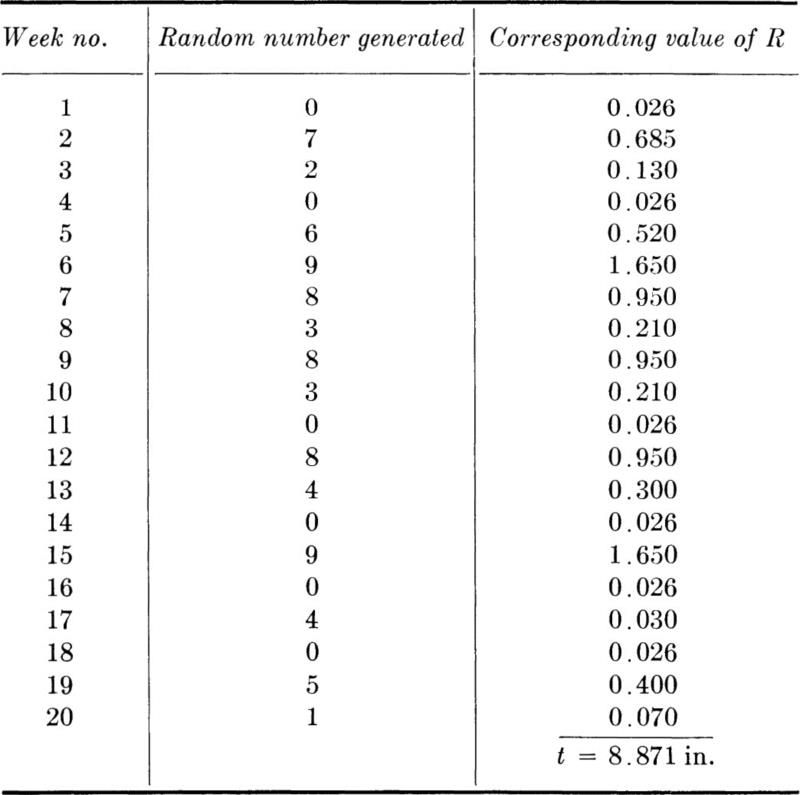

Table 2.3.2 Simulated values of the rainfall in the 20 rainy weeks of 1 year

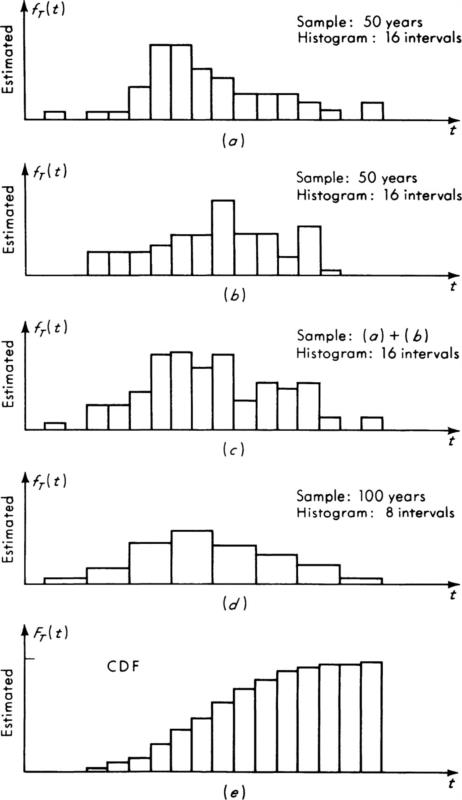

Fig. 2.3.16 Histograms of several simulation runs reduced to estimated density functions and an estimated cumulative distribution function.

It should be evident even from these simple illustrations that many complex engineering problems can be analyzed by Monte Carlo simulation techniques. The models need not be restricted to functional relationships, but can involve complicated situations in which the distributions of variables depend upon the (random) state of the physical system or in which the whole sequence of steps to be followed may depend upon which particular value of a random variable is observed. Elaborate probabilistic models of many vehicles on complicated networks of streets and intersections have proved most useful to traffic engineers trying to predict the performance of a proposed design. The uncertainty and variation in drivel reaction time, driving habits, and origin-destination demands can all be treated on a probabilistic basis. Long histories of the operation of whole river-basin systems of water-resource controls have been simulated in minutes (Hufschmidt and Fiering [1966]). Rainfall and runoff values form probabilistic inputs to chains of dams and channels (real or designed) whose proposed operating policies (e.g., the degree to which reservoirs should be lowered in anticipation of flood runoffs) are being evaluated for long-term consequences, likelihoods of poor performance, and economics. Simulation, combined with numerical integration of the equations of motion, has been used to obtain approximate distributions of the maximum dynamic response of complex, nonlinear structures to the chaotic, random ground motions during earthquakes (Goldberg et al. [1964]).

The successful application of simulation depends upon the appropriateness of the model and the interpretation of the results as much as on the sophistication of the simulation techniques used. The former problems are the ones the engineer usually faces in using mathematical models of natural phenomena; for the latter problems, those of technique, the engineer can find help and documented experience in a number of references. (See, for example, Tocher [1963] or Hammersley and Hands-comb [1964].) Many methods are available, for example, to generate random numbers, to account for dependence among variables, or to reduce the effort needed to get the desired accuracy.

This section presents methods for deriving the distributions of random variables which are functionally dependent upon random variables whose distributions are known. In general, one should seek the CDF of the dependent random variable Z. For any particular value z, FZ(z) is found by calculating in the sample space of X (or X and Y) the probability of all those events where g(x) [or g(x,y)] is less than or equal to z:

![]()

This can be done by enumeration if the distribution of X (or X and Y) is discrete. If the distribution of X is continuous, integration is required. In certain circumstances (monotonic, increasing, one-to-one relationships), this procedure simply reduces to

![]()

The density function of Z can be found by differentiation of FZ(z) (assuming that Z is a continuous random variable). In certain cases the differentiation can be carried out explicitly before particular probability laws FX(x) are considered, in which case one can obtain a formula for the PDF of Z directly. The two most important examples are

1. Under monotonic, one-to-one conditions:

![]()

2. If Z = X + Y :

![]()

Certain computational methods are available for cases where analytical solutions are difficult or impossible. They include

1. Approximating continuous distributions by discrete ones, and solving by enumeration

2. Applying simulation techniques to obtain, by repeated experimentation, observed histograms which approximate desired results.

Because of the very nature of a random variable it is not possible to predict the exact value that it will assume in any particular experiment, but a complete description of its behavior is contained in its probability law, as presented in the CDF (or PMF or PDF, if applicable) of the variable. This complete information can be communicated only by stipulating an entire function, e.g., the PDF. In many situations this much information may not be necessary or available. More concise descriptors, summarizing only the dominant features of the behavior of a random variable, are often sufficient for the engineering purpose at hand. One or more simple numbers are used in place of a whole probability density function. These numbers usually take the form of weighted averages of certain functions of the random variable. The weights used are the PMF or PDF of the variable, and the average is called the expectation of the function.

We will find that, compared with entire probability laws, these expectations are much easier to work with in the analysis of uncertainty, as well as much easier to obtain estimates of from available data. Therefore, in engineering applications, where expedience often dictates that approximate but fast answers are better than none at all, averages and expectations prove invaluable.

Mean Every engineer is familiar with averages of observed numerical data. The sample mean and sample variance (Sec. 1.2) are the most common examples. Although they do not communicate all the available information, they are concise descriptors of the two most significant properties of the batch of observed data, namely, its central value and its scatter or dispersion.

On the other hand, given a solid body, e.g., a rod of nonuniform shape or density, the engineer is accustomed to determining certain numerical descriptions of the body such as the location of its center of mass and a moment of inertia about that point. Not complete in their description, these quantities are nonetheless sufficient to enable the engineer to predict a great deal about the gross static and dynamic behavior of the body.

Both these examples deserve being kept in mind when we define the mean mX or the expected value E[X] of a discrete random variable X as

or, for a continuous random variable, as

In the mean (or mean value) we are condensing the information in the probability distribution function into a single number by summing over all possible values of X the product of the value x and its likelihood pX(x) or fX(x) dx.

Recall from Chap. 1 that the sample mean of n numbers was defined as

If several observations of each value xi are found, this definition can be written

in which r is the total number of distinct values observed, ni is the total number of observations at value xi, and fi = ni/n is the observed frequency of the value xi in the sample.

Notice the close proximity in appearance between the definition of the mean of a (discrete) random variable, Eq. (2.4.1), and the sample mean of a batch of observed numbers, Eq. (2.4.4). This similarity helps make clear the notion of the mean of a random variable (especially when repeated observations of the random variable are anticipated), but the student should be most careful to avoid confusing the two means. The sample mean is computed from given observations, and the mean (or expectation) is computed from the mathematical probability law (e.g., from the PDF, CDF, or PMF) of a random variable. The latter is sometimes called the population mean to distinguish it from the sample mean. Geometrically, it is clear from its definition, Eqs. (2.4.1) or (2.4.2), that the mean defines the center of gravity of the shape defined by the PDF or PMF of a random variable.

In a physical problem, where some phenomenon has been modeled as a random variable, the mean value of that variable is usually the most significant single number the engineer can obtain. It is a measure of the central tendency of the variable, and, often, of the value about which scatter can be expected if repeated observations of the phenomenon are to be made. The sample mean of many such observations will, with high probability, † be very close to the (population) mean of the underlying random variable. For these and other reasons to be seen, when probabilistic model and a deterministic (nonprobabilistic) model of a physical phenomenon are compared, it is usually the mean of the probabilistic model which one compares with the single value of a deterministic model.

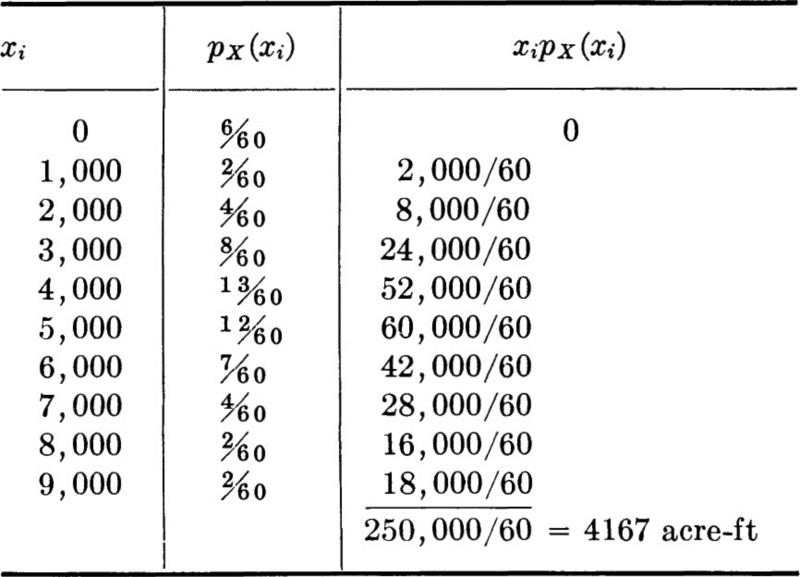

The mean of the discrete random variable adopted in Sec. 2.2.1 to model the annual runoff (see Fig. 2.2.3) is computed as follows, using Eq. (2.4.1):

The mean runoff is 4167 acre-ft. This is a central value, a value about which observed values of X will tend in the long run to be scattered. It is probably the number the engineer would use if he were restricted to using only a single number to describe the runoff, that is, if he had to treat runoff deterministically rather than probabilistically in his analysis.

