt, an independent distributor of imported appliances. On his own, Jemal went to China and convinced Haier executives that a market existed for Chinese-branded appliances in the United States. Jemal specifically identified an underserved niche for compact refrigerators among college students and took the idea to Wal-Mart and other retailers, who responded enthusiastically. Haier executives were impressed and decided to grant Jemal exclusive rights for distributing Haier products in the United States. Shortly thereafter, he was asked to become chairman and CEO of the newly created Haier America. Next, the company turned to wine coolers, also sold through channels directly to the relevant niche market. After that, Haier launched Frog TV, a learning TV set for children, which did not sell well but helped raise brand awareness.

Jemal’s approach was disarmingly simple and a thorough revelation of niche thinking. GE, Whirlpool, Maytag, and Frigidaire “can step on us anytime they want,” he said in 2001, “because we are so small compared to them in the United States. So we don’t look to compete. What we do is try to find our own position.”7 One of those positions included a chest freezer with a pullout drawer, something never seen before in the appliances industry. In fact, this model—with a top part using a conventional lid and a lower section with a pullout drawer for easier access—was designed following a customer suggestion and a tentative blueprint made by Jemal, and the first unit was produced within one day. “Many companies have a lot of ideas,” Jemal said. “The reason we have the winning strategy is that we have the speed, the innovation, and the desire to be the best. You can’t find another company that can design a product in 17 hours.”8

Haier, though, did not stop at niche dominance. The company thought of small market segments as stepping-stones in the process of conquering the mainstream of the market by gradually introducing new product lines aimed at covering a wide spectrum of needs. Ten years after the initial assault, Haier sells its entire product range in the United States, many of them built at manufacturing facilities in Camden, South Carolina, to better serve the market on a timely basis.

Haier has followed the same core philosophy to break into other markets around the globe. The company entered the brutal German market with air conditioners. When distributors there proved reluctant to carry the product, Haier arranged for quality control to be undertaken by a European independent laboratory in order to show that its units outperformed some competing German-made products. Step by step, the company introduced products not only in Germany but also elsewhere in Europe, focusing first on the unattended needs in each market. After setting up a joint venture to manufacture air conditioners in the former Yugoslavia in 2000, the company established its European headquarters in Italy and a year later acquired a refrigerator plant.

In Asia, Haier entered Indonesia first through a joint venture set up in 1996, initially aimed at producing refrigerators. Power shortages and problems with voltage led Haier to design low-consumption refrigerators able to function with variable voltage. Other Asian and Middle Eastern countries followed. In 2002, Haier entered Japan through an alliance with Sanyo with midsize appliances, ideal for typically smaller Japanese homes. Interestingly, Haier has recently acquired Sanyo’s refrigeration and washing machine business units from Panasonic, which had purchased them as recently as 2009, turning the Chinese company into the fifth-largest appliance manufacturer in Japan.

Nowadays Haier is a truly global company with a worldwide sales network and 29 manufacturing facilities and 16 industrial parks in the United States, Europe, Asia, the Middle East, and Africa. The company boasts eight research and development centers in the United States, Germany, Japan, and South Korea, and has been the world’s best-selling brand of major appliances since 2009. Only Whirlpool and Electrolux, which market their products through numerous brands, have a greater global market share. This is a huge achievement given the company’s humble origins.

Haier’s unending growth has been a major nightmare for Whirlpool, which continues to hold the lead position in manufacturing household appliances thanks to its commanding market share in the United States and its 2005 acquisition of Maytag. Whirlpool executives, though, know better than most Haier’s uncanny ability to find the path of least resistance to meeting customer needs. “We are organized to understand what customers want and to meet those needs, which are sometimes quite differentiated,” said Zhang. “Large companies are established and slow moving, and we see an opportunity to compete against them in their home markets by being more customer focused than they are.”9

Haier has looked into growing in the United States and elsewhere through acquisition. It, too, had been interested in Maytag, and in 2008, the company looked closely at buying GE’s appliance division. But Zhang and Haier are patient and confident enough to realize that they can enhance their position as the world’s leading brand through hard work and organic growth.

Beer is the world’s most popular and probably oldest alcoholic beverage. Our Neolithic ancestors are thought to have started brewing it more than 9,000 years ago, not long after they mastered cereal farming. Written records from ancient Egypt and Mesopotamia detail methods of beer production. Germanic and Celtic tribes later spread the brewing secrets throughout Europe. The industry is both very global—dominated by Anheuser-Busch InBev and SABMiller—and extremely local, with thousands of regional and local brewers catering to some of the smallest market niches you will find in any consumer product category.

