an ambitious but still unfinished 105-floor skyscraper in Pyongyang.

an ambitious but still unfinished 105-floor skyscraper in Pyongyang.Learn and profit from adverse institutional environments.

If you have something at risk, you think differently.

—HENRY KRAVIS

Chaos is a friend of mine.

—BOB DYLAN

ONCE UPON A TIME, WAY BACK IN THE TWENTIETH CENtury, there were safe markets and there were risky ones. Safe markets offered predictability, minimal government interference, and a good infrastructure for doing business. Risky markets were mostly in the developing world, where governments often made capricious decisions, placed myriad obstacles for entrepreneurs, and lacked the minimal legal, financial, transportation, and telecommunications infrastructure for firms to operate.

Welcome to the twenty-first century. In multiple arenas of the global economy, the line separating safe and risky markets has become blurred, almost to the point of extinction. Many developed countries—the United States included—have chaotic and unpredictable governments, some so deeply in debt that they have let critical infrastructure become dilapidated over time. Stock markets, too, are no longer easily characterized as either safe or risky. More and more, financial-market volatility is global, not local.

While developed economies are sinking toward a world mean, many emerging economies have been rising to meet them and in some cases surpass them. Numerous developing nations have built a world-class infrastructure in areas such as ports, telecommunications, airports, high-speed rail, and business parks. In many of them, governments are not as unpredictable as they once were. Companies that learned the ropes in developing and emerging markets are capitalizing on these confusing trends. They’ve learned to live with chaos.

As we’ve already seen, Argentina’s Arcor, the world’s largest candy manufacturer, had no choice but to set up its supply chain from scratch. Its home country is notoriously unpredictable: more than 25 different presidents and 50 economy ministers have held office since World War II. Economic and trade policies abruptly changed every three or four years. Hyperinflation reached nearly 4,000 percent in 1989. “One of the main conditions for managing firms in Argentina is to be flexible, that is, to know how to adapt quickly to changes,” observed Luis Pagani, Arcor’s second-generation CEO. “With high inflation rates, the capacity to be flexible and to react quickly to changes is very important.”1 Other companies we looked at in previous chapters—Bimbo, Suzlon, and Haier—were similarly toughened by the vicissitudes of conducting business in at least semihostile, frequently chaotic environments.

Street smarts, of course, are not the exclusive property of emerging markets. Spain’s Telefónica, the world’s third-largest telecommunications operator, grew internationally by focusing on Latin America, a region widely perceived to be too risky at the time. In 1995, while the executives of North American firms were being driven around Peru’s capital in armored cars, Telefónica’s top brass walked around town unhurriedly and eventually made a bid for the state-owned telephone company more than twice as high as that by GTE and Southwestern Bell. “Telefónica had a very different idea of risk,” both in financial and in personal terms, Iñaki Santillana, former CEO for international expansion, told us.2

No one would accuse Ikea, the world’s largest furnishings retailer, of having developing market roots, either. Sweden is first world all the way. But when the company’s home-country suppliers imposed a boycott because of the firm’s harsh negotiation tactics, Ikea responded by adopting an emerging market mindset. Instead of fretting over the boycott, Ikea opted to pursue foreign sourcing and market opportunities, and let the disgruntled suppliers stew in their own juices. “Who knows what problems can do for you?” assert the authors of The Viking Manifesto, a study of Swedish management practices.

But while multinationals like Telefónica and Ikea show that the old guard can embrace and profit from chaotic environments, emerging market multinationals have perfected the art of doing so. Let us learn from Acer’s meteoric rise to the number two spot in worldwide personal computer sales, Orascom Telecom’s daring investments in Iraq and North Korea, and Bharat Forge’s vicissitudes in some of the world’s most difficult markets.

The story of Acer is one of the most tantalizing among emerging market multinationals. The firm was founded in the 1970s when Taiwan was a developing country struggling to find a place for itself in the global economy. Back in 1999, the company had a mere 3 percent global market share, the tenth largest. Nowadays, it commands a 13 percent share, second only to Hewlett-Packard’s 19 percent and closely followed by Dell with 12 percent and Lenovo of China with 10 percent.