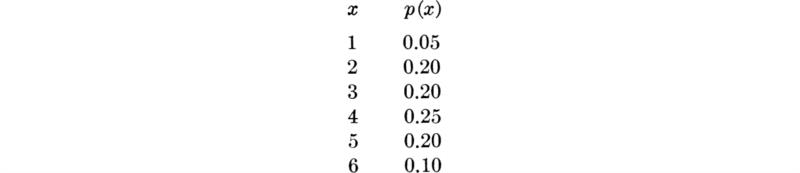

The mean value of the rainfall in a rainy week, the random variable R in the illustration in Sec. 2.3.3, is calculated by integration, after Eq. (2.4.2). Substituting for the PDF the function 2e–2r, r ≥ 0,

If it rains in a week, ½ in. is the mean value or “expected” value of the rainfall. Comparing this value with the density function of R (Fig. 2.3.15), it is apparent that in this case, the mean of R is not central, in that it does not correspond to a peak in the distribution. Nor is the mean the value which will be exceeded half of the time.† (That is, 1 – FR(½ in.) = e–1 = 0.368 ≠ 0.5. Solving 1 – FR(u) = 0.5 yields the median u = 0.346 in.) Nonetheless, even here the mean value yields “order of magnitude” information as to weekly rainfall in rainy weeks, and, if the observed records of many such weeks are averaged, this sample average would almost certainly be very close ‡ to ½ inch (assuming always that the mathematical model is a good representation of the physical phenomenon).

Variance The mean describes the central tendency of a random variable, but it says nothing of that behavior which leads engineers to study probability theory at all, namely, uncertainty or randomness. Here we seek a descriptor, a single number, which will give an indication of the scatter or dispersion, or, loosely, of the “randomness” in the random variable’s behavior.

Several such measures are possible. The range of the random variable is one example, although it is frequently a rather uninformative pair of numbers such as – ∞ to ∞ or 0 to ∞. Even if the range is two finite numbers, say, a to b, it gives no indication of the relative frequency of extreme values as compared with central values. It is desirable therefore to measure the dispersion from a central value, the mean, and to weight all deviations from the mean by their relative likelihoods.

The most common and most useful such measure of the dispersion of a random variable is the variance σX2, or Var [X], It is defined as the weighted average of the squared deviations from the mean:

or

The variance of a random variable bears the same relationship to the sample variance of a set of numbers (Sec. 1.2) as the mean does to the sample mean, and a comparison analogous to that made above between Eqs. (2.4.1) and (2.4.4) could be made with ease. A more meaningful analogy to draw is that between the variance of a random variable and the central moment of inertia of a bar of variable density (and unit mass). The variance σX2 is the second central moment of the area of the PDF or PMF with respect to its center of gravity mX.

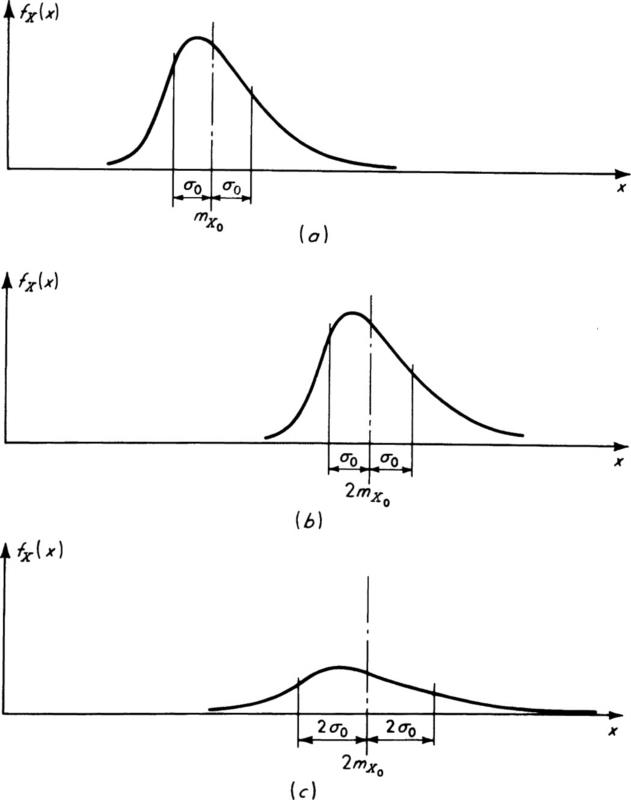

In Fig. 2.4.1 are shown probability density functions of the same basic shape. The curves in Figs. 2.4.1a and b differ only in their mean, while the curves in Figs. 2.4.1b and c differ only in their variances. Smaller variances generally imply “tighter” distributions, less widely spread about the mean.

Standard deviation The positive square root of the variance is given the name standard deviation:

The conventional form of the standard notation, σ and σ 2, seems to indicate that in practice the standard deviation is given more importance than the variance. That is, in fact, the case.† The standard deviation has the same units as the variable X itself and can be compared easily and quickly with the mean of the variable to gain some feeling for the degree and gravity of the uncertainty associated with the random variable.

Fig. 2.4.1 Changes in PDF’s with changes in means and standard deviations.

Coefficient of variation A unitless characteristic that formalizes this comparison and that also facilitates comparisons among a number of random variables of different units is the coefficient of variation VX:

The coefficient of variation of the strength of the concrete produced by a given contractor is often assumed to be a constant for all mean strengths and to be a measure of the quality control practiced in his work (see ACI [1965] and Prob. 2.45). Thus a contractor practicing “good” control might produce concrete with a coefficient of variation of 0.10 or 10 percent, implying that concrete of mean strength 4000 psi would have a standard deviation of 400 psi, whereas “5000-psi concrete” would have a standard deviation of 500 psi.

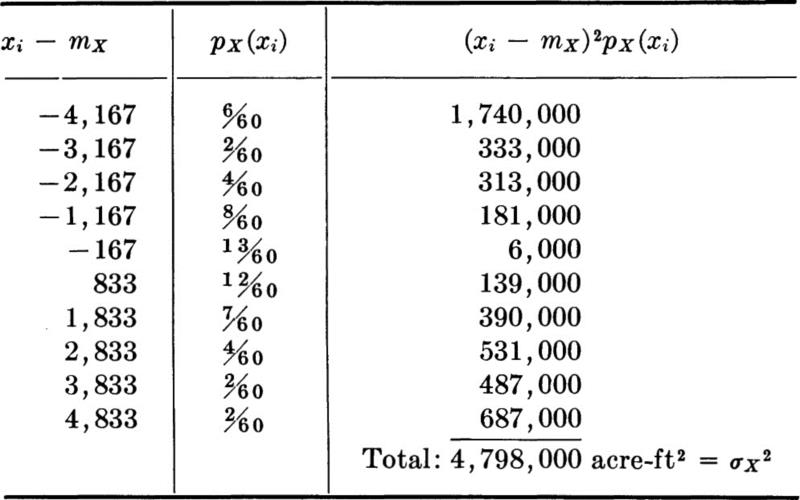

The variance of the discrete runoff random variable can be computed from Eq. (2.4.7) as follows:

The standard deviation of this variable is

![]()

and the coefficient of variation is

![]()

The variance of the rainfall variable R is found by applying Eq. (2.4.8):

while

![]()

and

![]()

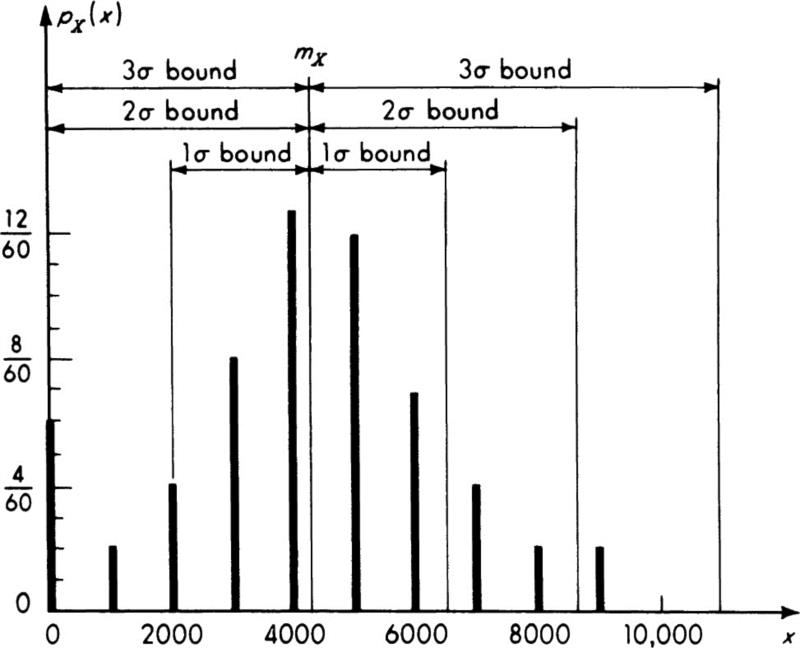

Illustration: Sigma bounds and the Chebyshev inequality It is common in engineering applications of probability theory to speak of the “one-, two-, and three-sigma” bounds of a random variable. The range between the two-sigma bounds, for example, is the range between mX – 2σX and mX + 2σX. The two-sigma bounds on the runoff variable X are 4167 – 2(2200) and 4167 + 2(2200) or 0 and 8567.† The three sets of bounds for this variable are shown in Fig. 2.4.2.

Fig. 2.4.2 Sigma bounds: runoff model.

In absence of the knowledge of the complete PDF, but knowing mean and variance, it is frequently stated in engineering applications (for reasons that will be clear in Sec. 3.3.1) that the probability that a variable lies within the one-sigma bounds of its mean is approximately 65 percent; within the two-sigma bounds, about 95 percent; and within the three-sigma bounds, about 99.5 percent. That even rough probability figures can be given with so little information is indicative of the value of the standard deviation and the variance as measures of dispersion. In fact, these approximate statements should only be used when it is known that the distribution is roughly bell-shaped.

More formally we can show that the mean and standard deviation alone are sufficient to make certain exact statements on the probability of a random variable lying within given bounds. The Chebyshev inequality ‡ states that

Note that, corresponding to the one-, two-, and three-sigma bounds, h equals 1, 2, and 3.