According to Euromonitor International, humans consume about 187 billion liters of beer each year. That’s a whopping 108 servings of beer annually for each person 15 years old and above, and amounts to nearly 80 percent of total consumption of all alcoholic beverages. China, the United States, Europe, and Latin America are the largest markets, but this is a business with $240 billion in annual sales worldwide.10

Brewing is also an industry in which 5 of the top 10 players are emerging market multinationals. In 2008, InBev of Brazil completed the acquisition of Anheuser-Busch and became the global market leader with nearly 19 percent of volume sales, followed by SABMiller, Heineken, and Carlsberg. The rest of the top 10 are made up of three Chinese firms, Grupo Modelo of Mexico, Molson Coors, and Kirin of Japan.

Founded in 1925 and controlled by a coalition of families since the early 1930s, Modelo has only 3 percent of global volume sales, but it has the most successful global “exotic” niche brand of all: Corona Extra. In 2011 Corona Extra was ranked the world’s second most valuable beer brand ($3.9 billion), according to Interbrand, closely followed by Heineken ($3.8 billion). The number one spot went to Budweiser ($12.3 billion),11 but Bud’s strength derives mostly from its big market share in the United States and Canada. Corona Extra, by contrast, sells well not just in Mexico but also in the rest of Spanish-speaking Latin America, the United States, Canada, and China.

“There’s no mystery about brewing beer. Everyone can do it,” said Michael Foley, Heineken’s president in 1995. “It’s all about imagery, and value perception … Beer is all marketing. People don’t drink beer; they drink marketing.”12 And Corona—a light golden beer marketed as “la cerveza más fina” (the finest beer)—has clearly beaten the Dutch firm at that.

“The marketing of Corona has been brilliant, whereas the marketing of Heineken has become schizophrenic,” wrote Philip Van Munching in Beer Blast, a book about the U.S. beer market. “Corona Extra’s association with the tropics and being drunk with a lime are indelible images that work.”13 Van Munching, it should be noted, is no innocent bystander in the beer wars: his family was one of Heineken’s U.S. importers from the 1930s to the 1990s.

How have the Mexicans managed to create a global brand in an industry in which all the other major players are lucky to succeed in one or maybe two major markets at most? The answer is niche thinking, coupled with market necessities. The Mexican beer market is both large and sophisticated. The conquistadors brought with them European-style brewing techniques. Upon independence from the Spaniards, the industry expanded quickly during the nineteenth century thanks to the construction of the railroad, which facilitated the transportation of cheap malt from the United States. Today, 90 percent of the industry is dominated by two giants, Modelo and Femsa, which was acquired by Heineken in 2010.

After consolidating its position in the Mexican market, Modelo was forced to go international to keep growing. The United States was the obvious choice because of proximity but presented daunting challenges, including entrenched competitors and sophisticated consumers. Export sales across the border during the early 1980s were low because Modelo was forced to redesign its bottle to satisfy a Puerto Rican brewer that had registered the Corona name. In 1985, Modelo finally managed to settle the legal issue and quickly started to sell the Corona Extra brand in its vintage transparent bottle with the characteristic long neck.

But the company had already set the stage for its assault on the U.S. market. In 1979, it signed contracts with two separate importers. The first focused on the states west of the Mississippi and initially targeted college students, some of whom had tasted Corona in Mexico during spring break. Beach parties were the main advertising theme for this niche. The second importer targeted Mexican immigrants by appealing to their nostalgia for the homeland. This dual-pronged approach to the U.S. market enabled Modelo to establish a beachhead in two different demographic niches. Sales ballooned from 1.8 million cases in 1984 to 13.5 million in 1986, behind only Heineken among imported beers.

During the late 1980s both importers stumbled over decisions concerning the choice of local distributors and points of sale, but by 1997, Corona Extra had surpassed Heineken to become the best-selling beer import in the U.S. market. By that time Corona was selling well outside the two original niches of party-going college students and Mexican immigrants. The beer was now positioned as a “vacation in a bottle” and “fun in the sun.” Corona Extra’s light character and smooth taste were also familiar to a broad swath of American beer drinkers, something that undoubtedly helped expand sales beyond the original base targets. “You just have to have it,” the manager of a popular singles bar and restaurant in Washington, D.C.’s Georgetown neighborhood told the New York Times in 1999.14 Pricing was also a key ingredient of success: higher than domestic beers but lower than Heineken’s.