In spite of being only 30 years old, the personal computer industry is very mature and commoditized. To succeed, you need to take risks, be bold, and engage the customer. As a contributor to the Chief Officers’ Network once put it, “The computer industry is like the fashion industry: It’s driven not by needs but by wants.”3 Like clothing companies, computer makers use planned obsolescence as a competitive weapon. You can’t run the latest software on an old computer, so you are compelled to upgrade your hardware. As with fashion, novelty and style are also vital to computer sales.

How, then, did Acer break into the top rank of this fashion-driven industry in spite of the technological and funding constraints it faced throughout its formative years? Instead of asking for loans, it maxed out retained earnings and invested abroad in collaboration with equity joint-venture partners. In the end, scarce capital proved to be a blessing in disguise. Yes, it carried risk, but the absence of ready funding taught the company how to economize on almost everything while developing new ways of expanding abroad. Acer learned to do more with less.

“Global expansion entails facing various challenges and requires making choices all the time,” explained Stan Shih, founder of Acer. “For a company pursuing sustainable growth, all kinds of risks will follow, like a shadow. But if you don’t take risks, what you create can be quite limited.”4 Fortune magazine once described Shih as “a fascinating combination of engineering nerd, traditional Chinese businessman, avant-garde manager, and international entrepreneur, with an outsize ambition and vision to match.”5 He and his company are also very much made in Taiwan.

Taiwanese electronics firms, of which Acer is the largest and most successful, make two-thirds of the world’s notebook PCs and cable modems, and one-third of all digital cameras and servers. They also manufacture the overwhelming majority of computer components, such as motherboards and LCD monitors. Like other Taiwanese firms, Acer used to make all of its products in Taiwan but has more recently shifted production to China and Southeast Asia.

Acer was founded in 1976 as Multitech, a distributor of electronic parts. Five years later, Shih changed the company’s name to Acer, from the Latin for “sharp,” and in 1983, Shih launched an IBM clone. At the time the company relied on outsourcing to IBM, Dell, Fujitsu, Hitachi, and Siemens for most of its revenue. All that began to change in 1987, when the company began marketing its first Acer-branded computer. In 1993, the company entered into a joint venture with Texas Instruments to manufacture DRAMs, setting up Taiwan’s first dynamic random access memory-chip fabrication plant, or “fab.” For several years, chips delivered windfall profits, but this investment turned into a liability when a glut developed in the global market after 1995.

Shih realized that high transportation costs; falling prices for processors, hard drives, and motherboards; high inventory expenses; and low margins required a new strategy. Under his Fresh Technology for Everyone campaign, Acer would put together the PC at local assembly facilities, using the most up-to-date components only after a customer had placed an order. In fact, Acer used to put an employee on a flight from Miami to each of its Latin American assembly facilities, carrying up to 1,000 Intel chips needed to meet customer demand on a just-in-time basis. Only nonperishable parts such as keyboards, mice, casings, and power supplies would be stocked on location. This fast-food approach earned Shih the title “the Ray Kroc of the PC business.” By emulating McDonald’s, the company reduced cycle times so that it could boot the computer just two hours after it was ordered.

Foreign expansion with decentralized and locally owned subsidiaries had made Acer scattered and complex. Seeing administrative costs skyrocket, Shih retired and brought in Leonard Liu as president of Acer Group and CEO of its U.S. subsidiary. A Princeton-trained PhD in computer science, Liu had been the highest-ranking Chinese-American at IBM. Rather than embracing Shih’s managerial philosophy of extensive delegation without accountability, and his emphasis on harmony, trust, loyalty, and employee-stock ownership, Liu insisted on establishing a panoply of organizational and financial controls, with the ultimate goal of turning Acer into a little Big Blue. Acer, however, didn’t need more bureaucracy. It needed a new strategy to succeed in a fiercely competitive global market with falling margins. Managers in Taiwan rebelled, dubbing Liu and his lieutenants the “parachute managers.” Liu lasted three years on the job, forcing Shih to stage a comeback. “In 1989, I thought IBM was the best-managed company in our field,” recalled Shih. “I supposed that Liu was more experienced and capable than I, but he was not an entrepreneur.”6

Shih decided to encourage his managers to design and launch new, innovative products. The Aspire computer, launched in 1995, was the biggest bet: a PC ahead of its time, designed as a home computer, Internet-enabled, and loaded with multimedia and voice-recognition applications. Runaway costs and lack of marketing savvy made it difficult for Acer to make money with the Aspire. The iMac, launched in 1998, stole the show, captivating a similar market of users eager for an easy-to-use home computer. Moreover, the iMac was cute, while Aspire was an ugly duckling. Acer lost over $100 million with the Aspire before pulling it out of the U.S. market in early 1999. Yet another problem with Acer’s strategy had to do with its dual role as a supplier for and competitor with IBM, Dell, and HP. The Acer brand was competing for customers against the very PCs that it made in Taiwan for the American brands.