For example, the runoff variable has mean 4167 and standard deviation 2200. The Chebyshev inequality states

![]()

If h = 2

![]()

Or, recognizing in this particular case that X, the runoff, is nonnegative,

![]()

or, in another form,

![]()

The rule of thumb for the two-sigma bounds suggests that the former probability, that is, P[X ≤ 8567], should be about 95 percent, while the exact value, Fig. 2.4.2, is ![]() .

.

The Chebyshev inequality does not yield very sharp bounds. [Consider, for example, any value of h less than 1, when the right-hand side of Eq. (2.4.11) is negative.] It has the advantage, however, that it requires no assumption on the part of the engineer regarding the shape of the distribution. Hence the probability statements are totally conservative, within the qualification, of course, that mX and σX are known with certainty. When these parameters’ estimates are based on only a small amount of observed data, they, in fact, are not known with high confidence; this uncertainty is a subject of Chaps. 4 and 6.

A host of less general, but more precise inequalities are available. (See, for example, Parzen [1960], Freeman [1963].) As the engineer makes more and more assumptions regarding the shape of the distribution, such as its being unimodal (single-peaked), having “high-order contact” with the x axis in the extreme tails, † being symmetrical, having known values of higher moments (see Sec. 2.4.2), etc., the sharper his probability statements can be. Finally, of course, if he is willing to stipulate FX(x) itself, he can state exactly the proportion of the probability mass lying inside or outside any interval. This progression is common in applied probability theory; the more the engineer is willing to assume to be known, given, or hypothesized information, the more precise and penetrating can he be in his subsequent probabilistic analysis.

Discussion It should be emphasized that from the point of view of applications, two quite opposite problems have been discussed in this section. The first is that of calculating the mean and variance of a random variable knowing its distribution, and the second is that of making some kind of statement about the behavior of the variable when only the mean and variance are known.

The latter case is frequent. It arises in many situations. Data is often available only as summarized by its sample mean and sample variance, which are the natural estimates of the corresponding two model parameters. Also, in the analysis of complex models, the mean and variance of the dependent random variable are often easily obtainable when the complete story, i.e., the whole distribution, is lost in a maze of intractable integrals (Sec. 2.3). As will be discussed later in this section, we can often determine these two parameters as simple functions of the same two parameters of the independent random variables involved, implying that the engineer may never need to commit himself to unnecessarily detailed models of these variables. As shown in the next section, the mean and variance alone contain a substantial amount of information on which to base engineering decisions. Finally, they represent the first and most important step beyond deterministic engineering models in that they characterize not only the typical value, as the traditional model does, but also the dispersion. Recognition of the existence of the variance indicates that the probabilistic aspects of the engineering problem won’t be ignored. Study of the mean and variance, and their later counterparts, is referred to as a second-order-moment analysis; there will be an emphasis on this notion throughout our study of applied probability and statistics.

Summary In Sec. 2.4.1 we have defined the mean, variance, standard deviation, and coefficient of variation of a random variable. They are defined as sums of the possible values of the random variable or as sums of the squared deviations from the mean, weighted by their probabilities of occurrence. The mean and variance are the center of gravity of the probability mass and its moment of inertia. They can be calculated from given probability distributions, or used alone, without knowledge of the entire distribution, as summaries of the predominant characteristics of central value and dispersion.

In Sec. 2.3 we emphasized the importance in engineering applications of being able to determine the behavior of a (dependent) random variable Y, which is a function g(X) of another (independent) random variable X, whose behavior is known. The computational difficulties involved in actually finding, say, the PDF of Y from the PDF of X have also been encountered. Fortunately, as mentioned above in the justification for a concentrated study of the mean and variance, no such computational complications arise if one seeks only these two moments of Y, given the probability law of the independent variable X. Often even less is needed; for example, often only the mean and variance of X can be used to find corresponding moments of Y.

Expectation of a function If we know the probability law of X and our interest is in Y, where

![]()

then the expected value or expectation of Y is, by definition [Eq. (2.4.2)],

The method for computing fY (y) and its attendant difficulties were the subject of Sec. 2.3. It is a fundamental, but difficult to prove, † result of probability theory that this expectation can be evaluated by the much easier computation‡

where the notation E[g(X)] is defined as:

For a discrete variable, § the expectation of g(X) is defined as

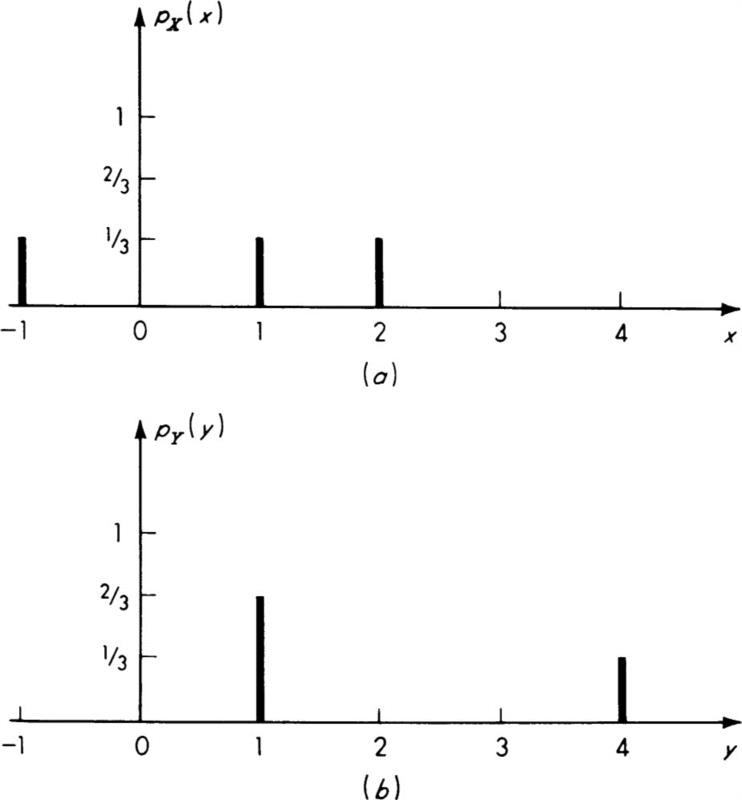

It is helpful to see a simple discrete illustration. Suppose a random variable X has PMF as shown in Fig. 2.4.3a. Then the PMF of Y = g(X) = X2 is as shown in Fig. 2.4.3b. This result can be verified by straightforward enumeration in this simple example. The expected value of Y is, by definition, E[Y] = (⅔)(1) + (⅓)(4) = 2. Equation (2.4.14) states, however, that this expected value can also be found without first determining PY(y) Using Eq. (2.4.14),

![]()

as before.

Notice that the two quantities defined in Sec. 2.4.1, the mean and variance, can in fact be interpreted as merely special cases of Eq. (2.4.14) with g(X) = X for the mean and g(X) = (X – mX)2 for the variance. This equivalence suggests that two quite different interpretations might be given to Eq. (2.4.14). In some situations one may think of E[g(X)] as representing the mean of a random variable Y = g(X) conveniently calculated by this equation rather than by Eq. (2.4.12). This interpretation is common when interest centers on Y = g(X) as a dependent random variable functionally related to another random variable X (with known distribution function), as, for example, when X is velocity and Y = aX2 is kinetic energy. On the other hand, if interest centers on X itself, then the expectation of g(X) as given by Eq. (2.4.14) is usually interpreted as weighted average of g(X), over X, that is, as the sum of the values of the function of X evaluated at the various possible values of X and weighted by the likelihoods of those values of X. The variance of X, for example, is usually thought of in this light, rather than as the mean of a random variable Y = (X – mX)2. The distinction between these two interpretations is not of fundamental importance, but it may prove helpful when considering the uses to which the material to follow will be put.

Fig. 2.4.3 PMF’s of X and derived Y = X2 (a) Discrete PMF of X; (b) discrete PMF of Y = X2.

Moments In keeping with the latter interpretation of E[g(X)] as a weighting of g(x) by fX(x), we introduce a family of averages of X, called moments, that prove useful as numerical descriptors of the behavior of X. We call

the nth moment of X. Notice that this moment corresponds to the nth moment of the area of the PDF with respect to the origin. If n = 1, when the superscript is usually omitted, we have the mean of the variable.

It is possible, of course, to consider moments of areas about any point. In particular, moments with respect to the mean are called central moments:

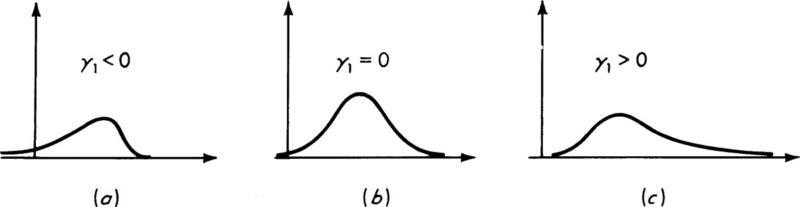

Such moments correspond to the familiar moments of areas with respect to their centroids. The most important particular case is for n = 2, when ![]() the variance. The first central moment is, of course, always zero. If the asymmetry of a distribution is of interest, this property is often quantified or characterized by the third central moment μX(3), or by the corresponding dimensionless coefficient of skewness γ1:

the variance. The first central moment is, of course, always zero. If the asymmetry of a distribution is of interest, this property is often quantified or characterized by the third central moment μX(3), or by the corresponding dimensionless coefficient of skewness γ1:

If a distribution is symmetrical, this coefficient is zero (although the converse is not necessarily true). Positive values of γ1 usually correspond to PDF’s with dominant tails on the right; negative values to long tails on the left (see Fig. 2.4.4).

A less common coefficient γ2, the coefficient of kurtosis (flatness), is defined similarly:

It is often compared to a “standard value” of 3.†

Fig. 2.4.4 Variation of shape of PDF with coefficient of skewness γ1. (a) Negative skewness; (b) zero skewness; (c) positive skewness.

For example, the central moments of the rainfall variable R, defined in Sec. 2.3.3, are, in general,

In the previous section, it was found that

![]()

Also

![]()

and

![]()

Hence the skewness and kurtosis coefficients are

![]()

indicating a positive skewness or long right-hand tail (see Fig. 2.3.15), and

![]()

Properties of expectation No matter which interpretation of the expectation E[g(X)] is involved, several general properties of the operation can be pointed out. For example, the expectation of a constant c is just the constant itself. This fact is easily shown. Simply by writing out the definition, we have

Similarly the following properties can be verified with ease for constants a, b, and c:

The implication of this last equation is that expectation, like differentiation or integration, is a linear operation. This linearity property is very useful computationally. It can be used, for example, to find the following formula for the variance of a random variable in terms of more easily calculated quantities.