Above everything else, Modelo got it right when its marketers decided to position Corona Extra as a premium import beer highlighting a specific lifestyle. The idea was to appeal to young people who wanted to have fun with their friends but did not want to develop a beer belly. “Corona used the parallel of a tropical vacation as an icon of representing that balance of life’s priorities,” observed Don Mann, director of Mexican brands for Gambrinus Company, one of the two U.S. importers.15 Serving the beer with a wedge of lime at bars and restaurants also reinforced its exotic origin and enhanced its taste. Competitors have since tried to jump into the same marketing space with brands such as Miller Chill and Bud Light Lime, but with limited success.

The creation of the North American Free Trade Agreement (NAFTA) in 1993 invited firms on both sides of the border to look for new ways to either further infiltrate the other’s market or to collaborate. Modelo chose the latter route by forming an alliance with Anheuser-Busch, selling it a 17.7 percent equity stake in exchange for continuing to be its exclusive distributor in the Mexican market. But Modelo also held on to its two exclusive importers for the U.S. market—a good decision since Corona sold in the United States much better than Budweiser and Bud Light did in Mexico, a trend that continues to this day.

As a result of its 2008 acquisition of Anheuser-Busch, InBev today holds a 50.2 percent equity stake in Modelo but has less than half the voting power. For all practical purposes—and despite going public in 1994—the Mexican firm operates as a separate company, the only major family-controlled beer company that remains in an industry once dominated by dynasties. Perhaps that is why, although the Corona brand is truly global, the company has stayed firmly rooted in its home country, where it is absolutely dominant. Modelo’s global success has been built solely on exports from its Mexican plants. The company does not own foreign breweries, although it licenses its brands in some markets.

Modelo’s global niche strategy has succeeded beyond anyone’s imagination. Corona Extra is the number one import beer in China, India, Indonesia, Japan, Thailand, Vietnam, Australia, Bolivia, Chile, Costa Rica, and Canada, as well as the United States; Modelo products are now sold in 170 countries. (True global reach, given that there are only 192 member states in the United Nations!) Thanks to Corona Extra, Mexico is now the world’s largest beer-exporting economy, having surpassed two of the most admired beer-producing countries, the Netherlands and Germany.

Entering the Chinese market, the world’s largest, didn’t prove as difficult as one might think, mainly because local competitors can’t offer such a differentiated, unique, and exotic product as Corona Extra. The main points of sale are bars, karaoke rooms, big retailers like Carrefour, and premium outlets. The company targeted white-collar urban males aged 23 to 30. To reach the right people in the right places, Modelo persuaded Anheuser-Busch in late 2006 to distribute Corona Extra in China. Anheuser-Busch was already well established there, with a 5.4 percent market share plus a 27 percent stake in Tsingtao Brewery, China’s second largest. With that kind of backing, Corona Extra quickly became the nation’s best-selling import beer. Plans now are to use Anheuser-Busch’s distribution in Brazil to introduce Corona Extra to the world’s third-largest market, after China and the United States, again positioning the brand as a premium beer for young urban professionals. Clearly, this is a company sequencing nicely from niche thinking to strategic partnerships to global dominance.

While it is true that the great recession, which began in 2008, has hit sales of imported beer disproportionately, Modelo has options at its disposal. “Corona is still a unique brand, which reflects a different lifestyle,” said CEO Carlos Fernández, who is a great-nephew of one of the company’s founders. “And this is not the first time that we’ve gone through a bump with that brand. I’m very confident we’re going to be able to make it grow.”16

Modelo can make acquisitions, launch new brands, and ride the wave of growth in emerging markets, where it is uniquely well positioned. “One of our goals is we want in the next [several] years to have almost 50 percent of our revenues coming from foreign markets. Today it’s 40 percent,” said Fernández. “Australia is having very good momentum. I think Asia will be very important for us going forward. Latin America has been really a surprise for us in many ways. Countries such as Chile, Argentina, and Colombia [have shown] double-digit growth.”17

We saw in Chapter 1 that emerging market companies have not yet conquered every industry. In IT services, firms like IBM or SAP are still at the top of their game. Personal care offers another example of how American or European firms can hold their ground in the face of stiff competition from emerging economies—or lose that same territory.