In fact, Acer was still swimming upstream, struggling to emerge from its birth in a developing market, but what held the company back was also Acer’s latent strength. Operating in chaotic environments characterized by inflation, changing regulations, and sharp macroeconomic shocks had taught the company to be nimble and to evolve as circumstances required, and in 2001 Shih began to put that experience into play.

He started by spinning off all manufacturing activities while keeping design and selling of Acer-branded computers within the Acer company itself. He created Wistron Corp.—a name concocted from the combination of wisdom and electronics—which focused on contract manufacturing of PCs, servers, PDAs, settop boxes, and circuit boards. He also founded BenQ—bringing enjoyment and quality—to take over the manufacturing of mobile phones, displays, notebook computers, flash drives, and scanners. Both spin-offs were eventually listed on the stock market, with Acer reducing its equity interest to a nominal stake.

The reorganization paid off handsomely. Acer could now pursue its dreams of becoming a truly global brand by focusing on design and selling. Its personal computers would be manufactured by Wistron or BenQ, which would also continue to serve the needs of IBM, Dell, and HP. In 2005, Shih installed a fresh management team, including J. T. Wang as chairman and Gianfranco Lanci as CEO. Armed with its new strategy of totally separating design and selling from manufacturing, and the additional capital raised through the spin-offs, Acer could now go on a shopping spree. In 2007 it acquired Gateway for $710 million, a key addition to Acer’s already strong positions in Europe and Asia. The acquisition enabled Acer to have an “effective multibrand strategy and cover all the major market segments,” in the words of Lanci.7 Then Acer acquired Packard Bell, E-TEN, and nearly 30 percent of Olidata. In October 2009, Acer surpassed Dell to become the world’s second-ranked PC brand, a major accomplishment for an emerging market multinational.

Acer’s distinctive approach to decision making enabled it to cope with the chaos of operating across so many emerging economies with different local partners in each of them. “Conflict and disagreement will inevitably occur during the transformation of a company,” Shih wrote in his book, Me-Too Is Not My Style. “If executives treat conflict from a pessimistic viewpoint, they would rather settle disputes in fear that chaos may occur. To view it from the optimistic side, conflict is the process of building consensus.”8

Chaos was also something Acer had to contend with at home. The mercurial political situation in Taiwan and the uncertainty surrounding the future status of the island weighed heavily in the firm’s decision in the mid-1990s to locate manufacturing abroad, as a hedge against tensions with China over Taiwan’s first presidential election in 1996. In a U.S. diplomatic cable dated August 2006, and made public by WikiLeaks, Shih “described the current political situation in Taiwan as chaotic,” adding that “he didn’t have time to complain.” Instead, the cable reads, “He views political uncertainty as one of the limitations of the business environment he has to operate in.” But those same limitations were also constantly schooling Shih and Acer for life on a far bigger stage.

Acer took significant risks in over 20 Latin American and Southeast Asian emerging economies, honing skills in the developing world before entering the hyperdeveloped U.S. market. “We decentralized our management to local branches and gave them discretionary authorization to make independent decisions. We also decentralized our purchasing, assembly, and production activities. We abandoned the strategy of sole-venture channel expansion and allowed joint-venture partners to hold greater shares in our subsidiaries and to join our strategy-making and execution,” explained Shih, looking back at two decades of rapid and chaotic growth. “Although we made a big detour before entering the U.S. market, we built a solid foundation in peripheral areas and accumulated tremendous internationalization strength, which in turn helped us finally secure an advantageous position in the global market.”9

In regulated industries such as telecommunications, emerging market companies such as Egypt’s Orascom Telecommunications Holding (OTH), Mexico’s América Móvil, and India’s Tata Communications abound. These companies have excelled at expanding into other emerging economies, while giants such as Vodafone and AT&T have shied away from many of these risky markets. Why? Because even though established multinationals may have deeper experience when it comes to operating telecommunications networks, they find it difficult to expand into countries with weak institutional environments in which politicians and regulators have high levels of discretion and important gaps exist in the development of the infrastructure. Their comfort level is found in completely different environments: countries with basic infrastructures already developed and stable regulatory conditions, so that initial investment is low and changes in the rules of the game are less likely.