![]()

Expanding the square,

![]()

Each term in the sum can be treated separately as a function of X and, according to Eq. (2.4.23), the expectation of their sum is the sum of their expectations:

![]()

Using other properties of expectation [Eqs. (2.4.20) and (2.4.21)],

![]()

But E[X] = mX; therefore

In an alternate form, the variance is said to be the “mean square” minus the “squared mean”:

Given the PDF of X, the simplest way to evaluate the variance is usually to calculate ![]() that is, E[X2], and then to subtract the squared mean.

that is, E[X2], and then to subtract the squared mean.

Note that this last derivation took place without any reference to a particular form of the PDF and even without indication as to whether a discrete or continuous variable was involved. It is this ability to work with expectation without specifying the PDF that often permits us to determine relationships among the moments of two functionally related variables, X and Y = g(X), before specifying or even without knowledge of the PDF of X. For example, in concrete the quadratic relationship

holds between compressive stress Y and unit strain X well beyond the linear elastic range (Hognestad [1951]). If the unit strain applied to a specimen by a testing machine is a random variable, owing, say, to uncertainties in recording, then so is the stress in the concrete. How might the expected or mean stress be determined? If the PDF of X is known, the mean stress mY could be found by using the methods of Sec. 2.3 to find fY(y), and then applying Eq. (2.4.2). Alternatively, E[Y] could be calculated using Eq. 2.4.14, since

But, if the mean and variance of the strain are available, even if the PDF is not, the mean of Y can be found much more directly as simply

![]()

Using Eq. (2.4.24),

![]()

Therefore

Thus the mean and variance of X are sufficient to determine the mean of Y. An important practical distinction between deterministic and probabilistic analysis is also illustrated by this example. In a deterministic formulation of this problem, one would assume only a single value of strain was possible, say the typical value mX. The predicted stress would then be bmX – cmX2, which does not coincide with the mean value of F, unless, of course, the dispersion in X is truly zero. The greater the uncertainty in the strain, the greater the systematic error in the predicted value of the stress.

Formalizing this observation: in general, we cannot find the expectation of a function of X by substituting in the function E[X] for X, or

For example, the mean of 1/X is not 1/mX.

The linearity property of expectation, which made the previous derivations so direct, does not carry over to variances. The variance of Y = 2X is not two times the variance of X. This fact is easily demonstrated:

Several useful general properties of variances can be stated (and easily verified) however:

That is, a constant has no variance, and the standard deviation of a linear function of X, a + bX, is just |b|σX A simple example of such a linear function is a problem in which there is a change of units.

Conditional expectation In Sec. 2.2 we discussed briefly the construction of conditional distributions which are formed conditionally on the occurrence of some event. For example, in a design situation we might be interested in the distribution of the demand or load X, given that it is larger than some threshold value x0, say, the nominal design demand. Then, by definition of conditional probabilities,

The conditional PDF is found by differentiation with respect to x:

![]()

The conditional distributions satisfy all the necessary conditions to be proper probability distributions, and may be used as such.

It is therefore also meaningful to consider conditional means, conditional variances, and in general any expectation that is conditional on the prescribed event. So the conditional mean of the demand X, given that it is larger than the nominal demand x0, is

and its conditional variance is defined as

In general, for some event A,

Note that there is a trivial case:

A numerical example of the use of conditional distributions and expectations in engineering design will be found in an illustration to follow.

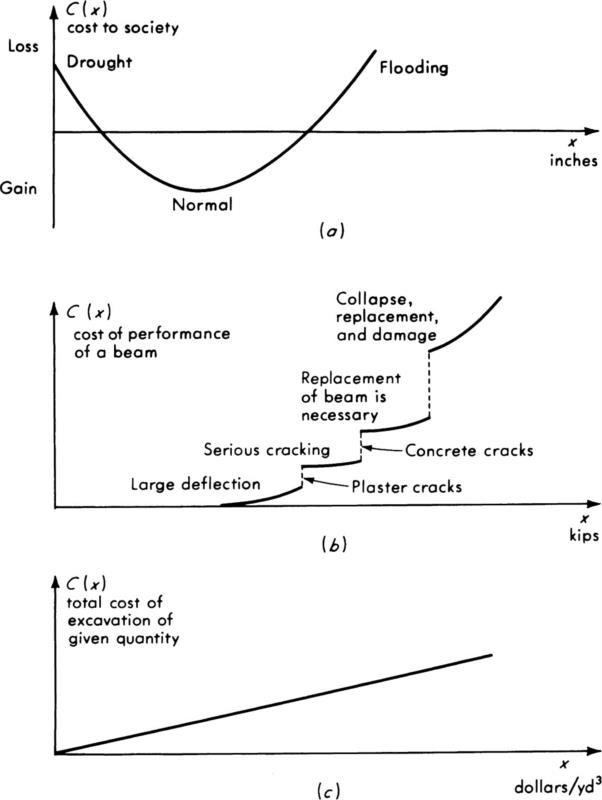

Expected costs and benefits A common use of expectation of a function of a random variable arises from the practice of basing engineering decisions, in situations involving risk, on expected costs. Frequently a portion of the total cost of a proposed design depends upon the more or less uncertain future magnitudes of such phenomena as local rainfall, traffic volume, or unit bid prices. If the engineer describes the uncertainty associated with these variables by treating them as random variables, then, when comparing alternate designs, the question arises of how to combine those portions of the costs or benefits that depend upon these random variables with the other, nonrandom, components of cost. How do you compare a more expensive spillway design with one of smaller initial cost, but of smaller capacity, and hence of greater risk of inadequacy during peak flows?

As demonstrated in previous illustrations (e.g., the industrial park example in Sec. 2.1), the expected cost (or benefit) related to the variable is usually used to obtain a single number; this cost reflects the sum of all possible values of the random cost weighted by the likelihood of their occurrence. The use of expected cost in making decisions is the subject of much experimental as well as theoretical investigation (Fish-burn [1965]), and it will be discussed more fully in Chap. 5. For the time being it can be accepted as an intuitively rational description of the economic consequences associated with the random variable.

In general, every value of the random variable leads to a corresponding cost or benefit. In other words, we can define cost as a function of the variable:

Examples of the shapes of such cost functions are sketched in Fig. 2.4.5.

In many cases the cost function is at least approximately linear. The cost of evacuating 100,000 yd3 of earth, for instance, depends linearly on X, the price bid per cubic yard, Fig. 2.4.5c. Then C(X) is of the form (in Fig. 2.4.5c the constant a is zero)

and the expected cost

That is, in this case the expected cost depends only on the mean of the random variable.

Fig. 2.4.5 Some cost functions, (a) Annual rainfall; (b) maximum load on a concrete beam; (c) unit bid price.

In other situations the cost can be approximated by a quadratic relationship. Figure 2.4.5a is a possible example. In this case the expected cost depends only on the mean and variance of the random variable:

The importance of the first- and second-order moments, i.e., means and variances, of random variables is magnified when it is recognized that frequently the ultimate engineering use of the probabilistic model will be in a decision-making context where a linear or quadratic cost function is a valid approximation. In such cases, the mean and variance are sufficient information on which to base the decision if an expected cost criterion is used.

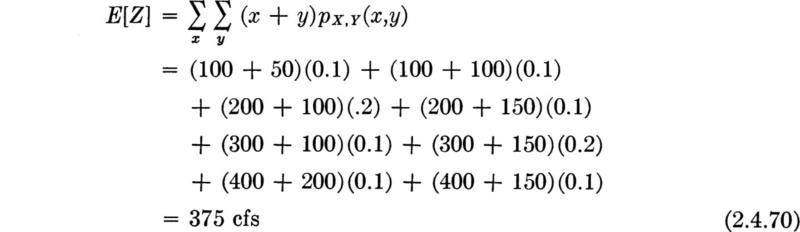

Illustration: Pump-capacity decision This extended illustration is designed to demonstrate a number of the concepts discussed to this point in the text and to serve as a discussion of others. In particular, a mixed random variable will be encountered, a result here of a function g(X) which takes on the same value for many different values of X.

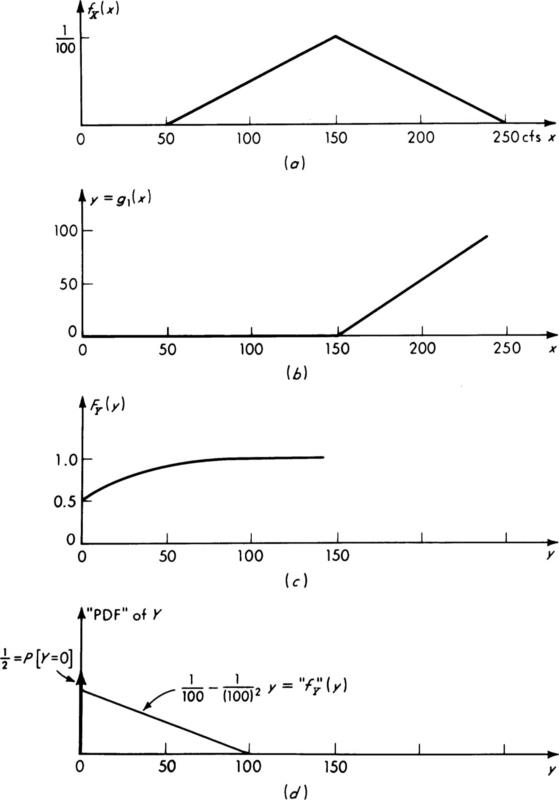

The demand X during the peak summer hour at a water-pumping station has a triangular distribution given by

and sketched in Fig. 2.4.6a.

The existing pump is adequate for any demand from 0 to 150 cfs. A new pump is to be added; it will be operated only if demand exceeds the capacity of the existing pump. Hence a demand of up to 150 cfs involves no load on the new pump, while a demand of 250 cfs would impose a load of 100 cfs on the new pump. Let Y be a random variable, “the load on the new pump” (i.e., the excess of demand over existing capacity):

This function is shown in Fig. 2.4.6b. It is not a one-to-one function.

Let us review how the distribution of Y can be determined. After Eq. (2.3.16), we have

![]()

where Ry is the region in which Y = g(X) ≤ y. Y is clearly never negative, but it is zero when X is less than 150; thus

![]()

By the symmetry of fX(x) about 150,

![]()

Fig. 2.4.6 Pump-design illustration, (a) Water-demand distribution; (b) load on new pump versus demand; (c) CDF of load on new pump; (d) PDF of load on new pump.

Y is never greater than 250 – 150, or 100, but the probability that Y is less than any value in the range 0 to 100, say, 30, is the probability that X is less than 30 + 150 = 180, or, in general, for 0 ≤ y ≤ 100,

![]()

Substituting for fX(x) in the range x = 150 to 250,since FX(150) = ½,

This function is, of course, unity for y > 100 and zero for y < 0, as shown in Fig. 2.4.6c.