Cosmetics, fragrances, and toiletries generate nearly $400 billion in sales annually. It’s a huge market, one that will never go away. No matter age, gender, health condition, or even wealth level, people spend a significant share of their income on personal care. Moreover, many products are aspirational. Leonard Lauder, the chairman emeritus of the Estée Lauder Companies, likes to say that lipstick is the most recession-proof consumer product the world has ever seen.

But big, personal care is also a difficult business. The industry is dominated by giants such as Procter & Gamble and L’Oréal, each with about 10 percent global market share. However, fragmentation of tastes and heterogeneity of needs due to climate, biology, and culture, has led to the proliferation of brands and product variations.

Enter Natura Cosméticos, perhaps the most promising challenger in personal-care products from an emerging economy. The company’s recipe for success is all about niche thinking. It targets customers concerned with sustainability and reaches them through direct sales. In fact, one of the key sources of heterogeneity in the industry lies in distribution channels. You can find personal care products at department stores, supermarkets, drugstores, health and beauty salons, online … and through direct sales by means of representatives exploiting sales opportunities within their personal network. Global trendsetters like L’Oréal and Estée Lauder shun direct sales, but they happen to be a very important distribution channel in emerging and developing economies—precisely where the growth is. Whereas direct sales account for just 3.3 percent of the market in Western Europe and 8.4 percent in North America, in emerging economies the proportion stands at over 20 percent, with Latin America holding the record at a whopping 27.9 percent.

The world leader in direct sales of personal care products is Avon, a company with origins going back to 1886 and nowadays the fifth-largest player in the industry, with a market share of 3.4 percent. Avon’s expertise in direct sales has allowed it to sail through the Great Recession, thanks especially to its burgeoning business in emerging markets. The plain truth is that Avon’s main advantage when entering a new emerging country is that larger rivals like Procter & Gamble and L’Oréal have neglected direct-sale channels.

Avon, though, appears to have met its match with Natura. Founded in 1969 as a cosmetics laboratory with a single store in São Paulo, the Brazilian firm makes and brands cosmetics, fragrances, and personal hygiene products. The company is number one in Brazil, with a commanding 24 percent share in one of the fastest-growing global markets—and especially in the high end of the market. Avon ranks number three in the same market but competes mainly in the middle and lower segments. Natura also has significant shares in Argentina, Chile, Colombia, Peru, Mexico, as well as operations in France aimed at learning and serving as a platform for further expansion in Europe.

Natura’s business model rests on three pillars:

An appeal to ecology, sustainability, and social responsibility. The company started by using natural ingredients in all formulas and increased this commitment by adopting carbon-neutral operations, refill packages, sustainable extraction of ingredients, and recycled and recyclable materials. Natura uses only vegetable oils in its soaps and creams, instead of animal fat and synthetic components. While this approach presently limits the size of the market, potential future growth opportunities are tantalizing. In 2000, with the launching of the Ekos product line, the company turned itself into a leader in sustainability as well, using Brazil’s phenomenal biodiversity as the sole source of ingredients. The company has established 19 alliances with indigenous communities in the Amazon basin to source herbal raw materials and vegetable oils. These alliances aim at ensuring active ingredients and other raw materials meet tight sustainability standards along the entire value chain, from manufacturing to packaging.

Managing this network of suppliers is exceedingly complex because it involves “local communities, cooperatives, NGOs, research centers, and governmental agencies,” said Marcos Vaz, sustainability director at Natura. “But in the end everybody wins: nature, communities, customers and Natura’s consultants [as direct-selling agents are known] … because creating wealth for everybody, from towns to forests, is the essence of the Ekos line.”18 According to Cochairman Pedro Passos, “Ekos is the materialization of what we have been striving for, in terms of values—natural active ingredients, awareness and responsibility. Our company is reaffirming its origins.”19

An emphasis on rapid innovation. Natura is innovative not only in terms of sustainability but also in the speed with which it brings to market new products that take advantage of the rich array of Brazil’s natural resources. To accelerate product development and keep costs under control, the company has launched partnerships with scientific institutions in Brazil and abroad, MIT among them. This includes the commercial use of ingredients from Brazilian biodiversity as well as the “sustainable use of natural resources, social biodiversity, eco-design, and environmental indicators.”20 Astonishingly, Natura generates more than 60 percent of turnover from products launched in the prior 24 months.