Years ago, for instance, U.S. telecommunications giant AT&T sold its Latin American assets to the Mexican group that owns América Móvil. The U.S. firm retained a minority stake in América Móvil and kept some collaborative links with the Mexican upstart, but this move was basically a concession that AT&T simply wasn’t as adept as América Móvil at turning a profit in an unpredictable environment. In 2010, Randall Stephenson, chairman and CEO of AT&T, crowed that “We have a major stake in Latin America through América Móvil, and it contributes a lot to our earnings and our cash flow,”10 but really he was just making the best of the same bad situation encountered by other old-line telecommunications firms seeking to operate in Latin-American and other emerging markets.

Consider the case of Orascom Telecom Holding, the Egyptian giant. It is hard to explain the growth of this company without taking into account its ability to operate in weak institutional environments subject to unusually high levels of risk such as Iraq and North Korea.

The origins of Orascom lie in a Cairo-based construction firm established in 1950 by Onsi Sawiris. While developing and building everything from dams and highways to shopping malls, the company acquired two capabilities that are invaluable to the telecommunications industry: experience in the execution of infrastructure projects and experience in dealing with politicians and regulators. Sawiris got a taste of political risk in 1971 when his business was nationalized. Five years later, under a new political regime more favorable to private business, he formed a second construction company that became the starting point of Orascom Group, a diversified conglomerate with three arms: Orascom Telecom Holding, Orascom Construction Industries, and Orascom Hotels and Development, each run by one of his sons. In the process, Sawiris became a legend in Egyptian business circles: “He’s a fighter; he started three times in his life,” his oldest son, Naguib, told interviewer Charlie Rose.11

Even though the Orascom Group had a presence in the IT field trading and distributing IT and telecommunications equipment, the company became a telecommunications service provider through acquisitions, not by growing from within. Its first foray was the purchase of InTouch, a domestic Internet service provider. In 1998, teamed up with Motorola and France Télécom, Orascom won the bid for the privatization of 51 percent of ECMS (Egyptian Company for Mobile Services), also known as Mobinil. So far, the story of Orascom might sound like the standard business saga of a well-connected family in a developing economy, but there’s much more to it than garden-variety cronyism.

In 1998, Onsi Sawiris stepped down after installing Naguib as chairman and CEO of Orascom Telecom Holding. Naguib was the one who realized the huge potential of telecommunications in emerging markets, thanks to the confluence of two factors. First, the lack of a preexisting telecommunications infrastructure and the flexibility of mobile networks meant faster growth than in the developed world. “Fixed lines were never available in our part of the world,” he said. “When the mobiles came, they overgrew the fixed line … so now the use is mostly on the cellular and not on the fixed line.”12 The second factor, he continued, was that established firms were reluctant to enter these countries because of the risks and also because, if they dared enter, they would not be patient enough to harvest the fruits. In his view, many companies that “ventured in Latin America sold too early. They didn’t understand the value of being in highly populated countries…. For me, [it] was a simple calculation. I knew [what’s] going to happen in our part of the world—we have more population, and revenues are going to be higher, and growth is going to be higher.”

Obviously, the risks were higher too, along with the returns, but the takeaway point is that Orascom was willing to go down this path only because of its experience in Egypt. “If you come from a risky destination, then the risk is relative,” Naguib Sawiris explained. “I remember when I went to Algeria, and they told me they were killing people there, and there are some bombs, and I said, ‘This is everyday news in my part of the world, so what’s the big deal?’”

From its highly educational home platform, Orascom started to expand into other emerging and risky countries that shared two features: high-growth potential and little competition. Sometimes these features were accompanied by weak institutional environments, which meant that once the investment was made, the rules of the game could change at any time. But Orascom and other companies in the telecommunications industry discovered that governments were in fact interested in developing infrastructure and would handsomely reward companies that helped them do so.