The distribution of Y is of the mixed type; that is, there is a finite probability, ½, that Y will be exactly equal to zero, but elsewhere it behaves as a continuous random variable. Strictly, it has neither a PMF nor a PDF,† but a graphical representation of the latter is possible, as shown in Fig. 2.4.6d. The spike at zero represents the finite probability of that value occurring. The area under the “continuous part,” which we will denote as “fY”(y), is, of course, only ½, not unity. This continuous part is given by

It is helpful to recognize that any mixed distribution of practical interest can be represented as the weighted sum of two proper distributions, one discrete and one continuous:

in which 0 ≤ p ≤ 1 and in which ![]() is associated with the discrete values which Y can take on and

is associated with the discrete values which Y can take on and ![]() is associated with the continuous range. In the example here, p = ½,

is associated with the continuous range. In the example here, p = ½,

![]()

and

The function denoted “fY(y)” in Eq. (2.4.43) is just ![]() . The treatment of mixed distributions does not deserve special discussion in this applied text, not because they are not useful, but because their treatment follows in an obvious manner from that of discrete and continuous variables.

. The treatment of mixed distributions does not deserve special discussion in this applied text, not because they are not useful, but because their treatment follows in an obvious manner from that of discrete and continuous variables.

Consider now the task of choosing a capacity for the new pump. A “conservative” design would be 100 cfs, the maximum value the pump could possibly be called on to provide. But the occurrence of large values of demand are rare, and so alternate design rules might prove more economical in balance. One such rule might be to match the new pump’s capacity to the expected demand upon the pump, that is, E[Y].

This value can be obtained using the definition of expectation. Here an obvious extension of both Eqs. (2.4.1) and (2.4.2) is needed to provide for the mixed distribution of Y:

Alternatively, if this expected value were the only objective, we could have obtained it directly using Eq. (2.4.14) without the necessity of finding the probability law of Y. In this case

![]()

Substituting first for g1(x) [Eq. (2.4.41)],

![]()

and then for fX(x),

This rule suggests a second pump of capacity 16.7 cfs.

An alternate design rule might call for a pump capacity equal to the average of the nonzero demands on the pump, i.e., the expected demand given that the pump must be turned on at all. Formally, this value is the expected value of Y given that Y is greater than zero. The conditional distribution of Y given that Y is strictly greater than zero is, in this case, just the continuous part of its probability law renormalized to unit area or

Hence, the expected value of Y given Y > 0, written E[Y | Y > 0], is

This design rule suggests a pump twice as large as the first rule.

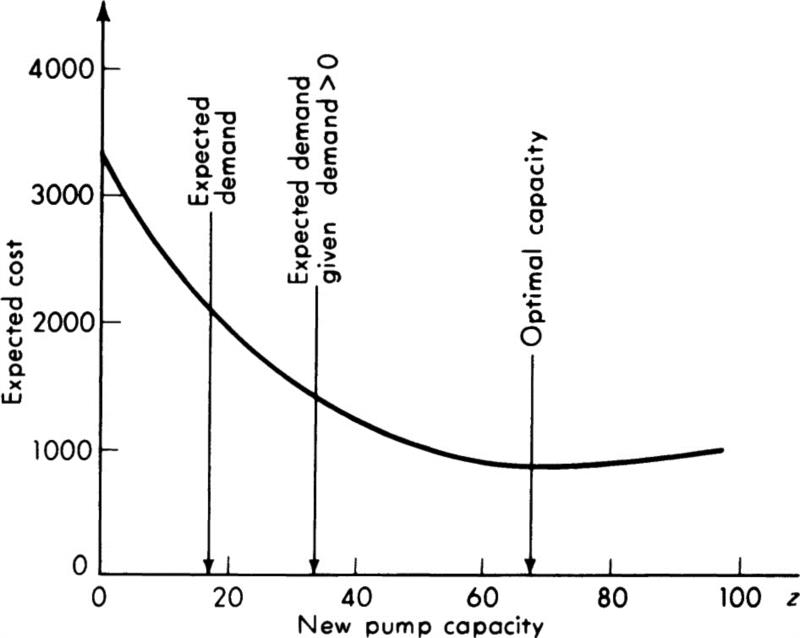

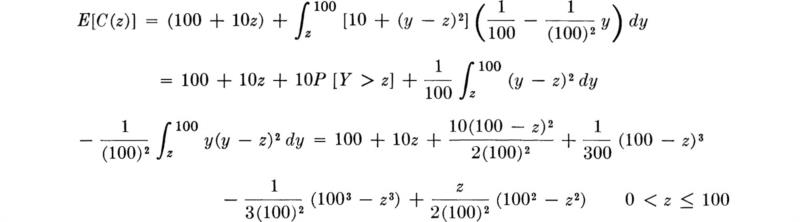

As a less arbitrary and more explicitly cost-oriented approach, the engineer might seek that pump capacity z which promises the lowest expected total cost. Costs (in arbitrary units) are thought to be described by a cost of 100 + 10z (representing a fixed installation cost and the cost of the pump itself) plus a cost associated with failing to meet the peak demand. Determination of this latter factor is complicated by the possibility of large, but off-peak, demands at other times in the same year and by the fact that the system will be in place over a number of years. The engineer might summarize these effects, however, by saying that they are represented in a cost of failing to meet the peak demand in any one arbitrary year given by 10 + (Y – z)2, if Y – z, the amount by which the pump of capacity z fails to meet a random demand of Y, is positive, and zero otherwise. Formally, for a given z > 0, the cost as a function of the random variable Y is

When z = 0, there is no initial cost—only the cost of failing to meet the demand.

For a pump of capacity 0 < z < 100, then, the expected value of the total cost C(z) can be found by using either the probability law of Y with Eq. (2.4.14) [and (2.4.15)] or the probability law of X with Eq. (2.4.31). The former path is taken here:†

The minimum cost must occur either (1) when no pump is installed, z = 0,

![]()

or (2) when the largest peak is matched, z = 100,

![]()

or (3) at some intermediate value found by differentiating the expression above, setting it equal to zero, and solving for the optimal value z0,

Solving,

![]()

The root of interest is

![]()

The expected cost at z = 67.5 cfs is about 883 units. (Therefore the extremum found is, in fact, a minimum and not a maximum.) Because this cost is less than the expected cost (3305) associated with the “do-nothing” (z = 0) policy, and less than the expected cost (1100) of the most conservative (z = 100) policy, the best design is to provide a pump with a capacity of 67.5 cfs.

Fig. 2.4.7 Expected cost versus pump capacity.

The other two design rules, suggesting capacities of 16.7 and 33.3 cfs, have, of course, expected costs larger than the optimum value. (In particular, the expected cost of a z = 33.3 cfs capacity decision is 1402 units.) The function E[C(z)] is plotted in Fig. 2.4.7. In words, such small-capacity designs, although cheaper initially, run a large risk of a very high penalty due to insufficient capacity. The high initial cost of a very large pump (say, 100 cfs) is apparently not justified in the light of the small likelihood of its full capacity being needed. The indicated optimum design achieves a balance between these two factors.

When two or more random variables must be dealt with simultaneously, their behavior is described by their joint probability distribution (Sec. 2.2.2). The notions of expectation are also extended easily to this situation. Owing to the difficulty in practice of dealing with entire joint distributions, analysis of the joint behavior of random variables is often restricted to their moments. Therefore this subject will be discussed in some detail.

Expectation of a function Generalizing Eqs. (2.4.13) and (2.4.14), we obtain the expectation of a function Z = g(X, Y) of two jointly distributed random variables as

if X and Y are continuous random variables, and

if they are discrete. As in the previous section it is possible but difficult to show that E[Z] calculated from the appropriate equation above is identical to that which would be obtained if, by the technique of Sec. 2.3.2, the distribution fZ(z) were first derived from that of X and Y and then the mean of Z were obtained by Eq. (2.4.2).

As before, we can distinguish between two interpretations of expectation. One looks upon E[g(X,Y)] as the average of a function of X and Y over all values x and y, weighted everywhere by the probability that X = x and Y = y. Moments fall into this category. The second interpretation sees E[g(X,Y)] as the expected value or mean of a random variable Z = g(X,Y).

Moments We have already seen that moments, examples of the “averaged function of X and Y” interpretation of E[g(X,Y)], facilitate the study of the marginal behavior of individual random variables. We shall find them of even greater value in studying the joint behavior of two random variables. Consider the function of X and Y of this form:

![]()

Then its expectation

is called a moment of order l + n of the random variables X and Y. The most important are the two first-order moments: (l = 1, n = 0) and (l = 0, n = 1). In the former case, g(X,Y) = X, and

Here we have simply the mean or expected value of X. Notice that this may be written as

The second integral is simply the marginal distribution fX(x) [Eq. (2.2.43)]; thus

which is the same definition given in Eq. (2.4.2). Thus the expected value of X, Eq. (2.4.53), is the average value of X “without regard for the value of Y.” The definition and meaning of E[Y] are, of course, similar.

It may be helpful for the civil engineer to observe that mX and mY locate the center of mass of a two-dimensional plate of variable density or the horizontal coordinates of the center of mass of the “hill” or terrain whose surface elevations are given by fX,Y(x,y). This follows from the definition of these terms and the fact that the volume under fX,Y(x,y) is unity.

By the same analogy, the second-order moments (l = 2, n = 0), (l = 0, n = 2), and (l = 1, n = 1) correspond respectively to the moment of inertia about the x axis, the moment of inertia about the y axis, and the product moment of inertia with respect to these axes.

Central moments As for a single variable, and as in mechanics, the more useful second (and higher) moments are those with respect to axes passing through the center of mass. Taking g(X,Y) equal to

![]()

we find

which is called a central moment of order l + n of the random variables X and Y. The first central moments are, of course, both zero.

The most valuable central moments are the set of second-order moments: (l = 2, n = 0), (l = 0, n = 2), and (l=1, n = 1). The first two cases, as above with the means, reduce to the marginal variances. With (l = 2, n = 0), for example,

The result for Y, (l = 0, n = 2), is similar.

Covariance The new type of second central moment that is found when joint random variables are considered is that involving their product, that is, (l = 1, n = 1). This moment also has a name, the covariance of X and Y: Cov [X,Y] or† σX,Y.

If the variances correspond to the moments of inertia about axes in the x and y direction passing through the centroid of a thin plate of variable density, then the covariance corresponds to its product moment of inertia with respect to these axes.