A big bet on direct sales. Beginning in 1974, Natura has organized an extensive network of 1.2 million independent sales consultants, of which one million are in Brazil. To reduce costs and preserve flexibility, consultants are not employees of the company. However, the company works very closely with them in order to ensure that they advise clients properly regarding which products to buy and how to use them, and follow Natura’s principles and values. For instance, the firm wants all customers to know that it recycles printed catalogues. “From the beginning, Natura’s consultants always had a more important role than just make sales,” said Guilherme Peirão Leal, Natura’s cochairman. “They had to be trained to provide customers with a deeper assistance in such a way that they can identify their esthetic needs and indicate to them the most appropriate products. Sales per se shouldn’t be the final goal. Through consultants, we aim at turning the selling of our products into inspirational, self-awareness moments, to be involved in social and environmental issues.”21

Thanks to this three-pronged strategy, the company has achieved a commanding leadership position in Brazil. Some customers value the use of active ingredients from the Amazon rainforest. “Natura’s make-up is truly expensive, but some products you can’t find in any other brand,” one customer told a Bloomberg reporter. Others value the company’s commitment to sustainability. “There’s confidence in the brand,” another customer said, adding, “I like the idea of being ecologically correct.”22 This is basically the same approach tried by the Body Shop, but with far deeper commitment. In the late 1980s, the Body Shop appeared to be similarly embracing the values of corporate social responsibility and sustainability through multiple initiatives around the world. One of the most renowned was an alliance with the Kayapo tribe from the green forest in the Amazon, which supplied the company with nut oil for a specific product line. Part of a wider program called Trade Not Aid, the alliance received wide coverage in the press, positioning the company as both eco-friendly and an ardent promoter of fair trade. Eventually, though, the project severely damaged the image of the Body Shop brand when it became apparent that the entire operation was little more than a publicity stunt. As insufficient as the Body Shop payments were, they also made the Kayapo ineligible for government subsidies and thus forced the tribespeople to engage in additional activities that threatened the rain forest. The Body Shop, which has been part of L’Oréal since 2006, never recovered entirely from the bad press. Natura is almost certainly too close to the ground and sensitive to the situation to make anything like the same mistake.

Natura’s strong knowledge and market bases in Brazil represent solid advantages when it comes to future international growth. It’s not just the exotic ingredients. Brazil’s racial diversity means that the company has had to develop products for each type of skin, hair, and body shape. True, American firms are exposed to similar diversity in their home market, but they have not turned this into a source of competitive advantage. They deal with each ethnic segment separately without thinking about the implications for global growth.

Natura’s homegrown advantages certainly proved crucial to its expansion throughout Spanish-speaking Latin America, where direct sales are as important as in Brazil. Mere exporting didn’t do the trick: the company had to replicate its entire value proposition, niche orientation, and preferred distribution channel in each foreign market.

Consider Natura’s entry into Argentina in 1994. The direct sale model did not work well at first. Turnover among consultants was high until Alessandro Carlucci, Natura’s current CEO, was dispatched to overhaul the underperforming operation. In 2001, Natura turned the Argentine financial collapse into an opportunity by not raising prices and appealing to consumers’ sustainability values. The Argentine peso had lost two-thirds of its value against the U.S. dollar, reducing purchasing power substantially, especially when it came to buying imported products.

“We looked for ways to reduce costs and put ads in the major magazines stating that we would keep our prices steady for the time being and would change them if and when local salaries were adjusted,” explained Carlucci at the time. “The idea was to create a kind of social pact involving suppliers, employees, and customers, showing to the Argentinean market that we were there for good and expected profits in the long run.”23 In fact, this proved to be an extremely effective way of conveying Natura’s values to the Argentinean customer. The company presently has 329 employees and 53,000 sales consultants in the country. Natura has achieved similar successes in Chile, Peru, Colombia, and Mexico.

By now, these multiple and varied experiences have made Natura very effective at replicating its direct sales model abroad. “It takes between one and one and a half years to complete the product portfolio in each new country,” Erasmo Toledo, director of international operations, told us. “We neither enter with a narrow range of products nor with a wide one. A narrow range is not profitable for our consultants, and a wide range does not allow us to build progressively the brand. So we enter with a basic range of products and gradually enter new ones as we see the acceptance of the products, and train our consultants on how to use them.”24

Niche-focused global expansion, however, won’t work on autopilot. You need to think carefully about national variations. About 70 percent of Natura’s products are common across Latin American countries, but being effective across different geographies requires tweaking. To facilitate building the brand as well as coordinating the consultants, Natura established a few exhibition centers called Casas Natura in selected locations, mostly exclusive commercial locations in big cities. In these centers consultants receive training and customers can try the products, although they cannot buy them. In Mexico, Natura put in place a multilevel system of consultants, with only the top-tier being able to buy products directly from Natura. The company decided to make this adjustment because multilevel direct sales systems were common in Mexico, although Natura made sure that consultants across all levels complied with its values.