Over the first decade of the new century, Orascom Telecom entered countries that are a roster of global hotspots: Jordan, Yemen, Pakistan, Zimbawe (with the acquisition of Telecel, which included 11 licenses to operate in several sub-Saharan African countries), Algeria, Tunisia, Iraq, Bangladesh, North Korea, Burundi, the Central African Republic, Namibia, and Lebanon. One would be hard-pressed to find another company in any industry that exposed itself to such epic risks in so many chaotic countries. The Sawiris family also invested in Italy’s Wind Telecomunicazioni S.p.A. (which also operates in Greece and Belgium) in 2005 and, in 2010, merged Wind and Orascom with Russian operator Vimpelcom, becoming the sixth-largest mobile operator in the world.

There’s no mystery why established firms chose not to enter the countries in which Orascom has flourished: they would be at a distinct disadvantage if they did. Orascom’s entry into North Korea is illustrative: the company’s Egyptian roots gave it a large edge over Vodafone and other competitors, and its willingness to develop a telecommunications infrastructure where virtually none existed won expressions of gratitude from the Dear Leader. No country is more closed to foreign investment and capitalism than North Korea, yet Orascom managed to develop a positive relationship with the government. How?

The good vibes began when Orascom Construction Industries was developing projects in China close to the North Korean border. The company established negotiations with the North Korean government and in 2007 agreed to invest $115 million in a cement plant in exchange for 50 percent of its equity. The money was directed to modernize the facilities. As part of the deal, Orascom Construction was allowed to use North Korean labor in its China projects. The arrangement allowed Orascom to get to learn about the government’s plans to promote infrastructure projects as well as to establish trust with politicians and regulators. Orascom was eventually granted a 25-year license with an exclusivity period of four years, without any licensing fee, although with the commitment to develop the telecommunications network.

“With no competition and no licensing fees, it was a golden opportunity for OTH,” said Hassan Abdou, CEO of Orascom’s parent holding company, Weather Investments II. The North Korean project, he added, “is, in fact, relatively low-risk when compared to the potential reward. In most other countries, the licensing fees are a significant portion of the initial investment, but in this endeavor there was no such cost.”13 Recently, Orascom has also diversified into a North Korean bank and is active in construction projects such as the Hotel an ambitious but still unfinished 105-floor skyscraper in Pyongyang.

Here is what’s smart about Orascom’s approach to doing business in North Korea. First, the company negotiated a win-win situation with the government, sometimes going beyond the conventional arrangements in the industry. And second, it followed a strategy of escalating commitments in the country, taking a series of small steps over time as opposed to making a big investment at the beginning. But Orascom was never stubborn or obsessed about succeeding at all costs. In countries in which the business did not evolve according to the initial expectations, the company liquidated its investment. That is what happened, for instance, in Iraq. Orascom invested there in 2003 with the idea of reaping huge rewards once the war came to an end but divested in 2007 in light of poor returns and worse prospects. “The war was never over … and we have to invest another $1.25 billion for a new license … and I wasn’t willing to do that,”14 explained Sawiris.

Orascom also exited its investments in Jordan and Yemen, and most of the sub-Saharan countries when conditions shifted in ways that made it difficult to make money. But note, too, that Orascom’s divestments can hardly be considered failures. For instance, when leaving Iraq, Orascom sold the license for $1.2 billion, for a net gain of $920 million.

Orascom’s generally smart and sensible approach to risk taking in emerging economies hasn’t been flawless. In Algeria, Orascom’s most profitable market, the relationship with the government deteriorated after December 2007 when the company’s construction arm sold its Algerian cement business to the French group Lafarge for $12.8 billion without notifying the Algerian government about the deal beforehand. After this diplomatic mistake, the Algerian government levied Orascom for what it claimed were unpaid taxes and further threatened the company with nationalization. Orascom, for its part, has pushed back aggressively, seeking support from both its own Egyptian government and also from the United States on the grounds that American investors hold the majority of the equity of the company.