Correlation coefficient A normalized version of the covariance, called the correlation coefficient ρX,Y,, is found by dividing the covariance of X and Y by the product of their standard deviations:

It can be shown that this coefficient has the interesting property that

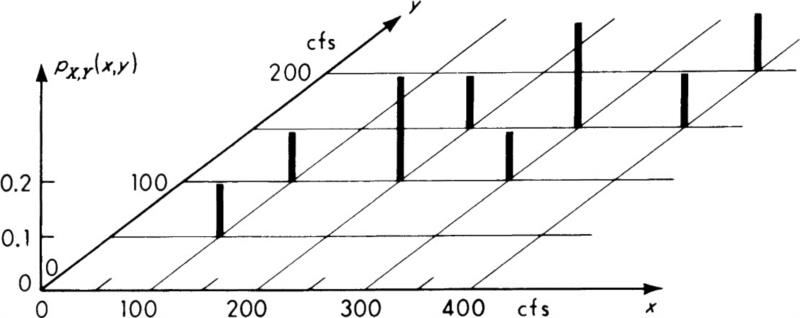

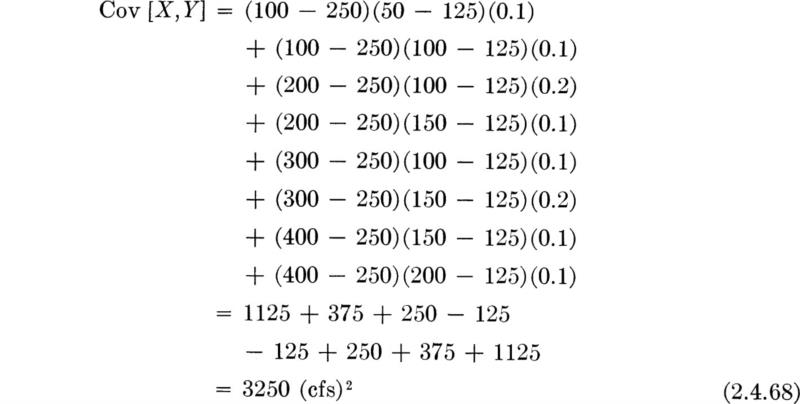

Before discussing the interpretations of the covariance and the correlation coefficient (and its bounds, ±1), let us illustrate the computation of these numbers in a simple discrete case. Consider the discrete joint distribution of X and Y sketched in Fig. 2.4.8, where the distribution might represent a discrete model of the maximum annual flows at gauge points in two different, but neighboring, streams. The engineer’s interest in their joint behavior might arise from his concern over flooding of the river which the streams feed or from his desire to estimate flow in one stream by measuring only the flow in the other.

Fig. 2.4.8 Joint PMF of stream flows.

The means and variances are found from the marginal PMF’s, or as follows:

Similarly

The covariance is found using the discrete analog of Eq. (2.4.58) or

which here becomes

The correlation coefficient pX,Y is

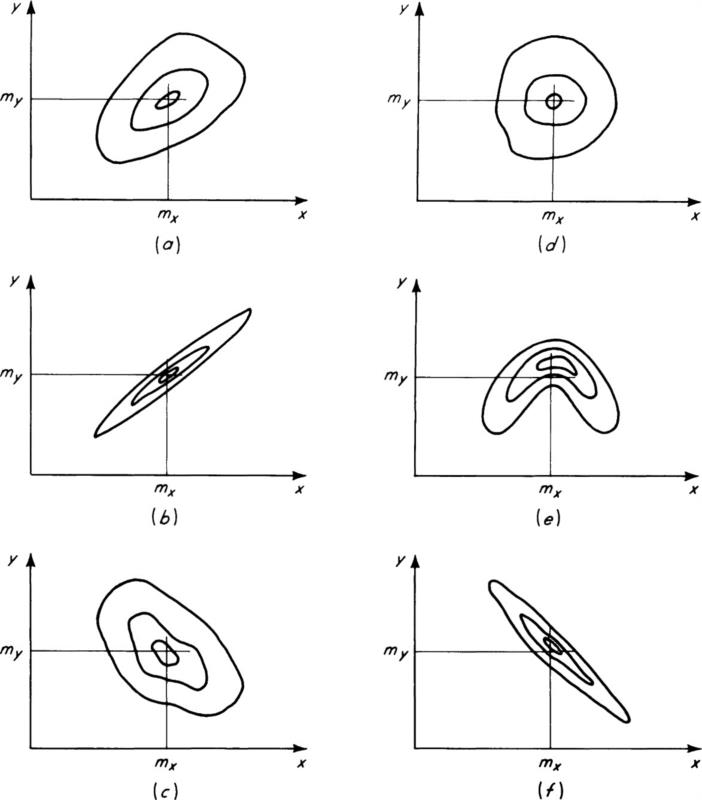

Fig. 2.4.9 Joint density-function contours of correlated random variables. (a) Positive correlation ρ > 0; (b) high positive correlation ρ ≈ 1; (c) negative correlation ρ < 0; (d) (e) low correlation ρ ≈ 0; (f) large negative correlation ρ ≈ – 1.

Discussion: Correlation In Fig. 2.4.9 some joint density functions are sketched and the corresponding values of the correlation coefficients are indicated. Note that the marginal distributions of X and Y remain the same from case to case. Comparing these figures with Fig. 2.2.13, it is clear that large values of ρ imply peaked conditional distributions, such as fY|X; the reverse is not necessarily true (e.g., case e). The implication is that if ρ is large, an observation of X will be very useful in refining and in reducing the uncertainty in predicting Y. Prediction will be discussed more thoroughly later (see page 175).

Examples of phenomena with large positive correlation coefficients (positively correlated random variables) include the length and weight of vehicles, and the yield strength and hardness of steels. Negatively correlated random variables include the speed and weight of vehicles, the ultimate compressive stress and ultimate compressive strain of concrete, and the capacity remaining in a dam and rainfall on its watershed for the past month. Random phenomena displaying small or zero correlation coefficients (uncorrelated random variables) are successive annual maximum floods at a site or the dead and live load on a structure.

Like the mean and variance, the correlation coefficient is often available when the complete probability law is not. This situation may result from the intractability of complete distribution calculations (Sec. 2.3), or from the lack of complete information about the variables. Rather than a well-defined joint probability law, we may have reliable estimates of only the first- and second-order moments. In this case, for example, pairs of observations from two variables may have yielded a scattering of points and an estimate of their correlation coefficient. For the proper interpretation of this number, it is important to know what it says and does not say about the joint behavior of the two variables.

First, from inspection of its definition [Eqs. (2.4.58) or (2.4.67)], the covariance (and hence the correlation coefficient) will be positive if larger than mean values of X are likely to be paired with larger than mean values of Y (and smaller with smaller). In this case the product (x – mX)(y – mY) will be positive where fX,Y(x,y) or pX,Y(x,y) is significantly large. If larger than average values of X usually appear with smaller than average values of Y (and vice versa), the covariance and correlation coefficient will be negative. In either case it can be said that at least some linkage or (stochastic) dependence exists between X and Y. This dependence may not be causal; in metals, greater hardness does not cause greater yield stresses, but the high correlation between the two characteristics is useful. It means that nondestructive hardness tests can be used to predict the strength of a piece of metal with a certain, but imperfect, reliability.

Secondly, if the two variables are independent, their covariance and correlation coefficient are zero. To verify this statement consider Eq. (2.4.58). Independence implies that fX,Y(x,y) factors into fX(x)fY(y); the integral becomes simply the product E[X – mX]E[Y – mY], both factors of which are zero. In words, if the variables are unrelated, their correlation coefficient is zero.

Unfortunately, in practice the error is often made of adopting the converse to this last statement; the third and most neglected fact about the correlation coefficient is that a small value does not imply that the X and Y are independent. Stochastic dependence (as reflected, say, by the sharpening of conditional distributions relative to marginals, Sec. 2.2.2) may be high even if ρ is zero or near zero.

More specifically, the correlation coefficient is a measure of the linear dependence between two random variables, in the following sense. An extreme value of ρ (±1) obtains if and only if there is a linear functional relationship† between X and Y, that is, if and only if Y = a + bX. Hence, if ρ is one in absolute value, an observation of X, for example, will permit a perfect prediction of Y; that is, the stochastic dependence is “perfect”—the conditional distribution of Y given X = x is simply a unit spike at y = a + bx. However, as will be demonstrated in an illustration to come, such perfect (or functional) dependence may exist, but, being nonlinear (for example, Y = aX2) may yield a small correlation coefficient. Less than functional dependence but a close (nonlinear) relationship such as indicated in Fig. 2.4.9e, can also yield a small or zero correlation coefficient. Stochastic dependence in such a case is clearly large; given a value of X = x, the conditional distribution of Y will greatly differ from its marginal distribution. But if one mistakenly concludes a lack of strong stochastic dependence from a small value of the correlation coefficient, he will not reach the proper conclusion in such cases.

In summary, given only the value of the correlation coefficient, one can conclude from a high value that the stochastic dependence is high and furthermore that X and Y have a joint linear tendency, whereas a small value implies only the weakness of a linear trend and not necessarily a weakness in stochastic dependence.

The definitions of moments may be generalized in a straightforward manner to more than two jointly distributed random variables, but the use of higher than second-order moments is seldom encountered in practice. Further discussion of moments will be postponed until they are needed.

Properties of expectation As suggested, Eq. (2.4.50) provides a more efficient way of computing the expected value of a random variable, Z = g(X,Y), than that of first finding its probability law and then finding its expectation. That is, if, in the discrete example of stream flows above, the mean of the total at the maximum flows ‡ Z = X +Y, is desired, it could be found by finding pZ (z) and then averaging. Alternatively and more simply, using Eq. (2.4.50), E[Z]

Even more simply we can make use of the easily verified linearity property of expectation

For example, in this special case,

![]()

The linearity property can be used, as in the preceeding section, to find relationships among expectations which simplify computations, or which, because they are independent of the underlying distributions, are valuable when only these expectations are known.

For example, the following relationship often simplifies covariance computation

which, using the linearity property, reduces to

Illustration: Correlated demand and capacity We illustrate the use of the linearity property in situations where moments are known, but distributions are not, by the following example. If the capacity C of an engineering system and the demand upon it D are random variables, the margin M = C – D is a measure of the performance of the system, whether it be inadequate, M < 0, or “over-designed,” M large. Even if the joint distribution of C and D is unknown, the mean and variance of M can be found from first and second moments of X and Y:

![]()

which, using the linearity property, is

The variance, on the other hand, is

Applying the linearity property to the first term and then grouping as

![]()

we recognize that

Demand and capacity may frequently be correlated. Both depend, for example, upon the average travel velocity of a highway system. Notice that if the correlation is positive, i.e., if higher than expected demand tends to occur with higher than expected capacity (as may be the case of a highway system where the better the system performs the more it is used), the variance of M is reduced from the sum of the variances. This latter value, the sum, obtains, of course, only if C and D are uncorrelated, or, in particular, if they are independent. If ρC,D = 0:

![]()

Notice that the variance of the difference between (independent) C and D is not the difference of their variances, but the sum. The uncertainty in both variables “contributes” to the dispersion in their difference.