France is Natura’s only foray outside Latin America to date. In this market, they sell through stores and the Internet as well as via 3,000 consultants. The company views France as a learning lab and launching pad for the rest of Europe. Meanwhile, there are huge growth prospects to exploit back in Brazil. According to Euromonitor, Brazil is the third-largest market in the world for personal-care products, behind the United States and Japan, and ranks as the most important in direct sales. The firm, however, stands to win from global sustainability trends once it feels ready to do so. Meanwhile, Avon, Procter & Gamble, and other leading companies are in a bind. None of them has the powerful combination of niche thinking, sustainability focus, and direct-sale experience that Natura possesses.

The success of emerging market multinationals such as Haier, Modelo, and Natura shows that global markets are an amalgam of heterogeneous niche segments in which a variety of strategies can be profitable. Niches, after all, are specific customer groups in which products or services enjoy tribal acceptance. When well managed, niches can become retinues of fanatic followers whose raw enthusiasm can level the playing field when it comes to taking on established firms with greater technological and marketing capabilities.

In today’s hypercompetitive global economy, established multinationals need to pay attention to marginal niches for both offensive and defensive reasons. Turning your back on niches courts losing important expansion opportunities outside the home country. Whereas L’Oréal encounters difficulties in emerging markets, Natura and Avon are thriving in them thanks to their expertise in direct sales. Recently L’Oréal considered the possibility of acquiring Avon or another direct seller, although it backed down after assessing the thorny integration issues.

Neglecting niches also can lock your company out of ill-defined but slowly emerging broad markets. Examples of this pattern abound. Back in the 1990s, General Motors enjoyed a technological lead in developing electric vehicles, but top management and the board thought that launching such a product would be disruptive to corporate growth and unprofitable given its limited, niche appeal. Wrong call: most automotive analysts expect hybrids to become much more than a niche in the near future, a trend that will benefit companies like Toyota, which never gave up.

Shifting consumer demographics also turn niches into large markets. Two decades ago, clothing companies ignored the 65-plus age niche. Today, they can no longer afford to do so. Within two decades, it will be the dominant segment in Europe, Japan, South Korea, and China—half of the global economy! Publishers of scientific books and journals grasped the new opportunities in digital technology while trade publishers did not. They thought it would remain a niche market for a long time—and were caught way off guard by consumers’ thirst for iPads, Kindles, and Nooks.

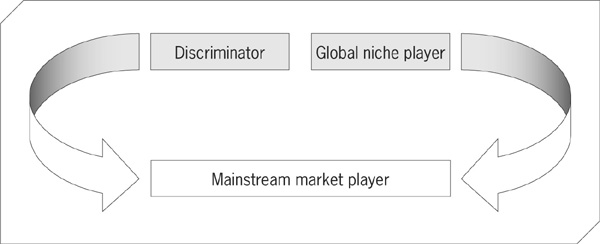

Underserved niches provide new opportunities for making profits, but they also represent weak points in the company’s defensive perimeter against the attacks of new multinational firms, especially those from emerging markets. For the underdogs and outsiders, market niches are important not only per se but also as points of entry into the mainstream of the market when a frontal attack is not possible. For these firms, following the path of least resistance by targeting niches does not necessarily entail addressing the same segment customers or introducing the same types of products. Niche companies do not always pursue the same niche across markets. Some niche-oriented firms from emerging markets are perhaps better thought of as discriminators because they offer in each country a specific product-segment combination adapted to the needs of local customers. Thus, there isn’t one but two different types of niche strategies:

The discriminator focuses on a different niche in each country without integrating operations across markets. Haier started its long march to global supremacy in this way.

Global niche players target the same niche of the market across countries. Natura and Modelo followed this path to success.

Later in the process of expansion, the legitimate aspiration to global leadership invites both discriminators and global niche players to move into the mainstream of the market. Haier is now in the process of making this transition (see Figure 2). But keep in mind that timing is everything. Discriminators and global niche companies cannot afford to move into the mainstream too early—or too late. It’s a fine balance that we explore in subsequent chapters.

FIGURE 2

Choosing the niche approach that fits your company.