One U.S. diplomatic cable released by WikiLeaks notes that Alex Shalaby, a “close colleague of Naguib Sawiris, Chairman of Orascom Telecom and an American citizen … said Orascom Telecom had already approached the Government of Egypt (GOE) but he was unsure how much the GOE could actually do to help solve the problem … Shalaby said he plans to consult with key U.S. investors and may consider requesting U.S. government assistance to help settle the dispute.”15

However the Algerian dustup turns out, Orascom’s hybrid approach to investing in the so-called high-risk countries—one combining proactive negotiations with the government and a defensive strategy of taking small steps—has paid off superbly. Even before the Wind-Vimpelcom deal, Orascom Telecom had 109 million subscribers in 10 countries and was generating $3.825 billion in annual revenue. Orascom has carved out a position for itself in the global mobile telecommunications industry virtually unnoticed. The firm has simply flown under the radar screen of the established multinationals, positioning itself for continued growth while learning along the way how to cope with political risk.

Acer and Orascom Telecom give you an accurate taste of what embracing chaos in the new global economy is all about. Let’s now turn to India’s Bharat Forge, a company whose very reasons for existence are chaos and deprivation. The world’s second-largest forging company—after Germany’s legendary Thyssenkrupp Forging Group—Bharat Forge has 11 manufacturing locations in Asia (4 in India and 2 in China), Europe (3 in Germany and 1 in Sweden), and the United States (1), where it makes all sorts of metal parts and components such as crankshafts and axle beams for the world’s largest automakers, household appliance manufacturers, and other producers of durable goods.

The business of forging dates back seven or eight millennia, which essentially means that it is a mature and technologically stable industry. Forging companies manipulate ferrous or nonferrous metals at different temperatures in order to shape them by pressing, squeezing, or hammering forces. Making metal components through forging provides a number of advantages, such as strength, uniformity, and reliability. Being a supplier to the automotive industry, however, is no fun. Forging companies are under constant pressure to reduce costs and to increase quality levels, design capabilities, and speed of delivery.

The Hindi word jugaad is critical to understanding how this Indian enterprise was able to catch the wave of globalization in this ancient industry. Traditionally used to define the art of delivering creative solutions to overcome the lack of resources, jugaad describes an ancestral practice in India, a country handicapped by the lack of resources and infrastructure. Necessity, after all, is the mother of invention, and Bharat Forge provides an excellent example of how jugaad has helped many firms become global players in this new century.

Located in Pune, India, Bharat Forge Limited was incorporated in 1961 and first started forging automotive components in 1966. The company initially focused on the domestic market, with the only recurrent export orders coming from Russian companies in the mid-1980s. As recently as the late 1980s, Bharat Forge was completely unprepared to succeed in international markets. The company simply couldn’t meet the requirements of design capabilities, quality, reliability, and speed of delivery associated with the just-in-time manufacturing systems that the Japanese pioneered and the Europeans and Americans were trying to emulate at the time. Moreover, Bharat Forge used outdated equipment and relied extensively on labor rather than machines. The transportation infrastructure around its facilities was so poor that the company had little hope of ever being able to compete on a global basis.

In the spirit of jugaad, however, Baba Kalyani, chairman, managing director, and son of the founder, managed to turn Bharat Forge into “the Infosys of manufacturing.”16 How? For starters, he realized that the company could be a global provider for the automotive industry by taking advantage of India’s lower costs. The easy part was to buy state-of-the-art technology to meet global quality standards and to build up scale so as to lower costs even further. Hammers were replaced by automatic forging presses churning out 16,000 tons of forgings per month. Things became more complicated when reorganizing the company to make the most of the new technology, as it required a different type of employee. Blue-collar workers were replaced by white-collar employees capable of using computers for both design and production.

Bharat’s decision triggered a series of unplanned—and initially rather chaotic—adaptations that eventually made the company stronger and more competitive. The thousands of new technicians brought in to run the operations could be hired at a much lower cost than in the developed world, allowing the company to introduce multiple process innovations. One of the most remarkable was the so-called maintenance management system. A mechanized process was designed to minimize downtime—that is, the time during which production is stopped to do maintenance or repair work. Specifically, the system was aimed at anticipating problems in advance. “We feed into the computer, every day and every hour, every piece of data that tells you what you have to do during the manufacturing process, instead of making you deal with the problem during the downtime,”17 explained Kalyani.