Even though their joint distribution is not known, the second-order moments of C and D are sufficient to obtain a lower bound on the system reliability, the probability that the capacity exceeds the demand. Clearly

![]()

The probability of “failure” of the system, P[M < 0], has an upper bound given by the Chebyshev inequality [Eq. (2.4.11)] as

Hence the system reliability is at least 1 – VM2 where VM, the coefficient of variation of M, is

For example, a highway engineer, who estimates that the demand on his system 10 years hence will have a mean 1200 vehicles per hour (vph) and a standard deviation of 400 vph, might consider a design with an expected capacity of 2200 vph and standard deviation 300 vph. Assume that the correlation coefficient in such situations has been measured to be +10 percent; then

The likelihood that the capacity will exceed the demand is at least

It is assumed here that the engineer knows the moments exactly. If they are the result of estimates from small samples, there arises another order of uncertainty, that is, statistical uncertainty (Chap. 4).

Moments of linear functions The linearity property, Eq. (2.4.71), can also be employed to derive some general results for the very important case when a linear relationship among two or more jointly distributed random variables is involved. Interest lies in the variable Y, where

The expectation of Y is

The result is valid whether or not the Xi are independent. In words, the equation states that “the mean of the sum is the sum of the means.”

An analogous statement does not hold for variances unless the random variables are all uncorrelated. In general,† by carrying out the now familiar steps, we can show that

which reduces for uncorrelated random variables to, simply,

The special case for n = 2 is worth displaying if only because it appears so frequently in practice. If Z = aX + bY, then, according to the previous equation,

This equation can be verified in a manner parallel to the technique used in determining the variance of M = C – D. In fact, notice that that illustration was a special case of the result above with a = 1 and b = – 1.

Illustration: Total capacity of a system of components Some of the implications of Eq. (2.4.82) are best understood by example. Consider the relative variability and hence relative reliability of two contending systems: the first consists of two elements, the sum of whose capacities or strengths, X and Y, determines the capacity of the system; the second consists of a single element of capacity Z. A simple example is the situation where two smaller bars of ductile steel or one larger bar will be used to provide the tensile capacity of a reinforced concrete beam. Other examples include simple pipe or transportation networks. Assume that mean system capacities are, by design, equal (that is, E[Z] = E[X] + E[Y] = m) and that the mean small-element capacities are equal (E[X] = E[Y] = ½m). How do the dispersions in the two systems’ capacities compare if the coefficients of variation of X, Y, and Z are equal †? In the latter case,

while in the case of the two-element system,

Notice that if X and Y are perfectly positively correlated, ρ = 1, the variability of the system capacity is equal to that in the one element case. But under any other conditions, the two- (parallel-) element system has less variance and generally higher reliability than the system with one larger element. In particular, if X and Y are independent, the variance of X + Y is ½ of that of Z. (There is evidence that two bars from the same batch of steel may have a ρ as large as 98 percent.)

Moments of a product The general properties of expectation in one final common case deserve mention, for it is one of the few functions outside of the linear ones considered above which lends itself to such simple treatment. If Z = XY, then, from Eq. (2.4.72),

If and only if the variables are uncorrelated, the expectation of the product is the product of the expectations

If X and Y are independent, expansion will show that

and that

Illustration: Correlation versus functional dependence The correlation coefficient alone is frequently used to make deductions about the joint behavior of random variables. In many fields, particularly the biological and social sciences, where basic laws are difficult to derive otherwise, it is common to measure repeatedly two variables which are suspected or hypothesized to be related and then to estimate † their correlation coefficient. If the coefficient is near unity in absolute value, strong dependence is assumed verified; if the coefficient is low, it is concluded that one variable has little or no effect on the other.

Such techniques of verification or determination of suspected relationships are becoming more and more common in civil engineering, where many of our common materials—e.g., concrete and soil—and many of our systems—e.g., watersheds and traffic—are so complex that relationships among variables can only be determined empirically. To use such an approach correctly, it is necessary to have a sound understanding of its implications and its potential errors. The following extended illustration is designed both as an exercise in using expectation operations and as an aid to understanding the effects on the correlation coefficient caused by such factors as the character of the functional relationship and the presence of other causes of variation. It is important to appreciate the fact that the conclusions deduced from this study do not depend on the shape of the joint probability distribution. This fact demonstrates the power and generality of working with means, variances, and correlations, without detailed probability law specifications.

Suppose that an engineer is investigating the possible relationship between density of a particular highway subbase material and the road’s performance. In each of a number of segments of a road of nominally uniform design, he measures both the density of the subbase material (found in a core drilled through the pavement) and the value of some index of the segment’s performance, namely, the smoothness of the ride provided to passing vehicles. ‡ Let the random variable Y be the “ridability” or performance index and let X be the deviation of the subbase density from the specified (say, the mean) density. §

The engineer could estimate from the data the correlation coefficient, ρX,Y. Generally, a low value of this coefficient would lead him to conclude that performance (ridability) is virtually independent of subbase density. A relatively high value of ρX,Y, on the other hand, would normally cause the conclusion that subbase density strongly affects performance (and hence, perhaps, must be well controlled in future jobs, if high performance is to be obtained).

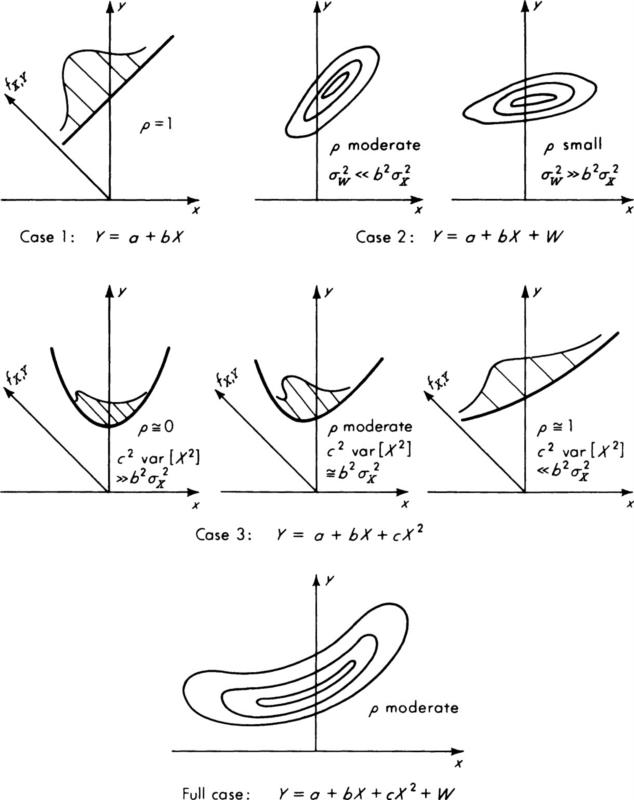

In order to understand the general validity of such conclusions, we want to presume that, in fact, a physical law or function (unknown to the engineer, of course) governs the relationship between performance Y and subbase density X. The law we shall assume is of the form

in which a, b, and c are constants and in which W is a random variable with mean zero, stochastically independent of X, and W represents the variation in Y attributable to factors other than the subbase density X. These might include such factors as settlement of the soil fill below the subbase or variations in pavement placement. Assuming the average effect of these factors is accounted for in the constant a, W need only represent the effect on Y of the random variations about the mean values of these factors. Thus the mean zero assumption is reasonable.

Calculation of the Correlation Coefficient First, as an exercise in dealing with expectation we seek the correlation coefficient ρX,Y given that Eq. (2.4.89) defines the relationship between Y, X, and the other factors. From Eq. (2.4.72),

![]()

Evaluating the first term with the use of the linearity property,

![]()

Owing to the assumed independence of W and X, E[WX] = E[W]E[X]. Since E[W] was assumed to be zero, the last term is zero. Assuming that X, the deviation from the specified subbase density, is symmetrically distributed about zero,† E[X] = 0, E[X3] = 0 and Var [X] = E[X2]. Thus

The sign of the covariance in this example depends only on the sign of b.

To find the correlation coefficient, we need the standard deviations of X and Y:

Owing to the assumptions above, many terms drop from this expression. Combining these results and grouping terms,

![]()

Simply to shorten the expression, we substitute† Var [X2] for E[X4] – E2[X2]:

Finally,

Let us concentrate on ρ 2, since it is simpler in form than ρ. Of course ρ = 0 implies ρ2 = 0 and ρ = ±1 implies ρ2 = 1; hence the same implications regarding presence or lack of dependence follow from ρ2 exactly as from ρ. Simplifying,

Note that no use has been made of integration or density functions in obtaining these results.

Values of ρ Implied by the Form of the True Law We are now prepared to use this equation to demonstrate how various conditions in the true underlying law, Eq. (2.4.89), affect the value of the correlation coefficient and hence the validity of conclusions drawn from its value. The joint density functions implied by each case are sketched in Fig. 2.4.10.

Case 1: Y = a + bX Notice first that the only way a value of ρ (or ρ2) equal to unity will be found is if b is not equal to zero but both c and σW2 are, that is, if a linear functional relationship, ‡ Y = a + bX, and hence perfect stochastic dependence, exists. Values of ρ2 less than 1 will be found in all other situations.

Case 2: Y = a + bX + W Let us look next at the case when c = 0, that is, when a linear relationship between X and Y exists, but other sources of randomness Y are present:

Then

In this case, if the variance of the other contributions to the variation in Y is relatively small, the correlation coefficient will be very nearly unity. The engineer’s conclusions, based on observing ρ ≈ 1, that strong stochastic dependence (almost a simple functional dependence) exists between X and Y would be valid. If, however, the contributions to the scatter in Y come predominantly from other factors, and/or if the functional dependence between X and Y is weak (b is small), then ![]() As a result the correlation coefficient will be very small. A conclusion (based on observing a small value of ρ) that there is no relationship between X and Y would not be valid, as a linear relationship does exist. But ρ does remain a good indicator of the stochastic dependence between X and Y, for this will be small too; the conditional distribution of Y given X = x will have variance σw2, very nearly as large as that of marginal distribution of Y, which is b2σX2 + σw2. In this case the random variation W, which is the result of other factors, masks the linear Y verses X relationship. The implication for field practice and betterment of performance is simply that, even though there may be a functional relationship between performance and subbase density, it is so weak or the variance of subbase density is so small that, compared with the influence of the other factors, the deviations in subbase density contribute little to the variations in performance. Hence the conclusion, based on observation of a small value of ρ2, that for nominally similar designs (i.e., same mean density) there is little effect of subgrade density on performance may be a valid one operationally.

As a result the correlation coefficient will be very small. A conclusion (based on observing a small value of ρ) that there is no relationship between X and Y would not be valid, as a linear relationship does exist. But ρ does remain a good indicator of the stochastic dependence between X and Y, for this will be small too; the conditional distribution of Y given X = x will have variance σw2, very nearly as large as that of marginal distribution of Y, which is b2σX2 + σw2. In this case the random variation W, which is the result of other factors, masks the linear Y verses X relationship. The implication for field practice and betterment of performance is simply that, even though there may be a functional relationship between performance and subbase density, it is so weak or the variance of subbase density is so small that, compared with the influence of the other factors, the deviations in subbase density contribute little to the variations in performance. Hence the conclusion, based on observation of a small value of ρ2, that for nominally similar designs (i.e., same mean density) there is little effect of subgrade density on performance may be a valid one operationally.

Fig. 2.4.10 Joint density-function contours fX,Y(x,y) for various cases of a physical law governing Y and X. In cases 1 and 3, the PDF’s degenerate into “walls” which are only suggested graphically.

Case 3: Y = a + bX + cX2 Next we look at another limiting case, namely when σw2 = 0, that is, when the variation in other factors is negligible or at least has negligible effect upon performance. Now a functional relationship between X and Y exists:

and so does perfect stochastic dependence; i.e., the conditional distribution of Y given X = x is a spike of unit mass at the value a + bx + cx2. But the correlation coefficient may well prove misleading:

If the squared term dominates over the linear one, that is, if ![]() the correlation coefficient will be small even though dependence is perfect. In this situation an engineer’s conclusion, based on an observed small value of ρ2, that subgrade density does not significantly affect performance, would be incorrect. Subsequent action based on neglecting the existing dependence could lead to relaxing of quality control standards on subgrade construction and consequent deterioration in performance (assuming b and c are negative). In this case a plot of the data points will usually exhibit the strong functional relationship which the correlation coefficient fails to suggest. Note, on the other hand, that if the linear term predominates, i.e., if

the correlation coefficient will be small even though dependence is perfect. In this situation an engineer’s conclusion, based on an observed small value of ρ2, that subgrade density does not significantly affect performance, would be incorrect. Subsequent action based on neglecting the existing dependence could lead to relaxing of quality control standards on subgrade construction and consequent deterioration in performance (assuming b and c are negative). In this case a plot of the data points will usually exhibit the strong functional relationship which the correlation coefficient fails to suggest. Note, on the other hand, that if the linear term predominates, i.e., if ![]() , the correlation will be high (but never unity) and will properly indicate strong dependence. This illustrates why it was stated that the correlation coefficient should properly be called a measure of linear dependence.† It must be pointed out that these last conclusions from the illustration depend on the assumption that E[X3] =0.† If this condition does not hold, the correlation coefficient is generally enhanced as a measure of dependence. No matter what the relative values of c and b, if additional sources of variation W also exist, they will tend to decrease ρ2 [Eq. (2.4.94)] and mask further the functional relationship between X and Y.

, the correlation will be high (but never unity) and will properly indicate strong dependence. This illustrates why it was stated that the correlation coefficient should properly be called a measure of linear dependence.† It must be pointed out that these last conclusions from the illustration depend on the assumption that E[X3] =0.† If this condition does not hold, the correlation coefficient is generally enhanced as a measure of dependence. No matter what the relative values of c and b, if additional sources of variation W also exist, they will tend to decrease ρ2 [Eq. (2.4.94)] and mask further the functional relationship between X and Y.

Spurious Correlation It is important, too, to point out another potential source of misinterpretation associated with the use of correlation studies. The discussion above revealed that small correlation does not necessarily imply weak dependence, and it is also true that spurious correlation may invite unwarranted conclusions of a cause and effect relationship between variables when, in fact, none exists. In the example here, for instance, some other variable factor, such as moisture content of the soil or volume of heavy trucks, might cause variation in both subbase density and performance. Hence higher-than-average values of density might, in fact, usually be paired with higher-than-average performance (and low with low), yielding a positive correlation that is not a result of subbase density’s beneficial effect on performance but is rather a result of both factors being increased (or decreased) by presence of the high (or low) value of the third factor. This fact does not, however, reduce the value of using an observation of one variable to help predict the other, as long as the factor causing the correlation is not altered.

Benson [1965] reported on spurious correlation and on its potential and actual presence in many civil-engineering investigations, even those which are deterministic rather than probabilistic in formulation. He cites as a particularly common source of spurious correlation that introduced by the engineer who seeks to normalize his data by dividing it by a factor which is itself a random variable. For example, correlation between X, accidents, and Y, out-of-town drivers, is not necessarily implied by correlation (observed in a number of cities) between X/Z, the number of accidents per registered vehicle, and Y/Z, the number of commuters per registered vehicle. Formally, X and Y may be independent, but X/Z and Y/Z are not, and high correlation between the latter pair does not imply correlation between the former pair. Similarly, correlation between live load per square foot and cost per square foot in structures need not imply that cost and load are dependent, because both may depend upon the normalizing factor, that is, total floor area.

Summary The correlation coefficient provides a very useful measure of dependence between variables, but the engineer must be careful in its interpretation. Large values of p2 imply strong stochastic dependence and a near-linear functional relationship, but not necessarily a cause-and-effect relationship. Small values may result from the predominance of other sources of variation (and hence low stochastic dependence), or, if a functional relationship exists, from its lack of strong linearity.

Conditional expectation and prediction† As with single random variables there is often advantage in working with expected values conditioned on some event A. In general we have

![]()

in which fX,Y|[A](x,y) is the joint conditional distribution of X and Y given the event A [for example, Eq. (2.2.58)].

The single most important application of conditional expectation is in prediction. If Y is a maximum stream flow or the peak afternoon traffic demand on a bridge, the engineer may be asked to “predict what Y will be.” To “predict Y” is to state a single number, which, in some sense, is the best prediction of what value the random variable Y will take on. Without additional information, the (marginal) mean of Y, or mY, is conventionally used to predict Y. Intuitively it is a reasonable choice. More formally it is the predictor of Y which has a minimum expected squared error (or “mean square error”). The error in predicting Y by mY is simply Y – mY. Its expected square is

![]()

or the (marginal) variance of Y. No other predictor will give a smaller mean square error. † It should be emphasized that the mean square error criterion for evaluating a predictor is simply a mathematically convenient engineering convention. More generally the engineer should use a predictor which minimizes the expected cost, the cost being some function of the error. If this cost is approximately proportional to the square of the error, whether positive or negative, then the mean square error criterion is also a minimum expected cost criterion and the mean is the best predictor. If, on the other hand, there are larger costs associated with underestimating Y than with overestimating it, the minimum cost predictor will be greater than the mean. Such economic questions are more properly treated in Chaps. 5 and 6; we restrict attention here to the conventional mean square error criterion.

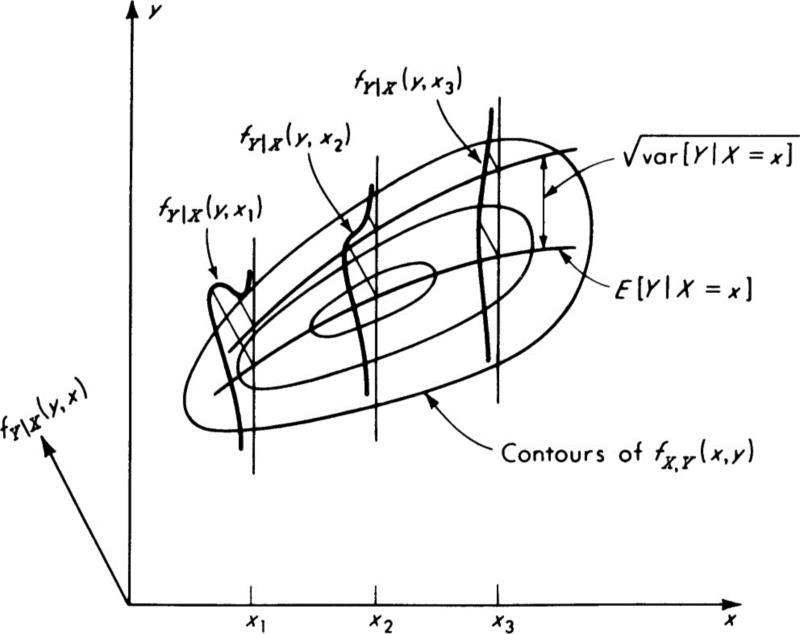

Suppose now that the engineer learns that another random variable X has been observed to be some particular value, say x. The hydraulic engineer may have learned the maximum flow in a neighboring river or at an upstream point, or the traffic engineer may have learned that the morning peak flow was x = 1000 cars per hour. Conditional on this new information, what value should the engineer use to predict Y? Applying the same argument used above to the conditional distribution of Y given that X = x, one concludes that the “best” predictor of F is the conditional mean, or mY|X.

![]()

Fig. 2.4.11 Illustration of conditional means and variances of Y given X.

Note that in general this conditional mean † depends on the value x. This predictor has a mean square error equal to the conditional variance of Y given X = x:

This variance is also a function of x, in general. These relationships are sketched in Fig. 2.4.11, where the square root of the mean square error (or rms) is indicated rather than the mean square error itself.

In Sec. 3.6.2 we will discuss in detail an illustration of conditional prediction applied to a particular, commonly adopted, joint distribution of X and Y. In that case we will find, upon carrying out the integrations indicated above, that

and that

We note in this special application that the predictor mY|X is linear in x and that the mean square error is a constant, independent of x. The importance, once again, of the correlation coefficient ρ is observed. For this particular joint distribution, † given X = x, the amount the conditional predictor mY|X will be altered from the (marginal) predictor mY is directly proportional to ρ. Also, the uncertainty in predicting Y given X = x (as measured by the mean square error or conditional variance) is smaller than the marginal uncertainty σY2 by an amount proportional to the square of ρ.

Illustration: Sum of a random number of random variables Conditional expectation is also valuable when studying probability models. Often moments of important variables may be difficult to determine unless one takes advantage of conditional arguments.

For example, recall that in Sec. 2.3.3 we assumed that T, the total rainfall on a watershed, was the sum of the (independent, identically distributed) random rainfalls, R1, R2, . . ., in N “rainy” weeks, where the number of rainy weeks is itself random (and independent of the Ri’s):

The estimation of the distribution of T by simulation was found to be a long numerical task. In addition, it required complete knowledge of the distribution of N and Ri. Having knowledge only of the means and variances of N and Ri, it would be desirable to be able to calculate explicitly the mean and variance of T. They are

and

The randomness in N makes a direct attack on this problem troublesome. But, given the number of rainy weeks (that is, conditional on N = n), we can apply familiar formulas [Eqs. (2.4.81a) and (2.4.81b)] for the sum of a known number of (independent) random variables:

and

in which σR2 and mR are the variance and mean of any Ri. The subscript R on the expectation symbol is simply a reminder that this expectation is with respect to the R’s. Now, recognizing that N is in fact random, we have two simple functions of the random variable N:

![]()

To find E[T] and E[T2], we need simply take expectation of g1(N) and g2(N) with respect to N:

and

![]()

This implies

In words, the expected value of the sum of a random number of random variables is just the mean number times the mean of each variable. The variance of the sum is, however, larger than the mean number times the variance of each variable (as it would be if N were not random but known to equal its mean). The additional term is just the variance of the mean of each variable times N; that is,

In short,