As Bharat’s productivity improved, its edge in efficiency started to be acclaimed by its clients. “It is a top-class company,” said Wilfried Aulbur, former CEO of Mercedes-Benz India, adding that “We have had good experience and great pricing for the components sourced from them.”18 Even its competitors admire and respect Bharat. “They are always looking for better ways to produce goods,”19 said Farrokh N. Cooper, chairman and managing director of Cooper Corporation, another Indian forging company.

Once the production process was running smoothly, the next challenge was acquiring new customers, especially outside India, in order to make efficient use of the investments in physical and human capital. That didn’t come cheap, but Kalyani was willing to bet big to make the new customers happen. As he once said, “Risks—taking acceptable risks—are part of generating growth.”20 Faced with the disadvantages of its birthplace, Bharat Forge exposed itself to the creative, serendipitous side of risk as the surest way to overcome a vicious cycle of infrastructure deficit, technological backwardness, and lack of international competitiveness. To move forward, the company had to look for new clients, and to facilitate and direct that search, it adopted what was called a “4 × 3 strategy,” a growth map based on international expansion (to three regions) and diversification (to up to four main product areas) to make the company less dependent on single clients or industries. The company focused not only on chassis components for commercial cars—its traditional business—but also chassis for passenger cars as well as engine components. It also looked for customers in other industries (the fourth branch of diversification), such as electric power, oil and gas, rail and marine, aerospace, and construction and mining.

On the international front, Bharat Forge’s aim was to become a provider to the main clients in these industries in three regions: Europe, the United States, and Asia. Even though this growth strategy entailed risks, it was equally a derisk strategy since Bharat Forge became less dependent on single countries and even on single industries while also leveraging its installed capacity and its forging capabilities.

By the end of the 1990s, the strategy of expansion had paid off, and Bharat Forge was exporting to its target triad of Europe, the United States, and Japan, but the company also realized that it would be difficult to keep growing operating just from India. “After turning the business model of manufacturing process upside down and replacing the blue-collar workforce with over 2,000 white-collar staff (with minimum graduate engineering degree), the U.S. market opened up for us from 1992 onward,” remembered Kalyani. “By the end of 1999–2000, we had a fairly large volume of exports to every continent, and that’s when we started building and getting into global leadership in business. We wanted to be among the top 3–4 companies of the world. For that we needed to be in American, European, and Chinese markets … So we began formulating our acquisition strategy. We bought companies which had these customers and turned [them] around.”21

To enter into the final stage of its growth strategy and overcome once and for all the liability associated with the dire conditions at home, Bharat Forge embarked in a series of global acquisitions. In 2004, Bharat took over Carl Dan Peddinghaus GmbH & Co. KG (CDP), the leading German forging company at the time, with a subsidiary specializing in aluminum forgings. The next year it acquired Sweden’s Imatra Kilsta AB, the leading manufacturer of front-axle beams, which included a Scotland-based fully owned subsidiary, Scottish Stampings Ltd. That same year, Bharat Forge gained global reach by acquiring Federal Forge, securing a manufacturing presence in the United States, which is now one of its largest markets. In 2005 the company also established a joint venture in China with FAW Corporation.

These companies gave Bharat not only market share but also technology, as in the case of aluminum forgings. In addition, Bharat Forge raised the value of the acquired companies by applying the best practices generated in the Indian plants. With these acquisitions Bharat Forge became a dual-shore manufacturer—one that can produce with the low-cost advantages of emerging countries but with the design and reliability of developed-country suppliers while also benefiting from a direct contact and access with its main clients, OEMs (original equipment manufacturers) such as Ford, Toyota, and Volkswagen. “It is not possible to develop deep relationships with large OEMs sitting here in India. You need front-end operations in these countries. When a European customer knows that CDP has a low-cost strategy, they will support CDP all the more. Part of the business then gets shifted to India,” Kalyani argued.22

The quest for new clients also led Bharat Forge to enter into joint ventures aimed at selling nonautomotive forging products. The main partners here are French companies Alstom and Areva and the Indian NTPC Energy Systems. These partners are helping Bharat Forge gain a foothold in forging components for power plants, where it can exploit its manufacturing know-how. Indeed, the nonautomotive business was expected to generate one-third of all company revenues in 2011.

Bharat Forge is not alone among emerging market multinationals that have successfully embraced and neutralized chaos in their favor. Other automotive suppliers are becoming global leaders following a similar blueprint. Consider the case of Wanxiang, China’s biggest automotive supplier. Founded in 1969, it initiated foreign growth earlier than Bharat Forge. Once a supplier to big U.S. auto-parts companies like Visteon Corp. and Delphi, Wanxiang used acquisitions in the United States and Europe to expand its product lines and technology base. Many other cases could equally be highlighted here. The low-cost manufacturing skills of emerging market multinationals tend to blend well with the technological capabilities of the targets—a best-of-two-worlds combination.

Inevitably, this type of development makes one wonder why emerging market multinationals are the hunters and not the hunted. Why don’t companies from Europe or the United States make acquisitions in emerging economies to pursue this type of strategy? The answer lies in part in the fact that the established automotive suppliers from the rich countries have not reacted well to the ongoing global crisis, in large measure because they were less prepared to face chaotic situations than those in emerging economies. Moreover, as we saw in Chapter 1, this strategy requires attention to detail and excellence at execution, something that emerging market multinationals are much better at doing.

The stories of Acer, Orascom, Bharat Forge, and many other emerging market multinationals send a powerful message: Growing up rough is not always a disadvantage. In fact, it builds character and can be a clear-cut edge in dealing with chaotic market conditions and still-evolving governmental structures and agencies.

Because the infrastructure is often spotty at best in their countries of origin, many emerging market multinationals are forced to build and maintain efficient logistics and adopt creative solutions to overcome and/or compensate for the lack of needed resources—a skill set that helps them expand globally, as Bharat Forge illustrates.

Because the infrastructure is often spotty at best in their countries of origin, many emerging market multinationals are forced to build and maintain efficient logistics and adopt creative solutions to overcome and/or compensate for the lack of needed resources—a skill set that helps them expand globally, as Bharat Forge illustrates.

Without ready-made access to capital markets, many emerging market multinationals have had to embrace the risks of expanding internationally with local partners. Acer found it hard to learn how to do it but eventually succeeded very handsomely.

Forced to find their way through labyrinthine bureaucracies, emerging market multinationals become skilled at proactively negotiating with governments—their own and those of countries they hope to expand into. Orascom Telecom has it all down to a science.

Having succeeded in extremely difficult situations, emerging market multinationals are loath to give up. On the contrary, they manage to overcome whatever obstacle they face. “When I go anywhere and someone says ‘impossible,’ I laugh. In 90 percent of the cases, the impossible happens,”23 said Naguib Sawiris in 2010, reflecting on his experience at the helm of Orascom Telecom Holdings.

Interestingly, in almost all cases these are skills that long-established multinationals once had to develop themselves but have allowed to atrophy. Talking about Telefónica’s successful expansion into Latin America, former international chief executive Iñaki Santillana told us, “we have the best ditch-digging technology around […] When it comes to installing a million access lines in record time, no one can beat us.”24 In another interview he argued that in Latin American countries, “we were facing problems of unsatisfied demand that we had solved not long ago in Spain. These problems required short-term project management expertise. North American firms […] were not used to installing so many lines at the same time, as their market had become saturated a long time ago.”25

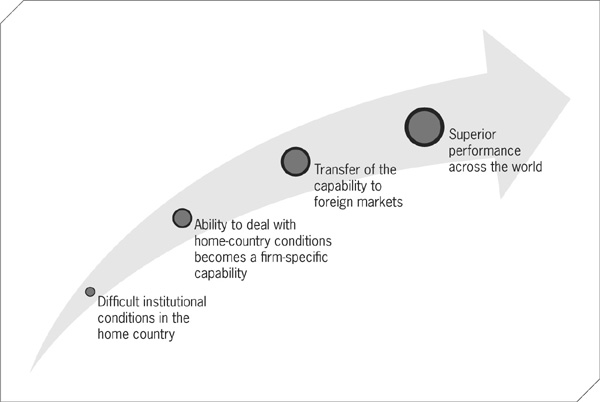

Figure 4 illustrates the value of recapturing these foundational experiences. Institutionalizing the mindsets born of adverse conditions can lead to superior global performance.

FIGURE 4

Learning and profiting from adverse institutional environments.